Types of exchanges

Exchange trading is the process of concluding transactions on an exchange according to established rules, where the objects are commodities, securities, currency pairs and other financial and derivative financial instruments.

Depending on the subject of trade, there are 3 types of exchanges:

- Commodity.

- Stock.

- Currency.

In the first case, we are talking about transactions of purchase and sale of goods. Exchange trading can be carried out on the basis of a qualitative description of the product, even in its absence.

Such products are homogeneous and standardized. These include: grain crops, meat and livestock, various metals, industrial raw materials, etc. The main functions of a commodity exchange:

- organization of trade exchange on mutually beneficial terms;

- identifying real demand and supply for goods;

- ensuring the execution of transactions;

- providing information to interested parties.

Transactions with securities

are carried out on the stock exchange It makes it possible to obtain additional funds for the development of production, the implementation of government programs, etc. Here are the main functions of the stock exchange:

- organization of tenders;

- preparation and implementation of contracts;

- quotation of exchange prices;

- guarantee of execution of transactions;

- Information Support.

On the foreign exchange exchange, currencies are purchased and sold in accordance with their quotes. Its main function is to set the market rate of national and foreign currencies.

Based on the type of transactions, the following types of exchanges are distinguished:

- real goods - after the transaction, mandatory delivery is carried out;

- futures, where a future is an obligation to purchase in the future a certain product in a given quantity at a set price. The buyer can resell the contract or fulfill it;

Who can take part in exchange trading

The main participants in exchange trading are:

- Dealers. For purchases and sales they use personal financial resources and carry out trade without intermediaries.

Brokers. Participate in auctions at the request of clients for a fee in the form of commissions.- Specialists. They engage in analytical activities and conduct consultations.

- Brokers. They play on the stock exchange.

- Organizers of the auction. Responsible for ensuring the progress of the trading process.

- Heads of the exchange. Monitor compliance with current legislation and implementation of market rules.

- Exchange staff. Responsible for technical support of trading activities.

Dealers have considerable influence on market liquidity. They publicly declare prices for assets, and then are obliged to execute transactions at the stated prices.

Brokers conduct trades in a separate section. They have assistants whose duties are to record the conclusion of transactions.

With the exception of the main participants, one-time and regular visitors can make transactions on open exchanges.

One-time visitors, which are understood as representatives of legal entities (employees of institutions) and individuals (individual entrepreneurs), can make transactions only on their own behalf and at their own expense.

Regular visitors include brokerage companies, as well as independent brokers providing intermediary services in the market.

They are not included in the number of participants forming the authorized capital. Such visitors use the services of the market for a fee paid for the right to take part in trading.

On closed exchanges, only its members and their representatives can make transactions.

Stock Exchange Specialists

Important participants in exchange trading involved in providing liquidity. One person is responsible for 1 issue of shares and is obliged to maintain stable liquidity of the issue assigned to him.

Specialists also keep a book of applications. There are limited ones that are executed immediately. All marked applications are executed in order of priority.

Brokers as participants in stock exchanges

These are legal entities or individuals who enter into transactions on behalf of customers and at their expense. The broker must be the link between the client and the exchange.

Brokers and brokerage companies operate under a license and must meet the following requirements:

- the presence in the headquarters of employees who have confirmed their qualifications and knowledge with a certificate;

- ownership of own capital necessary for financial liability to investors;

- availability of a developed accounting and reporting system.

Stock brokers are not associated with one company; they can work with any of the brokerage firms. For this, brokers receive interest paid by the client for services.

The broker has the right:

- purchase or sell an exchange commodity, guided by the wishes of the customer;

- change the price and quantity of goods intended for sale;

- operate with information about goods put up for auction;

- use the services provided by the exchange.

The broker receives an application from the client to sell or purchase securities and places it on the market. When the broker finds a counter order, the transaction is considered successful. In the event that a counterparty is not found, the transaction is recorded by a specialist and made available to all trading participants.

Commission Brokers Mission

The main function of commission brokers is to mediate between the trader and the exchange during the execution of client requests from brokerage firms. Brokers provide market participants with access to the market. Brokers charge commissions for intermediary activities, the amount of which varies depending on the volume of the transaction.

Functions

There are four functions of the exchange:

- organization of tenders;

- contract development;

- publication of prices (quotations);

- guaranteeing the execution of transactions.

Organizing trading (the first function) is impossible without performing the function of informing trading participants.

She also undertakes the obligation to resolve conflict situations (arbitration) that may arise in the process of making and executing transactions.

The role of stock trading in the modern world economy

The role of commodity exchanges in the global economy of the twentieth century was controversial. Along with the steady decline in the role of commodity exchanges as a form of wholesale trade, their importance as centers of financial transactions increased sharply.

The changes that took place in the position of commodity exchanges concerned the following aspects of their activities:

· the range of goods and markets that are the subject of transactions,

volume of transactions and number of commodity exchanges,

· type of transactions,

· organization of trade and accounting of exchange transactions.

Exchange-traded goods include goods sold in whole or in part through exchanges. As noted earlier, the objects of exchange trading are goods that have such properties as homogeneity, interchangeability, and the possibility of establishing a quality standard. In addition, for quite a long time it was believed that perishable goods could not be exchange-traded, but the modern scientific and technological revolution has made it possible to introduce a number of types of perishable products into exchange circulation. [4, 62]

Pricing practices have a great influence on the formation of the exchange market for a particular product. Goods with a low degree of monopolization of production or consumption have a greater chance of remaining the subject of exchange trading for a long time. At the same time, the existence of exchange trade in highly monopolized goods is also possible, if there is a stable share of free trade and non-monopoly participants - sellers or buyers. An example of this is the oil and petroleum products market.

Overall, the number of goods traded on commodity exchanges has declined significantly over the past century. At the end of the 19th century, there were more than 200 types of exchange goods. Large groups of exchange commodities in the past were ferrous metals, coal and a number of other goods with which transactions are no longer carried out today.

By the middle of the twentieth century, the number of exchange-traded goods had decreased to about fifty and since then the number has remained approximately constant. At the same time, the number of futures markets was steadily expanding. The futures market is understood as a market for a certain quality of a certain commodity, so there can be several markets for one commodity.

The range of exchange goods traditionally consisted of two main groups - agricultural products and industrial raw materials and semi-finished products.

The group of industrial raw materials and semi-finished products includes energy resources (oil, gasoline, fuel oil, diesel fuel), precious metals (gold, silver, platinum, palladium) and non-ferrous metals (copper, aluminum, zinc, lead, nickel, tin).

The number of commodities in the agriculture and forestry group has been steadily declining. This group includes oilseeds (seeds, meal, and oils), grains (wheat, corn, barley, rye, oats), livestock products (live cattle and pigs, meat, hams, etc.), food products (sugar, coffee, cocoa beans), textile products (cotton, wool, silk, yarn). natural rubber and lumber. Other items include potatoes and frozen orange juice concentrate.

The structure of exchange goods is influenced by a number of factors, including scientific and technological progress. Thanks to him, many substitutes for some exchange-traded goods of artificial or synthetic origin have appeared. The competition between these goods contributes to the stabilization of prices, which means a decrease in exchange turnover. This is clearly seen in the example of the wool market, where the volume of transactions has decreased significantly in recent decades, and on many leading exchanges trading in wool has ceased altogether.

At the same time, scientific and technological progress has contributed to the improvement of methods for determining the quality of goods, using the latest technical means for these purposes. As a result, the ability to achieve stable quality made it possible to expand the range of exchange-traded goods to include some lumber and precious metals that were previously unavailable to exchange trading under standard contracts.

On modern commodity exchanges, a new group of trading objects has appeared that are not tangible goods and have received the general name of financial instruments. Transactions are carried out on trading price indices, bank interest, mortgages, currencies, charter contracts, and government securities. These operations began to be practiced on commodity exchanges around the 70s.

The development and growth of financial futures markets was influenced by changes in the global economy in the 1970s, when fixed exchange rates between the US dollar and Western European currencies began to fluctuate. Exchange rates floated not only due to the volatility of monetary exchange rates, but also due to fluctuations in the rates of other financial instruments, such as bonds and treasury notes. This reason, together with the sudden increase in US government debt, influenced the relatively stable interest rates, which led to the establishment of more fluctuating, unstable rates.

To meet the demands of the times, the world's leading exchanges, and most notably the Chicago Board of Trade, have extended futures contracts to financial instruments, thereby enabling financial institutions to cope with price risks. The first futures contracts on financial instruments were concluded on certificates of collateral of the Government National Collateral Association (USA) and on foreign currencies in the 70s. The certificates were the result of a joint effort between the Chicago Exchange and entrepreneurs active in the collateral business. The contracts took several years of intensive work to develop, and trading of these contracts began in October 1975.[6,99]

Since the introduction of the first financial futures, trading in futures on financial instruments has expanded to cover more and more types of different financial instruments, including long-term Treasury bills and Treasury notes, stock futures, municipal bond futures, and "swaps" futures (the purchase of foreign currency in exchange for domestic currency). subsequent repurchase).

As a result, a very diverse product range of exchange operations has now emerged, which is in constant development. Thus, it is estimated that approximately 70% of the number of contracts traded on US exchanges were approved over the past 10-15 years.

Commodity futures contracts played a leading role on exchanges until the end of the 70s. Gradually, their share decreased, while the share of financial futures increased sharply. Currently, they account for 3/5 of the total number of transactions on futures exchanges.

Among commodity futures and options contracts, fuel commodities, precious and non-ferrous metals now occupy a significant place. The volume of trading in futures for agricultural commodities, especially coffee, cocoa, cotton, and sugar, is significantly less.

Thus, international exchange trading has a pronounced geographical concentration. The leading centers were and remain the USA, Great Britain and Japan. The specialization of American commodity exchanges has traditionally been agricultural products, the UK - precious and non-ferrous metals and energy, and the Japanese - agricultural products, although now this specialization in all three centers is not so pronounced.

Mission

Exchange trading, as the basis of exchange activity, facilitates the process of buying and selling, and also protects the interests of sellers and buyers from losses that may arise in the event of price fluctuations or fraudulent activities.

Today, the trading process has become much easier, since transactions can be concluded using the Internet.

But in order for trading to be successful and profitable, a thorough study of all mechanisms, terms, and concepts is necessary. A classic textbook is the work of Alexander Elder “Fundamentals of Exchange Trading”. We invite you to watch the interview with the author in the video.

Bidders

According to the main purpose of the exchange, it serves as a link between sellers and buyers. They are the main participants in the auction. They can be both individuals and individual companies. There are two types of markets:

- primary;

- secondary.

Only issued shares are placed on the primary one in order to attract investments into the issuing company. In this case, it is the issuer (legal entity) who acts as the seller. Buyers can be any investors in a public offering of securities, as well as a certain circle of investors if the placement is private.

At the secondary stage, securities are freely circulated between market participants, and the issuer can already act as both a buyer (for example, buy back his shares) and as a seller: sell the purchased shares. It is in the secondary market that the main turnover occurs, where traders make money by buying and selling securities due to fluctuations in market value.

Exchange functions

- organization of exchange trading;

- regulation of trade through established rules and standards;

- development of standard forms of standard contracts;

- quotation, i.e. establishing the price of a product that is announced by the seller or buyer and at which they are ready to make a transaction;

- dispute resolution;

- information activities;

- provision of guarantees for the fulfillment of obligations by trading participants.

100 rubles discount on your first order!

Promotion for new clients! Place an order or make a cost estimate and receive 100 rubles. The money will be credited to your account in your personal account.More details Guarantees Reviews

Activity

If you look at the situation globally, the division of functionality among market participants is aimed at:

- To increase capitalization indicators.

- Improving the qualifications of exchange participants.

- Tightening control over compliance with rules.

- Development of a system of self-regulation of trading.

- Increased competence of domestic participants to enter foreign trading platforms.

Types of activities in the securities market

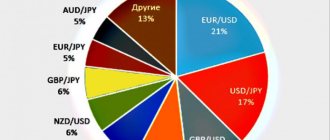

Plus, the distribution of options is necessary for a visual presentation of the strengths and weaknesses of Russian exchange trading.