Investments

21.08.2020

18468

Author: Igor Smirnov

Photo: pixabay.com

There is always interest in short-term investments. Because there are much more people and companies who have temporarily available funds than those who are ready to invest for a long time. There are many options for short-term investments, they are very different from each other, and it is difficult to identify any common features other than the investment period. But there are still general trends.

Last news:

How much can you earn from investments? A $60 million portfolio manager explains

“You can’t fix people,” I thought, and invested.” A shareholder of a sparkling wine factory told how much he managed to earn

Short-term investments: what is it?

Short-term investments are usually called the placement of free funds in various assets for a period of up to one year. They allow you to receive passive income and protect your savings from inflation risks.

A classic example of short-term investment is a bank deposit. Suppose you are thinking of getting a guaranteed income from your hard earned money as soon as possible. At the same time, you are not burdened with the invaluable experience of a financial guru. In this case, placing money at a bank interest rate will become a quickly recouped investment, although not extremely profitable.

Short-term investments have a number of advantages.

Firstly, the low entry threshold allows you to attract the smallest amounts. Secondly, you can purchase several assets at the same time, that is, diversify your portfolio and possible risks. Thirdly, if desired, they can be bought and quickly sold. And finally, short-term investments allow you to gain growth in a relatively short period of time.

Short-term investments are widespread among individual entrepreneurs and small businesses. Large companies also give short-term money, because it allows them to meet their urgent financial obligations.

Financial risks and returns

By placing money for a short period, the investor expects impressive profits. Consultants, analysts, and authorities in the financial world often promise a big jackpot. Indeed, the potential for short-term investments is great for experienced traders.

A novice investor with no experience in speculation should count on a modest income if the outcome is favorable. According to the law of the financial market, the higher the profitability, the greater the burden of risk. To minimize possible losses, it is better to include highly reliable assets in your portfolio.

The most reliable transactions are with securities and precious metals, bank deposits and mutual funds.

It’s better not to think about HYIPs and pamm accounts - this is roulette, not subject to financial logic and market laws. The probability of success of such short-term “investments” is comparable to the possibility of winning in a casino or lottery.

Advantages and disadvantages

Short-term investments have their advantages, which increase the attractiveness of this method of generating income. There are also disadvantages that force investors to choose long-term investing. Advantages and disadvantages of short-term investments:

| Advantages | Flaws |

| Low entry threshold. There are methods that require a minimum amount of starting capital from 5 tr. | High degree of risks that must be predicted in order to make a profit |

| Wide range of ways to multiply your investment | Low level of profitability with relative safety of the schemes |

| High liquidity of assets. All methods (except bank deposits) are quickly repaid | In order to successfully place capital, you need to have special knowledge |

| Quick profit. You can receive income within a day | |

| You can invest in several assets at the same time. This is beneficial for diversifying the investor’s portfolio and reduces the level of risk | There is a strong dependence on the political situation in the state |

| It is an excellent source of profit during periods of financial and economic instability, when investors stop trusting long-term projects |

Types of short-term investments

You can invest money for a short period of time in real values and financial assets.

In the first case, we are talking about the purchase of precious metals, real estate, and franchises. Metal assets are reliable. They generally outpace inflation, but are taxed if purchased in physical form (bullion).

Real estate brings a stable income, but is not very liquid and requires large overhead costs. The value of a franchise as an investment is determined by the expected future income.

Short-term investment in financial assets represents the placement of funds on deposits, transactions with currencies, and securities. Savings instruments must be in the arsenal of a novice investor: there are many options, the risk is minimal, and a small income is guaranteed.

By purchasing currency, you can make money by placing it on deposit, through speculation, or by purchasing Eurobonds. Foreign exchange assets are highly liquid, their profitability is directly proportional to the investor’s experience.

Successful transactions in the stock market can bring consistently high income. Stocks allow the owner to receive dividends, bonds - coupon payments.

Popular types of investing on the Internet

Forex allows you to make money on exchange rate differences around the clock and without intermediaries. The profitability here is potentially high, provided you understand trends, technical and fundamental analysis. The investor will be helped by demo accounts, webinars, analyst opinions and his own intuition.

PAMM accounts are an option for those who do not plan to independently enter the financial market. The assets are transferred to the trader for trust management. The profit accumulated on his account is distributed among investors in proportion to their investments.

Cryptocurrencies are also in price now. The return on investment directly depends on the exchange rate of the digital currency, the method of investment, and even the power of your processor. It’s worth investing if you don’t mind the low level of trust and the risk of government sanctions.

Investments in HYIPs (highly profitable projects) are the most unpredictable. They often work on the principle of financial pyramids. The size of the profit, and more often the loss, is determined by the moment of exit.

Internet investments are very risky, but they are loved by Russians. The idea of making quick money is quite in keeping with the national character. Our people, historically seasoned by change, are not used to waiting. It’s like walking into a field of miracles when it comes to online investing. The ending is usually unprofitable, nervous and sad.

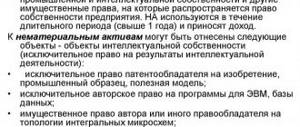

Accounting for long-term investments in the form of capital investments

Capital investments represent investments in non-current assets, including costs for new construction, expansion, reconstruction and technical re-equipment of existing organizations, purchase of machinery, equipment, tools, inventory, design and survey work, etc. Capital investment is an economic process. Like any other business process, it is reflected in accounting as a set of costs and results. Accounting primarily reflects costs incurred in the process of capital investment, i.e. costs for design, construction and reconstruction of facilities, purchase and installation of equipment, machinery, instruments, costs for the purchase of finished facilities, etc. The result of the capital investment process is new or reconstructed non-current assets.

Accounting for long-term investments is carried out on an independent synthetic account 08 “Investments in non-current assets”. This account is intended to summarize information about the organization’s costs for objects that will subsequently be accepted for accounting as non-current. Separate sub-accounts can be opened to this account for the types of these assets: “Purchase of land plots”, “Purchase of natural resources”, “Construction of fixed assets”, “Purchase of fixed assets”, “Purchase of intangible assets”, etc. By debit of the account 08 “Investments in non-current assets” reflects the actual costs of the acquisition, construction and installation of individual objects of this category of assets on an accrual basis. The balance (debit) of the account reflects the value of unfinished investments (construction). On account 08 “Investments in non-current assets”, analytical accounting is carried out for each construction or acquisition project and cost items.

Capital investments are grouped in accounting according to the technological structure of expenses, so the following grouping is usually accepted:

- construction works;

- equipment installation work;

- purchase of equipment requiring installation;

- purchase of equipment that does not require installation;

- other capital expenditures;

- expenses that do not increase the cost of fixed assets.

Construction work is carried out in the presence of title lists, design estimates and sources of financing. Title lists are a list of objects scheduled for construction or reconstruction. They provide for the start and completion dates of work, the estimated cost, the volume of capital investments by year, etc. The design and estimate documentation includes a project, drawings, a set of technical documents, a summary estimate, explanatory notes and other materials necessary for the planned construction or reconstruction of a building, structure or enterprise. Design and estimate documentation is developed on the basis of feasibility studies and technical and economic calculations.

When carrying out contract construction, the customer enters into a contract, as a rule, with the main contractor (general contractor). He is responsible to the customer for the performance of all general construction, special construction and installation work. The general contractor may involve other construction or installation organizations, which are called subcontractors, to perform the work. Subcontractors enter into contracts with the general contractor and are responsible to him for the performance of certain types of work, their timing and quality. Customers pay for work completed by contractors depending on the payment methods chosen by the parties.

Organizing the construction of facilities, monitoring its progress and maintaining accounting records of the costs incurred in this case is carried out by developers. At the same time, the accounting procedure is regulated by the Accounting Regulations “Accounting for agreements (contracts) for capital construction” (PBU 2/94) [13].

Construction refers to the individual type of production. The construction process begins with planning, which is carried out according to existing estimates for construction work, and determining the sources of their financing, and ends with the commissioning of constructed facilities. In the accounting of the developer and contractor, payments for construction projects are reflected based on their contractual value specified in the construction contract. Therefore, in construction, the custom method of accounting for costs incurred is usually used. The developer keeps track of costs on an accrual basis from the start of work until the facility is put into operation. In this case, the costs of capital construction take the form of the initial cost of the commissioned fixed assets. Until the completion of construction work, the costs of their construction, recorded on account 08 “Investments in non-current assets”, constitute unfinished capital investments.

Construction work is carried out either by contract, i.e. by specialized construction and installation organizations (contractors) on a contractual basis, or in an economic way, i.e. by the developer himself.

With the contract method, completed and executed construction and installation work is reflected by the developer on account 08 “Investments in non-current assets” at the agreed value. The cost of construction work in the developer's accounting is reflected on the basis of the act of acceptance of work performed (in form No. KS-2), which is signed by the developer and the contractor. The specified work is paid by the developer based on a certificate of the cost of work performed and expenses (according to form No. KS-3). Based on this certificate, the developer includes the cost of work performed as part of investments in non-current assets. This operation is reflected in the accounting accounts as follows:

Dt 08 “Investments in non-current assets”, 19 “Value added tax on acquired assets” Kt 60 “Settlements with suppliers and contractors”.

The decrease in debt as bills are paid is reflected:

D-t 60 “Settlements with suppliers and contractors” D-t 51 “Settlement accounts”, 52 “Currency accounts”, 55 “Special accounts in banks”.

For the contractor, all costs for performing construction work are the main activity and are accounted for on account 20 “Main production”, i.e. Based on documents for the release of materials and spare parts, payroll statements, etc., accounting entries are made:

Dt 20 “Main production” Kt 10 “Materials”, 70 “Calculations with personnel for wages”, 69 “Calculations for social insurance and security”, etc.

According to PBU 2/94, the developer identifies the financial result from the performance of its functions by determining the difference between the amount of funds included in the estimate for objects under construction in a given reporting period and the actual costs. In the case of settlements between the developer and the investor for the delivered object at the agreed value, the financial result also includes the difference between this cost and the actual costs of constructing the object, taking into account the costs of maintaining the developer. Thus, after completion of construction and delivery of the object according to the act to the customer, the following entries are made in the contractor’s accounting accounts:

Dt 62 “Settlements with buyers and customers” Kt 90 “Sales”, subaccount “Revenue”.

When writing off the actual cost of work performed by the contractor and value added tax on the work and services of the contractor:

D-t 90 “Sales”, sub-account “Cost of sales” D-t 20 “Main production”, 68 “Calculations for taxes and fees”.

Thus, on account 90 “Sales”, the contractor traditionally determines his profit or loss from the construction of a specific facility. If construction activity is not a normal activity for the customer, then the financial result is revealed in account 91 “Other income and expenses.”

In accordance with the construction contract, settlements between the developer and the contractor can be carried out: after completion of all work at the construction site; in the form of advances (interim payments) for work performed by the contractor on structural elements or stages.

As already noted, the procedure for payment for work performed by construction and installation organizations is regulated by a contract, which may provide for advance payment of costs for unfinished work. In this case, the funds transferred by the customer are reflected as advances issued, i.e. a note is made:

Dt 60 “Settlements with suppliers and contractors”, subaccount “Settlements for advances issued” Kt 51 “Settlement accounts”, 55 “Special accounts in banks”.

If there are insufficient own funds, the developer can obtain a loan from a bank to pay the contractor’s bills. The receipt of the loan is reflected:

Dt 51 “Current accounts”, 55 “Special accounts in banks” Kt 66 “Settlements for short-term loans and borrowings”, 67 “Settlements for long-term loans and borrowings”.

According to the Accounting Regulations “Accounting for loans and credits and the costs of servicing them” (PBU 15/01), when using a loan for prepayment of received property or services, interest accrued from the moment of its receipt until the receipt of the acquired property (consumption of services) is attributed to increase in accounts receivable arising in connection with the transfer of the advance. Interest accrued after receipt of property (services) is recognized as operating expenses

Interest on the loan accrued before receipt of the property (service) is reflected -

Dt 60 “Settlements with suppliers and contractors”, subaccount “Settlements for advances issued” Kt 66 “Settlements for short-term loans and borrowings”, 67 “Settlements for long-term loans and borrowings”.

Attributing accrued interest to the debit of the account for settlements with the contractor is quite understandable. If, before receiving the property, the transaction is terminated due to the fault of the contractor, then the developer, in accordance with civil law, will have the right to demand from the counterparty compensation not only for the advance amount, but also for all costs incurred, including interest accrued during this time on the loan After receiving the property ( services) and before the facility is put into operation, the accrual of interest will be reflected -

Dt 08 “Investments in non-current assets” Kt 66 “Calculations for short-term loans and borrowings”, 67 “Calculations for long-term loans and borrowings”.

The contracting organization may record advances received as revenue for stages of construction in progress. For these purposes, the contractor uses account 46 “Completed stages for work in progress.” This account summarizes information about stages of work completed in accordance with concluded contracts that have independent significance. This account, if necessary, is used by organizations performing long-term work, the initial and final deadlines for which usually relate to different reporting periods. The contractor shows the cost of the stages of work paid by the customer:

D-t 46 “Completed stages of work in progress” D-t 90 “Sales”, sub-account “Revenue”.

At the same time, the amount of costs for already completed and accepted stages of work is written off.

Dt 90 “Sales”, subaccount “Cost of sales” Kt 20 “Main production”.

Amounts of funds received from customers in payment for accepted stages are reflected:

D-t 51 “Current accounts”, 55 “Special accounts in banks” K-t 62 “Settlements with buyers and customers”.

Upon completion of all stages of work, the total cost of stages paid by the customer is written off:

Dt 62 “Settlements with buyers and customers” Kt 46 “Completed stages of work in progress”

The cost of fully completed work, recorded on account 62 “Settlements with buyers and customers”, is repaid from previously received advances and amounts received from the customer in the final settlement.

At the same time, the customer accepts (consents to pay) the contractors’ invoices for the completed stages of construction work in accordance with the acceptance certificate for the work performed:

D-t 08 “Investments in non-current assets”, sub-account “Construction of fixed assets” K-t 60 “Settlements with suppliers and contractors”, sub-account “Settlements for advances issued”.

Under the terms of the contract, the customer can supply the contractor with equipment that is to be installed at facilities under construction, i.e. requires installation. To account for incoming equipment, an independent synthetic account 07 “Equipment for installation” is opened in the customer’s accounting records. The debit of this account reflects the costs of equipment that arrived at the organization's warehouse and requires installation. These costs consist of the cost of equipment on suppliers' accounts (according to purchase prices), transportation costs for the delivery of equipment, procurement costs (including commissions to intermediary firms), the cost of commodity services exchanges, customs duties, etc.

The purchase of equipment for installation is reflected in the customer’s accounting accounts by the following entry:

Dt 07 “Equipment for installation” Kt 60 “Settlements with suppliers and contractors”

But the acquisition of equipment and its receipt in the warehouse does not yet mean capital investments in the full sense of the word. During installation, the equipment is transferred to the contractor according to the equipment acceptance certificate for installation. Only after its actual transfer to the contractor for installation is an accounting entry made in the accounts:

D-t 08 “Investments in non-current assets” D-t 07 “Equipment for installation”.

The contractor, who received equipment from the customer for use in the construction of the facility, accounts for such equipment in off-balance sheet account 005 “Equipment accepted for installation.” When receiving equipment that requires installation, the contractor makes a simple entry: D-t 005 “Equipment accepted for installation”, and when installing equipment in a facility under construction: K-t 005 “Equipment accepted for installation”. The customer accepts the installed equipment according to the work completion certificate. The act shows only the cost of installation and commissioning work performed, without the cost of equipment.

If the contractor provides the construction with the necessary equipment, then its cost is reflected by the customer on account 08 “Investments in non-current assets” along with the cost of installation and other work (according to the invoice).

When carrying out construction and installation work on an economic basis, costs are accounted for in account 08 “Investments in non-current assets”. This account reflects the actual costs incurred by the developer:

Dt 08 “Investments in non-current assets” Kt 10 “Materials”, 70 “Settlements with personnel for wages”, 69 “Calculations for social insurance and security”, etc.

If organizations have independent structural divisions that carry out construction and installation work, then they account for their costs in account 23 “Auxiliary production”:

D-t 23 “Auxiliary production” K-t 10 “Materials”, 70 “Calculations with personnel for wages”, 69 “Calculations for social insurance and security”, etc.

Upon completion of this work, the costs are written off:

D-t 08 “Investments in non-current assets” K-t 23 “Auxiliary production”.

The commissioning of fixed assets is reflected in the accounting accounts:

D-t 01 “Fixed assets” D-t 08 “Investments in non-current assets”.

The acquisition of fixed assets and intangible assets is considered in Accounting for the receipt of fixed assets and Accounting for the receipt of intangible assets, respectively.

One of the main tasks of accounting for capital investments is to determine the entire set of costs related to the constructed construction project, its reconstruction or acquisition. These costs upon completion of the work will determine the inventory (initial) cost of the objects put into operation - buildings, structures, equipment, etc.

The inventory cost of commissioned facilities consists of the costs of construction and other capital work. The inventory value of completed construction, reconstruction, and acquisition is determined. Special commissions are created to check the suitability of the facility for operation. Full readiness for operation is confirmed by the acceptance certificate of the object. It indicates the volume, production capacity, area, parameters characterizing the object, its readiness for operation, the quality of the work performed, the presence of deficiencies, and the timing of their elimination. A fully completed and signed act is transferred to the customer-developer and is the basis for determining the inventory value of the capital investment object.

When carrying out capital construction, the organization incurs costs that are not directly related to the construction of the facility, but without them it cannot be built. They are defined as costs that do not increase the inventory value of objects. Costs that do not increase the value of fixed assets are recorded on account 08 “Investments in non-current assets” separately from construction costs. Such costs can be divided into costs provided for in estimates and calculations, and costs not provided for by them.

The first group includes: costs for training operational personnel for the main activities of enterprises under construction; costs of reimbursing the cost of buildings and plantings demolished during the allocation of land for construction; funds transferred for the construction of objects in the form of shared participation during the subsequent transfer of constructed objects, etc.

The second group includes costs: to pay interest on bank loans in excess of the discount rates established by the Central Bank of the Russian Federation; for conservation of construction; for demolition, dismantling and protection of objects stopped by construction, etc.

Short-term investing methods

The financial market provides ample opportunities for short-term investments. There are many ways to invest short-term in a particular asset.

For example, for currency there are exchange offices, Forex, foreign currency deposits, conversion on Internet accounts.

You can invest in securities yourself, at your own peril and risk, or you can transfer them to short-term trust management. Investments in precious metals involve the purchase of bars, coins, unallocated metal accounts, as well as gold-backed securities.

Recommendations for beginning investors

You need to think about investments as soon as your savings appear, because time is your money. It is better to start investing with reliable traditional instruments. Placing everything at once is not the best option - diversify. In pursuit of excess profits, balance between risk and profitability.

Do not rely on the services of financial intermediaries. Show independence, but within reasonable limits, so that it does not cause excruciating pain for wasted time and money.

Try to stay on top of things all the time. News channels, analyst reviews, and the experience of successful investors will significantly expand your horizons and be useful for making the right decisions.

Finally, I assure you that every ruble invested can bring profit and within a year make you a wealthy citizen. I hope I was able to guide you on the path of investing. I propose to continue to move together through the thorns towards financial well-being. Subscribe to our channel, share your impressions, invest!