Fed rate raised

The US Federal Reserve System (FRS) again raised the key rate to its highest level in a decade - 2.25-2.5 percent. The regulator this time ignored Donald Trump’s calls to ease monetary policy

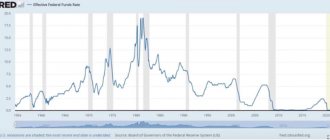

The US Federal Open Market Committee (FOMC) decided to raise the key rate by 0.25 percentage points. — now this figure is in the target range of 2.25–2.5 percent. The key rate level has reached its highest level since the beginning of 2008, during which the Fed, against the backdrop of the international economic crisis, reduced the rate from 4.25 to 0–0.25 percent.

The decision to increase the rate was expected - only 2 out of 92 experts who took part in the Bloomberg consensus survey noted that they expect the key rate to remain at the current level. Economists surveyed by the agency assumed that the Fed could adjust its plans to tighten monetary policy only over a longer term horizon—in 2019–2020.

A press release from the US Federal Reserve said that the American economy is showing strong growth rates, and the situation on the labor market is getting better. The risks to the US economy are “roughly balanced,” the regulator notes. At the same time, as experts expected, the American regulator adjusted the “dot diagram”: now the US Federal Reserve is expecting 2 rate increases next year to a level of about 2.9 percent and still one increase in 2021.

The Fed also recalculated its forecast for US GDP growth this year to 3 percent instead of 3.1 percent. Next year the regulator expects growth of 2.3 percent (from 2.5 percent).

Economists believe that the regulator will increase the rate twice in 2019 and only once in 2021. And the latest “dot plot” (the median forecast of each FOMC meeting participant for the key rate), dated September of this year, assumed 3 rate hikes next year to a level of more than 3 percent.

There were similar sentiments in the market related to the current Fed decision: Chicago exchange operator CME Group estimated, based on futures quotes for the federal bond rate, that the probability of an increase was 68 percent.

The situation on the US financial markets “leaves much to be desired,” according to the VTB Capital report. The index of lending to companies with a high debt burden, the index of high-yield bonds, the index of American bank shares and the index of inflation expectations in the United States reached new lows, experts say. The S&P 500 is down 7 percent in December, and the Dow Jones is also down. This December, which in normal years is characterized by a “New Year's rally” or “Santa Claus rally,” may become their worst since 1931, analysts predict.

On Wednesday, the American stock market corrected up by about 1 percent for the major indices after declining in the previous 2 days.

The regulator makes the decision amid continued pressure from American President Donald Trump, who had previously criticized the Fed for increasing rates. According to Trump, with its policies the regulator is undermining his efforts to stimulate the economy (after $1.5 trillion in tax breaks for US companies, the rate of economic growth accelerated). On Tuesday, December 18, Trump once again called on the Fed to keep rates at the same level.

“I hope the people at the Fed read today's editorial in the Wall Street Journal before they make another mistake,” the US president said on Twitter. “Don't let the market become even less liquid than it currently is. Feel the market, don’t rely only on meaningless numbers,” Trump addressed the regulator’s representatives.

In an article by The Wall Street Journal, which the American leader refers to, the editors urge the Fed to listen to signals that indicate that it needs to take a “prudent pause in the process of raising rates.” The personal consumer expenditure (PCE) deflator index is declining, the dollar has strengthened against gold and other currencies, gold and commodity market goods continue to become cheaper, which also does not contribute to inflation growth, the WSJ material lists arguments against raising rates. In addition, the number of jobs is growing by 170 thousand per month, the unemployment rate is at a historically low 3.7 percent.

Despite low inflation, US economic growth may slow. The growth of the economies of China and Europe has already slowed down, and the trade conflict between America and China adds uncertainty.

Against this background, “investors may well perceive the softening of the Fed’s position as a signal of a worsening situation in the financial markets and even as the regulator’s fear of a possible recession in both the American and global economies,” according to VTB Capital.

Source

The gentlemen are fighting...

If in February, when Goldman Sachs protege Janet Yellen left the post of head of the Fed, it was planned to increase the Fed discount rate by the end of this year to 2–2.5% per annum with a target inflation rate of 2%, now these figures may well be adjusted in on the upward side: especially since there are four more FOMC meetings coming up (July 31-August 1, September 25-26, November 7-8 and December 18-19).

The fact is that each “step” of a quarter of a percent in the discount rate means an increase not only in government spending on servicing the federal debt, but also in the corresponding expenses of the corporate sector of the economy, including pension funds, as well as households. That is, it is becoming increasingly difficult and expensive for all economic entities to “refinance” from banks.

The “issue price” is changing due to the cumulative effect, and is now in the range of $175–200 billion annually (including corporations and households).

Global Look Press / Jesco Denzel / dpa

This increases the profitability and, therefore, the attractiveness for investors of “treasuries” (bonds and bonds) of the federal treasury, but creates pressure on the stock markets, from which “conservative” players leave, as a result of which the overall level of risks and the likelihood of a collapse in stock prices increases.

The same applies to “emerging markets”, from where foreign investors, including “offshore” structures of local comprador capital, are beginning to flee to the American “safe haven of Treasuries” with their billions.

The dollar becomes “strong”, the competitiveness of the American economy decreases, and unemployment rises accordingly. This, together with the increased debt burden, leads to massive bankruptcies and the “collapse” of the US domestic market.

US Federal Reserve in 2021, latest news

The latest US statistics indicate that the Federal Reserve may lower its key rate, which will result in support for gold. TD Securities commodity strategist Daniel Gali is confident of this.

“Gold has held up better than expected amid the recent strength in the dollar, which is a major source of pride for the gold market in the near term,” said John Caruso, senior market strategist at RJO Futures.

The dollar index (the exchange rate of the dollar against a basket of currencies of six countries - the main trading partners of the United States) has been fixed at 98 points since the last week of May. Note that this level is the highest since May 2021.

Analysts note that the strengthening of the US dollar, as a rule, negatively affects the cost of gold, which in this case becomes more expensive for investors who own other currencies. In addition, they draw attention to the fact that the American currency received support due to trade risks around the United States and China.

Why do you need an interest rate?

Its necessity is as follows: it serves as the basis for calculating other rates in the state. Moreover, Fed loans are low-risk loans because they are issued only for one night and only to banking institutions with excellent credit histories.

When looking at stock markets, an increase in rates is an increase in the cost of capital of an organization. That is, for enterprises whose shares are traded on the stock exchange, this is a negative point. It’s different for bonds – raising rates leads to lower inflation.

The foreign exchange market is a little more complicated; here the Fed rate affects rates from several sides. Of course, there is a course; all transactions with currencies are based on it. But this is only a small part of the scheme. The financial flows of the world, which are responsible for most of the transactions carried out in the world on the foreign exchange market, are the movement of capital, which is caused by the desire of investors to find greater profits from investments. Taking into account the state of all types of markets, including the housing market and inflation data, in any country, an increase in the discount rate has both a positive and negative impact on profitability.

Prior to this, the Fed rate increased on June 29, 2006. For 2007-2008 The Federal Reserve slowly lowered it until it approached the lowest level of 0-0.25% in the winter of 2008.

What should markets expect?

At the time of writing this article, there is panic in the markets, from exchanges in the US and Europe to Australia and Japan.

Why? Because no matter what Powell, the CPI scale, or other financial puppets say, forward-looking markets are expecting higher inflation (from money printing to supply chain shocks).

At the same time, those same markets are hanging on Powell's every word. This is further proof that today's modern and horribly unnatural markets are driven entirely by the Fed rather than by old (and now extinct) capitalist principles such as, say, natural supply and demand or legal price discovery. You can simply say that the Fed is the market.

At the moment, there is a real fear that Powell will hint at a reduction in quantitative easing, which will provoke another hysteria on Wall Street.

Meanwhile, as markets nervously await the Fed's next carrot or stick (dove or hawk), they can't help but ignore the S&P 43 earnings ratio (historical average of 17-20), which screams overvaluation but could actually lead to even more high stock prices (bubbles) until the Fed stops printing money and cutting interest rates.

But if Powell can still offer Wall Street the stick of raising rates rather than the carrot of yield curve control, any future rate cuts and money supply "accommodation" will cause markets to simply collapse.

So, what will it be: carrot or stick? Dove or Hawk?

Meanwhile, the stock faces a host of other headwinds. The S&P's dividend yield fell to 1.5%, below even the artificially depressed 10-year Treasury yield of 1.66%. Will investors flee stocks to the “safety” of bonds, causing this outflow to push down stock prices?

At the same time, the number of stimulus payments is being reduced, as is the projected extension of unemployment benefits. If this support is reduced, consumer demand and therefore corporate earnings will feel the pressure, as will stock prices.

Arsenal is exhausted

But here's the rub: what happens when there is no more room to cut rates? Well, this is exactly the situation the Fed (and other central banks) find themselves in now—their arsenal has been exhausted.

The graph above makes this point clear; these are far from hypotheses and theories: there are no rates that need to be lowered, and, therefore, what “worked” in the past simply will not work tomorrow.

For example, in the early 1980s, Fed rates fell from 19% to 8%; in 1989 they lowered rates from 10% to 3%; and during the dot-com bubble of the early 2000s, rates fell from 6% to 1%. See the pattern? With each "accommodative" rate cut, more bubbles appeared, which led to more bubbles, which meant more rate cuts to "accommodate" the markets.

In 2008, of course, the Fed responded to the Great Financial Crisis with, you guessed it, another rate cut—all of which helped “recover” markets (from real estate to tech stocks) amid cheap debt. Unfortunately, however, when we look to the far right of the chart above, we again see that there are no rates left to cut. Powell, of course, knows this too. He's far from a fool. That's why he's been trying so hard in 2021 to raise rates and scale back his quantitative easing program, so he'll have something to "cut" when markets fall again.

Of course, attempts to raise rates against a national and global backdrop of historically unprecedented government and corporate debt have not been successful for Powell, as we saw with the subsequent market surge in late 2021 or the 2019 repo crisis.

What is the conclusion? It's simple: the Fed can't go for a hawkish rate hike without bringing markets—and economies—to their knees; by extension, they now have nothing to “cut” when the current bubble of “everything” bursts. And that's the real problem.

What is the Federal Reserve Discount Rate?

Every day, banks carry out a colossal number of transactions, and each of them tries to increase their volume in order to increase their profit. Sometimes clients come in without warning and withdraw large amounts of money, causing the financial institution's reserve requirement level to fall below Federal Reserve guidelines. This will cause many problems for the bank in the future.

The Fed interest rate is the rate at which America's Central Bank lends money to American banks. Through these loans, financial institutions increase the level of reserves in order to comply with Federal Reserve requirements.

In most cases, banks borrow from each other, but if banks are unable to help their “colleague,” the latter turns to the Fed. According to the law, this loan must be returned the next day. The Fed has a negative attitude towards such loans. If they also become more frequent, the Fed has the right to tighten requirements for required reserves.

More signs of inflation

Stocks continue to spiral nervously as the Fed behaves like a cornered animal trying to downplay inflation risks by propping up a mega "everything bubble" based on inflation tools.

The "official" CPI inflation measure rose to 4.2% in April, the fastest rise since 2008 and twice the Fed's mandate. The regulator says this is due to the deflationary trends of COVID in 2021, which made this relative rise in inflation "expected", "temporary" and soon "contained". But we've heard this before.

Meanwhile, U.S. producer prices rose 6.2% in the same month, the highest since 2010, as core inflation, which excludes energy and food, posted its highest rise since 1981.

In energy and food, prices for everything from ethanol to canola and corn, from milk, chicken wings and lean pork to beef and coffee are skyrocketing at high double digits.

So, if you think inflation is still a matter of debate, the facts once again tell us that it is here. And regarding inflation in risk asset markets, this is a clear bubble narrative.