Any bank holds different amounts of money at different times. Today borrowers deposited one amount, tomorrow another. It’s the same with borrowers: today they took so much money, tomorrow – a little more, etc. A lack of money can cause panic among investors, and the excess should not lie as a “dead weight”.

Therefore, a bank cannot exist on deposit and credit transactions alone. Given the huge amounts, banks are starting to lend to each other. For these purposes, the LIBOR rate was invented. It provides the weighted average rate on interbank loans issued by banks represented on the London Stock Exchange. Since 1985, the rate has been fixed daily by the British Bankers' Association at 11.30 am, based on data provided by banks.

To do this, an authorized agent of the association calls 16 leading banks selected as money market indicators and clarifies quotes for loan rates for a period of 1 to 12 months. From the obtained values, the four highest and four lowest rates are cut off. From the remaining ones, the average value is derived and published. Each term and currency has its own LIBOR value.

Short description

Experts say the name Libor rate is an abbreviation that comes from the name London Interbank Offered Rate. This indicator plays an important role in the banking structure. The rate is calculated using percentages published by the UK Association. Large financial banks, as market makers, provide loans to everyone for a period of 1-365 days in numerous currencies. Experts have been calculating Libor every day since 1985 at 11-00 GMT. The data obtained will be published by Reuters Thomson.

Economists believe that even the % on bonds itself is further from the point of view of the “risk-free rate” than Libor. This is due to the fact that the rate from the state treasury is quite often artificially low. This trend is observed after the adoption of steps towards government regulation and imposition of the tax burden.

Libor data is actively used in England. In addition, large financial institutions located in Switzerland, the USA and Canada are looking at the numbers. It is worth noting that Libor is widely used among market participants as an indicator of demand in terms of the overall liquidity of financial institutions.

Why is LIBOR needed?

LIBOR is the main benchmark rate in Europe. It has long been recognized and used as a serious indicator in international financial relations. Its calculation is open and absolutely understandable to every participant. The question of why LIBOR is published from London is rhetorical. This is where 20% of the world's lending transactions take place. The main volume of commodity and raw materials transactions is also concentrated here. More than 500 banks have their offices in London.

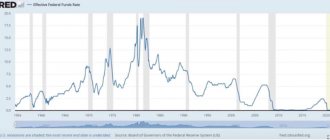

Floating lending rates using LIBOR are used by banking professionals. If LIBOR decreases, you can save a lot of money, but if LIBOR increases, you may end up with unforeseen expenses. The monthly payment will be recalculated as LIBOR changes. It is almost impossible to guess the dynamics of LIBOR, which depends on the global market. Over the past 20 years, rates have varied from 9 to 1.5%. The dynamics can be found on the website of the British Bankers Association.

All banks that are considering the option of attracting loans from other banks borrow money at the LIBOR rate. Its size depends on the currency and loan term. If there is excess money, the bank can provide another bank with a short-term loan at LIBOR. This bet is considered risk-free. If government rates are lowered due to regulatory pressure and a large volume of taxes, then this does not happen when using LIBOR. LIBOR is in great demand not only in London, but also in Canada, the USA and Switzerland.

Characteristic differences

The Libor rate is currently used by experts as a basic benchmark for the value of money. Libor, as an indicator, is necessary to calculate the percentage of different debt financial instruments. The volume of market products with a % indicator depending on Libor includes hundreds of trillions in USD. The Libor percentage is calculated for the 5 most common currencies: pound sterling and euro, American dollar and Swiss franc, yen.

For these currencies, experts calculate 7 different digital parameters. The final figure depends on the cancellation date (maximum 12 months). For each day, experts calculate a total of 35 different Libor figures, which must be taken into account by qualified financial investors in all jurisdictions. To prevent mistakes, experts interview 16 banks. All data is recorded, and only then 25% of the extreme values are discarded. For the resulting Libor range, the weighted arithmetic mean is calculated, which is rounded to five decimal places.

What is LIBOR and why is it important to monitor it?

LIBOR (London Interbank Offered Rate) - London interbank offered rate. It is defined as the weighted average interest rate on loans on the London interbank foreign exchange market. In other words, this is the average rate at which major UK banks lend to each other.

The LIBOR rate is considered to be a key benchmark for the value of money.

It serves as the basis for calculating interest rates on various debt instruments around the world. The volume of financial products whose rates depend on LIBOR amounts to hundreds of trillions of dollars. LIBOR was first calculated in 1986. This was done by the British Banking Association (BBA), which surveyed from 8 to 20 largest banks and, based on the results of the surveys, derived the average interest rate. In 2014, the association lost its LIBOR settlement rights due to rate manipulation scandals, and those rights were transferred to the Intercontinental Exchange Group (ICE), which continues to do so today.

The LIBOR rate is calculated for five currencies:

- U.S. dollar

— Euro

— British pound

- Swiss frank

- Japanese yen.

For each currency, seven different values are calculated depending on the maturity: overnight, week, 1,2,3,6 or 12 months.

In total, 35 different LIBOR values are calculated every day, which are used by investors around the world.

To calculate each bet, 11-16 banks are surveyed. Of the obtained values, 25% above and below are discarded, and from the remaining values a weighted arithmetic average is calculated, rounded to 5 decimal places. The exact calculation methodology and list of participating banks can be found on the Intercontinental Exchange website.

Why is LIBOR needed?

As noted above, LIBOR is the basis for calculating interest rates on loans and debt instruments around the world. Interest rates on government and corporate bonds, currency and interest rate swaps, various loans and long-term deposits, futures contracts and many other financial instruments are tied to this standard.

A change in the rate reflects a change in the value of money, so linking interest rates to it allows you to fix certain lending conditions, flexibly adapting to changing macroeconomic conditions. As a rule, for such instruments the interest rate is a floating value LIBOR + X%, where X is a fixed premium for the risk of default of the borrower, depending on its creditworthiness.

The LIBOR rate itself also contains risk components (risk premium) in the form of liquidity and credit risk. This leads to another function of the LIBOR rate in the modern world - an indicator of the stability of the banking system and market confidence in it.

Based on the dynamics of changes in spreads of 3-month USD LIBOR with American T-bills (government short-term zero-coupon bonds) and IOS (overnight index swaps), one can assess how confident the market is in the creditworthiness of banks.

Current situation with rates in the economy

In 2007-2008 the above spreads reached unprecedented levels when the LIBOR rate premium was 3.5-4.5% to risk-free rates. Since then, the growth of these indicators has been very wary of the market, so the widening of the LIBOR/IOS spread since the end of 2021 from 14 to 58 basis points - the maximum value since 2009 - has made market participants nervous. Together with the increase in yields on American treasuries, the increase in LIBOR may indicate a decrease in investor confidence in the stability of the global financial system and an increase in risks.

However, a number of experts point to the possibility that there may also be technical factors behind the current rally in interest rates. Among them are the provisions of the US tax reform introduced in December, under which international companies will no longer be able to receive a tax deduction for interest paid by foreign subsidiaries.

Instead of funding from foreign subsidiaries, corporations became more interested in unsecured loans from a third party. The demand for such loans directly affects the LIBOR rate.

For the stock market, an increase in LIBOR is a negative factor, but in most cases it has a minimal effect on quotes. Therefore, the rate increase itself, in isolation from other macroeconomic indicators, is not significant for this market. However, if the dynamics of spread widening continues, the negative effect may intensify and become more noticeable.

The future of LIBOR and alternatives

The British organization FCA announced in 2021 that the calculation of the LIBOR rate will be discontinued by the end of 2021. The rate is planned to be withdrawn from use due to the opacity of the mechanism for its formation.

The weaknesses of the LIBOR rate became clear after the 2008 crisis, when a series of fines for rate manipulation followed in 2012. The rate calculation mechanism was vulnerable to the possibility of bank officials colluding to manipulate the rate to their own advantage. The total amount of fines was about $9 billion, and UBS, Royal Bank of Scotland, ICAP and Rabobank were among the fined banks.

Since then, control over banks has been significantly tightened (including the right to administer LIBOR transferred from BBA to ICE), but the imperfection of the mechanism still carries risks. “We do not believe we can successfully move to real-world benchmarks if markets continue to rely on LIBOR in its current form,” FCA chief executive Andrew Bailey said in the summer of 2017.

The question of an alternative to the LIBOR rate remains open today. For some currencies, other benchmarks are already widely used. For example, for the euro, the more popular rate is EURIBOR, calculated based on data from 40-50 largest European banks. In Russia, an analogue of LIBOR is the MosPrime interest rate, which is not yet used very often, but in the future may become more widespread.

OIS rates may also be an alternative. In the pound sterling market, this rate is called SONIA (sterling overnight interest rate average swaps), in the European Union - EONIA, in Russia - RUONIA, etc. The conventional swap rate is calculated based on the government bond yield curve and represents a credit premium for the risk of interbank defaults. Essentially, the swap rate is the average forward rate determined from the government's zero-coupon yield curve.

Experts note that since a very large number of financial instruments are linked to LIBOR, the transition to new indicators will be gradual.

open an account

BCS Broker

Libor: principle of use

In the archive you can see practical value that determines the steps of various types of businesses and, of course, the financial sector.

Numerous advantages have influenced the fact that Libor is used as a key link rate in powerful financial instruments:

- Inflation rate. In this case, experts can determine as accurately as possible the speed of the period of money circulation in the financial system of a particular state.

- Calculation of forward rates with Libor for the supply of raw materials (primarily this applies to agriculture, oil and metals).

- Interest rate for stock securities, bills, bonds. Experts use this indicator in the industry where there is a floating coupon rate, which is tied to the indicator itself.

- Quotes of universal futures and other assets presented on markets. The Libor financial instrument is used on stock and commodity exchanges, as well as in the industry where contractual agreements linked to crosses or majors appear. This option is especially important for those actively trading on the Forex market.

- Libor discounts for transactions with the Central Bank.

- Level for credit products, here the rate is used by financial institutions to provide lines to customers. This category includes mortgage loans.

- Discount rate. The basic indicator that appears in investment calculations. This applies not only to the financial sector, but also to those cases where projects are being implemented in any economic area.

If a novice investor wants to figure out how to practically work with Libor, then it is better to consider all the subtleties using the example of pounds sterling. This question is of interest to active users of the Forex market and those who decide to invest their savings in the European real estate market. Since about 2000, the rate has been on a downward trend, therefore, the value of money itself decreases. Thanks to this, with Libor you can predict rates on the foreign exchange market years in advance and identify the right moment to create a deposit in a particular conversion.

Investors are advised to proceed with caution as Libor is a relative indicator. The market is subject to the influence of positive and negative factors that can distort the real value of money.

Impact on the economy

It is Libor that today gives an idea of the overall assessment of the global financial condition. This indicator is a kind of “barometer” for a huge number of large organizations specializing in issuing and receiving loans. Libor has a direct impact on virtually all interbank and private flow transactions.

For analysts, Libor is the main refinance rate for multifunctional financial instruments and market assets:

- Loan syndication.

- 1-3 month futures, where the rate is fixed.

- Securities with no fixed interest rate.

- Universal % swap.

- Deferred rate.

It is worth noting that for any transactions in euros, the EURIBOR percentage is increasingly used every day.

Libor dynamics is indispensable in the following cases:

- The rate is like a qualitative calculation of % on options and futures. Minimum terms are taken into account.

- On large commodity and stock exchanges, where a large number of transactions are made daily. Libor dynamics are necessary in calculating fines when one of the parties to the transaction does not fulfill the obligations assigned to him.

- Careful calculation of the financial value of numerous over-the-counter assets if a cash loan is issued to a borrower whose rating has not reached the acceptable AA. Then the exact rate of the exact size of the loan is calculated as regular Libor, as well as “+” or “-” margin on the loan.

Importance in the banking industry

The latest data showed that today Libor in USD is calculated for different periods of demand for interbank loans. Universal Libor for 1 month. presented as the interest rate at which financial institutions issue loans to their clients for one month. Of course, no one is stopping the bank from accepting a profitable deposit from a third-party company under standard Libor. This service is available if the credit rating of the organization in question is not lower than AA.

The rule is very relevant. If a financial organization has an AA rating, then it has every right to attract credit lines from other banks as an option for quickly increasing its base capital. Management borrows funds from more developed enterprises at the current % Libor (the rate takes into account the currency and the date of repayment of the debt).

If fruitful work has contributed to an excess of capital, then the actual borrower has the right to provide short-term loans to other banks. Universal interbank lending operates according to this scheme. Libor is always a reliable basis for determining %.

Numerous studies have allowed experts to prove that Libor data is closest to the risk-free rate. This parameter managed to bypass even the % on government bonds. Experts explain this effect by the fact that the treasury rate is often underestimated due to a large number of taxes and the pressure of government regulation.

What is LIBOR used for?

Banks often use LIBOR in a variety of products. The conditions for them are determined based on the LIBOR rate increased by 2-6 percentage points.

- Credit. Foreign currency loans are often tied to LIBOR. In this case, the rate turns out to be floating, which affects the size of the monthly payment. If at the beginning of the term it seems to the client that he took out a loan very profitably and cheaper than existing offers, then he can also suffer from changes in LIBOR and overpay more than borrowers at fixed rates. The loan rate in the contract is written, for example, as “LIBOR+7 pp.” If the LIBOR is 1.96%, then the rate for the borrower will be 8.96%, and if it rises to 3%, then the rate will also rise to 10%. For large amounts, the credit burden will increase significantly.

- Deposit. LIBOR rates in deposits are rarely used and for long periods. Thus, for a three-year deposit, the conditions for rates may be as follows: 1 year – “LIBOR+6 percentage points”, 2 year – “LIBOR+4 percentage points”, 3 year – “LIBOR+3 percentage points.” Short term deposits using LIBOR rates are not offered by banks.

- Futures contracts for short periods.

- Swaps. The parties sign an agreement according to which they exchange credit obligations on different terms while maintaining the same amount.

- Syndicated loans. They involve the transfer of money to one recipient from several banks.

- Floating rate bonds. The calculation uses the yield on government bonds and interbank loans.

Bet: possible prospects

Despite the UK's post-Brexit status, the pace of Libor deployment continues to accelerate. This comes with several significant advantages:

- Investors have the right to count on sufficient transparency and simplicity of calculations.

- Libor can be used for long-term forecasting. A large database of historical statistics has been recorded since 1985.

- The rate, as a financial indicator, can be used for any economic instruments that are used in the investment industry.

- If banks actively use Libor in their work, then they belong to the category of organizations with the highest degree of security.

Experts say that regular use of the Libor monetary indicator allows investors to achieve financial stability against various negative factors.

Libor: calculation rules

Every day, a qualified BBA agent records data from 16 of the most reliable and largest banks. The management of financial organizations provides all the information about the level of interest rates at which they are willing to issue financial loans to other organizations. For calculations, experts can only use data that corresponds to current currencies and loans with maturities of up to one year.

The rate of banks that are respondents is continuously monitored. Due to this fact, the UK Banking Association reviews key data on financial companies at least once a year, then publishes the figures.

Now Libor 6m is calculated according to the standard scheme: all figures that were received by RT organizations are displayed in descending order. Experts remove 4 largest and the same number of smallest numbers. After these manipulations, the rate remains with eight percentage indicators, which are recalculated according to the arithmetic mean principle. The resulting figure is Libor for that day.

Due to the fact that interbank loans can be issued in financial institutions of different jurisdictions, Libor must be calculated separately by qualified employees for all currencies. The final daily rate is divided into several levels, which are tied to the loan term. Many investors prefer Libor 12m as they can make good profits over this period. In total, experts publish calculations for 15 periods.

Scandalous situations with LIBOR.

Recently, there has been active discussion around the LIBOR rate. The reason was the fraudulent actions of traders and banks who are trying to hide financial problems. In 2011, the US Department of Justice began an investigation. After 4 months, Japan, EU countries and Switzerland joined it. The investigation revealed that Barclays bank carried out the most fraud with LIBOR. He made money by manipulating the rate and covering liquidity gaps. For this he paid a fine of $450 million, which amounted to 5% of the bank’s income.