The US Federal Reserve lowered the refinancing rate for the first time in 10 years. Although the easing was the very step that the US administration demanded, the specific decision to reduce the rate by 0.25 percentage points was criticized by the American president for lack of decisiveness. The markets did not like the decision either: stock indices sank significantly around the world. Izvestia explains why the key rate is needed and why the decision to cut it on July 31 may turn out to be extremely important.

What is the US Federal Reserve rate?

We need to start with what the Fed is. Fed - The Federal Reserve System is the American equivalent of the Central Bank of any state. It is there that the main controlling and regulatory financial functions of the country are concentrated, as well as the issuing function, the function of ensuring economic stability in the United States, and conducting domestic and foreign financial policies. I described in more detail the composition, operating principle and functionality of this organization in a separate article: US Federal Reserve System.

Among other tools for influencing the country's monetary policy, the US Federal Reserve, like any Central Bank, uses the discount rate.

The discount rate is the interest rate at which the country's central bank (in the USA this is the Federal Reserve) provides loans to commercial banks. The size of the discount rate directly and indirectly affects a large number of other macroeconomic indicators:

- Interest rates on loans and deposits in banks, volume of the lending market;

- Growth or decline in production, GDP;

- Growth or decline in consumption;

- National currency exchange rate;

- Inflation rate;

- Unemployment rate;

- Etc.

Resetting the Fed: Trump's belated victory in the fire of a new global crisis

A few months before the US presidential election, what Donald Trump has come true: the Federal Reserve has lowered its base rate to almost zero. At the same time, a new “quantitative easing” program was announced in the amount of $700 billion, the bulk of which will be used to buy back US Treasury bonds. But it’s difficult to call this a triumph for Trump over uncooperative bankers, since the Fed’s actions were dictated by the impact of the spreading coronavirus panic and did not calm American markets. The very next day, the Dow Jones index collapsed by 13%, and the largest investment banks announced the onset of a new global recession, although by the end of the year, according to their forecasts, the world economy could begin to recover.

“The coronavirus outbreak has wreaked havoc on communities and disrupted economic activity in many countries, including the United States,” began the Fed’s March 15 announcement that it would cut the federal funds rate to 0-0.25%. The last time the Fed rate dropped to this level was at the end of 2008 - at the time of the global financial crisis - and stayed there for seven whole years. A few days after Trump was elected president of the United States, the Federal Reserve launched another cycle of rate hikes. From November 2021 to December 2021, it was gradually increased from 0.25-0.50% to 2.25-2.50%, which increasingly angered Trump. At the end of July last year, the Fed nevertheless lowered the rate to 2-2.25%, but the US President immediately made it clear that this was not enough to stimulate the American economy with cheap money.

“Our problem is not China. We are stronger than ever - money is pouring into the US while China is losing thousands of companies from other countries and their currency is under pressure. Our problem is a Federal Reserve that is too proud to admit it was wrong for moving too fast and tightening too much,” Trump said last August. These verbal interventions, coupled with growing market concerns about a slowing global economy, had an effect: over the next six months, the Fed rate continued to decline, with the last time before zeroing this happened on March 3, when the rate was set at 1-1.25%.

Meanwhile, the debt burden of the American economy grew even without the Fed cutting rates. By the middle of last year, the total debt of US citizens, as reported by the Federal Reserve Bank of New York, reached a new historical high of $13.86 trillion, and mortgage debt exceeded the level of 2008, when the global crisis was triggered by the mortgage “bubble”. The corporate sector was not far behind: over several years, American companies issued $1.2 trillion in loans. And if until recently their traded value was close to par, then due to recent events it, as evidenced by data from Bloomberg and the New York credit association LSTA, fell to 84 cents per dollar, demonstrating the same trend as in 2008 , when American loans depreciated to 60 cents on the dollar.

However, Donald Trump did not hide his satisfaction with the Fed’s actions. “I want to congratulate the Fed. What happened to her is phenomenal news. I can say that I am very happy. I never expected this. And I like to be surprised,” the American president reacted to the Federal Reserve’s decision. For its part, the Fed leadership announced its readiness to take aggressive actions to counter the coronavirus. The head of the Federal Reserve in Minneapolis, Neel Kashkari, in an interview with CNBC, said that the US central bank is the fourth echelon in the fight against the crisis, after health professionals, the public and Congress.

“The Fed is prepared to use its full range of tools to support the flow of credit to households and businesses and thereby advance the goals of maximum employment and price stability,” the Fed's Open Market Committee said in a recent statement. “In order to ensure the smooth functioning of the Treasury and mortgage-backed securities markets... the committee will increase its Treasury securities holdings by at least $500 billion and its mortgage-backed agency securities portfolio by at least $200 billion in the coming months.”

In addition, US Treasury Secretary Steven Mnuchin announced an emergency program to support households. “Americans need money, and the president wants to give them money now. Right now, within two weeks,” he said at a White House briefing. According to American media reports, the economic stimulus package could cost $1-1.2 trillion, with $250 billion to be allocated in the form of “helicopter money”—“direct financial transfers.” In other words, just like in 2008, they again decided to pour money into the crisis.

The reaction of American markets to the Fed rate cut was immediate: already on March 16, the Dow Jones index, which had lost 14.3% a week earlier, fell at the opening by more than 2 thousand points (from 23,186 to 20,918 points), and by the end of the day fell up to 20,180 points. On March 17, there was a rebound to the level of 27,174, but by that time Bloomberg had already added fuel to the fire, citing forecasts by economists at investment banks Goldman Sachs and Morgan Stanley. According to them, the coronavirus has triggered a new global recession, and the question now is how long it will last and how deep it will be. In particular, Morgan Stanley considers a recession in the global economy as a “base case scenario” - global growth will slow to 0.9%, which is comparable to the “Great Recession” of 2009. Goldman Sachs' forecast is slightly more optimistic: the global economy will grow by just 1.25% this year. However, for now, both investment banks expect that the recovery will begin in the second half of the year, but warn that the current negative effects may intensify.

At a closed meeting at Goldman Sachs, which Forbes magazine wrote about, forecasts were also made about the prospects for the spread of coronavirus: 50% of US citizens and 70% of German citizens are at risk of becoming infected, and although 80% of those infected will have a mild form of the disease, the average mortality rate will be up to 2 %. It was also noted at the meeting that the epidemic will reach its peak only in eight weeks.

The Fed was not the only central bank to lower its base rate in recent days; more precisely, a wave of such decisions was launched by the Fed's rate cut in early March. The Bank of England lowered its base rate from 0.75% to 0.25% on March 11, expressing hope that this “will help support business and consumer confidence in difficult times and support cash flows for businesses and households.” On March 13, Norges Bank announced a radical reduction in the interest rate from 1.5 to 1%, explaining this by significant uncertainty regarding the duration and consequences of the coronavirus outbreak, which carries the risk of a pronounced economic downturn. The precedent-setting decision to reduce the base rate to the historically minimum level of 0.75% was made on March 17 by the Central Bank of South Korea. Over the past two weeks, the Bank of Canada has already made two rate cuts: on March 4, it dropped to 1.25%, and on March 16, to 0.75%, and at the same time, the Canadian Ministry of Finance announced the launch of a lending program to support businesses and stimulate the economy.

Despite the fact that the Fed and its friendly central banks are actively easing monetary policy, most governments are reacting more slowly to the situation and are currently only developing tax stimulus packages for economies, which may not be enough to reassure investors, Bloomberg notes in its material. At the same time, the impact of the coronavirus and tightening financial conditions could result in a physical shock to the global economy, economists at Morgan Stanley add.

The European Central Bank finds itself in a very interesting position, whose base lending rate has been kept at zero for quite some time, and the deposit rate is generally negative (minus 0.5% per annum). At a meeting on March 12, European bankers headed by Christine Lagarde decided not to change the level of rates, but announced the expansion of the next quantitative easing program, which started last fall in the form of a monthly repurchase of securities in the amount of 20 billion euros. By the end of this year, the ECB intends to additionally purchase assets (mainly corporate bonds) for 120 billion euros.

The drama of the situation lies in the fact that quantitative easing measures for the EU economy seem to be completely meaningless. In the fourth quarter of last year, eurozone GDP, according to Bloomberg, showed the weakest growth since 2013 - only 0.1%. Back in early February, the European Commission issued a relatively optimistic forecast that eurozone GDP would grow by 1.2% in 2020-2021, including in its base scenario that the coronavirus epidemic would peak in the first quarter with fairly limited global consequences. Two weeks before the end of the first quarter, it is quite obvious that this cannot be counted on - the rate of spread of the epidemic in the European Union leaves no hope that the second quarter will be successful for its economy.

An important indicator for further developments will be the position of the People's Bank of China, which in November last year reduced the rate on one-year medium-term loans (MLF) for the first time in five years. And although the decrease was symbolic - from 3.3% to 3.25% per annum, the Chinese monetary authorities hinted that they were ready to resort to such measures in the future. A few days after this decision, the Global Times, the English-language version of the official publication of the Chinese Communist Party, People's Daily, published an article under the suggestive headline "China needs to prepare for zero interest rates." But so far the Chinese Central Bank is in no hurry to lower the rate following the Fed, and this raises concerns among a number of experts.

“The regulator did not ease monetary policy, apparently considering this a temporary factor that will disappear with the lifting of quarantine. The market reacted to this confidence of the financial authorities with an increase in demand for government securities (up to +0.32% for 10-year bonds), as well as a correction in stocks (-4.3% at closing), which can be interpreted as increased tension,” noted on the eve of Invest analysts, noting that easing regulations for banks would provide about 550 billion yuan to stimulate lending in China. However, measures to prevent the crisis have already begun - a few days ago, for example, information appeared that the People's Bank of China and the government of Liaoning Province would buy 44% of the shares of the troubled regional bank Jinzhou.

Finally, there remains intrigue around the key rate of the Bank of Russia, which throughout the past year decisively lowered its level, stopping in January at 6% per annum, which is considered the upper limit of a loose monetary policy. The situation in recent days is reminiscent of the actions of the Central Bank at the end of 2014, when the fall in oil prices and the devaluation of the ruble led to a sharp twofold increase in the rate to 17%. Now the ruble’s reaction to a two-fold decline in oil prices has turned out to be not as catastrophic as five years ago, but on March 20, the day of the next Central Bank meeting on the key rate, Elvira Nabiullina and her colleagues will have to make a difficult decision. In 2014, they acted in full accordance with the canons of monetarism: if the currency falls, raise the rate, but now there is definitely no critical need to take this step again. As shown by the Bloomberg consensus forecast, in which 21 experts participated, at the next meeting the Central Bank of the Russian Federation will leave the key rate unchanged.

A number of Russian experts note that in the current situation, Russian economic authorities need to support aggregate demand in response to the coronavirus. “It is better for the Central Bank not to do anything with the rate, but not to allow a significant weakening of the ruble - perhaps with the help of interventions if the ruble turns out to be weaker than other currencies of emerging markets,” says financial analyst Viktor Tunev . — So far, the ruble has fallen, like the Brazilian real or the Mexican peso, by 15-20%. This is normal given the shock from oil prices and the collapse of the OPEC+ deal. Further dynamics of the ruble must be better if we really want to prove to everyone that we have done everything to ensure macroeconomic stability at any oil price.”

Nikolay Protsenko

Increase and decrease in the US Federal Reserve interest rate

Let's look at what happens when the US Federal Reserve raises or lowers its interest rate. First of all, this affects the situation within the country, but since the economies of other countries in the world are very dependent on the United States and the dollar, such events affect everyone to one degree or another.

So, when the discount rate increases:

- Loans are becoming more expensive;

- The level of production and consumption, trade volumes are decreasing;

- Inflation is decreasing;

- Economic growth is slowing down.

When the discount rate decreases:

- Loans are becoming cheaper;

- Business is developing faster, the level of production and consumption, and trade volumes are increasing;

- Inflation is increasing;

- Economic growth is accelerating.

It may seem that if this is so, then why raise the discount rate at all? You can systematically reduce it as much as possible. But this is not so, since lowering the discount rate also entails certain economic problems. For example, rising inflation and weakening of the national currency.

Therefore, any Central Bank, including the US Federal Reserve, uses this instrument as they see fit in a particular situation.

The US Federal Reserve may raise or lower interest rates during its meetings. Such meetings are held 8 times a year, approximately every 40-50 days.

Monetary policy: why and how rates are regulated

The stakes are high and low. However, these values are always relative, and therefore it is important to take into account historical dynamics and growth/decrease in relation to their own historical values.

Photo from the March meeting of officials of the US Federal Monetary Policy Committee (FOMC)

The central bank is raising rates to prevent the economy from overheating. This happens when there is no room for growth in the economy and prices begin to rise beyond the real increase in the production of goods and services, which leads to an acceleration of inflation and a decrease in the trading rate of the currency.

An increase in the rate slows down inflation and makes the currency more attractive in the eyes of investors, and commercial banks place investor funds on deposits at a higher interest rate.

The rate reduction, on the contrary, is stimulating in nature and serves to speed up economic processes, cheap loans for business, low taxes, reduce unemployment and increase business activity. This accelerates inflation and reduces the trading rate of the currency.

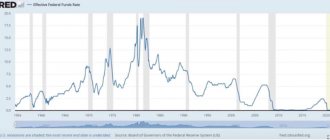

Dynamics of the US Federal Reserve interest rate

Let's briefly look at how the US Federal Reserve's discount rate has changed in recent years. Here is a graph: the dynamics of the Fed discount rate from the 80s to the present day.

As can be seen in the graph, in the 80s the US Federal Reserve discount rate was quite high, comparable to the current rates of the Central Bank of the Russian Federation or the NBU. For a short time it even rose above 10% per annum. Then a progressive downward trend began with its minimums and maximums. In December 2008, the Fed discount rate reached its minimum at 0.25% and remained there for 7 years until December 2015. Then the rate began to gradually increase. In January 2021, it reached a local maximum of 2.5%. And only now, at the Federal Reserve meeting on July 31, 2021, the discount rate was reduced for the first time in the last 10 years, and now it is 2.25%.

What's happening in the Forex market

If you opened the economic calendar and found that officials of any national central bank are meeting to make a decision on interest rates, then rates may change and change the trend, depending on whether they are lowering or increasing.

Or rates may remain at the same level, and then the trend will be determined based on the current dynamics: if the rates were reduced the previous time, then the trend will be bearish, and if they were raised, then the trend will be bullish.

Typically, prospects for rate increases or cuts are announced repeatedly over long periods of time before they are changed. Long-term investors and position traders use this to make a profit or, conversely, to avoid risks.

US Federal Reserve rate cut: consequences

So, throughout the previous week, financial analysts around the world discussed the possible consequences of lowering the US Federal Reserve interest rate. By the way, its drop to a minimum in 2008 coincided with a strong spiral of the global financial crisis.

The reduction in the discount rate caused a fall in the price of most exchange-traded assets on world financial markets. Including in relation to the dollar. On the one hand, this may seem illogical: after all, the rate reduction is intended to increase the rate of economic growth in the United States and, as a consequence, throughout the world, which is heavily dependent on the dollar and the American economy.

But, on the other hand, the rate reduction, and even such a “historic” one (for the first time in 10 years), suggests that the situation in the global economy and the US economy is already quite unfavorable. Indeed, one of the main criteria for making this decision was the slowdown in the growth rate of the global world economy. Simply put, “since the Fed is cutting the Fed rate, it means everything is bad” - this is how investors and traders reacted on world exchanges.

In addition, world analysts believe that such a reduction in the US Federal Reserve interest rate is not enough to normalize processes in the global economy. There were expectations for a more significant reduction in the rate or at least an announcement of intentions to reduce it further (which US President Donald Trump has been insisting on for a long time), but this did not happen.

The reduction in the US Federal Reserve rate should theoretically facilitate the outflow of investments from dollar assets (since they will become cheaper, their profitability will fall) and their flow into other assets and currencies, incl. to developing countries (Russia, Ukraine, etc.). For example, after the announcement of the decision to reduce the rate, oil and gold prices rose slightly, as well as other leading world currencies (euro, Swiss franc, Japanese yen). It is also very likely that this will cause some growth in the market for alternative assets, such as cryptocurrencies.

Is the current rate high?

The last time the Fed cut rates was at the end of 2008, amid the acute phase of the financial crisis. However, at that moment it dropped to record lows - 0–0.25%. Before this, even a decline to 1% was exceptional and took place over a fairly short period of time in the early 2000s. The last time it lasted at zero level for more than six years. Moreover, the rate cut was then accompanied by other unprecedented support measures, for example, the “quantitative easing” program, which meant the purchase of government bonds worth trillions of dollars. All these steps were justified by the severe recession in the American economy, which became the most serious since the Great Depression of the 1930s.

It was only in 2015 that the Fed began raising rates again, but very slowly and carefully so as not to “scare off” the still sluggish economic growth. By the second half of 2021, the rate increase had stopped, despite the fact that GDP growth rates had almost fully recovered from the crisis.

FRS

American stock indices

Photo: TASS/Zuma

Engaged in the dollar: Russians increased savings in foreign currency

Deposits in dollars and euros increased by almost 5%

At the moment, the situation in the US economy looks good enough to raise the rate rather than lower it. The unemployment rate is 3.6%, one of the lowest in the last half century. Economic growth has slowed down slightly, but still remains at a quite respectable level - 2.1% at the end of the second quarter. No country in Western Europe can boast of such indicators, even though rates are now significantly lower in the eurozone. Inflation has mostly remained below 2% in recent years, so in this case it also cannot seriously influence the Fed’s decisions.

If the situation on the stock market causes concern, it is perhaps in terms of overvaluation of assets. Over the past year, stock indices have been located close to record values, which are constantly updated. In a normal situation, this signals an overheating of the economy and the need to tighten rather than soften financial policy.