Investing in stocks, bonds and other securities to regularly receive income is a thought that comes to many people. The most intelligent of them realize that, without special skills, engaging in such activities is very risky. Therefore, you either need to learn or find someone who will buy and sell securities for you.

It is for such purposes that a mutual fund (mutual investment fund) exists.

But is it worth investing your money in mutual funds? Before making a decision, let's understand how such funds function.

- What is a mutual fund and how does it work?

- How does mutual fund work?

- Types of mutual funds

- Pros of mutual funds

- Disadvantages of mutual funds

- How to choose a reliable mutual fund

- 5 signs of a financial pyramid: don’t get confused!

- Mutual Fund – is it profitable or not?

Mutual funds: advantages

Professional management. Mutual funds are managed not by one person, but by a whole team of professionals. Each of them has a specialized education in their field, extensive work experience (which amounts to several years, sometimes even decades) and, accordingly, is a good specialist. Management includes portfolio management, ongoing market research and the search for the best investments that can provide the greatest returns at acceptable levels of risk.

Agree, you can hardly cope with such work alone. And even if you have some experience in this area, how long will it take you to analyze the current market situation? And is independent analysis and the time spent on it worth the additional profits you will receive?

This is especially true for investors with small capitals. Well, how much can you earn from 100 - 200 thousand rubles by analyzing the market yourself? At best, 20-30 thousand per year. BEST CASE SCENARIO!!! And you will spend disproportionately more time than the income received. Therefore, it is better to trust the professionals.

Low cost of management. Typically, mutual funds buy and sell tens or even hundreds of thousands of shares at a time in the stock market. And due to turnover, they have a preferential tariff on commission costs, which can be ten times lower than in the case of independent sales by private investors with their several lots. As a result, the annual costs borne by shareholders in the amount of 2-3% are sometimes more profitable than independent trading.

Diversification. Private investors, when purchasing certain assets, completely forget about diversification (diversity of investments). Their portfolio usually consists of 8-12 different stocks, covering a maximum of 3-4 sectors. This kind of investment is very risky. After all, if the quotes of one or two issuers included in your portfolio collapse, you may lose most of your investments.

If you still try to properly diversify a private portfolio, then investors face two problems.

Firstly , in order to diversify your portfolio as much as possible with various assets in all major industries, you need a lot of money. If you have a small amount, you can forget about this idea.

Secondly , even if you have the necessary amount on hand for proper diversification, managing such a portfolio is quite difficult. Imagine that you will have 50-100 shares. How much time will you devote to monitoring, portfolio analysis, and monitoring the current position in a particular company of which you are a shareholder?

By investing in mutual funds, you immediately achieve maximum diversification, which you would hardly achieve as a private investor. Maximum diversification can not only reduce risks, but, paradoxically, it can also increase the return on investment or obtain higher profits.

Low threshold for entry into mutual funds. If you have little money, then a few thousand rubles will be enough to buy shares. The average purchase price is about 10,000 rubles. Most management companies adhere to this price range. There are, of course, lower entry prices. But don’t think that mutual funds are investing for the poor. Large organizations and companies also invest money in mutual funds for lower cost and high quality money management.

State control. The fund's activities are constantly monitored by the Financial Services Authority for Financial Markets. Therefore, mutual funds are required to report all financial indicators for their activities: profits, losses, operating expenses, etc.

Large selection of mutual funds with different levels of risk and profitability. You can choose for yourself the fund that best suits your financial capabilities, goals, investment horizon and possible level of losses and profits.

For example, if you invest for a long time (5-10 years) and are aiming for maximum profitability, then equity funds are most likely suitable for you. If you want to avoid large drawdowns in the value of your shares, then your choice is mixed funds or bond funds. In general, you cannot tolerate losses, and you may need money in the near future - your choice is money market funds.

Despite all the apparent simplicity and a lot of advantages, mutual funds also have disadvantages.

Hedge risks and diversify investments

Why, if the mutual fund’s assets have already been diversified - you ask and you will be wrong. Because diversification is diversification, but managers add assets to the portfolio, following their logic of strategy, so assets, in general, “slightly” correlate with each other. Well, for example, Mutual Fund China invests in Chinese stocks. If the economy of the Middle Kingdom grows, shares rise, and so do mutual fund shares. If America declares another economic war on China, the economy will go out, and with it everything that relates to it. Well, share too.

So. in 2015, following the shares of Russian companies, shares of mutual funds that had the misfortune of investing in this industry crashed below the plinth. But bond mutual funds felt excellent, since the Central Bank raised the key rate and printed 100,500 OFZ with a double-digit coupon rate.

Thus, protect possible risks and build a balanced portfolio.

What is a mutual fund and why is it needed?

A mutual fund is an investment instrument, often a long-term one, that helps increase capital. His job is as follows: you come with a certain amount of money and use it to buy shares of a mutual investment fund. Other participants do the same.

The fund's management company (MC) accepts money from investors, accumulates it and gives instructions for the purchase or sale of shares, bonds, and real estate. Shares, for example, give ownership of a business. It turns out that you also own a share (even a tiny one) of the business.

What business do you own? To the one that buys the management company. She diversifies her portfolio and buys different stocks. These are usually large well-known players: Sberbank, Lukoil, Megafon, etc.

The growth of the securities of these companies brings an increase in the share that you purchased. If you decide to sell them, they might go for a bargain price and you'll keep the difference. But shares may also lose value.

Working with ETFs

First, you need to clearly define your goals. If investing is aimed at obtaining regular income, then you should pay attention to funds that offer securities of companies that pay dividends. If the goal is to get the maximum benefit from the sale of a package, then you should take a closer look at ETFs that include the relevant assets.

For information!

You can buy shares on the stock exchange yourself or through a management company. In both cases, you will need to open a broker account, or an IIS - an individual investment account.

How mutual funds are structured

A mutual investment fund can be compared to a safe in which investors’ assets are stored: money, real estate, securities, shares in an LLC, etc.

A share is a conditional share of property in this fund. This is a registered security that confirms that you own such and such a share of such and such a fund.

The property from the safe is managed by the management company. Its task is to earn money for shareholders on behalf of the mutual fund. To do this, it manages the fund's assets: rents out real estate, issues loans, buys and sells securities, currency, and shares in organizations. If the value of the fund's assets increases, the price of the unit also increases.

Management services are paid. It is beneficial for the management company that the shares of its funds grow in price: this is the best advertisement for attracting new shareholders. The more shareholders, the more assets the management company has and the more money it receives for its work.

The management company is responsible for the assets of its shareholders before the law, so it cannot simply sell them, take the money and ride off into the sunset.

Before becoming a shareholder, an investor studies the rules of trust management of the fund, PDU, a document that sets out the operating conditions of the mutual fund, and then transfers money or other property to the management of the management company. It becomes the common shared property of the shareholders, and it can no longer be taken away from the fund.

There is a concept of “anchor shareholder”. This is a large investor who is ready to invest a large amount of assets at once, on average from 25 million rubles, but wants the mutual fund to work on his terms. Then the management company creates a separate fund, all shares of which belong to this shareholder. The company manages the property, the shareholder receives income.

Let me explain a little what is shown in the diagram.

Shareholders invest in different funds, and the management company manages them, earning money for the shareholder. Different shareholders can invest in the same fund. Funds invest in different assets.

The same management company can manage different mutual funds. Every month she withdraws a portion of the funds from each fund as her remuneration.

The management company works closely with the specialized depository (SD). The Board of Directors provides services to the management company: it maintains parallel records of the assets of the funds, issues consent to transactions, controls the disposal of the property of mutual funds in the interests of shareholders, and coordinates the reporting of the management company. For these services, the special depository also receives a monthly remuneration from the management company.

Management companies and boards of directors are controlled by the Central Bank of the Russian Federation: they submit funds’ reports to it, provide information upon request, and comply with all regulations of the Central Bank.

The Central Bank of the Russian Federation and the Board of Directors are the controlling bodies for the management company. They monitor the actions of the management company in order to protect the interests of shareholders.

The Central Bank can send a request to the special depository to obtain information about the management company that interests it, and the Board of Directors is obliged to provide this information.

Ten questions about mutual funds

1. Is it possible to use a closed-end mutual fund as a tool for evading income tax when selling property (investment rights or real estate) transferred into trust management, and using the funds received to invest the closed-end mutual fund in other projects?

In response to your request, I would like to point out that the question posed is incorrect.

In accordance with Article 246 of the Tax Code of the Russian Federation, Russian organizations are recognized as taxpayers of corporate income tax. Considering that a mutual investment fund is a separate property complex without the formation of a legal entity, mutual investment funds are not payers of income tax. (This position is confirmed in the Letter of the Ministry of Finance of Russia dated November 25, 2004 N 03-03-01-04/1/153, Letter of the Federal Tax Service of Russia for Moscow dated December 16, 2004 N 26-12/81335).

Also, income from managing a mutual fund for the trustee is remuneration. The trustee does not have a direct economic benefit from the income received from managing the mutual fund; thus, the management company is also not a taxpayer of income tax for this reason.

2. When does the founder of trust management have a taxable income base? Only at the time of presentation of the share for redemption?

The basis for paying profit (income) tax for a shareholder is the sale of a share or other disposal of a share (including its redemption), as well as the payment of periodic income , which, according to Art. 14 of Federal Law No. 156-FZ “On Investment Funds” is possible in closed-type mutual funds.

When answering this question, it is also necessary to note the existence of some controversial issues, including the exchange of investment shares .

We draw your attention to the fact that at the moment there is a position of the Ministry of Finance of Russia, set out in Letters dated 03.29.2007 No. 03-04-06-01/93, dated 06.24.2005 No. 03-05-01-04/203, dated 15.02 .2006 No. 03-05-01-04/30, dated 02.16.2006 No. 03-05-01-04/31, dated 03.03.2006 No. 03-05-01-05/38 and the Federal Tax Service Department for Moscow, expressed in Letter No. 28-11/29667 dated April 14, 2006. It is assumed that transactions for the exchange of investment shares fall under the characteristics of an exchange agreement, to which the rules on purchase and sale apply, which in turn leads to the obligation to pay tax .

However, in our opinion, this position is not sufficiently substantiated and contradicts the basic principles and principles of taxation provided for by the legislation on taxes and fees, for the following reasons.

In accordance with Art. 8 of the Tax Code of the Russian Federation, a tax is understood as a mandatory, individually gratuitous payment levied on organizations and individuals in the form of alienation of funds belonging to them by right of ownership, economic management or operational management for the purpose of financial support for the activities of the state and (or) municipalities.

Clause 1 of Art. 17 of the Tax Code of the Russian Federation establishes the general conditions for the establishment of taxes and fees and assumes, together with other elements of taxation, the presence of a tax base for the established tax.

When determining the tax base for personal income tax in accordance with paragraph 1 of Art. 210 of the Tax Code of the Russian Federation, all income of the taxpayer received by him both in cash and in kind, or the right to dispose of which he has acquired, is taken into account.

Thus, when determining the tax base for personal income tax on transactions with securities, clause 1 of Art. 214.1 of the Tax Code of the Russian Federation, income received from transactions of purchase and sale of investment units of mutual investment funds, including their redemption, is taken into account.

Articles 23 and 25 of the Federal Law of November 29, 2001 No. 156-FZ “On Investment Funds” define one basis for the redemption of shares - filing an application for redemption of investment shares and provides for the obligation of the management company to pay monetary compensation to the founder of the management only in connection with the redemption of shares on the basis submitted application for redemption of shares.

Clause 4 of Art. 226 of the Tax Code of the Russian Federation provides that tax agents are required to withhold the accrued amount of tax directly from the taxpayer’s income upon their actual payment.

According to paragraphs. 1 clause 1 art. 223 of the Tax Code of the Russian Federation, the actual date of receipt of income is understood as the date of payment of income, including the transfer of income to the taxpayer’s bank accounts or, on his behalf, to the accounts of third parties - when income is received in cash.

However, when the founder of the management submits an application for the exchange of investment shares, the management company does not have an obligation to pay the founder of the management monetary or any other compensation, and, accordingly, there is no possibility of withholding tax at the source of payment.

The exchange of shares occurs within the framework of trust management of the property of the management founder and does not provide for any payments to the management founder, i.e. receiving economic benefits (income) in the form of payment of monetary compensation.

Thus, the founder of the management, when submitting an application to the management company for the exchange of investment shares, performs the operation of exchanging investment shares not on the basis of an exchange agreement provided for in Art. 567 of the Civil Code of the Russian Federation (under an exchange agreement, each party undertakes to transfer one product into the ownership of the other party in exchange for another), and on the basis of a trust management agreement for a mutual investment fund, when the transfer of ownership of the exchanged investment shares from its owner to the management company , or to third parties does not occur.

Based on the foregoing, it should be recognized that when exchanging investment shares in the manner established by Art. 23 of the Federal Law “On Investment Funds”:

— there is no fact of purchase and sale (exchange) of investment shares, since in accordance with the purchase and sale (exchange) agreement, the transfer of ownership is provided for, i.e. payment of monetary compensation to the individual who is the founder of the management;

— there is no fact of payment of income (monetary compensation) to the individual who is the founder of the management, which does not allow the tax agent, in accordance with the requirements of the current legislation on taxes and fees, to determine the tax base and withhold personal income tax from the missing source of payment.

Thus, when exchanging shares, an individual who is the founder of the management does not have an object of taxation and, accordingly, the management company does not have the obligation to fulfill the duty of a tax agent to calculate, withhold and remit personal income tax.

However, accepting the above position, the taxpayer must understand that the tax authorities and the Ministry of Finance have a different point of view on this issue.

3. Is it possible to make an interim payment of income from trust management? In which case?

We draw your attention to the fact that in accordance with Article 14 of the Federal Law of November 29, 2001 N 156-FZ “On Investment Funds”, the rules of trust management of a closed-end mutual investment fund (hereinafter referred to as the closed-end mutual investment fund) may provide for interim payment to shareholders of income from the trust management of property constituting fund .

The procedure for determining the amount of the specified distributed income, the procedure and terms for its payment, the procedure for determining persons entitled to receive income are established by the rules of trust management of closed-end mutual investment funds (clause 36 of the Model rules of trust management of a closed-end mutual investment fund, approved by Decree of the Government of the Russian Federation of July 25, 2002 N 564, paragraph 4 of article 17 of the Federal Law “On Investment Funds”).

So, for example, the Rules may contain the following phrase: “The amount of income on an investment unit to be paid to owners of investment units is equal to _____% of the income on the investment unit for the reporting ________ (quarter, year).

4. Who is the tax agent? Interested in different options: the founder of the remote control is an individual. person (resident), individual person (non-resident), legal entity person - Russian Federation, legal entity person is a foreign organization receiving income from a source in the Russian Federation.

If the shareholder of the mutual fund is an individual who is not a resident of the Russian Federation, then:

In accordance with paragraph 2 of Art. 207, from January 1, 2007, residents are recognized as individuals who stay on the territory of Russia for at least 183 days within 12 consecutive months (that is, the months of residence preceding the current calendar year will also be taken into account).

The object of taxation for income tax for individuals who are not tax residents of the Russian Federation is income received by taxpayers from sources in the Russian Federation. (Clause 2 of Article 209 of the Tax Code of the Russian Federation). Based on clause 3 of Art. 224 of the Tax Code of the Russian Federation, a tax rate of 30 percent is established for all income of such persons.

In accordance with Art. 226 of the Tax Code of the Russian Federation, Russian organizations , individual entrepreneurs, notaries engaged in private practice, lawyers who have established law offices, as well as permanent representative offices of foreign organizations in the Russian Federation, from which or as a result of relations with which the taxpayer received the income specified in paragraph 2 of this article , are obliged to calculate, withhold from the taxpayer and pay the amount of tax calculated in accordance with Article 224 of this Code, taking into account the specifics provided for by this article.

The persons specified in paragraph one of this paragraph are referred to in this chapter as tax agents.

If the shareholder of the mutual fund is a Russian organization, then:

When determining the tax base for transactions with investment shares, the provisions of Art. 280 of the Tax Code of the Russian Federation establishes that income upon disposal (sale, redemption or exchange) of an investment share of a mutual investment fund in the event that the specified investment share is not traded on the organized market, the market price is the estimated value of the investment share, determined in the manner established by the legislation of the Russian Federation about investment funds. Expenses upon the sale (or other disposal) of securities, including investment units of a mutual investment fund, consist of the purchase price of the security (including the costs of its acquisition), the costs of its sale, discounts from the estimated value, the amount of accumulated interest (coupon) income paid by the taxpayer to the seller of the security.

It follows from this article that the organization must independently determine the tax base for transactions with investment shares, as well as calculate and pay the amount of income tax to the budget based on the rate specified in paragraph 1 of Art. 284 Tax Code of the Russian Federation.

When considering the taxation of non-residents, we will accept the assumption that the shareholder is a Cyprus company. If the shareholder of the mutual fund is a Cypriot company that does not have a permanent representative office in the Russian Federation, then:

According to paragraph 1 of Art. 7 of the International Agreement between the Government of the Russian Federation and the Government of the Republic of Cyprus dated December 5, 1998, if an enterprise carries out business activities through a permanent establishment, then the profit of the enterprise may be taxed in the Russian Federation, but only in that part that relates specifically to this permanent establishment in the Russian Federation.

Thus, income received by a foreign organization on the territory of the Russian Federation, which does not lead to the formation of a permanent representative office in the Russian Federation in accordance with Art. 306 of the Tax Code of the Russian Federation, payments are not subject to taxation at source (clause 2 of Article 309 of the Tax Code of the Russian Federation). In addition, in accordance with the norms of paragraph 1 of Art. 7, paragraph 1, 2 art. 5 of the Agreement between the Government of the Russian Federation and the Government of the Republic of Cyprus dated December 5, 1998 “On the avoidance of double taxation in relation to taxes on income and capital”, the profit of a Cyprus resident from business activities carried out in the Russian Federation not through a permanent establishment is not subject to income tax in the Russian Federation . Thus, in this case, with regard to the tax on income of a foreign organization, the management company will not be a tax agent.

At the same time, according to paragraph 1 of Art. 312 of the Tax Code of the Russian Federation, the management company must be provided with confirmation that this foreign organization has a permanent location in Cyprus. Said confirmation must be certified by the competent authority of the Republic of Cyprus.

If the shareholder of the mutual fund is a Cypriot company with a permanent representative office in the Russian Federation, then:

According to Art. 7 of the above-mentioned Agreement, if an enterprise of the Republic of Cyprus carries on business activities in the Russian Federation through a permanent establishment located there, then to this permanent establishment shall be attributed the profits that it would have received if it had been a separate and separate enterprise engaged in the same or similar activities under the same or similar conditions, and acted in complete independence from the enterprise of which it is a permanent establishment. Profits may be taxed in the Russian Federation only in that part that relates specifically to this permanent establishment in the Russian Federation.

Thus, if the register of shareholders includes a permanent representative office of a Cypriot company located on the territory of the Russian Federation, then the interim payment of income on the shares will be recognized as the income of this representative office.

In accordance with paragraph 6 of Art. 307 of the Tax Code of the Russian Federation, foreign organizations operating in the Russian Federation through a permanent representative office pay tax at the rates established by paragraph 1 of Article 284 of this Code, with the exception of income listed in subparagraphs 1, 2, paragraph two of subparagraph 3 of paragraph 1 of Article 309 of this Code . As for the two clauses providing preferential conditions, in our opinion, the income received as a result of the redemption of investment shares and the income received in the event of an interim payment on the shares do not fall under the income defined in paragraphs. 1 and 2 paragraphs 1 art. 309 of the Tax Code of the Russian Federation.

Thus, in our opinion, the income of a representative office from the trust management of property constituting a closed-end mutual fund should be taxed at a general rate of 24%.

If the Management Company pays interim investment income on shares to a shareholder who is a resident of Cyprus, then

When paying trustees interim investment income on investment units, the question arises of how to classify this income. What type of income should the interim payment be classified as? In our opinion, the income indicated in paragraphs is the closest in content. 1 and 2 paragraphs 1 art. 309 of the Tax Code of the Russian Federation. Let's consider these options.

According to Art. 43 of the Tax Code of the Russian Federation, a dividend is any income received by a shareholder (participant) from an organization during the distribution of profits remaining after taxation (including in the form of interest on preferred shares) on shares (stakes) owned by the shareholder (participant) in proportion to the shares of shareholders (participants) in the authorized (share) capital of this organization.

Dividends also include any income received from sources outside the Russian Federation that are classified as dividends in accordance with the laws of foreign countries.

Dividends are also mentioned in Federal Law 208-FZ “On Joint Stock Companies”. From the above, we can conclude that the payment of dividends is carried out by organizations (legal entities) and does not apply to mutual investment funds.

property of the organization, other associations in favor of foreign organizations is named as an object of taxation for foreign organizations operating in the Russian Federation through a permanent representative office. Since a mutual fund is not an association of persons , but an association of property, we believe that equating this type of income with intermediate investment income on shares is incorrect.

Thus, summing up the above, we can conclude that the specified income, in fact, is a payment of income from the trust management of property constituting a closed-end mutual fund (Article 14 of the Federal Law of November 29, 2001 No. 156-FZ “On Investment Funds” ") and for tax purposes will be taken into account as part of other income.

According to Art. 22 of the International Agreement between the Government of the Russian Federation and the Government of the Republic of Cyprus dated December 5, 1998, if the recipient of other income does not have a permanent establishment in the territory where the income was received, then the income is subject to taxation in the territory of the Other State, i.e. the state of which he is a resident.

If the shareholder (Cyprus company) carries out business activities through a permanent representative office, then the interim payment of income on the shares will be recognized as the income of this representative office and taxed at the rate specified in paragraph 1 of Art. 284 Tax Code of the Russian Federation.

5. VAT issue with the management company.

When selling property (investment rights or real estate) transferred into trust management by the founders of the management company, the management company should calculate and pay VAT on transactions subject to VAT (clause 1 of Article 174.1 of the Tax Code of the Russian Federation). So?

We draw your attention to the fact that with the introduction of Article 174.1 into the Tax Code on January 1, 2006, the trustee of a mutual fund is recognized as a VAT payer.

At the same time, there is the position of the Department of the Ministry of Taxes and Duties of the Russian Federation for the city of Moscow, expressed in Letter dated August 30, 2004 No. 24-11/55864 with reference to Letter of the Ministry of Taxes of Russia dated June 23, 2003 N 03-2-06/1/1936/ 22-Ts956 that when carrying out transactions for the sale of goods (works, services) within the framework of trust management, the calculation and payment of VAT to the budget is carried out by the trustee of the mutual fund in the generally established manner at the expense of the property constituting the mutual fund.

Therefore, when selling apartments, VAT is not assessed? Do we impose VAT only on the sale of non-residential premises? YES?

From January 1, 2005, in accordance with paragraphs. 22 and 23 clause 3 art. 149 of the Tax Code of the Russian Federation is not subject to VAT (exempt from taxation) on the territory of the Russian Federation the sale of residential buildings, residential premises, shares in them, as well as the transfer of a share in the right to common property in an apartment building when selling apartments.

Based on clause 3 of Art. 167 of the Tax Code of the Russian Federation in cases where the goods are not shipped or transported, but there is a transfer of ownership of this product, such a transfer of ownership for the purposes of Ch. 21 of the Tax Code of the Russian Federation is equivalent to its implementation .

According to paragraphs. 22 and 23 clause 3 art. 149 of the Tax Code of the Russian Federation are not subject to VAT taxation of transactions on the sale (including by investors) of residential premises (shares in them) under a purchase and sale agreement , as well as on the transfer of a share in the right to common property in an apartment building when selling apartments under a sale and purchase agreement .

When applying this benefit, the object of sale must be a residential premises, which is possible only when concluding a purchase and sale agreement.

Thus, this benefit applies only to transactions involving the sale of residential buildings or premises under sales and purchase agreements.

This benefit does not apply to transactions involving the transfer of property rights to residential premises (shares in them).

This position was expressed in the Letter of the Federal Tax Service Department for Moscow, expressed dated February 22, 2007 No. 19-11/017221.

Also, according to the explanations of the Moscow Federal Tax Service, stated in Letter No. 19-11/106200 of December 5, 2006, the procedure for assessing VAT on apartments is as follows:

In accordance with paragraph 1 of Art. 454 of the Civil Code of the Russian Federation , under a purchase and sale agreement, one party ( the seller) undertakes to transfer the thing (product) into ownership of the other party (the buyer), and the buyer undertakes to accept this product and pay a certain amount of money (price) for it.

According to Art. 429 of the Civil Code of the Russian Federation , under a preliminary agreement, the parties undertake to enter into a future agreement on the transfer of property, performance of work or provision of services (main agreement) on the terms stipulated by the preliminary agreement. The preliminary agreement must contain conditions allowing to establish the subject matter, as well as other essential terms of the main agreement .

Taking into account the provisions of paragraph 8 of Art. 149 and paragraph 2 of Art. 162 of the Tax Code of the Russian Federation, taxpayers, when receiving an advance payment for the upcoming sale (under purchase and sale agreements) of residential buildings, residential premises, as well as shares in them and the transfer of a share in the right to common property in an apartment building when selling apartments, the amount of the advance payment received has the right not subject to VAT.

However, it should be taken into account that the specified exemption procedure does not apply to construction and installation work on the capital construction of residential buildings and residential premises, carried out on the basis of relevant contract (subcontract) agreements by contractors (subcontractors).

Consequently, when the customer-developer transfers to the investor (investors) the costs for the construction of residential premises (or shares of the costs accruing to each investor) in connection with the completion of capital construction of the object (residential premises), invoices are issued to the investor (investors). These invoices reflect the VAT amounts paid by the customer-developer to suppliers of material assets used in the construction of residential premises and to contractors for construction and installation work performed. In addition, the amounts of VAT paid to third parties are reflected, including the services of the customer-developer, which are taken into account in the actual costs of construction of residential premises.

This benefit also does not apply to transactions involving the transfer of property rights to residential premises (shares in them) .

6. Property tax. Does a mutual fund have a property tax base? Article 374 of the Tax Code of the Russian Federation and Art. 11 and 15 of Law 156-FZ give “hope” for a mutual fund not to have this base, right?

Issues related to property tax are regulated by the provisions of Chapter. 30 of the Tax Code of the Russian Federation.

regarding the payment mutual fund property taxes According to the Tax Code (Article 378), only the founders of trust management as taxpayers for corporate property tax . The object of property tax for Russian organizations is movable and immovable property (including property transferred for temporary possession, use, disposal or trust management contributed to joint activities), recorded on the balance sheet as fixed assets , in accordance with the established procedure accounting. At the same time, the tax base in accordance with Art. 375 is defined as the average annual residual value of the property.

But the founder, firstly, owns investment shares . And secondly, according to the regulatory documents of the Federal Financial Markets Service, the value of real estate at the end of the reporting period is determined by the mutual fund appraiser (depreciation is not charged, the residual value is not formed).

However, in accordance with the explanations of the Ministry of Taxation and the Ministry of Finance (for example, the joint Letter of the Ministry of Taxation and the Ministry of Finance No. 01-3-03/666 and N 01-СШ/45 dated June 10, 2004 “On the procedure for taxation of mutual investment funds”, property acquired in within the framework of a trust management agreement, it is subject to property tax for the management founder , in proportion to the value of the investment shares belonging to the management founder (his share in the common property of the shareholders) based on information received from the management company.

At the same time, it is necessary to take into account the fact that Chapter 30 of the Tax Code does not provide for the submission to the tax authorities at the place of registration of the trustee of a tax return on the property tax of organizations for the founder of the management (the corresponding explanations are given, in particular, in the Letter of the Ministry of Finance of Russia dated August 2, 2005 . N 07-05-06/216).

7. Can a management company have other economic activities other than trust management of mutual fund assets?

We draw your attention to the fact that legal norms limit the range of activities of the Management Company permitted by the legislator (clause 2 of Article 38 of the Federal Law of November 29, 2001 No. 156-FZ “On Investment Funds” (hereinafter referred to as Law No. 156-FZ), Part. 3 clause 2 article 2 of the Federal Law of 02/08/98 No. 14-FZ “On Limited Liability Companies”). The management company can combine its activities only with the activities of trust management of securities, management of pension reserves of non-state pension funds and management of insurance reserves of insurance companies.

Also, the market regulator FFMS expressed its position regarding the implementation of entrepreneurial activities by Management Companies in Letter dated April 10, 2007 No. 07-OV-01/7235 “On combining activities for managing investment funds, mutual funds and non-state pension funds with other types of activities” (hereinafter referred to as the Letter).

The Letter indicates that, in accordance with paragraph 1 of Art. 2 of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation), independent activity carried out at one’s own risk, aimed at systematically obtaining profit from the use of property, sale of goods, performance of work or provision of services by persons registered in this capacity in the manner prescribed by law, is entrepreneurial. And based on the essence of the Letter, management companies licensed to carry out activities for managing investment funds, mutual funds and non-state pension funds, carry out activities that are entrepreneurial, but not provided for in paragraph 2 of Art. 38 of Law No. 156-FZ, illegal.

In addition to the above Letter, the FFMS issued a letter dated May 15, 2007 N 07-OV-01/9826 “On the activities of managing investment funds, mutual funds and non-state pension funds”, which contained a list of types of activities that can be carried out by Management Company:

— trust management of pension savings funds — in accordance with Federal Law dated July 24, 2002 N 111-FZ “On investing funds to finance the funded part of labor pensions in the Russian Federation” and Federal Law dated May 7, 2002 N 75-FZ “On non-state pension funds ";

— trust management of savings for housing provision for military personnel - in accordance with Federal Law dated August 20, 2004 N 117-FZ “On the savings and mortgage system for housing provision for military personnel”;

- trust management of mortgage coverage - in accordance with Federal Law of November 11, 2003 N 152-FZ “On Mortgage Securities”;

— trust management of the compensation fund of a self-regulatory organization of appraisers — in accordance with Federal Law dated July 29, 1998 N 135-FZ “On appraisal activities in the Russian Federation”;

- trust management of the endowment capital of a non-profit organization - in accordance with Federal Law dated December 30, 2006 N 275-FZ “On the procedure for the formation and use of endowment capital of non-profit organizations.”

From the above, we can conclude that the Organization can only carry out exclusive activities - management of investment funds, mutual funds and non-state pension funds, as well as other activities, such as: trust management of pension savings, savings for housing of military personnel, trust management of mortgage coverage, funds of the compensation fund of a self-regulatory organization of appraisers, endowment capital of a non-profit organization.

In our opinion, in particular, investing one’s own funds in financial investments is an activity that does not require licensing and relates to the general legal capacity of the Organization.

This position is expressed in paragraph 18 of the Resolution of the Plenum of the Armed Forces of Russia and the Plenum of the Supreme Arbitration Court of Russia dated July 1, 1996 N 6/8, which “when resolving disputes, courts are ordered to take into account that commercial organizations, with the exception of unitary enterprises and other organizations provided for by law, are endowed with general legal capacity (Article 49 of the Civil Code of the Russian Federation) and can carry out any types of business activities not prohibited by law, unless the constituent documents of such commercial organizations contain an exhaustive (complete) list of types of activities that the relevant organization has the right to engage in.”

Also, defining entrepreneurial activity (clause 1 of Article 2 of the Civil Code of the Russian Federation) as the simultaneous fulfillment of the following conditions: independent activity carried out at one’s own risk, aimed at systematically obtaining profit from the use of property, sale of goods, performance of work or provision of services by persons registered in In this capacity, in the manner prescribed by law, it can be assumed that the absence of one of the components of this definition will make it possible not to recognize this type of activity as entrepreneurial. Taking this fact into account, we can assume the following: transferring one’s own funds into trust management of another company may not be considered a systematic receipt of profit and will make it possible to comply with the recommendations of the Federal Financial Markets Service regarding the combination of licensed and other activities by the management company.

Advertisement _

The solution to this issue does not relate to the field of accounting and taxation. However, in our opinion, when answering it, it is necessary to take into account the fact that the activities of the management company are directly related to the level of remuneration (in fact, remuneration is its main source of income).

9. As part of the trust management of mutual fund assets, is it possible for the management company to attract credit (borrowed) funds to be repaid at the expense of the mutual fund property?

We draw your attention to the fact that, according to Art. 40 (Restrictions on the activities of a management company) of Federal Law No. 156-FZ (clause 1, paragraph 7) The management company has no right to:

— to receive, under the terms of loan agreements and credit agreements, funds to be returned from the property constituting the mutual investment fund, not otherwise than for the purpose of using these funds to repurchase investment shares if the funds constituting this mutual investment fund are insufficient. At the same time, the total amount of debt subject to repayment from the property constituting a mutual investment fund under all loan agreements and credit agreements should not exceed 10 percent of the value of the net assets of the mutual investment fund. The period for raising borrowed funds under each loan agreement and credit agreement (including the extension period) cannot exceed three months;

— provide loans at the expense of property owned by a joint-stock investment fund and property constituting a mutual investment fund.

However, when creating a mutual fund, you must understand that borrowing operations are very risky. And the creation of mutual funds serves to form and preserve the population’s savings, and not for high-risk speculation.

10. Is it possible for the founder of trust management to attract credit (borrowed) funds secured by a share to use these funds in the interests of the mutual fund?

In our opinion this is possible. An essential condition of the pledge agreement is the assessment of the collateral. However, in accordance with paragraph 3. Art. 14 of the Federal Law “On Investment Funds”, an investment share does not have a nominal value, and the procedure for determining the estimated value of an investment share, the amount for which an investment share is issued, as well as the amount of monetary compensation payable in connection with the redemption of an investment share are determined by the rules of trust management mutual investment fund, which are subject to registration by the federal executive body for the securities market.

In addition, the value of the investment share may change during the process of trust management. In this case, a change in the value of the investment share after the conclusion of an agreement on its pledge does not affect the rights and obligations of the parties under this agreement. The inclusion in the agreement of a condition on the provision of additional property as collateral to the pledgee in the event of a decrease in the value of the investment share will not be the basis for presenting a requirement for early fulfillment of the main obligation in accordance with Art. 351 Civil Code of the Russian Federation.

An exception to the general rule regarding changes in the value of an investment share is a securities pledge agreement concluded to ensure the borrower fulfills his obligations arising from the loan and credit agreement. Article 813 of the Civil Code of the Russian Federation states that “if the security is lost or its conditions deteriorate due to circumstances for which the lender is not responsible, the lender has the right to demand from the borrower early repayment of the loan amount and payment of interest due, unless otherwise provided by the agreement.” A decrease in the value of pledged investment shares represents a deterioration in the terms of the security of the loan or credit agreement, therefore, in this case, the pledgee has the right to demand early execution of the main agreement, and in case of non-fulfillment, foreclose on the pledged property.

We would also like to draw your attention to the fact that the FCSM Resolution No. 20/PS dated 06/07/2002 provides not only for maintaining a register of owners of investment shares, but also for opening personal accounts of “registered persons”. Registered persons, in addition to owners of investment units, nominee holders, pledgees of investment units , also include a trustee. For registered persons, the Regulations provide for the opening of personal accounts of registered persons, which include, respectively, the personal account of the owner, the personal account of the nominal holder, the personal account of the pledgee and the personal account of the trustee (clause 4.1). Pledgee's personal account is a personal account opened for the pledgee to record the right of pledge on investment shares.

Author: Irina Nesterova, acting Head of the Audit Department of Exchanges, Extra-Budgetary Funds and Investment Institutions AKG ARNI Polaris International

How to make money on shares

It is impossible to withdraw property and money invested in a mutual fund. But the shareholder has two ways to exchange his shares for money: redeem the shares or sell them to another investor.

Redemption of shares. In this case, the management company compensates the cost of the redeemed shares with money.

Sale to another investor. The shareholder has to find a buyer and negotiate a price with him. Some shares are limited in circulation, so they are not so easy to sell.

The possibility of sale depends on the investors for whom the shares are intended. If the mutual fund is for qualified, experienced investors, then it is not possible. If it’s for the unskilled, it’s possible.

Units for non-qualified investors are called unrestricted units. Shareholders can freely dispose of them: sell, pledge, give, leave as an inheritance. Anyone can freely buy such shares, receive income from them and sell them at any time at the market price.

On shares, like on any other securities, you can make money speculatively: buy when they become cheaper and sell when they rise in price.

The share has a current value and a market value. The current value is recorded in the documents; this information can always be found on the website of the management company. The market value is slightly different from the current one and depends on many factors, including the general information background. Here's how you negotiate.

I'll explain with an example. Let's say you own shares of a closed mutual fund, its main assets are residential real estate. Statistics on the real estate market come out, and it turns out that the market has declined. This means that the cost of housing owned by the fund will decrease. Hence, the value of your shares will also decrease in the next couple of months. If at this moment you decide to sell your shares, their market value will be lower than the current one.

Another example: the mutual fund whose shares you purchased invested in shares of oil companies. The cost of a barrel is rising and dragging the entire oil sector with it. If at this point you decide to sell the shares, they will be bought above the current price.

Alternative to mutual funds

As an analogue of mutual funds, you can consider ETF (Exchange Traded Fund). The principle of operation is similar , but ETFs have an order of magnitude lower management fee , there are more of them and it is easier to buy them . The entire process is similar to a regular stock purchase through a broker. ETFs are traded on regular exchanges .

The best option is to invest money in index funds . These ETFs replicate a basket of the corresponding index, and each of their shares is essentially a portfolio of shares of ordinary companies .

A few examples:

- SPDR S&P 500 ETF (ticker SPY) – largest fund, under the management of more $250 billion. With high precision copies American index S&P 500. The probability of bankruptcy is almost zero since the fund is essentially reflects state all US economy. Average annual profitability order 9-10%, in the moment share price grew up approximately by 660%;

Open an account with Just2trade and buy ETFs

- SPDR Gold Trust (GLD). Price shares are very close to the price of yellow metal, the difference is within a few percent. Owns more how 1000 tons of gold, this is an ideal option for investing in this precious metal without physically purchasing it. At the moment the cost grew by 325%.

- iShares PHLX Semiconductor (SOXX). Allows you to quickly invest in the securities of companies operating in the field production semiconductors. Without this it is impossible to create high-tech products, therefore sector stable growing. In the fund basket more than 100 companies so it is a kind of indicator of the state of the industry.

If we compare which is better - ETFs or investing in mutual funds, then ETFs benefit primarily due to the manager's commission . It is at least 10-15 times lower .

As for which brokers you should use to invest in shares of these ETFs, I recommend taking a closer look at the companies in the table below.

| Company | Just2trade | United Traders |

| Minimum deposit | From $100 | $300 |

| Commission per cycle (buy + sell trade) | 0.006 USD per share (min. 1.5 USD), 0.25 USD for each application. that is, per lap – $3.50 | “Beginner” tariff – $0.02 per share Average $4 per round |

| Additional charges | The ROX platform will cost at least $39/month. (for the American market), for an additional $34.50 they connect Canada/TSE, Level II On the over-the-counter market, the additional fee is 0.75% of the transaction volume (minimum $30), in the case of dividends - 3% from the issuer (minimum $3) | On the Day Trader tariff, they charge $60/month for the Aurora platform, free on other plans |

| Account maintenance cost | $5/€5/350 rub. reduced by the amount of the commission paid | — |

| Leverage | for Forex Up to 1 to 500 for stocks up to 1 to 20 (day) to 1 to 5 (night) | 1 to 20 on the Day Trader tariff, this is the maximum leverage (daily) |

| Margin call | -90% | Standard -30% of the deposit, in technical terms. support can be set -80% |

| Trading terminals | MetaTrader5, ROX | Aurora, Sterling Trader, Fusion, Laser Trader, Volfix.Net, Pair Trader |

| Available markets for trading | Forex, American, European and other stock markets, cryptocurrency | American and other stock markets, more than 10,000 assets in total, cryptocurrency |

| License | CySEC | Lightweight license from the Central Bank of the Russian Federation |

| Open an account | Open an account |

Types of funding sources

You can attract money from external and internal sources. To understand which of the possible tools is the most suitable, ask yourself 4 questions:

- Why and how much money do I need? For how long? What result do I plan to get?

- Where can I get them?

- Which resource will cost me the least? Make the list in ascending order of cost.

- What will be the return from using each tool (or combination of them)? Calculate your profits and make a rating - from ineffective to profitable.

Such a simple analysis will allow you to choose a resource that will bring the greatest results at lower costs. Let's take a look at these tools.

Activity of the domestic market

Let's look at how things are in our country. Despite the turbulent recent years, we can say that the situation is quite good. Several random structures can be considered:

- Mutual Fund "Petr Stolypin". It is one of the oldest representatives in our country. It was founded already in the last millennium, or more precisely, in 1997. It positions itself as a fund for investors who want maximum profit and are willing to accept the risk that comes with it. Over the past three years, it has posted a return of 57%. During the same time, the Peter Stolypin mutual fund increased the value of its net assets by 220%. Data is for the end of 2021.

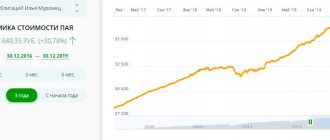

- Mutual Fund "Ilya Muromets" This is a fund created under the auspices of Sberbank. Over the past three years, it has shown a profitability of 27%. The value of net assets increased by 188%. Mutual Fund "Ilya Muromets" specializes in working with bonds of the municipal, corporate and public sectors.

In general, if you do not have significant experience and desire to take risks, then you can pay attention to investing in Sberbank mutual funds. Their reviews are mostly positive, and their profitability also deserves attention. Although, of course, this is far from the only bank that offers such conditions. Perhaps someone would prefer investing in mutual funds of VTB or another financial and credit institution. If you have a desire to take risks and opportunities for this, then why not take advantage? Moreover, the yield on the main proposals, if not higher, is at least equal to funds from deposits.

Mutual fund and share: pros and cons

Like any other way of making money on investments, investing in mutual funds has its positive and negative sides. You can only assess whether this type of investment is right for you after studying all the pros and cons.

The main advantages of mutual funds are as follows:

- Accessibility to the general population due to the minimum entry threshold (in some mutual funds it is only 1000 rubles).

- Competent management of funds (of course, provided that the management company was chosen correctly). You don't have to become a financial expert to make a profit.

- Funds held in a mutual fund are not subject to taxes. Only if you want to withdraw your savings from the fund will you have to pay income tax. If you do not withdraw funds within three years, you will be entitled to a tax deduction (the maximum amount for deduction is 3 million rubles per year).

- The probable profitability of mutual funds is much higher than that of bank deposits.

- High liquidity of shares (in open-end funds), i.e., if you wish, you can sell your share within 1–3 days and receive money.

Mutual funds also have significant disadvantages:

- To choose a management company, you need certain knowledge, and even an analysis of the work over the previous few years is not a guarantee of successful results in the future.

- During a serious crisis, the profitability of mutual funds goes into the negative.

- Mutual fund funds do not have state protection, like bank deposits.

- The state controls and imposes certain restrictions on the formation of the fund's asset portfolio.

- With a general drop in prices on the market, a mutual fund cannot get rid of all depreciating assets and convert them into money, i.e. in such a situation you will not be able to withdraw your funds from the fund immediately.

- The management company receives a monthly fee for asset management, regardless of the profitability of the mutual fund.

IMPORTANT! Despite the fact that the property of mutual funds does not have state protection, like deposits, it is protected in a different way. The fact is that all the fund’s assets are located in a specialized storage facility - a depository. In it, all transactions with funds are recorded, and records of shareholders are kept. If something happens to the management company, you will not have to look for evidence that you transferred money to it.

Summary

Mutual funds can be considered as a replacement for traditional bank deposits . It is realistic to get approximately the same reliability , but 1.5-2 times greater profitability. At the same time, you will not be limited in the time of purchase and sale of fund shares. The only difficulty is choice , but this issue is easily resolved. BCS offers profitable mutual funds with high returns.

As for ETFs , this is also a good option for investing without excessive risks . You can buy their shares through a broker, and you can actually get a return of 8-10% per annum. It is difficult to cover all issues related to investing in mutual funds and ETFs in one article. I will be happy to answer any remaining questions in the comments.

With this I say goodbye to you, see you soon. And don’t forget to subscribe to blog updates, so you’ll be among the first to know when the next article is published.

If you find an error in the text, please select a piece of text and press Ctrl+Enter. Thanks for helping my blog get better!

Disadvantages of mutual funds

Mutual funds do not guarantee any future returns. Even if over the past few years the fund has consistently shown excellent results every year in terms of profit (growth in the value of the share), in the next year it may work in the negative (well, maybe make a small profit).

The activities of the fund are strictly regulated by the state. Those. management companies are prohibited from carrying out operations not provided for in the fund’s charter. Let’s say in an index fund, when the general market falls, the management company is prohibited from getting rid of falling assets, because The charter states that the fund must consist precisely of the shares included in the index and in exactly the same proportion. That's why. when others can sit out “bad times” in money, the shareholders of such a fund will suffer losses as long as the market falls.

Additional expenses borne by the shareholder. This includes entry and exit fees, i.e. for a purchase you will be charged a so-called “premium”, for the sale of shares - a “discount”. Typically, the “premium” is 1-3% of the amount of shares purchased, the “discount” is 1-1.5%. If you own shares for several years (usually from 3 years), then you do not lose anything when selling. Management company o.

Please remember to include fund asset management fees. They usually amount to 1-3% per year, regardless of the result that the company received. Profit or loss is the same - you will be charged a certain amount for management.

Taxes. You are subject to 13% tax on profits received. The tax is taken at the time of sale. As long as you own the shares, you will not be taxed. And although the tax is taken from the profit received from any activity (investment), for many investments it is lower or even absent compared to mutual funds. If anyone is interested, read in more detail.....

Useful tips for profitable investing

Based on my own experience, I will give some recommendations to beginners:

- Mutual funds are not capable of accelerating capital . The profitability will exceed the bank one, but not a single fund will give a profit of 1000+% per year. Even aggressive management strategies yield profits of 20-40%. This threshold is rarely exceeded.

- If you choose this direction, your planning horizon should be calculated in years . There is no point in buying shares in order to resell them in a couple of months; the income will be small. You will feel the effect if you hold the shares for at least 2-3 years. There is one more advantage - if shares were purchased after January 1, 2014, then if they are held for more than 3 years, personal income tax is canceled upon redemption.

- Use it foreign exchange funds. The dollar remains stable, given the tendency of the ruble to depreciate, you can get a multiplier effect from investing. The income will consist of an increase in the value of the share and the dollar in relation to the national currency.

- Funds that focus on bonds are more reliable , but their growth potential is lower than that of mutual funds focused on investing in stocks .

- I recommend not to get involved with interval and closed-end funds. Restrictions on the time of sale and purchase of shares can cause a lot of inconvenience .

- Invest only that part of the funds that your family budget will not feel the loss of. It is better not to touch this money for several years. Never take out a loan or invest your last savings in mutual funds .

If possible, I recommend purchasing additional shares on a regular basis ; open-end funds allow you to do this. As a result, without noticing it, you will collect a solid portfolio.

Pros and cons of investing in mutual funds

Investments in mutual funds attract some and repel others.

Profitability and risks

What is the attractiveness of investing in such institutions?

The arguments for and against are as follows:

- the opportunity to earn good money (compared to bank deposits);

- you can exchange shares of one mutual fund for shares of another in the same management company;

- minimum investment management, time saving (when compared with securities);

- protection of shareholders (the management company must be licensed, risky operations, as well as the intended use of shareholders’ funds, are controlled by independent bodies);

- reporting on the structure and composition of assets;

- low entry threshold.

Disadvantages of investing:

- no one guarantees profitability, there is a risk of loss;

- The management company may lose its license, and then it is necessary to find a new management company;

- In order for investments to generate income, it is necessary to hold funds for at least 2–3 years.

Underwater rocks

The interests of investors are protected by the state: investment management and preservation are carried out by different organizations (MC, depositary, registrar and auditor), and control over all participants is exercised by the Federal Service for Financial Markets)

But the state is not responsible for the results of the mutual fund’s activities. Investment funds undertake to place the following text in advertising brochures: “Past performance results do not guarantee future income. The state does not guarantee the return on investment.”

Investor protection

Mutual funds are protected by legislation regulating the securities market - the management company will not be able to abscond with your money. The property of a mutual fund is separate from the property of the company itself; it cannot appropriate it (the Central Bank of the Russian Federation strictly monitors this), and in case of violation, the management company will simply lose its license. By the way, even if something happens to the management company, the fund’s property will remain intact: the fund’s assets will be distributed among all investors.

The management company cannot, of its own free will, suddenly change the strategy of the fund, turning a conservative mutual fund into an aggressive one. If, nevertheless, the manager wants to change the strategy, the initiative is agreed upon with the Central Bank of the Russian Federation.

So the investor can be calm: everything works like clockwork.

How to choose which mutual fund to invest money in with the greatest benefit: step-by-step instructions

It is quite difficult to choose a profitable mutual fund for investment, since last year’s profitability is not a guide. The same applies to net asset value indicators, alpha, beta and Sharpe ratios. They show the success of investing in the past.

The market and the fund are complex systems that cannot be controlled. The work of an investment fund depends not only on economics and politics, but also on the professionalism of the people who make important decisions. But there are points to consider when investing in a fund.

What to look for when choosing a mutual fund

There are significant criteria for investing in the fund. Go through them all:

- the amount of commissions (more details in the mutual fund commission section);

- the investment fund has been operating for at least 3 years;

- relative returns over several years of operation are higher than the market index;

- dynamics of capital growth (more investors, stronger reliability of the investment fund).

Where can I buy

Investing can be started either at the office of the management company or through its agents. The difference lies in the amount of the entry threshold. In management companies it is much higher (since the work is focused on large investors and fund management).

Pleasant: you won’t be charged a premium here. The agent’s work is aimed at interacting with old shareholders and attracting new ones.

List of leading mutual funds in Russia

Popular mutual funds in terms of investment volume for [year] year include: VTB Capital, Sberbank, RSHB Asset Management, Gazprombank, Raiffeisen Capital, Otkritie, URALSIB, Aton Management, TRANSFINGROUP.

Rating of mutual funds by reliability and profitability 2019

As in all operations involving the investment of funds, investment funds have risks, however, there are areas and industries in which investments almost always bring good profits to investors.

As of November 2021, the most reliable and fastest growing funds are:

- Sberbank - Biotechnologies Sberbank. Profitability - 10.96%

- Alyonka – Capital. Profitability - 8.58%

- URALSIB Global innovations. Profitability - 8.22%

- System Capital - Mobile. Profitability - 7.81%

- BKS Technologies of the XXII century. Profitability - 7.38%

- System Capital - Biotechnology. Profitability - 7.30%

- Kapital-Information technologies of the future. Profitability - 6.28%

- VTB – Future Technologies Fund. Profitability - 5.98%

- Alfa-Capital Technologies. Profitability - 5.96%

- Raiffeisen – Information technologies. Profitability - 5.94%

All of the funds listed are open-ended, so we can say with complete confidence that investments in this type of mutual funds are the most profitable and reliable.

We recommend reading: rating of the Top 10 most profitable and reliable mutual funds in Russia. Overdraft - what it is in simple words and how to use this service correctly. See information here.

TOP 5 debit cards with overdraft credit line: https://wikiprofit.ru/finances/cards/debetovye-karty-s-overdraftom.html

Combined mutual fund

A combined mutual fund is a new instrument that appeared on the Russian market at the end of 2021. In such a mutual fund you can include anything except cash. For example, airplanes, private roads, collectible cognac, stamps and other collectibles, works of art, options on oil and wheat, precious metals and stones, cryptocurrencies, foreign deposits. It all depends on what the management company has written down in the fund’s rules.

But there is a nuance: property, with the exception of real estate, must be stored in a depository. Therefore, it will not be possible to “pack” a factory for sewing sneakers into the fund, but the sneakers themselves will be fine. To do this, you need to register the sneakers in the remote control in advance and agree with the depository on storage, and the mutual fund will have to buy the sneakers themselves from the factory as goods.

Management companies are not yet in a hurry to purchase everything for combined funds and stick to more traditional financial instruments.

On the first results of the work of combined funds in the specialized depository "Infinitum"PDF, 233 KB

Don't look at profitability

From the word absolutely. Profitability is such a marketing tool. It shows how much the fund has earned in the past, but does not say anything about future profits. This is not a bank or a bond.

The returns of previous years will not give you anything. Last year, the mutual fund lost 20% in value, but this year it entered the top ten most profitable - these are normal tricks on the market. Similarly, this year the fund may turn out to be extremely profitable, and you enter at the peak - and in the future you will lose 30% of the initial investment (pah-pah).

Profitability is a reference indicator, and it needs to be considered in dynamics. As you look at the graph, ask yourself these questions:

- The profitability of the mutual fund is stable or the chart is “twitching”;

- how large are the drawdowns and can you psychologically survive them if they occur again and again;

- how does the yield curve compare with the benchmark chart and does it deviate too much from it;

- whether trend movements are observed on the chart and whether you have hit the upper peak.

If the answers suit you, go ahead and invest.

And here’s another interesting article: How much money do you need for investment?

By the way, I recommend assessing profitability over an extended period - at least three years. During this time, the chart will display all the managers’ mistakes, if any, and the shortcomings of the trading strategy. Well, plus you will understand whether the fund is profitable in the long term or whether you can make money on it only at a certain stage.

Mutual Fund Commissions

Mutual funds charge a commission for managing funds. It comes in 3 types:

- allowance. Charged when purchasing a share (up to 1.5%);

- discount. Charged upon sale (the more you hold the deposit, the lower its value);

- for management. The value ranges from 0.3 to 1% of net asset value annually.

As a result, you can leave 1-3% of the profit. To reduce fees, it is worth holding funds for at least 3 years. The same applies to the premium if the investment was for a large amount. Federal Law No. 156-FZ “On Investment Funds” provides for restrictions: the maximum amount of the premium is 1.5% of the calculated value of the share, the discount is 3%.

Investments can deduct 13% of your income tax if you redeem the share with profit with a maturity of less than 3 years. After this time has expired, the tax office will provide you with a tax deduction in the amount of 3 million rubles annually. The longer you have funds in an investment fund, the more significant the deduction amount.

About their appearance

It should be noted that this instrument is considered very young. He is not even a century old. The first mutual funds appeared in the USA in 1924. To tell the truth, before this there were many different offices and funds that performed a similar function. But they worked individually with each client. And they even accepted very small deposits. But it was not always possible to work effectively with small capitals. Because of this, large players raised the entry threshold. And small offices could not manage the funds that were entrusted to them with maximum efficiency and profitability. At the same time, there was no desire to lose investors who could boast of millions. Therefore, such a structure as a mutual investment fund (UIF) was developed. But first they had a cool meeting. This was largely due to the stock exchange and economic crisis, the lack of a legislative framework, as well as a lack of understanding on the part of potential clients of the principles of their functioning. And on top of all this is the simple mistrust of private investors. What can we hide here, the Americans then believed that it was better to store paper shares in a box at home. Yes, all those stories about American families suddenly finding their grandfather's old Coca-Cola shares hidden away are not fiction. These funds were appreciated only after the Second World War. The real dawn came in the mid-1950s. Since then, both the number of funds themselves and the funds they accumulated have increased not only in the United States itself, but throughout the world.

Mutual Fund assets

A mutual fund is considered a property complex, and not a legal entity, and cannot perform any actions on its own (for example, participate in trading on the stock exchange). A mutual fund is investors' funds, a set of assets. These include:

- securities of various enterprises, including banks;

- money in accounts;

- cash reserves (which are necessary for current payments to investors upon redemption of shares).

Securities and funds in accounts make up the fund's investment portfolio. And by purchasing one share, an investor acquires a certain share of all securities that make up the mutual fund’s portfolio.

About state control

This plus stands apart. The activities of mutual funds are constantly monitored by authorized government agencies. Thanks to this, the funds provide all their financial indicators that cover their activities, such as profit, loss, operating expenses, and the like. Thanks to this, it is not difficult to obtain comprehensive data on the situation with each individual structure. The fact of state control plays a very important role. It is no secret that there are many people in the world who would not mind making money. And given the financial illiteracy that is rampantly blooming in the vastness of our country, there is a high probability that someone dishonest will take advantage of the situation. But this will undermine confidence in the system even more, and this despite the fact that it is not in the best condition right now. Therefore, you have to keep your finger on the pulse and control the situation very tightly.

Alternatives to investing in mutual funds (ETFs)

There is another investment tool - ETF. He, like the mutual fund, uses collective investment of funds.

Differences:

- you need a brokerage account or IIS;

- the activity of the management company is more passive: it does not strive to beat the index;

- commission is lower than mutual fund;

- It is believed that ETFs are more transparent: control not only from the Central Bank of the Russian Federation, but also from foreign authorities.

Not suitable for everyone: Some government employees cannot own foreign securities.