Investment greetings, friends! I’ll say right away: don’t believe those who say that the era of mutual funds is over. Mutual funds are like Lenin - they were, are and will be. And investing in mutual funds will always be on the list of a successful investor. The reason is the convenience of this financial instrument. Well, where else can you invest in a bunch of assorted assets in one fell swoop and you won’t get anything for it (well, except for profit - there will be profit). But you also need to buy fund shares wisely, otherwise you can lose both money and the desire to invest somewhere. And to prevent such troubles from happening to you, I will tell you 7 rules for investing in mutual funds. I hope they will help make investments more consciously profitable. Go!

How I learned about mutual funds and decided to try investing money

My name is Oleg Mazurenko, I live in St. Petersburg. I would like to share my own experience of investing in mutual funds (hereinafter referred to as mutual funds). Now I invest in mutual funds of Sberbank - the profitability is quite high, which suits me. I will use my own example to tell you how to invest money in Sberbank mutual funds, but only because this is how it happened historically. You can choose any funds presented on the market, the essence will not change. But let's go back to basics.

Beginner's first steps

It started back in 2009, just as the financial crisis was flaring up, and at that moment I had quite a decent amount of cash. There was a great desire not only to save funds, but also to increase them. First of all, I opened a deposit at Societe Generale Vostok bank (now Rosbank), where they offered me the service of investing in mutual funds of the Troika-Dialog company.

And on May 19, 2009, I bought shares of six mutual funds (Oil and gas sector, Consumer sector, Electric power industry, Dobrynya Nikitich, Natural resources, Telecommunications and technology) in the amount of 50,000 rubles each. every.

Screenshot from the deals archive

I would like to draw your attention to the fact that five days passed from the date of submitting the application through the bank to the actual purchase of shares. Therefore, I then went directly to the Troika-Dialog office and worked with them, and not through my bank. The period from payment of the application to the actual purchase has been reduced to three days.

Mutual funds vs. ETF. What is the difference?

In reality, the ETF instrument is considered more popular than the old mutual funds. If you compare these tools, what are the advantages of the two investment methods?

- ETFs are more liquid and easier to buy. We buy through a brokerage account or buy on an IIS, get a tax break. We buy mutual funds at the office of the management company, through an agent. It is not possible to buy mutual funds on an IIS - this is a minus.

- Mutual funds are actively managed, most often managers try to outperform the index, investment funds and exchange-traded funds follow the stock index.

- Commissions - for mutual funds 3-5%, not counting premiums and discounts, for ETFs the figures are lower - less than 1%, without additional surprises.

- Mutual funds have a bad habit of suddenly changing investment regulations, as a result of which money is directed to other assets, while investors do not even know about it. This is not the case with ETFs.

Many people think that this tool is outdated. When it comes to investing in exchange-traded instruments, there are two alternatives on the surface:

- ETFs, and generally a better option;

- acquisition of various assets, stocks, bonds on an individual investment account for long-term investment, on our own to obtain a tax deduction. Anyone can do this, the main thing is skills and experience.

When are mutual funds profitable? If you are looking at real estate, this tool will be unique; it is a kind of analogue to American rates.

Risk and return assessment. How to choose a mutual fund for investing

How I chose mutual funds to purchase shares from a large list of funds that at that time were managed by the Troika-Dialog company. In 2009, I completed my MBA program, where we were taught that investments should be diversified, that is, do not put all your eggs in one basket. I used the data that Troika presented on the website for each fund, these are “Standard Deviation”, “Sharpe”, “Sortino”, “UP” ratios, etc. Their description is presented in the picture.

This is taught in university financial courses, but you can learn it yourself

I have compiled a table with these ratios for all funds (they describe the degree of risk, projected return, risk/return ratio, etc.). In the table, indicators that promised investment returns with the least risk are highlighted in blue. As a result, I chose mutual funds that had the best indicators.

The financial crisis hit our country in the third quarter of 2008 and the minimum value of shares was in mid-November 2008, as shown in the picture:

I managed to buy shares at the bottom.

I entered into shares only at the end of May 2009, that is, when the market had already begun to grow.

Trading principles say: “buy when the price falls and sell when the price rises.” But few people follow this.

As a result, by December 2009, the value of the shares of my mutual funds increased and I received an income (less income tax) of more than 100,000 rubles, which amounted to about 60% per annum. It is clear that the positive financial result of one’s own investments is inspiring, but the country’s economy has already begun to emerge from the crisis, and therefore such profitability could no longer be expected.

Real cases

Case 1. 163 thousand rubles in 15 years

Hired worker Vasily Petrov decided to invest 200 thousand rubles, or $3,000 in dollars, into a mutual fund. He can invest 15 thousand rubles monthly and wants to receive a return of 20% per annum.

Vasily invests $200 per month. That is, per year - $2400. To get $2,000 of passive income per month with a return of 20% per year, he needs to create a capital of $120,000. Next, we calculate using an investment calculator.

| Result for 5 years | |

| Investments | 12600$ |

| On an investment account | 16800$ |

| Net profit | 4200$ |

| Result for 10 years | |

| Investments | 24600$ |

| On an investment account | 59000$ |

| Net profit | 34400$ |

| Result for 15 years | |

| Investments | 36600$ |

| On an investment account | 156700$ |

| Net profit | 120100$ |

After 15 years, the goal has been exceeded. A capital of $150,000 allows him to receive a monthly income of $2,500, while the amount in the account will not decrease.

Case 2. 68 thousand rubles of income for 1 year

Office worker Anatoly invested 150 thousand rubles in a mutual fund, and over the course of a year he replenished the account by 2,000 rubles per month. Expected return 30% per annum. Anatoly’s net income for the year amounted to about 76 thousand rubles.

Total capital: 226 thousand rubles.

Basic concepts. What you need to know about mutual funds

Therefore, I began to analyze the dynamics of changes in the value of shares, as well as the expenses that I incur for this type of investment. This is what I want to share with you.

I note that a lot of time has passed since 2009, Troika-Dialog was bought by Sberbank, which, of course, increased the security of investments, but if earlier in Troika’s offices you could get acquainted with their analytical forecasts and talk with consultants, now you can talk in Sberbank there is no one to talk to, the specialists sitting in the Premier departments (where they serve investors), alas, do not understand anything about investments, so don’t even ask them which mutual funds to invest your funds in.

Now some information about what mutual funds are; I present the data as of July 2021, since many funds have already either merged or ceased to exist.

So, mutual funds are divided into several categories:

- Open and closed. Anyone can enter (buy a share) in the first, but I don’t even know how to enter in the second. Previously, there were also interval funds in which you could enter (buy shares) and exit (sell shares) only at a certain time interval and, as a rule, this interval was once a quarter. You can enter and exit open mutual funds at any time, taking into account the duration of the procedure for repayment or exchange of shares and the working days of the management company.

- Bond funds, stock funds, mixed investment funds (the fund buys both bonds and company shares) and funds of funds , and the latter are slightly lower.

But this is a classification. Let's go back to the very beginning. What is a mutual fund?

A mutual fund is a commercial company that uses the shares we buy to purchase securities ; the names of the funds make it clear that these are bonds of companies and state entities, shares of enterprises, and both for “mixed” ones. Funds of funds acquire derivative foreign financial instruments: depositary receipts, etc. Accordingly, the value of the fund’s shares depends on the current value of the fund’s securities on the current date (the so-called NAV - the amount of net assets), that is, if the securities grow, then the fund also grows the cost of your share.

Exchange differences

I would like to draw your attention to the fact that we buy shares for rubles and upon redemption of shares we receive rubles. But some mutual funds are practically denominated in foreign currency, since they buy securities for foreign currency. Of the bond funds, these are the “Eurobond Fund” and the “Global Debt Market Fund”, from the stock funds, partly the “Global Internet Fund” and all funds of funds (America, Europe, Emerging Markets, Gold, etc.).

What is the danger: if in foreign currency the value of securities increases, but if the exchange rate of the ruble decreases, the value of the share may decrease significantly. Previously, in the “investor’s personal account” of Troika Dialog, when viewing the dynamics of the value of a share, one could see both in rubles and in dollars. Sberbank now gives only in rubles and it is very difficult to actually estimate the profitability of a mutual fund denominated in foreign currency.

Don't go in at the peak

Well, you don't have to do that. See. that the mutual fund entered the top 10 income funds, and before that it was hanging out in the hundredth position - run away from there. There are no miracles in the stock market - only luck. But he can’t always be lucky.

It is better to choose a mutual fund with a clear strategy and predictable income. Let it not depend on external factors - or it does, but you understand the principle (for example, “oil” mutual funds lose in price along with oil, and the IT sector grows with the release of a new iPhone and an increase in the capitalization of Bitcoin). And enter when shares are cheaper. This way you will make money on the rise and buy more shares for the same money.

Service fees and taxes

What you need to pay attention to in order to reduce your costs for purchasing and redeeming shares. The management company of the mutual funds lives on the commission, which is withdrawn when purchasing shares and when they are redeemed (that is, when withdrawn into money).

My little trick for saving

At the moment, the lowest commission for entering and exiting bond funds is 0.5%. Therefore, when I enter, I buy shares of the “Advanced Bond Fund” (it used to be called the “Risk Bond Fund”), then exchange its shares for the stock fund in which I intend to invest. In the same way, I redeem shares, that is, I withdraw money by changing the stock fund to a bond fund, and then redeem the shares.

Personal income tax from mutual funds

Thus, I lose 0.5% at the entrance and 0.5% at the exit, but plus 13% of income tax, which Sberbank withdraws if, according to its calculations, my profit is included in the withdrawal amount. According to Sber, how much personal income tax should be withdrawn, I don’t know, since I withdraw funds as needed, but based on the assessment of the value of the share at the time of withdrawal and the amount of funds received into my account, it is only 1-2% of the account. It is clear that if I had redeemed all the shares, then the entire personal income tax would have been withheld from the profit.

Previously, personal income tax was withheld not when redeeming shares, but when exchanging shares of one fund for another. That is, you invested 100,000 rubles in one fund, the value of the shares increased to 120,000 rubles, and you exchange all the shares for shares of another fund, the state took away income tax from 20,000 rubles (no commission of the management company is charged when exchanging shares, only on purchase and redemption ). If the value of your shares in the new fund decreased, then it was your problem, no one returned the tax. Now this absurdity has finally been eliminated; we pay personal income tax only on profits and only when withdrawing funds (redeeming shares).

Hold shares for 3 years

Firstly, at such a distance the best properties of the mutual fund appear, and it begins to earn money.

Secondly, you won't have to pay tax. Yes, yes, the same personal income tax. If you sell shares for more than you bought them and do it after 2014 (and everyone now does it after 2014), then you will have to pay 13% of the profit. Of course, they can be returned, but that's a completely different story. But after a 3-year period of ownership of shares, an individual is exempt from paying income tax, even if he earns 100% of the profit.

Thirdly, most management companies will not charge a “discount” (i.e. commission) after 3 years of holding shares. Some companies charge up to 2% of the sales price - you have to admit, together with tax, this is quite expensive.

In short, hold on to your shares as long as possible - like a good French wine.

How much can you earn on mutual funds? Theory and practice

Now, after a little educational program, I’ll tell you how I make money investing in mutual funds (how to save on input and output was discussed above). All mutual funds are divided into three groups according to the risk/return ratio: low risks/returns, medium risks/returns and high risks/returns.

The higher the risk, the higher the return, and vice versa.

How do I make money on mutual funds? Seasonality analysis

There are sectoral mutual funds of shares, such as Electric Power, Natural Resources, Telecommunications and Technology, Consumer Sector, they have seasonal dynamics due to the fact that shareholder registers are closed in the spring and dividends per share are declared; as a rule, by this time the value of company shares is falling ( holders of shares sell them, fixing profits) and, consequently, shares of the corresponding mutual fund. Then at the end of summer the shares begin to rise again, and the value of the shares along with them. Above, I told you that I began to analyze the dynamics of the value of shares.

It is clear from the chart that it is more profitable to enter in the summer at the lowest point of NAV (buy cheap!)

The figure shows graphs of the value of the Natural Resources Fund by year and the value of the share on the 15th day of each month (after 2015, everything was already clear to me, and I did not engage in such analysis).

As a result, my strategy is very simple: in February-March we leave the sectoral fund, I exchanged its shares for shares of the bond fund, in August-September we return to this fund.

I used the bond fund as an option to take profits and wait to re-enter the sector fund. The alternative would be to exit by redeeming the shares, but then I would lose the management company commission and income tax.

Stock funds or bond funds?

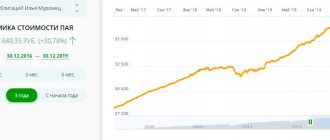

In principle, the Perspective Bond Fund itself gives a return higher than a bank deposit - it is 12-14% per annum. That is, while I was taking profits before returning to high-yield funds, my profits were still growing in the bond fund. Its return over three years was 42%:

Dynamics of profitability. As you can see, there are no drawdowns. If you buy shares of a bond fund, you will always sell them for more.

Moreover, even during the crisis of 2015, the value of shares fell, and then recovered and continued the same dynamics.

In principle, those who do not want to take risks and are willing to be content with a profit that is not much greater than a bank deposit can limit themselves to one bond fund, even taking into account that commissions and income taxes will be deducted.

For those who want to try to make money on currency appreciation, you can enter funds denominated in currencies (America, Emerging Markets, etc.). At the end of 2015, due to the dollar surge, I earned about 40% per annum on these funds. But, alas, such currency fluctuations do not happen often.

Have a cash reserve and systematically buy shares

Naturally, only when their price falls. A real investor is not depressed by a drop in the value of an asset, but rather annoyed: after all, he can buy more for less money