Nowadays, more and more attention is being paid to the financial literacy of the population.

And this is not without reason. A huge number of people cannot achieve material well-being simply due to the lack of sufficient knowledge in this area. Even seemingly simple concepts such as “asset” or “liability” cause difficulties in interpretation, and some even consider them simply terms from accounting. In reality, everything is not so complicated.

And our financial stability and material well-being directly depend on understanding their essence and practical application. Let's figure it out.

Key Concepts

First of all, we will determine what is considered to be the assets of the enterprise.

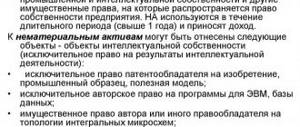

Enterprise assets (EA) are the total combination of property and finances of an economic entity, formed and controlled by its owners (founders). That is, AP can include cash (in cash and on current accounts), inventories, fixed assets, patents, and other property.

All APs can be divided into three key groups:

- material or they are also called real AP;

- financial or monetary;

- intangible.

Real assets are objects of property of an organization that have specifically expressed physical properties (weight, shape, volume). For example, buildings, machines, goods, raw materials.

Intangible (IMA), in turn, do not have physical properties. For example, a patent or exclusive rights to an invention, a trademark.

Financial assets include all funds at the disposal of an economic entity (cash, currency, non-cash and electronic money).

However, all types of assets have one key point - these objects are capable of generating profit for the enterprise to which they belong.

Parsing scheme

Example

To better understand what a passive is, let’s look at a specific example.

Let's assume that you become the owner of 5 million rubles (let it be an inheritance). And you decide to invest this money in the purchase of real estate, but at the same time you have your own home. You are buying a good apartment in a good area, already finished. You have the opportunity to rent it out and make a profit. Alternatively, the apartment can always be sold.

Let's move on to the numbers. Let's say you decide on the option of renting out an apartment. You manage to do this for 20 thousand rubles monthly. In total, over the year, you will receive 240 thousand in profit. We subtract utility bills from here and get about 180 thousand in hand. Thus, the purchased property will be an asset; it brings you income.

In addition, as a result of inflation, the cost of your apartment will increase annually. Let's take an average figure of 10%. After, for example, 2 years, your apartment will no longer cost five million, but six.

In other words, such a purchase, in a couple of years, will make you richer by an average of a million (even taking into account taxes, possible repairs and utility bills). The cost of rent will also only increase every year.

But you can do things differently with money. Alternatively, buy a new luxury car. It may seem like an asset because the acquisition is valuable. As soon as a car crosses the threshold of a car dealership, it immediately loses 15-20 percent of its price. Add to this the cost of gasoline, insurance and maintenance. Unfortunately, the purchase will not bring you any income, but will only require additional costs. Let the maintenance of this car cost you 400 thousand rubles annually.

If, after a couple of years, you decide to sell it, then you will be able to get a little more than half of its value for the car. And annual maintenance is minus 1.2 million rubles.

Thus, after 2 years, the funds invested in the purchase of real estate will make us richer by an average of 1 million rubles (this is an asset). A purchased car, on the contrary, will deprive you of approximately 1.2 million rubles (this is a liability).

How to understand the difference

Of course these are all extremes. But it is thanks to this contrast that you can more easily understand the difference between these two concepts.

In everyday life, an asset is something that brings you income. This includes both the main salary and part-time work; funds received through investment or rental; goods that we produce ourselves and deposit accounts.

Liabilities will be everything that deprives you of income received:

- • These are the funds that you spend on life processes, buying food, personal hygiene products, clothing, medicines, medical care.

- • Utility fees.

- • Taxes and fees.

- • Financial obligations: mortgage, credits, loans.

- • Maintenance and maintenance of transport.

- • Payment for entertainment (cafes and restaurants, cinemas, museums and exhibitions).

Important! An asset can become a liability and vice versa.

Let's look at an example.

You rent out an apartment (this is an asset). Suddenly, the tenants move out. And now the costs of payments, taxes and repairs fall on you. This is how an asset becomes a liability for you. It does not bring you any income, only expenses. But as soon as you find new tenants and rent out the apartment again, this is again an asset, now there is income.

How to deal with assets and liabilities?

Of course, it is almost impossible to remove liabilities from our lives. Every day we need food and clothing, use technology, and depend on medical care. The main thing is to be able to find a balance, and, ideally, to ensure that the profit received from assets exceeds the expenses spent on liabilities.

Asset classification

Fixed assets have their own classification. For convenience, let’s group the data in the form of a table:

| No. | Classification feature | Name | Essence | Example |

| 1 | By AP turnover rate | Non-negotiable | The total value of an organization's property resources that repeatedly participate in the stages of the company's economic life. The period of use is more than one year. | Fixed assets (buildings, transport, machines, leasing objects). |

| Negotiable | Property assets of an enterprise that support the economic and production processes of the enterprise. The period of use is up to one year. | Inventories and raw materials, fuel and fuels and lubricants, goods, accounts receivable and money. | ||

| 2 | By degree of liquidity | Absolutely liquid | The property of an organization, which is a ready-made means for making payments and settlements. Does not require implementation. | Money cash, in foreign currency, electronic. |

| Highly liquid | Objects that can be implemented in the shortest possible time (up to one calendar month), and without significant financial losses. | Accounts receivable, short-term financial investments. | ||

| Medium liquid | Property resources of the company intended for sale within a period of one to six months without financial costs and losses. | Accounts receivable, stocks of finished goods (manufactured products) intended for sale. | ||

| Low liquidity | The assets and property of an enterprise that can be sold at a market price without significant costs (losses). The implementation period for such objects is long (from six months to 12 months). | Fixed assets, stocks of raw materials and materials, intangible assets, long-term financial investments. | ||

| Illiquid | A type of AP that cannot be implemented as independent objects, but only in a group or aggregate with other AP. | Uncollectible accounts receivable, deferred expenses. | ||

| 3 | By right of ownership | Own | Objects of property and financial resources and values that belong exclusively to an economic entity. | AP purchased using own funds. |

| Rented | Property and funds received under rental, leasing or loan agreements. | Leased or borrowed properties. | ||

| Received free of charge | Resources transferred to the ownership of an enterprise free of charge. | Deposits, donations, targeted funding free of charge. | ||

| 4 | To attract funds from borrowers | Investment | An investment asset is property assets acquired using funds received under credit, loan and loan agreements. | For example, equipment purchased on credit. |

| 5 | On the use of financial instruments | Basic | The underlying asset is the entity on which the derivative is based. The price of such an agreement is the basis for calculations for the execution of a fixed-term contract. | Securities, goods, currency. |

| By importance | Basic | Objects without which the company’s business activities are difficult or impossible. | Buildings, transport, equipment, raw materials. | |

| Others | Other assets are property resources that do not play a key role in the activities of the enterprise. | Future expenses, mothballed equipment, machines ready for installation, etc. |

General information

Terminology

In the modern information environment, there are two fundamental interpretations of the concept of these terms.

Firstly, this is traditional accounting, characterized from the position of balance sheets. And the second is investment. This interpretation came into use thanks to the famous business consultant and author of the world bestseller “Rich Dad, Poor Dad.” In his book, Robert Kiyosaki talks about how gaining financial independence is directly related to increasing the number of assets and reducing liabilities.

Let's figure it out. In order not to delve into financial definitions and scientific terminology, we will write simply and clearly.

Assets bring you money. Liabilities - this money is taken from you.

For any successful enterprise or financial entity, it is very important to maintain a balance: assets must either exceed liabilities or be equal to them. Otherwise, losses may occur or bankruptcy may occur.

Types of assets and liabilities

Assets include those of your monetary investments that: bring stable financial (passive) income, and (or) will increase in value after a certain period.

Assets

There are a huge number of assets. As practice shows, for most citizens, the most preferable investments are:

- Bank deposits. Money deposited at interest in reliable banks and on favorable terms that bring profit to the investor.

(We are now making deposits at 7.5% per annum in Tinkoff, if using my link you get 0.5% of your deposit directly to your account, you can open a deposit here) Open a deposit in Tinkoff Investments - Stock. They enable their holder to make a profit in two ways.

When you buy shares as a piece of a business, expecting that its value will increase in the future. And this will entail an increase in the price of the shares themselves. Or buying dividend stocks. For the purposes of their proportionate participation in the annual distribution of campaign profits. (I use Tinkoff Investments, if you are investing for the long term and not speculating, I recommend using my link - you will receive a 500 ruble bonus to your account) Register and articles as an investor - Bonds. This security can bring its owner several options for profit: • coupon income.

This is when the company that issued these securities undertakes to make payments to you at an annual interest rate predetermined in the contract. This usually happens once a year, maximum twice. • discount income. This is the difference in the purchase price and the redemption price of a security (its par value). Bonds can be called a financial instrument that allows you not only to save funds, but also to receive moderate income from them, with relatively low risks. You can also buy bonds at Tinkoff Investments and you will receive a bonus of +500 rubles using my link =>> Open an account and invest in bonds - Real estate. This type of investment is one of the most reliable options for making a profit in the long term. By purchasing real estate, you not only guarantee yourself a stable flow of finance from rent, but also the value of the property itself, as a rule, grows annually.

I'm going to buy a large apartment with a mortgage and divide it into small studios, then the apartment can yield 30% per annum, but remember that you need to choose a good location.

It is profitable to take out an Apartment with a Mortgage from Tinkoff Bank

*Following my link, if you get a mortgage, 5% cashback in the Repair category at Tinkoff Bank for six months!

Note! The car you buy is a liability. But, if you decide to use it not for personal purposes, but for work, for example, as a taxi driver, it will already become an asset, now the car is a source of profit.

- Mutual Funds. Mutual investment funds are perfect for beginners, or for those who are simply too lazy to decide how and where to invest their money. You simply transfer your assets to professionals for management. And they, for their part, charge you a certain percentage for these services.

- Borrowed money . And this is also an asset. But provided that you get some benefit from this (not necessarily related to finances). Otherwise, we get - passive.

- Income from the results of your own business.

- Assets that increase in value annually. Precious metals, antiques, art and collectibles.

Liabilities

Liabilities are considered:

- • loans;

- • credit cards;

- • loans taken from the bank (for example, for the purchase of vouchers, equipment, electronics);

- • houses or apartments pledged to the bank;

- • business that brings you losses;

- • car (because it needs maintenance);

- • apartment or house in which you live. They require funds to pay utility bills and repairs. And even more so if the property was purchased with a mortgage;

- • borrowed money. Even an interest-free loan, in any case, will have to be repaid.

Classification of rare species

In addition to the generally accepted classification of AP, there are rare types that are quite rare in the economic activities of companies. These include:

- An information asset is an object that does not have physical properties and characteristics, however, it has high significance (value) for the company. For example, databases, information portals, etc.

- Problem assets are company property that is burdened with special conditions that prevent standard sale. For example, seizure of a company's building and car.

- Reserve assets are property and financial resources controlled by the state, that is, the sale of these reserve assets can only be carried out with the permission of government agencies. For example, shares of large companies (Sberbank, Rosselkhozbank), reserve funds.

Risk

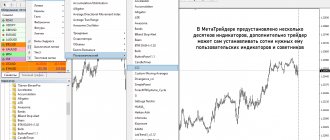

Profitability is only one side of the coin. The second side is risk. Next, we will talk about the market risk of assets - in other words, this is the degree of fluctuation in the profitability of an asset. The greater the annual fluctuations in an asset's return, the greater its market risk. Risk is measured by standard deviation, which is a number that shows how much returns typically differ from the average.

For example, the standard deviation of asset A with a return of 5%, 8%, 4% will be 2. And for asset B with a return of 15%, -5%, 25% will be 15. The standard deviation means that in 68% of cases the return on the asset will be within the range of one standard deviation. In other words, if the return is 8% and the standard deviation is 15, then in 68% of cases the return was in the range from -7% to +23%.

Assets with a high standard deviation are considered riskier because their future returns are less predictable than assets with a low standard deviation.

The chart below shows the risk and return of major asset classes. The vertical axis displays the arithmetic mean return, and the horizontal axis shows the standard deviation.

A bank deposit in rubles is located in the lower left corner - this is the least profitable and least risky asset.

Government and corporate bonds are located above and to the right in the diagram - their yield is slightly higher than that of deposits, but their standard deviation is also larger.

The dollar and euro are located lower and to the right - they bring less profitability than deposits and bonds, but at the same time their risk is greater. Therefore, from a risk/return point of view, this looks worse than ruble deposits and bonds.

Real estate, precious metals and American stocks are roughly next to each other - their returns are higher than those of deposits and bonds, but the risk is also greater.

The Moscow Exchange index is located in the upper right corner - that is, it is the most profitable, but also the riskiest.

Looking at this diagram, you can easily notice a pattern - the higher the profitability of an asset, the greater its risk - this is one of the most important rules in investing. In other words, if you want to receive high returns, be prepared for high market risks. If you are not ready to take risks, then you should not count on high returns. If somewhere you are offered high returns without risk, then most likely you are being deceived.

Is it difficult to invest abroad?

In our country, investment opportunities are still limited to the purchase of Russian securities and participation in domestic mutual funds, while after opening an account abroad you get access to thousands of different investment instruments. However, many people still have not thought seriously about investing abroad. At one time, I was amazed by one person’s explanation of why he does not invest money abroad. My interlocutor referred to the complexity of this process. From further conversation, however, it turned out that he did not even try to find out how difficult or simple it really was.

In fact, there is nothing complicated here. Any investment is carried out through a foreign intermediary, which can be:

- bank;

- Insurance Company;

- brokerage firm.

First you need to open an account with one of these organizations. Documents can be prepared in Russia and then sent to the addressee by mail. After this, you need to transfer money abroad from your Russian bank account. Finally, an order must be given to invest (for example, to purchase bonds from the European Investment Bank). For help in preparing documents and choosing a broker abroad, you can contact Russian consultants. Another option is to independently study the offers of foreign intermediaries on the Internet and contact the broker directly.

© Vladimir Savenok, General Director

Formulate goals

The second stage is goal setting. To do this, you need to write down all your goals, ideally for the rest of your life. These may include the purchase of a new phone, household appliances, repairs, purchase of a car and/or real estate, formation of capital for passive income in retirement, payment for higher education for a child, etc. For each goal you need to specify the amount, deadline and currency.

To achieve short-term goals (up to a year), regardless of the amount, savings accounts or a deposit are best suited. To achieve more global goals, it is wiser to use more complex financial instruments: bonds, shares, ETFs, etc. - depending on the parameters of the goal and your risk appetite.

Selection of financial instruments

By determining risk appetite and the parameters of each goal, you can effectively select suitable financial instruments. If an investor has a low risk appetite and/or short-term goals (up to three years), then conservative financial instruments with fixed income are suitable for him: bonds, bond funds, real estate investment trusts, deposits, structured products with full capital protection. These tools are easily accessible and profitable at the same time.

With a moderate risk appetite, an investor can combine fixed income instruments with riskier instruments: stocks, equity ETFs, structured products with partial capital protection and precious metals. The proportion depends on the duration of the goal: the higher it is, the more risky instruments can be used.

Investors with a high risk appetite may prefer risky instruments without capital protection. However, even in this case, for medium-term goals, it is better to have part of the portfolio in fixed income instruments.

Trying to guess the market is useless

Many people think they can guess where the market will go and try to make money from it. Thousands of analysts and experts make predictions every day about what will happen to the market, or where it is better to invest money next year. In reality, these forecasts are useless in most cases.

The table below shows the ranking of asset returns for each year. The table is constructed as follows: at the very top of the column is the most profitable asset, at the very bottom is the most unprofitable.

As you can see, the assets in the table are arranged chaotically. The asset that was in first place last year may be in any other place next year. Return on assets can vary greatly from year to year.

Looking at this table, try to honestly answer the question - is it possible to guess the most profitable asset every year? Obviously not. Therefore, trying to guess what will happen to the market, or where it is better to invest money next year, is practically useless.

What your asset list should look like

In my books, I have repeatedly cited as an example the investment portfolio of the average American millionaire (I consider this distribution of personal funds exemplary):

- 20% – securities, shares of investment funds;

- 30% – pension programs (insurance companies, pension funds);

- 20% – real estate;

- 20% – business;

- 10% – other assets.

I also note that millionaires are constantly expanding their investment portfolios. At least 20% of income is allocated to investments. If you don’t have many real assets, I advise you to create new ones by regularly investing part of your income. To get started, you can open a regular bank deposit. The main thing is to hide from yourself the money that you decide to invest.

Make a plan and stick to it

Using this information, you can create a roadmap that will help you stick to your goals in the future. This will give you an understanding at each moment of time about what part of your income to save and with what frequency, how often to replenish your brokerage account, as well as what instruments to buy and in what proportion.

Once every six months, it is better to review your goals, evaluate whether you are able to stick to the plan and, if necessary, adjust it, because life circumstances change, and, probably, in a year you will be more able to save.

Personal financial planning is the key to your peace of mind and well-being. By sticking to the plan, you will have confidence in the future and can significantly improve your quality of life. You just need to be disciplined, keep a budget, save systematically, and very soon you will begin to achieve your goals.

Cover photo: StockStyle/shutterstock.com