Book-entry securities are one of the ways to fix and secure rights to securities using the capabilities of modern electronic devices.

Securities are a document confirming property rights that exist as a physical object.

Documentary form is the existence of rights in paper form. But uncertificated securities simply imply the presence of information about ownership with recording in the register (special purpose “depot” account, personal account) of all significant data.

Both options for the existence of securities have the right to life, in accordance with the norms of current legislation.

Main types of securities

Shares are perhaps the most famous and popular type of securities. They represent a form of equity participation in the business of the company that issued them. This equity participation involves both the opportunity to influence the fate of the company through voting at general meetings of shareholders (the larger the share of shares owned, the greater this opportunity), and receiving your share of profits in the form of dividends.

There are different types of shares, some of them guarantee the payment of dividends at the expense of the ability to vote, others, on the contrary, provide voting rights, but do not promise a stable payment of dividends. You can find out more about this here: Different types of shares.

Bonds are also a fairly well-known financial instrument in wide circles. Unlike shares, bonds do not imply equity participation in the affairs of the company that issued them. They are an analogue of a simple promissory note and are intended so that the issuing company can borrow money. By buying bonds, investors thus borrow money for the needs of the company, and the company, in turn, undertakes to pay them an agreed interest (coupon income) for this.

Certificates of deposit and savings are documents confirming the rights of their owners to a bank deposit. As a rule, they accrue a slightly higher interest rate than simple deposits. Certificates of deposit are issued to legal entities, and savings certificates are issued to individuals.

Promissory notes are non-equity debt securities. This means that they are a document confirming the existence of a debt of one person in relation to another, but they are not issued en masse (in series, such as shares or bonds), but in single copies. Bills of exchange can be simple and transferable, registered and payable to bearer. They can be transferred to another person by applying a special endorsement - an endorsement.

A check is nothing more than a simple order from the owner of the bank account to issue, upon presentation, the amount of money specified in it. The one who writes the check is usually called the drawer, and the one to whom the check is written is called the check holder. The check holder can cash the check issued to him at any branch of the bank indicated on it, but no later than a certain period (6 months in the USA, 15 months in Australia, etc.).

A bill of lading is a document issued to the owner of the cargo during its transportation. This document is written out and given to him by the cargo carrier. In this case, the bill of lading performs the functions of several documents at once. It simultaneously represents an act of acceptance of the transfer, a document of title, a waybill, and actual confirmation of the agreement concluded with the owner of the transported cargo.

Warrants are securities certifying the right of their owner to purchase a specified number of shares at a specified price. Usually this price is slightly lower than the market price. Warrants usually have a limited duration, but they can also be indefinite.

In addition, a warrant is a document of title - a certificate issued by a warehouse stating that the goods specified in it have been accepted for storage.

Futures are a derivative financial instrument, that is, they are based on some underlying asset (for example, the same shares, bonds or commodities) in relation to which a specific contract is concluded. For example, purchasing a six-month futures contract for 100 barrels of BRENT oil means an obligation to buy back this product in six months at a price pre-agreed in the contract. But, as a rule, the matter does not reach the point of actual repurchase of the goods, and at present, most futures contracts end in simple mutual settlements between their parties.

Brent crude futures chart

Options are also derivative financial instruments and are similar in many ways to futures.

However, unlike them, they do not imply an obligation, but only the right to conclude the transaction specified in them. That is, in other words, the option contract to buy the same BRENT oil from the previous example is not binding. It can be executed in the event that the price indicated in it turns out to be more profitable than the market price. And if the price of oil specified in the option contract is higher than the market price by the time it expires, then it will not be necessary to execute this contract (in this case, buy oil).

How are all these types different?

The differences are presented in the table.

| Characteristic | Bond | Bill of exchange | Treasury bond | Savings certificate |

| Release form | Electronic or paper | Paper | Electronic form | Paper |

| Payment form | Money or property | Money | Money | Money |

| Circulation | Big | Single copies | Big | Big |

| Nature and time of interest payment | Interest is paid at different frequencies and at different rates | The interest is fixed, paid at the time of return of capital | At the time of return of capital | At the time of return of capital, a fixed percentage is paid |

| Validity | For 3–5 years | Up to 1 year | Up to 3 years, usually up to 6 months | Up to 3 years |

| Remuneration for the use of capital | + | Maybe | + | + |

| Can it serve as a means of payment? | — | + | + | — |

| The need for state registration | + | — | + | + |

Not only interest rates and frequency of payments differ, but also the very economic essence of each type.

Classification of securities

All currently existing securities can be classified according to the following main characteristics.

For financial relations:

Debt . By purchasing this type of security, you become a lender. That is, in other words, you lend your money at a pre-agreed interest rate (or at a discount). Debt securities include such securities as: bonds, savings certificates, bills, etc.

Equity . Owners of securities of this type no longer act so much as creditors (although the money they paid for the possession of these securities also ultimately goes to the development of the issuer), but rather as partners or shareholders. A striking example of this type of security is shares. An equity security gives its owner the right to a share in the business conducted by the company that issued it (the issuing company). This share in the business is commensurate with the share of securities that you own. For example, owning a 50% stake in a company gives its owner the right to a decisive vote, and one or two shares are just a drop in the ocean of votes at the general meeting of shareholders.

By method of transfer of rights:

Registered papers imply that all rights granted by them go directly to the person whose name is indicated on them.

Bearer papers allow the right granted by them to be exercised by any person who presents them for execution.

An order security can be transferred to any other person through a simple endorsement (endorsement). Accordingly, along with this, all rights granted to it will be transferred.

By degree of primacy:

Basic securities . This type of paper involves transferring to its owner the rights to a part (or share) of certain property assets. These include: stocks, bonds, checks, certificates of deposit, bills, etc.

In turn, basic securities can be divided into two more types:

- Primary . Based directly on assets. These include: shares, bills, bonds, etc.;

- Secondary . They are based on primary securities, that is, they give their owner the right not to the asset itself, but to those securities for which the asset in question is the underlying. These are, for example, depositary receipts (for shares) or warrants.

Derivative securities (derivatives) . They differ from the main ones in that they express not so much the right to own a certain exchange asset, but rather the right or obligation arising as a result of changes in the price of this asset. The most striking representative of this type of securities can be called a futures contract.

According to the period of their existence, all securities can be divided into two main types:

Urgent . They have a limited circulation period and, in turn, are divided into:

- Short-term securities (circulation period less than one year);

- Medium-term securities (circulation period from one year to five years);

- Long-term securities (circulation period over five years).

A typical example of fixed-term securities are bonds, which, a priori, involve borrowing your money for a certain period of time, at a certain interest rate.

Indefinite . As is already clear from the name, such securities do not have an expiration date and the time of their validity and (or) redemption is in no way limited. Securities of this type include, for example, shares.

By form of existence:

Documentary securities presuppose the presence of a certain material form. This form, as a rule, includes the name of the issuer, par value, details, etc.;

Book-entry securities do not have any material form, but are recorded, for example, in electronic form. These include, for example, derivatives.

By release form:

Emission . These types of papers are issued through pre-arranged and planned events. The process of their release itself is called emission, and their number has a strictly defined value. As a rule, the main purpose of the issue is to raise funds for the further development of the issuing company. These types of securities include stocks and bonds.

Non-emission . These papers are not issued in predetermined editions. They may not have any specific issuer behind them. These are, for example, futures, checks, bills of lading, bills, etc.

By type of appeal:

Marketable securities are usually called those that are circulated (traded) on official exchange platforms. These types of papers can be bought and sold on the secondary market;

Non-marketable securities cannot be sold or purchased in the secondary market. These papers can only belong to the person to whom they were originally given.

By purpose of use or from the point of view of its investment attractiveness:

Investment securities are intended to be acquired for the purpose of obtaining some investment income. This income can be calculated as interest (on bonds), dividends (on shares) or as a discount (on discount bonds).

Non-investment . These securities do not serve their owners as a tool for obtaining investment profits. That is, they are not purchased in order to receive a certain income from them over time. For example, such paper as a bill of lading is simply confirmation of the cargo owner's ownership of the goods being shipped.

Well, in conclusion, we can divide all securities according to their degree of risk:

Risk-free securities involve virtually no chance that holding them will result in a loss. That is, in this case, the situation is almost completely excluded when their value will decrease over time relative to the price at which they were originally purchased. In general, securities of this type can be understood as all those for which you can at any time receive at least the amount of money for which they were purchased. These are, for example, bank deposits or government bonds of developed countries (US treasury bills, UK government bonds, etc.).

Low risk . Securities of this type traditionally include bonds and shares of the largest blue chip companies.

Medium-risk securities include first- and second-tier shares.

High risk . These are, as a rule, all derivatives and shares of companies belonging to the third echelon and below (not quoted on official stock exchanges).

For greater clarity and ease of understanding the material, the entire above classification is presented in the form of one figure:

Resulting consequences

Documentary securities physically confirm the right to own them, which is stated in the register. The shareholder may request the issuance of an official document indicating the basic details.

Russian joint stock companies practice issuing free securities due to the speed and low cost of the process. The issue takes place without delays, which has a positive effect on the price of shares and the overall profit of the joint-stock company.

When purchasing such securities, you need to take into account that they can only be registered, because the owner’s details are indicated in the register when issued. Therefore, this issuance format is a priority for shares, while bills must have a form.

Book-entry securities are so-called paperless shares, which, nevertheless, give all rights and are recognized by law.

Issue of securities

It is with the issue that the life path of securities begins, so to speak. An issue is nothing more than the release of securities into circulation, or their transfer into the hands of their first owners (in exchange for remuneration in the amount of the nominal value of the issued securities).

Objectives of the issue

The purpose of the issue is to attract investments (in the case of issuing equity securities), or borrowing funds (in the case of issuing debt securities). The funds raised through the issue of equity securities are used to form or increase the authorized capital of the company. And the funds received through the issue of debt securities replenish the company's borrowed capital. This money, unlike that received as a result of the issue of equity securities, will eventually have to be returned to investors (acting, in this case, as creditors).

The issuance involves the sequential passage of the following main stages:

- First, the decision to issue securities is made and approved;

- The following is the procedure for state registration of a new issue of securities;

- After this, securities are placed (for example, through an IPO or SPO);

- Finally, a placement report is made, which is also subject to mandatory state registration.

Prospectus

The issue of securities is usually always accompanied by the creation and publication of a document such as a “Prospectus”. This document contains basic information about the upcoming issue of securities. It must perform a dual function: on the one hand, its task is to attract as many potential investors as possible, and on the other, it must necessarily reflect all the risk factors inherent in newly issued securities (this is a requirement of state regulatory authorities).

In Russia, the requirements for the content of the prospectus are reflected in Article 22 of Federal Law No. 39-FZ “On the Securities Market” dated April 22, 1996 (last amended on December 27, 2018). According to the letter of the law, the prospectus must contain the following basic information:

Excerpt from Federal Law No. 39-FZ “On the Securities Market”

Bill of exchange - brief description

As mentioned, this is one of the most common debt securities. This is a rather specific document with clear characteristics:

- Approved form - it must contain strictly defined points and details. The slightest deviations from the rules may become grounds for declaring the bill void.

- Negotiability - a bill of exchange can be transferred from hand to hand an unlimited number of times, this makes it an independent instrument for settlements. Compensation for the bill will be received by the person who turns out to be its last legal owner.

- Strictness - debts on this type of securities are collected much faster.

- Unconditionality means that by the end of the term the money must be returned to the holder without any additional conditions.

- Abstractness - such a security is issued without reference to the event (operation) that served as the basis for its provision.

Properties of securities and rights secured by them

According to its classic definition, given in most economic dictionaries, a security must satisfy the following basic requirements:

- The security must be freely traded on the market, that is, bought and sold;

- It must meet certain standards that make it a liquid (tradable) commodity;

- It must be available for civil circulation;

- Its circulation must be regulated, and it itself must be recognized by the state;

- As part of a certain market segment, a security must, to a certain extent, be a reflection of it, be marketable;

- It must be in documentary form (it does not matter whether it is issued on paper or in electronic form);

- Information openness for potential investors is another important feature;

- Risk is another property inextricably linked with securities. It reflects the degree of probability that the costs associated with the acquisition and ownership of a security will ultimately exceed the income received from it;

- Profitability is what, to a greater extent, an investor purchases this or that security for. It is directly related to risk. The greater the risk, the higher the potential return.

Depending on the type of security, it may give its owner the following rights:

- The right to claim a certain amount of money and interest on it (debt securities, shares of investment funds);

- The right to a share in the business (including part of the profit from it in the form of dividends) and to participate in its management (equity securities - shares);

- The so-called property right. That is, the right to certain goods that are in the temporary possession of another person, for example, a carrier (various kinds of documents of title, for example, bills of lading).

Differences in the legal regime

The legal regime of undocumented papers differs from the documentary form, although in many respects they are similar.

Key points of legal relations:

- The right of ownership is secured in an electronic document by the person who is given the right to make changes to the registers of shareholders.

- This type of security represents an absolute right.

- In the management of securities, regulation of the proprietary type prevails in any case - the right to own an asset is absolute, formed on the model of property rights, but has certain differences.

Civil law explains the absolute ownership of uncertificated securities as the legally established possibility of a shareholder to be recorded as authorized on paper. He has the opportunity to dispose of the asset according to his interests and desires.

Securities as a source of income

We have already said above that, from the point of view of the possibility of using securities as financial instruments for making a profit through trading operations on the exchange or over-the-counter markets, they can be divided into two categories:

- Investment;

- Non-investment.

For earnings purposes, as you already know, the first of these two categories is used - investment securities. Or in other words, those of them, investing money in which can bring a certain income over time. The most popular investment securities are:

- Stock;

- Bonds;

- Investment shares;

- Savings and certificates of deposit;

As well as derivative financial instruments, such as:

- Futures;

- Forwards;

- Options.

Profits from investment securities can be made in two main ways:

- Due to changes in their market value;

- By generating income from owning them.

And, of course, no one forbids combining these two methods, making a profit from owning a security, and after some time, selling it at a higher rate, also making a profit from changes in market value.

Generating income through changes in market value

Any security that has some degree of liquidity has its value set by the market at each current moment in time. This cost depends on many fundamental factors (economic, political, etc.). Traders try to predict in which direction the price will move in a certain time frame and, based on their forecasts, buy or sell the analyzed financial instrument.

In the future, if the forecasts come true, the position is closed with a profit (for example, the purchased security is sold at an increased price). Well, if the forecast does not come true, then the trader suffers a loss.

Forecasting methods

To predict future price changes, two main types of market analysis are used:

- Fundamental Analysis;

- Technical analysis.

Fundamental analysis tries to take into account all possible factors (economic, political, social) in order to determine the influence of each of them separately and all of them in combination on how the market will evaluate the analyzed financial instrument (security). Read more about this in the material: “Fundamental market analysis and methods for conducting it.”

In this type of analysis, not the last place is occupied by the assessment of current news. There are both planned and spontaneous news. Scheduled news includes those that are published as scheduled. For example, quarterly published data on the unemployment rate, the consumer price index or the trade balance of countries.

For each planned news, there is a certain expectation on the part of market participants. And depending on how well the actual published data corresponds to expectations, appropriate conclusions can be drawn about the impact of the news on the price.

The situation is much more complicated with news that is spontaneous in nature. Such news is difficult to predict because it appears unexpectedly. These include information about natural disasters that have occurred or major man-made disasters. Or, from the realm of science fiction, the news that aliens have given us a source of free, inexhaustible energy. It’s a joke, of course, but imagine with what a roar the prices of oil and other energy resources would collapse.

As for technical analysis, it is entirely based on the information that is presented on the price chart of the financial instrument in question. These charts are examined in different time perspectives (timeframes) in order to search for characteristic models of price behavior (patterns), as well as to determine current trends and levels of support and resistance.

Price takes everything into account - this is the main postulate of technical analysis. This means that all the variety of events and factors that fundamental analysis tries to cover is, in this case, already taken into account by the price chart. And in order to predict further price movement, you just need to correctly analyze this same price chart.

You can get more detailed information about technical analysis and the methods used in it in the article “What is technical analysis”.

Earning income from ownership

By owning securities, you can also receive income that does not depend on changes in their market value. This is interest income paid on debt financial instruments (bonds, certificates of deposit, etc.) and dividend income paid on shares.

Interest income

By investing in debt securities, you are lending your money to their issuers. By purchasing corporate bonds, you act as a creditor to the company that issued them, and by purchasing government bonds, you are lending money to the state. Well, as compensation for the loan provided, the issuer of the bond (whether it is a commercial company or the state) pays you a pre-agreed interest.

A similar situation arises when purchasing a savings certificate (or, for legal entities, a certificate of deposit), in this case the issuer is the bank, for the deposit in which the corresponding certificate is issued. The bank uses your money in its operations (including for issuing loans), and pays you a set percentage per annum.

The essence of hedging

The emergence and popularization of derivatives or secondary securities was associated with the need for maximum protection of transaction participants from financial risks and losses. One of the classic schemes for trading in major securities is hedging. Translated from English, the term means “to protect, prevent damage.”

Derivative hedging is a financial transaction carried out with an expectation of a future outcome. This is a transaction that is concluded between the two parties to the contract in order to maximize the protection of the funds invested in the business. Market factors typically include:

- adverse effects of inflation or deflation;

- fluctuations in securities prices;

- other force majeure circumstances.

A hedger (the so-called business entity) has the opportunity to act in any direction: to lower or increase derivatives as opposed to the direction of primary securities. In the case of upward hedging, funds are insured against a possible jump in the exchange rate or an increase in the cost of the goods specified in the contract. Future purchases are made strictly at the price established and agreed upon between the parties at the time of signing the contract.

Hedging downward derivatives provides protection against price declines. If an investor is sure that in the future the value of a product will certainly decrease, then he sells an option on the stock market at a high price today, and after selling his product some time later, he buys an option at a price that has decreased proportionally with the cost of the product.

Thus, hedging with derivatives makes the profits and associated costs of participating in the stock market more predictable. Speculators who trade derivatives assume maximum risk. By effectively using price instability for their own purposes, they are able to make a profit by properly insuring their risks.

The most popular scheme for hedging primary securities is with futures contracts. The first such transactions with valuable derivatives were carried out in Chicago, which made it possible to protect participants of commodity exchanges from difficult to predict fluctuations in market conditions. It is considered incorrect to say that hedging means removing and completely removing risks. In fact, the procedure only helps to optimize the ratio of costs, losses and profits based on a competent assessment of derivative securities and market analysis.

Debt Central Bank is a type of loan agreement

Everything that applies to a loan agreement applies to a debt security, just the terms may be slightly different. After all, we are talking about the monetary relationship between the borrower and the issuer. The paper is a written certificate issued by a bank or other lending institution to confirm the deposit of money.

The interest income is usually known in advance and does not change during its life. The issuance of bonds and other securities of this type is similar to lending, the only difference being that there is no collateral and the procedure for transferring claims is significantly simplified.

The similarity of debt securities with a loan and confirmation that this is really a type of loan determines the very purpose of issuing bonds - for the issuer it is a way to attract additional funds (issue a loan, in fact) for a long period on favorable terms. It’s just that here the creditor is not the bank, but the investors who bought the debt securities.

Otherwise, the principle is the same: the investor undertakes not to demand the invested funds before the maturity date of the paper, the issuer guarantees the return of the money with interest on the specified date. The security of such an investment is, as a rule, high, because the opportunity to issue securities is provided after a mass of checks of the issuer for compliance with the necessary requirements; the procedure is carried out with the involvement of certain structures and regulators.

Market

The concept of “securities market ” describes a system of microeconomic relations between participants involved in the purchase and sale of documents. The market participant is the issuer, investor or investment vector institution. For those who do not know, issuers are enterprises whose activities are aimed at the issue (issue) and sale of securities.

Latest changes in the Civil Code of the Russian Federation in relation to the Central Bank

Amendments to the Civil Code of the Russian Federation, which fundamentally affected work with the Central Bank, came into force on June 1, 2018. Clarifications were made to financial transactions (factoring, loans, loans), and bearer savings certificates were abolished.

On June 1, 2021, amendments to the joint will and inheritance agreement came into force. From October 1, 2019, the concept of “digital law” will come into effect.

The Bank of Russia has developed new requirements for maintaining the Central Bank register, the draft is still at the approval stage (the estimated effective date is January 1, 2020)

Brief overview of the main changes

Securities as joint property can be bequeathed in a joint will.

Remote transactions concluded online (using form filling, SMS sending, or the “OK” button) are considered valid.

Commodity derivatives

This type of derivatives includes warehouse receipts and bills of lading.

The bill of lading certifies the owner's right to dispose of the cargo, information about which is included in the document. If there are several copies of paper, they cease to be valid after the cargo is released under the first presented bill of lading. A simple warehouse receipt confirms the fact of delivery of goods for storage. Acts as collateral and gives the right to receive property from the warehouse.

A double warehouse receipt consists of 2 parts, each of which is an independent derivative. The second document, a warrant, provides the opportunity to sell or pledge the goods specified in it.

Both components must be identically designed. The authorized person puts his signature and seal of the organization that accepted the property for storage.

The following details must also be indicated:

- name and address of the warehouse;

- registration number of the certificate;

- information about the legal entity: name/F. I. O., location/residence;

- information about the product: name, quantity, shelf life;

- remuneration amount or storage tariffs.

State securities banks

This type of debt securities represents a form of existence of the country's internal debt. Here the state itself acts as the issuer. The main advantages of state securities are the maximum level of reliability and security of the deposit, preferential taxation (in comparison with other types of securities and areas of investment).

Government securities are usually issued through ministries of finance or central banks. The main investors are insurance and pension funds, the population, investment funds and companies. Securities can be issued in documentary (there is a form) and non-documentary forms (there is only an entry in the account in the depository).

The distribution of government securities in paperless form can be carried out through auctions, through open sale at set prices to everyone, through closed distribution only to certain investors, etc.

In the bond market, government securities usually occupy a leading position (the share reaches 50%). In Russia, the largest share belongs to medium-term and long-term bonds.

The relevance of borrowing finances using securities securities

Many companies have already appreciated the benefits of this type of borrowing. In the modern world, this option for obtaining finance has been practiced for a long time. Securities can be equity or debt. And the main advantage of debt is that they do not give the owner any property rights or the opportunity to influence decisions on the development and operation of the company.

Debt securities involve exclusively credit relationships - the investor buys a document confirming his investment in the issuer and giving the right, after the specified period, to receive the amount and interest back.

State bodies and legal entities can issue securities. State central banks are the most popular, as they are considered more reliable.

After the payments are made, the relationship between the investor and the issuer ends: the obligations are fulfilled, the parties do not owe each other anything. The issuer used the funds for his own needs, the investor received interest, avoiding all the difficulties and risks of obtaining a loan from a bank.

Tools for raising funds

Many entrepreneurs perceive debt securities as a tool for obtaining additional funds at their disposal without the need to give someone a part of the company or the right to make decisions regarding its work. Compared to a regular bank loan, this option offers a lot of advantages: lower interest payments, reliability, no collateral, etc.

Bank certificate

Only banks that meet the established requirements have the right to issue such certificates. A bank certificate is a debt security that can be compared in principle to a bank deposit.

The certificate form assumes the presence of all degrees of protection and is produced only in specialized printing houses with licenses. If any of the details on the form are missing, it immediately loses its status as a security. Registration journals, folders with certificate stubs are stored in fireproof cabinets and cash vaults.

Unlike a check or bill of exchange, a bank certificate is not used as a means of payment/settlement. When the deadline for circulation of the paper arrives, the holder receives the deposit amount and interest.

In the process of issuing securities by a bank, the funds received are included in its borrowed capital and must be included in the capital, which is the basis for determining the calculations of all important financial standards of the bank. These are borrowed funds from the bank. To issue the paper, you just need to have your passport with you; you can pay in cash or with funds from a deposit already made in the bank.

The main disadvantage of a bank certificate is the impossibility of its participation in the insurance system for all deposits of individuals. Interest is paid when the certificate is redeemed upon presentation of the paper. The main purpose of the paper is to borrow money from the bank for the implementation of a specific project or activity.

Monetary relationship between issuer and borrower

Debt securities are a type of loan agreement. All types of securities are examples of capital investments for the purpose of investment, on the one hand, a legal means of financing investments. Organizations are able to raise additional funds without having to sell assets or shares in the company.

But for the buyer, debt securities are a means of earning money only, since they do not give the right to a part of the issuing company, its property or assets. The only purpose of purchasing securities is to receive profit in the form of interest without any personal contribution to the development of the issuer (except money), which can be considered passive income.

At the time of purchase of securities, the investor and the issuer enter into financial, economic, civil legal relations that fall under the regulations of the conditions of issue of the Central Bank.

The main value of the Central Bank is providing investors with the opportunity to participate in a variety of relationships/operations based on the conditions and content of the Central Bank.

While in the case of bank lending the subject of the relationship between the borrower and the lender is the amount of funds, the investor and the issuer work with securities backed by capital (money invested for certain purposes, participating in socially useful or entrepreneurial activities ).

At the time of sale of a security, the previous owner gives the new owner his place as an investor and the right to participate in transactions with securities. But all guarantees are already provided by the issuer - in terms of compliance with conditions, payments, treatment, etc.

Debentures

To define what debt securities are, it should be understood that they primarily represent the debt obligations of the issuing company towards the holder. It is essentially a loan in which principal and interest are paid.

Debt securities can be issued by the state, international organizations, local governments, commercial companies, and credit institutions. The securities may or may not be secured by collateral. The loan agreement may contain various conditions.

Features of debt securities:

- The face value is the basis for calculating interest and is paid on the maturity date.

- The maturity date is the date on which the issuer is obligated to pay the holder the principal amount and close the obligation. Securities can be short-term (up to a year), medium-term (1-10 years), long-term (from 10 years).

- Coupon rate - this is the name of the interest rate that the issuer pays to the owner of the securities; it can be floating or fixed. Floating depends on short-term interest rates and is fixed for a specific period. Short-term securities do not require a coupon, because they are issued at a discount (the difference between the nominal price and the cost of the security).

- The coupon payment date is the period during which the interest payment is made.

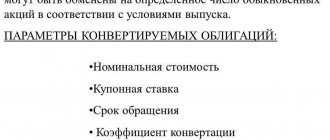

- Derivative debt securities are a loan that involves some special conditions (example: convertible bonds that can be exchanged for shares on a specified date).

When purchasing a security, the client fixes the rate of return at the time of the transaction. It depends on the purchase price, coupon rate, accumulated coupon profit, which is paid to the previous owner of the paper. The liquidity of securities depends on a lot of factors (market segment, issue volume, market situation, level of supply/demand, etc.).

The main advantages of debt securities:

- A good alternative to bank deposits - higher income.

- Opportunity to sell securities before maturity.

- Preservation of accumulated interest upon sale, no penalties.

- A large selection of combinations of conditions - currency, profitability, investment period, risks.

- The opportunity to form a good portfolio is to buy securities of enterprises from different countries and economic sectors, diversifying investments.