olegas Jun 17, 2021 / 75 Views

Despite the fact that bonds are rightfully considered one of the safest types of financial instruments, investing in them is nevertheless associated with certain risks. And if you decide to choose them as an object for your investment, you must be fully aware of all the dangers that may await you along this path.

All risks of investing in bonds can be divided into two main categories:

- Credit risks;

- Market risks.

What are bonds

The word " bond " comes to us from the Latin language. Obligatio is translated as “ obligation ”, in the financial world - an obligation to buy back this paper after a certain period. The first bonds appeared during the Great Geographical Discoveries. Adventurers were looking for investors to equip a ship and sail away in search of gold, colonization of new lands or trade. The aristocracy built palaces and sewed dresses, so only bankers, merchants and artisans had free money They rarely took the word of the sailors and demanded a special receipt - they say that in two years you will return and pay them back with interest.

During the colonization of the New World, the development of technology and scientific discoveries, many capable businessmen faced financial obstacles to the development of their business. Let's say an inventor comes up with a new engine, but there is no money for production. Bankers are not engineers; they do not believe in the commercial success of the engine. Other manufacturers want to support the inventor, but their finances are limited . The inventor issues securities ; anyone with enough money can buy them. The issuer received the money, started production and made a profit. After a set time, the holder can call for redemption , and the issuer (who issued the debt) buys back the bond and rewards the holder with interest. How do they work? Like a loan from a bank, the only lender is you .

The issuer expects to receive cash , put it to work and make a profit. Part of this profit will certainly be used to pay off bonds and other debt obligations. In this case, percentage is most often fixed - regardless of the company’s profit, the bond holder will receive only the amount indicated in the bond. Securities are often issued to finance individual projects, programs and facilities in order to establish precise levels of income and costs. At the same time, the sale of bonds does not require such paperwork as full-fledged lending from a bank or investment fund.

Additionally, you may want to know the difference between a stock and a bond.

Who are they suitable for?

OFZs are suitable for long-term investments, but a deposit is more suitable for a financial safety net, notes Veniamin Kaganov, director of the Association for the Development of Financial Literacy.

OFZs with a maturity of two to three years can be a good choice for novice investors to gain first experience and understand the working mechanisms of the bond market. They do not require constant attention and presence at the terminal, says Pavel Lukyanov, head of the sales department on the debt market of the Moscow Exchange.

Where to choose

- rusbonds – simple, fast, informative. The site contains lists of state, municipal and corporate bonds, information on yield, terms and methods of repayment.

- cbonds – securities in the CIS. Nice design and functionality, calculators and tools for comparing the profitability of different securities.

- Website of the Ministry of Finance , section “Bonds”.

Also, a list of bonds is available from any broker or bank. Bond characteristics may not correspond to reality or be incomplete - check information from several sources.

OFZ and corporate bonds

Any broker or information site will separate government and corporate securities. State ones are considered to be extremely reliable - the state is obliged to pay the bills. Typically, government securities (OFZ) have a maturity of 1-10 years with regular coupon payments.

The annual yield depends on the Central Bank rate. Previously, there were offers with 8-10% per annum. After the Central Bank lowered the rate, yields around 5-6% became the norm. If you add to this the benefit of 13% on IIS, you get a good income .

Private companies try to obtain financing by offering the most favorable terms to investors. For the urgent launch of promising projects, some reliable companies can offer 12-20% per annum , and their securities will be immediately taken up by smart investors. If the company has met its obligations before, why not make money from it? It’s another matter if such interest is offered by a dark horse , a company on the verge of collapse, or an overly secretive legal entity. Are you ready to risk your money to earn an extra 10% per annum? Personally, I am always suspicious of such proposals.

What bonds can you buy in the Russian Federation?

The first bonds in Russian history were issued after the Crimean War. Military operations were carried out with the money of creditors; loans were going to be repaid with indemnity. After the peace treaty, it was necessary to give more financial freedom to entrepreneurs and allow the construction of private railways. The government printed government securities (hereinafter referred to as Securities) for British banks, and railway magnates issued corporate bonds. A few years later, the city authorities also began to sell their own bonds - municipal, the proceeds went to the improvement of cities and infrastructure development. The following types are currently in use:

- State - issued by the state to cover the budget deficit. The redemption of bonds is guaranteed by the state. The most reliable type of securities, and therefore the least profitable.

- Municipal - issued by local authorities, income from them is not taxed.

- Corporate - issued by banks such as Sberbank, VTB or commercial companies to finance projects. High risk, high reward if successful.

Here is a good video about Russian government bonds.

Differences between bonds by yield

- Discount (Zero Coupon) - fully repaid by the issuer on time. Sold at a price below par, redeemed at par. Due to the difference, the holder makes a profit.

- With a fixed rate, coupon profit is paid regularly as a percentage of the face value. The Central Bank does not lose its nominal value.

- With a floating rate - profit is paid regularly, but the interest is tied to agreed economic indicators. Most often - to loan rates.

The specific profit depends only on the conditions under which the security is issued. For example, government ones for a period of one year can bring up to 6% profit. And some UTair will offer 968% per annum. The chance of getting money from government bonds is 99.9% versus 1% for UTair. Choosing bonds is a search for a middle ground with good reliability and the best return.

Issuer Description

State Transport Leasing is one of the largest companies in Russia in terms of the size of its leasing portfolio (exceeded 800 billion rubles as of June 30, 2018). It is an instrument for implementing state policy on the modernization and development of the country’s transport complex. The history of the company dates back to the Civil Aviation Leasing Company CJSC, created in 2001. Subsequently, along with the implementation of programs in the field of air transport, STLC began to work in such segments of the leasing market as road facilities, railway, river and sea transport, transport infrastructure, dynamically increasing and diversifying its portfolio of projects. An increased role in government programs in the transport sector has allowed the company to take a leading position in the industry in recent years.

Examples of bonds

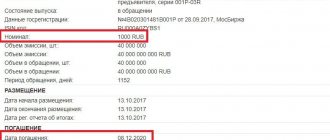

- state - OFZ-26211-PD . Bonds for individuals with a face value of 1,000 rubles in the amount of 15 billion rubles, maturity - 10 years, long-term. The redemption method is coupon; every six months the holder is paid a certain percentage of the face value. Annual yield at 7%, which will bring up to 70% income by the maturity date;

- corporate – VTB-KS-2-311-bob . For individuals, nominal value - 1,000 rubles, total amount - 75 billion rubles, repayment period - one day, short-term. The redemption method is discount, the holder is paid the nominal value. Profit - 0.0186% for the period or 6.79% per annum.

When compiling a portfolio, I recommend paying attention to the following bonds. They are reliable and give a good income.

| Company name (data as of February 2021) | Coupon size, % per annum | Price srvzv. net, % of nominal | maturity date | Ticker |

| Sovcombank-5-bob | 7.5 | 101.08 | 25.11.2027 | RU000A0ZYJR6 |

| Rosneft-002R-04-bob | 7.5 | 104.029 | 03.02.2028 | RU000A0ZYT40 |

| PIK GK-BO-PO1 | 5.65 | 99.29 | 25.02.2022 | RU000A0JXK40 |

| AFK system | 9.75 | 105.21 | 30.09.2025 | RU000A0JVUK8 |

| Uralkali-PBO-04-R | 7.7 | 104.4 | 09.06.2023 | RU000A0ZZ9W4 |

| MTS-001P-06 | 7.25 | 104.612 | 26.02.2025 | RU000A0ZYWY5 |

The price of a bond is formed depending on the method of calculating profit . Government bonds are sold at par value, and the holder receives interest. VTB securities are sold below par value (for 99.9805% of par) and are redeemed at par. only difference is the ease of calculation . In the first case, it is easier for the state to calculate the profit from the sale, and for us - the invested amount; in the second, it is easier for the corporation to calculate its debt, and for us - the profit.

The method of selling bonds “at 90 cents on the dollar” originated in the United States and is mainly used for the sale of corporate securities. Calculating taxes is inconvenient in both systems. By the way, you can quite legally not pay them if you register an Individual Investment Account , I’ll tell you about this later.

Issuer ratings

| Rating agency | Rating | Forecast | Revision date |

| ACRA | A+(RU) | Stable | 28.06.2018 |

| Moody's | Ba2 | Positive | 29.01.2018 |

| S&P | BB- | Positive | 08.08.2018 |

| Fitch | BB | Positive | 19.12.2017 |

Bond yield

The yield on Russian government bonds does not exceed 8% . For good corporate bonds you can get a yield of 10-14% . By collecting a portfolio, you can get an average return of 10% per annum . If you take advantage of the tax deduction and purchase securities for the entire 400,000, we get 10 + 13 = 23% per annum or 92 thousand rubles plus. By choosing profitable bonds, you can get more than 100,000 per year .

Structure of liabilities (IFRS, June 30, 2018)

| Article | Billion rubles | Share |

| Bonds issued | 201,4 | 56% |

| Loans received | 125,4 | 35% |

Finance lease liabilities | 18,3 | 5% |

| Other obligations | 11,9 | 3% |

| TOTAL | 357,0 | 100% |

Where to open an account?

I wrote a separate article about where it is better to open an individual investment account. In short - either at the bank or at the broker . It is better to start working with bonds in a large bank such as VTB or Sberbank - they charge a commission for every sneeze, but they have minimal risk of default and lengthy litigation in an attempt to return the deposit. Personally, I worked through Promsvyazbank , which still offers low commissions and convenient conditions.

You can also work through brokers. A little more commission, a little more ways to extract money from the client - in exchange, we are offered more ways to earn money . For example, PSB’s IIS does not have access to the currency section. You also cannot enter the futures securities market - experienced traders will say that without these high-risk instruments you cannot make money. But we are still learning, so even the absence of leverage will benefit us.

Among the best brokers with virtually no shortcomings, I would like to highlight:

- BCS – there are no restrictions on trading platforms; you can work with Russian shares on the MICEX and St. Petersburg Stock Exchange, and with shares of foreign issuers. If active trading is expected, you can choose the “Trader” tariff plan with a commission reduced to 0.0155%; on the “Investor” tariff it reaches 0.3%.

- Tinkoff Investments - I would call this option ideal for passive investors . There is no convenient terminal here, but you can buy from 1 share and store them for as long as you like. The process itself is no more complicated than purchasing a product in an online store. Here you do not need to pay for account maintenance (the “ Investor ” tariff) and the depository. The commission on the starting tariff plan is 0.3%.

I will provide a detailed comparison of conditions in tabular form.

| Company | Tinkoff investments | |

| Minimum deposit | Unlimited, you can even buy 1 share, they recommend starting from RUB 30,000. | |

| Transaction fee | 0.3% for the “Investor” tariff | 0.05% for the “Trader” tariff |

| Opening, replenishing, closing an account, withdrawing money, service in the depository and exchange commission | For free | For free |

| Account maintenance cost | Free for the "Investor" tariff | 0 ₽ when not trading 0 ₽ if you have a Tinkoff Premium card 0 ₽, if the turnover for the last billing period exceeded 5 million ₽ 0 ₽ for portfolios from 2 million ₽ 290 ₽ in other cases |

| Leverage | Calculated for different instruments, the calculation is linked to the risk rate | |

| Margin call | Depends on the asset | |

| Trading terminals | The purchase of shares is implemented like an online store, professional software is not used | |

| Available markets for trading | American and Russian stock markets | |

| License | TSB RF | |

| Open a Tinkoff account | Open a Tinkoff account | |

Financial position of the issuer

While the company's average annual revenue growth rate (CAGR) in 2012-2017. amounted to an impressive 34%, business margins remain low. Thus, the net profit margin of STLC during this period did not exceed 2.5%; the company ended last year with a net loss of 3.8 billion rubles. (which was mainly due to the creation of reserves). The situation improved somewhat in the first half of 2021: STLC received positive total comprehensive income in the amount of RUB 645 million. against 1.7 billion rubles. loss a year earlier.

The state, as the sole shareholder, is actively recapitalizing the company: in 2009-2017. injections of budget funds into the capital of State Transport Leasing Company amounted to 69 billion rubles; in the first 6 months of 2021, state investments (program for the development of leasing of domestic helicopters) amounted to 5 billion rubles.

The growth of share capital expands STLC's ability to attract market funding. It should be noted that the expansion of the company's business is primarily financed through an active increase in debt. Thus, for the period from January 1, 2021 to June 30, 2021, the volume of the company’s public debt obligations alone increased 5 times - to 201 billion rubles. The volume of attracted loans is also growing - as of mid-2021 it amounted to 125 billion rubles. As a result, the company's capital adequacy (capital/assets) as of June 30, 2018 fell to 16% (in 2015-2017 it was 19-25%). However, continued injections of budget funds into capital will apparently prevent a further decline in this indicator.

"STLC" follows the principle of the unacceptability of accepting currency risks and the emergence of an open currency position. The currency structure of funding and the leasing portfolio are the same - foreign currency financing is attracted only for transactions with clients with foreign currency earnings.

The loan portfolio appears balanced and is represented mainly by long-term loans (as of June 30, 2018, 48% of loans received had a repayment period of more than 5 years). Due to regular replenishment of share capital from the state, stable attraction of funding from Russian state banks and free access to the public debt market, the risk of issuer refinancing appears low.

How to choose a briefcase

brief here , since I have a separate article about the principles of forming a securities portfolio. 60-70% of the portfolio should be guaranteed government bonds. It is difficult to find government securities with a yield above 10%, so we take “people’s” OFZs with different maturities. 35% of the capital (140,000) for OFZ-53002- for a period of 3 years (repaid in 2021, coupon payments twice a year, total yield - 7.67% per annum). another 30-35% for OFZ-25083-PD with an average yield of 6.78% per annum, repayment in 2021. We have 120,000 left , which should be divided into two parts and invested in more profitable corporate bonds. For example, Leventuk-1-bob with a yield of 18% per annum and payment of coupons once a quarter. The downside of the bonds is that full repayment will be in 2027 , but I can always sell them while maintaining the cash flow on the bonds. The remaining 60,000 is the purchase of GTLK-001R-08-bob (8.8% per annum, coupon payments 4 times a year, duration 10 years). Like the previous ones, they can be sold .

Let's calculate the income for one year from the date of purchase of bonds. With OFZ-53002-we will receive 11 thousand, with OFZ-25083-PD we will receive 9,500, with Leventuk - 10,800, with STLC - 5,280. Together we get 36,580 for the first year, the average income is 9% . If you add a tax deduction in the form of a refund, you get 22% or 88 thousand profit for the year of holding bonds. How to calculate profitability? Use a calculator like this one .

Asset structure (IFRS, June 30, 2018)

| Article | Billion rubles | Share |

| Net investment in leasing | 168,4 | 40% |

| Assets leased under operating lease | 162,5 | 38% |

| Cash and equivalents | 16,0 | 4% |

| Other assets | 75,7 | 18% |

| TOTAL | 422,6 | 100% |

Taxes on profits from bonds

If you have an IIS , and the deposit made does not exceed 400,000 per year, you do not have to pay taxes on the profit received of any size. You can open an IIS from any broker with a license to trade securities. We select a broker we like, read the account servicing agreement, look for any problem areas (like a commission of 100 rubles for each transaction). We agree if the conditions suit you. We read the instructions for opening an account in a specific company, follow all the steps, wait several days for the application to be processed and the account to be opened. Have you opened it? Then read on.

Investment risks

There is always a risk. Even the state, under certain conditions, will not be able to pay off its obligations - the USSR is an example of this. Corporations and banks offer profits from 7% per annum, there are options with 100% and higher. Everyone understands that such proposals signal that “a young dynamic company is on its last legs and desperately looking for money.” But some investors can take a risk and invest in such a company in order to receive their profit in case of success, and in case of bankruptcy - to sue. But it is better not to touch risky options until you have experience in investing. risks can be identified in any bonds :

- Interest rate risk . The price of bonds in the market is inversely proportional to the average interest rate. If I bought bonds at 8% per annum, but securities at 10% suddenly appeared on the market, I will try to sell the portfolio in order to get money to buy more profitable bonds. And I will sell below par if the loss on the sale covers the profit from the higher annual interest. Where is the risk here? Bonds may lose value due to the release of more profitable securities.

- Reinvestment risk . I bought a Central Bank at 15% per annum for a period of 3 years. Two months passed, the valuation of the bonds changed, the issuer decided to call them back! Yes, he has such a right if this is agreed upon when issuing securities. The issuer gives me my money, interest for two months and a small compensation. But instead of 45% of the profit over three years, I only have money in my hands, which again needs to be invested somewhere. The same issuer again offers me to buy its debt obligations, but at 10% per annum. You will have to be content with less profit.

- Inflation risk . Everything is simple here - in 2013 the dollar was at 30, I bought people's bonds at 30% per annum (dreams, dreams) for 3 years. In 2021 I received 90% of the profit, the ruble depreciated by half. Total - I lost 10% in value. I regret not buying dollars.

- Default risk . We buy some “Horns and Hooves” securities at 100% per annum and pray. Three days before repayment, the company defaults and disappears into thin air along with its money, property and personnel. It sounds exaggerated, but even the largest banks and giant corporations could declare bankruptcy tomorrow. To assess the risk, you need to look at the statements and compare the company's profits with the amounts that it must repay for its debts. The lower the debt relative to projected earnings, the lower the chance of bankruptcy and default.

- Credit rating risk . I woke up, saw bonds at 15% per annum from a small and fairly reliable company, and bought myself several bonds. The Standard & Poor's analyst woke up and looked at the company's reporting. I decided that they would not be able to repay their obligations, and gave them a credit rating of D (nowhere lower). The bank director woke up, saw D, sweated with excitement and raised the company's loan rate. The head of the company is horrified, but there is nowhere to go - he needs to attract investment by offering more favorable interest rates. Investors woke up and saw new Central Banks at 20% per annum. “Something is unclean here...” they thought and went to look at other papers. The company was unable to attract investment and closed, and I lost money.

- Liquidity risk . I bought bonds for a period of 5 years, but I suddenly and urgently needed money. It turned out that no one needed the obligations of the local candle factory on the stock exchange, and I had to sell the securities for 50% of the face value. Some bonds are simply illiquid and, if necessary, difficult to sell to other investors.

You can reduce the risks to nothing if you study the market, the situation in the country, the general situation on the market, interest rates, credit ratings, reports of the selected company and a dozen important things . And still, the risk cannot be avoided - the most reliable issuer will face force majeure in the form of a meteorite falling on the main office and will not be able to repay its debts. In simple words: limit risks by distributing capital between 5-10 types of securities.

Alternatives

There are several alternatives to bond trading - investing money in deposits, storing money in unallocated metal accounts or buying different shares, that is, investing in mutual funds.

Deposits are the most stable, but they bring the lowest profit. Today, interest on deposits will barely protect your nest egg from inflation, and sometimes it won’t even be enough for that. Thus, the average rate on bank deposits ranges from 1 to 7%. The inflation rate, according to the Central Bank, for 2021 was 4.3%, and for 2019 - 3%.

Moreover, banks offer high rates of 4% for long-term deposits for a period of 12–18 months without the possibility of withdrawal and for amounts from 1,400,000 rubles. Let me remind you: deposits are insured only up to 1,400,000 rubles in each bank. Obviously, such a deposit is beneficial to the bank itself, but not to you and me.

Unallocated metal accounts allow you to buy gold, silver, palladium and platinum not in physical bullion, but also virtually. The advantages here are that such metals are steadily growing in price and are a “safe haven” in times of crisis. The disadvantages are that these deposits are not protected

Accordingly, they can be opened only in the most reliable banks by the Deposit Insurance Agency. However, this instrument is only beneficial for long-term investments. It is not suitable for short-term trading, since the rates for selling and buying metals from the bank vary.

And in order to make up this difference, you need to wait until the price of the metal increases significantly. And this takes a long time.

Mutual funds allow you to earn income from securities without purchasing them directly and spending time learning the intricacies of trading. The fund is created by a management company, which accumulates the funds of shareholders and then invests them in various assets. As a rule, management companies offer ready-made securities portfolios; an investor just needs to buy a share and expect a profit.

Portfolios are distinguished by the direction of investment: stocks, bonds, foreign exchange market, mixed investments. A unit in a mutual fund that engages in high-risk activities can yield 15–25% per annum, while a unit in a bond fund will yield 5–10% per annum. But at the same time, the owner of the share bears the same risks as an ordinary investor. That is, he is in no way insured against losing all his money if the mutual fund goes into negative territory.

A more profitable analogue of a mutual fund is ETF. In essence, they are close: an investor also buys a share, only if the management company of a mutual fund invests in certain assets, then an ETF invests in a stock index, i.e., in an entire industry at once.

Let's sum it up

Bonds are a profitable and reliable alternative to bank deposits. Interest on bonds varies from 7% to 20% per annum, terms - from one day to 15 years . Payments on bonds can be received once at the end of the term or regularly throughout the term. Payments are calculated as a percentage of the bond's face value. Bonds can be sold on the market at any time. The most reliable investment option is to buy people's federal loan bonds .

Securities are issued by the state, local authorities and legal entities. State and municipal securities are the most reliable, corporate securities are the most profitable. It is important correctly assess the risks of bonds so as not to lose your deposit and not sue for compensation. For each type of bond there is a minimum and maximum quantity for purchase - read the conditions. For transactions worth less than 400,000, you can make a tax deduction of 13% (52,000 for 400,000).

Information can be found on special websites, on the Ministry of Finance website and from brokers. You can buy bonds at a bank or from a broker; to do this, you need to open an investment account and sign a contract. Read the contract slowly and thoughtfully - brokers make money on inattention and commissions. An investor's life credo is don't put all your eggs in one basket .

That's all for today. Subscribe, tell your friends, learn new information and get rich.

If you find an error in the text, please select a piece of text and press Ctrl+Enter. Thanks for helping my blog get better!

Trader reviews

On forums, experienced and less experienced stock market players share their opinions and talk about their trading strategies.