RusHydro. We came to support 6 times - we are waiting for growth

Address for questions and suggestions about the site: [email protected]

Copyright © 2008–2021. LLC "Company BKS" Moscow, Prospekt Mira, 69, building 1 All rights reserved. Any use of site materials without permission is prohibited. License for brokerage activities No. 154-04434-100000, issued by the Federal Commission for the Securities Market of the Russian Federation on January 10, 2001.

The data is exchange information, the owner (owner) of which is PJSC Moscow Exchange. Distribution, broadcast or other provision of exchange information to third parties is possible only in the manner and under the conditions provided for by the procedure for using exchange information provided by Moscow Exchange OJSC. Brokercreditservice Company LLC, license No. 154-04434-100000 dated January 10, 2001 for brokerage activities. Issued by the Federal Financial Markets Service. No expiration date.

* The materials presented in this section do not constitute individual investment recommendations. The financial instruments or transactions mentioned in this section may not be suitable for you and may not correspond to your investment profile, financial situation, investment experience, knowledge, investment objectives, risk appetite and return. Determining the suitability of a financial instrument or transaction for investment objectives, investment horizon and risk tolerance is the responsibility of the investor. BKS Company LLC is not responsible for possible losses of the investor in the event of transactions or investing in financial instruments mentioned in this section.

The information cannot be considered a public offer, an offer or an invitation to purchase or sell any securities or other financial instruments, or to make transactions with them. The information cannot be considered as guarantees or promises of future investment returns, risk levels, costs, or break-even of investments. Past investment performance does not determine future returns. This is not an advertisement of securities. Before making an investment decision, the Investor must independently assess the economic risks and benefits, tax, legal, and accounting consequences of entering into a transaction, his readiness and ability to accept such risks. The client also bears the costs of paying for brokerage and depositary services, submitting orders by telephone, and other expenses payable by the client. The full list of tariffs of BCS Company LLC is given in Appendix No. 11 to the Regulations for the provision of services on the securities market of BCS Company LLC. Before making transactions, you also need to familiarize yourself with: notice of risks associated with transactions on the securities market; information about the client’s risks associated with making transactions with incomplete coverage, the occurrence of uncovered positions, temporarily uncovered positions; a statement disclosing the risks associated with conducting transactions in the market for futures contracts, forward contracts and options; declaration of risks associated with the acquisition of foreign securities.

The information and opinions provided are based on public sources that are recognized as reliable, however, BKS Company LLC is not responsible for the accuracy of the information provided. The information and opinions provided are formed by various experts, including independent ones, and opinions on the same situation can differ radically even among BCS experts. Given the foregoing, you should not rely solely on the materials presented at the expense of conducting independent analysis. BKS Company LLC and its affiliates and employees are not responsible for the use of this information, for direct or indirect damage resulting from the use of this information, as well as for its accuracy.

Analysis of the issuer. RusHydro

RusHydro is one of the largest electricity generating companies in Russia and a leader in the renewable energy industry.

The group unites more than 90 energy facilities in Russia and abroad, thermal power plants and power grid assets in the Far East.

The total installed capacity of power plants is 39.1 GW or 16% of all Russian generation. The installed capacity of solid fuel power plants, which are concentrated in the Far East, is 8.3 GW. The thermal power of stations in the Far East is 18,147 Gcal/h.

Of the foreign assets, it owns the Sevan-Hrazdan cascade of hydroelectric power stations in the Republic of Armenia - 7 stations with a total installed capacity of 561 MW. The company's assets also include electrical companies.

Structure of the RusHydro group

The group of companies operates in three main reporting segments. This is the parent PJSC RusHydro, the subgroup ESK RusHydro and the subgroup RAO ES of the East. A complete list of all controlled energy facilities is shown in the graph above. It is worth noting that RusHydro’s share in companies included in each segment is not always 100%.

Below is a table with results for 2021 by segment in million rubles.

Based on the table above, it can be seen that the main segments in terms of revenue are the parent RusHydro and RAO ES of the East. However, it is worth saying that the profitability of the latter is extremely low. Even taking into account higher revenues and government subsidies, EBITDA from the Far Eastern assets is lower than that of the parent company. The main negative of the RusHydro case is concentrated in this segment.

The weakest link

At the level of net profit, RAO UES of East ended 2021 with a loss of 13.4 billion rubles . including subsidies. A year earlier, the loss amounted to 6.2 billion rubles . This is due to the inefficiency of enterprises and, as a consequence, high operating costs.

One of the main expense items is fuel - 58 billion rubles. Also a big expense item is personnel and electricity distribution. Impairment of accounts receivable and fixed assets is common.

Old inefficient capacities need to be modernized, which will be the subject of a future large-scale investment program, which will be discussed later.

One can also note an increase in financial expenses, despite a decrease in the debt burden from 86.9 billion rubles. in 2021 to 43.3 billion rubles. in 2021. For this purpose, the RusHydro group in 2017. it was necessary to carry out an additional issue of shares in favor of VTB and sell treasury securities in the amount of 55 billion rubles. , eroding the share of existing shareholders.

As a result, interest expenses of RAO ES East actually fell by half. But the money from VTB came in the form of a loan from the parent RusHydro, which is a hybrid financial instrument that is reflected at fair value with changes in profit or loss depending on the dynamics of the shares of the RusHydro group on the Moscow Exchange. In total, due to the fall in share prices, RAO ES of the East had to record a loss of 10.8 billion rubles . The loss is still paper, but under the terms of the forward contract with VTB it may well become real.

Investment program

Another weak point of RusHydro’s case, at least in the short term, can be safely noted as the high investment program for 2018-2023. Its volume, taking into account projects in the Far East, will amount to more than 443 billion rubles .

From 2021 to 2023, the Group plans to commission: the first stage of Sakhalinskaya GRES-2, the 3rd hydroelectric unit of the Ust-Srednekanskaya HPP, Nizhne-Bureyskaya HPP, Zaramagskaya HPP-1, Vostochnaya CHPP, CHPP in Sovetskaya Gavan, 1- th stage of construction of two single-circuit high-voltage lines 110 kV Pevek-Bilibino and others. In total, RuHydro should gain more than 1.5 GW of new capacity over the years.

In addition, the company continues to implement a comprehensive modernization program (CMP), within which it is planned to replace more than half of the main equipment at hydroelectric power plants. The implementation of PCM makes it possible to achieve a noticeable increase in power. In 2021 this is 42.5 MW . In 2021, it is planned to increase the installed capacity of hydroelectric units by another 46.5 MW . But these capital expenditures are not subject to the return on investment program under the CSA.

In 2021 The RusHydro group allocated a total of 92 billion rubles . Far Eastern assets accounted for 26.4 billion. In 2021, investments across the group are planned at the level of 122.8 billion rubles. But according to the current plan, this will be the peak of capex.

Management reported that the program would be balanced across funding sources. This means that we can expect both an increase in the debt burden and the next additional issue. If assessed subjectively, the company is trying not to increase debt. Last year, ACRA assigned RusHydro a credit rating at the highest level of reliability “AAA(RU)” on the national scale, with a “stable” outlook.

To better understand the scale of capital expenditures, we can assume that for the next six years RusHydro plans to spend on average about 74 billion rubles. in year. At the same time, the group’s EBITDA for 2021 amounted to 104 billion rubles, and in 2021, according to management forecasts, it will be even less - 93.8 billion rubles. That is, the figures are generally comparable and very high.

And this does not take into account the thermal generation modernization program for 2022-2035. Earlier, during a teleconference following the results of 2021, management reported that it was focusing on modernizing approximately 1.3 GW of heat generating capacity in the Far East. This may require another 300-350 billion rubles. investments.

But later the figures were 140-150 billion rubles. The first modernization costs are planned for 2021. This means that the current investment program plan will be adjusted. The coal-fired Artemovskaya CHPP (455 MW), the gas-fired Khabarovskaya CHPP (344 MW of new construction) and the Yakutskaya GRES (145 MW) should be modernized. Perhaps other facilities will be announced later, because the total declared capacity remained at 1.3 GW.

But the plus is that these costs will be compensated according to the new DPM-Shtrikh program, which will provide additional income from the sale of capacity after the modernized facilities are put into operation.

Separately, it is worth mentioning the investments in the construction of the Taishet aluminum smelter (TaAZ) together with the Rusal group. The cost of entry into the project is no more than $319.5 million . The group will partially pay for the investment project with shares of OJSC Irkutsk Electric Grid Company in the amount of $150 million. RusHydro planned to pay another $150 million by paying off TAZ's debt to the companies of the Rusal Group after reaching its design capacity. RusHydro could repay the remaining $19.5 million in installments over three years.

But due to US sanctions against Rusal, the project was in question. However, at the AGM of RusHydro management stated that they would re-discuss Rusal’s entry into the project for the construction of the Taishet aluminum smelter in the Irkutsk region, taking into account the changed conditions on the metal market.

Capital structure and additional issues

In March 2021, RusHydro entered into a 5-year forward contract with VTB Bank for RUB 55 billion. As a result, the company carried out an additional commission of 40 billion shares and sold another 15 billion in treasury securities. The money received from the bank was used to partially repay the debt of RAO ES of the East.

RusHydro will pay interest on the forward (Central Bank rate + 1.5%) minus dividends paid to VTB. But if, after the expiration of the deal, the price of RusHydro shares is below 1 ruble, then the company will have to return the difference. If it’s higher, VTB will have to compensate for the difference.

As a result of the additional issue, VTB ended up with 13.3% of the shares. The Russian Federation accounts for 60.5%. Free - Float is about 25% . However, on June 21, 2021, the Board of Directors of RusHydro approved another additional issue of 14,013,888,828 ordinary shares with a par value of 1 ruble. A share of 10 billion shares will be paid for by the main shareholder - the Russian Federation. These funds were approved in the budget at the end of last year.

The scope and terms of the placement provide for granting shareholders a pre-emptive right to purchase shares. It is expected that the funds received from the additional issue will be used to finance the construction of power lines in Chukotka. At the same time, the company plans to spend no more than 5 billion rubles on the project from its own funds.

Thus, the Russian Federation’s share in RusHydro’s capital will increase to 60.9%. But the latest additional issue will dilute the share of non-participating minority shareholders by 3.2%, which in general is not that much. Taking into account the redemption of the issue at par and its phased implementation, the negative impact on quotes is limited.

In general, it is worth noting that this is not the first and, apparently, not the last additional issue of RusHydro shares. For example , in 2012 additional capitalization by the state for 50 billion rubles. The funds received were intended for the construction of new facilities in the Far East.

Debt load

Over the past three years, RusHydro has demonstrated a significant reduction in debt. Net Debt/ indicator has decreased since 2015 from 2.4x to 1.4x at the end of 2021. The group’s net debt for 2017 decreased by 8.4%, to RUB 143 billion. At the same time, the greatest impact on the dynamics of debt was the repayment of part of the debt obligations of RAO ES of the East with the help of funds raised from an additional issue in favor of VTB.

But as we found out above, at the moment the forward transaction with VTB involves provisions for financial losses in the amount of depreciation of shares. In addition, the group pays interest on the forward (Central Bank rate + 1.5% minus dividends paid by VTB), which is also negative and does not fully mean a reduction in the debt burden.

The group's debt portfolio is mainly concentrated in bonds. About 40% comes from bank loans. Debts are denominated primarily in rubles. There are no currency risks in this regard. The average cost of debt is about 8.6% per annum.

The amount of debt in relation to EBITDA, as well as the repayment schedule, currently looks quite comfortable. However, do not forget about the massive investment program for the next 6 years. The company will try to take advantage of good credit ratings (S&P - BBB-; ACRA - AAA(Ru), outlook "stable") and low borrowing costs, which will most likely worsen its debt profile.

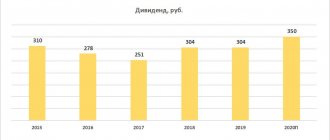

Dividends

One of the positive aspects of the RusHydro case could be called its dividend policy. The company has increased payments for 5 years in a row , both per share and in aggregate.

But weak profit results in 2021. were able to provide only 11.2 billion rubles. dividends or 0.026 rubles. per share. The dividend yield dropped from 6.3% for 2021 to 3.8% at the end of 2021.

In accordance with the current dividend policy, at least 5% of the net consolidated profit under IFRS can be allocated for payments to shareholders at the end of the year. But thanks to the adopted Plan for increasing the value of RusHydro until 2021, aimed at increasing the fundamental and market value of the group, and the Government directive on dividends of state-owned companies, the issuer has spent the last three years paying out 50% of net profit. In addition, the scenario of paying dividends from positive cash flow may be considered in the future.

Thus, if the profitability indicator is restored and management guidelines remain unchanged, RusHydro could become a good dividend story.

Production figures

During 2021, the installed electrical capacity of the RusHydro group increased by 170.37 MW and by the end of the year amounted to almost 39.1 GW. The increase in capacity was ensured by the commissioning of the first stage of Yakutskaya GRES-2, technical re-equipment of the Zhigulevskaya HPP, Volzhskaya HPP, Saratovskaya HPP and Novosibirsk HPP.

Meanwhile, some facilities of RAO ES East were decommissioned, at JSC Chukotenergo and PJSC Kamchatskenergo for a total of 45.9 MW.

It is worth noting that, according to the investment program, the removal of old inefficient capacity will continue in the coming years. Part of it will be modified. At the same time, new capacity will also be added under the PCM program and during the construction of new generating facilities under the CSA program.

In 2021, the first stage of Sakhalinskaya GRES-2 (+120 MW), GTU CHPP (139.5 MW + 432 Gcal/h), Zamaragskiye HPPs (+342 MW), Ust-Srednekanskaya HPP (+142.5 MW) is expected to be commissioned. It is planned to spend 71.2 billion rubles on new construction in 2021 . The bulk of new facilities currently under construction should be completed by the end of 2021.

Electricity generation of the RusHydro group in 2021, including the Boguchanskaya HPP, increased by 1.06% compared to 2021 and reached a record - 140,285.6 million kWh. The useful supply of electricity also increased significantly - to 135,913.8 million kWh.

The operating performance of the group as a whole depends largely on the state of the hydrological parameters of the reservoirs on which the generation facilities are located. In addition, the production and supply of electricity, as well as thermal energy, depends on weather and climatic conditions.

Modernization and commissioning of new capacities also plays an important role. For example, record volumes in 2021 are ensured by the commissioning of the Yakutskaya GRES-2 in the fall of 2021 and the gradual achievement of the design output of the second stage of the Blagoveshchenskaya CHPP, commissioned in 2021.

But thanks to the large share of hydro generation, there is also a seasonal factor in the company’s production indicators. Below is the dynamics of energy production over the past few years.

Thus, in connection with the expectation of an increase in installed capacity, one should not be surprised at the increase in electricity generation, adjusted for climatic and hydrological factors. However, we note that most energy market participants see excess capacity on the market in 2017-2023. This may put pressure on prices on the wholesale electricity market.

Financial indicators

The group's revenue in 2021 decreased by 2.7% compared to 2021, which was due to the disposal of ESKB LLC and a drop in income from the sale of electricity against the backdrop of lower tariffs in the Far East. However, the last factor was compensated by government subsidies. But there are questions about the timing of compensation. Companies that are one way or another involved in energy supplies in the Far Eastern Federal District may temporarily develop a cash gap due to a lag in the receipt of subsidies to specific counterparties.

Like-for-like revenue, excluding the Bashkir Energy Sales Company, increased by 5.4% . For 2021, the company plans to increase revenue to RUB 394,162 million . (including government subsidies).

Meanwhile, operating expenses excluding ESKB grew slightly higher, by 5.6% YoY. The main cost items are the increase in personnel costs, energy distribution and fuel costs.

EBITDA in 2017 increased by 3.6% . This is due to the growth in electricity generation, the increase in power prices on the wholesale market and the increase in power sales with the introduction of new facilities. The increase in margins is due, among other things, to the sale of non-core assets.

Long-term EBITDA dynamics indicate the company's sustainable development, in particular due to the implementation of the investment program, liberalization of the wholesale electricity market and tariff increases. Electricity tariffs increased in 2015-2018. by 12% in the European part of the Russian Federation and 11% in Siberia.

However, the final result for 2021 turned out to be significantly worse than the previous reporting period. Net profit under IFRS decreased by 43.5% and amounted to 22.5 billion rubles. This happened against the backdrop of an increase in financial expenses and depreciation of fixed assets and receivables.

We note the loss from economic impairment in relation to JSC Yakutskaya GRES-2 and PJSC Yakutskenergo in the amount of 24 billion rubles . This was caused by insufficient tariff revenue, which does not provide a full return on invested capital.

Financial loss 13.9 billion rubles. appeared due to the revaluation of the forward contract with VTB. Accounts receivable depreciated by almost 6 billion rubles .

Thus, future net income on the basis of which dividends will be paid is highly dependent on asset impairment charges. Taking into account the construction of new facilities, we assume write-offs in the future.

Interesting point. The fall in RusHydro shares is ultimately strengthened by positive feedback against the background of a decrease in dividend yield due to write-offs under the contract with VTB. But the opposite dynamics of securities, on the contrary, will affect the improvement of the company’s financial results, thereby further supporting quotes.

Management forecasts

According to the adopted program for increasing the fundamental and market value of RusHydro until 2021, the management was set goals of reducing costs and increasing the efficiency of the group. Most of these were achieved in 2021, with the exception of positive stock performance.

From the table above, it is worth especially noting the expected decrease in EBITDA in 2021. Free cash flow will remain negative, although it may improve compared to 2021. In 2021, management forecasts an increase in both indicators, which certainly creates a positive basis for RusHydro’s investment case .

Separately, it is worth noting points 7 and 8. Increasing labor productivity and reducing operating costs is what the weakest link of the group, RAO ES of the East, primarily needs. Management's forecast is encouraging.

conclusions

Strengths

1. Long-term potential of the company . According to the dynamics of EBITDA, the company is on the path of sustainable development. Technical re-equipment and new generating facilities create the potential for growth of installed capacity and income in the future. High business EBITDA margin. Potentially unlimited resources (water) to create profit.

2. CSA program . The company continues to build and commission facilities under a guaranteed return on investment program, which will provide additional income from the sale of capacity in the coming years.

3. Dividend policy . With the exception of 2021, the company has consistently increased its dividend payments. The coefficient is 50% of net profit according to IFRS. There are plans to transfer payments from FCF, which would be positive if the level for dividends is simultaneously maintained at no lower than 50% of profit under IFRS (Government Directive).

4. Management forecasts . And although at the end of 2018 a decrease in EBITDA is predicted, in general, management’s expectations are fully consistent with the dynamics of production indicators, the progress of the investment program and the tariff policy. Particularly interesting is the positive FCF, which can be a good trigger for stock growth.

5. Trend towards cost reduction. Management's forecasts through 2021 assume a consistent reduction in operating costs and an increase in labor productivity. The indicators for 2021 turned out to be quite good, and there is an expectation that the dynamics will continue in light of the large room for maneuver, especially in Far Eastern assets.

Weak sides

1. RAO ES East . The weakest link in the case, which significantly worsens the final result for the group, even taking into account subsidies.

2. Large investment program. While this is still positive in the long term, it does put pressure on cash flow in the short term. Considering that RusHydro is a state-owned company, there are great fears of a permanent increase in capital costs, even without taking into account the modernization of old thermal generation.

3. Deal with VTB . Currently, RusHydro is forced to incur losses due to the revaluation of the forward. Considering the payments under the contract, the reduction in debt burden is formal. A stock decline and forward financial losses are mutually reinforcing factors.

4. Write-offs and impairments of fixed assets. Non-cash write-offs for constructed facilities as a result of economic impairment.

5. Regulation of tariffs in the Far East. This may lead to a lag in the receipt of subsidies from the state, which will negatively affect the reported financial indicators.

6. Additional issues. As a result of the high investment program, the company needs additional capitalization. To a large extent, it is carried out through the issue of new shares.

Thus, on the one hand, investors may be wary of RusHydro shares due to the high investment program, additional issues, periodic write-offs and impairments, as well as financial losses in the deal with VTB. RusHydro shares have been gradually declining since the 1st quarter of 2021, showing worse dynamics than the Moscow Exchange index. Considering the forecast for a decline in EBITDA in 2021 and the peak of the investment program, we assume that the dynamics will continue to be inexpressive in the coming quarters.

However, the financial profile of the company, according to management forecasts and plans for implementing the investment program, should improve noticeably over the next 2-3 years. Most of the capex will be completed. New costs for the modernization of thermal generation in the Far East will be provided by additional income under the DPM-Shtrikh program. Dividend policy and management's attitude to costs also speak in favor of positive disclosure of the long-term potential of the stock. The expected increase in dividend yield as FCF enters positive territory, according to the company's forecasts, should help increase the attractiveness of the shares.

Short term, medium term: neutral view

Long term: moderately positive outlook

Konstantin Karpov

BCS Broker

RusHydro's net profit for 2021 is expected to be higher than in 2021. But it could have been better

The capacity of power plants of the RusHydro group in 2021 increased by 335 MW, incl. hydroelectric power station capacity - by 50 MW.

The head of RusHydro N. Shulginov reported this to the President of the Russian Federation V. Putin during a working meeting held in the Kremlin on January 11, 2019.

During the meeting, N. Shulginov reported on the results of RusHydro’s work and plans for the near future.

In 2021, RusHydro demonstrated steady growth in operating indicators.

Electricity production for the group as a whole and for hydroelectric power plants (HPPs) in particular is higher, although the previous year was also a record year.

The capacity of power plants increased by 335 MW due to the commissioning of the Vostochnaya CHPP in Vladivostok with a capacity of 140 MW.

The modernization of the hydroelectric power station continues - the commissioning of the 3rd hydroelectric unit at the Ust-Srednekanskaya hydroelectric power station has been completed, the penultimate hydroelectric unit of the hydroelectric power station on the river. Kolyma, Magadan region.

As a result of the modernization of hydroelectric power stations, their capacity increased by 50 MW.

According to RusHydro’s financial indicators for 2021, N. Shulginov is full of optimism.

Revenue at the end of 2021 is expected to be 407 billion rubles, EBITDA - about 102 billion rubles, net profit - 30 billion rubles.

The figures could have been even higher, but the depreciation factor had an impact.

N. Shulgino noted that the non-monetary effect is recorded due to unpaid projects in the Far East, for which write-offs have to be reserved.

But still, RusHydro’s profit for 2021 is expected to be higher than in 2021.

This will allow RusHydro to pay dividends 35% higher than in 2017; RusHydro plans to submit this proposal to the Russian government.

According to N. Shulginov, this will be exactly 50% of the profit according to IFRS.

Tax payments to budgets of all levels will also increase to 78 billion rubles.

RusHydro has serious plans for 2021.

The business plan for 2021 was adopted by the company's board of directors with revenue growth.

But there is also an increase in costs due to an increase in the cost of the fuel basket by 10.5 billion rubles. or by 17%.

Of this 17%, 9.5% is due to rising coal prices.

RusHydro's plans for 2021 include completing the construction of the Sakhalinskaya GRES-2 and Nizhne-Bureyskaya HPPs.

It is also necessary to complete the construction of a thermal power plant in Sovetskaya Gavan and Zaramagskaya HPP-1 in the Republic of North Ossetia-Alania.

Work will continue on the program for replacing retired facilities and on the program for modernizing thermal energy in the Far East.

Regarding some positions of the Far Eastern projects, N. Shulginov turned to V. Putin for support.

N. Shulginov also asked V. Putin to entrust the implementation of these programs to the operating companies of RusHydro - the Far Eastern Generating Company, and the Far Eastern Distribution Grid Company and RAO ES of the East.

In addition, RusHydro is counting on government support, which will provide profitability comparable to the modernization program in the European part of Russia, Siberia and the Urals, i.e. about 14%.

Another support measure would be to pay the cost of these projects at the expense of wholesale market consumers.

This model has been tested in the Kaliningrad region, showing its success.

The company wants to double profits by 2025

According to Kommersant, RusHydro expects a noticeable increase in financial indicators in the coming years. The state company’s draft business plan includes a forecast for net profit growth in 2021 by 43%, to 47.86 billion rubles. The reason is the end of the period of large “paper” write-offs after the commissioning of planned unprofitable power units in the Far East. The consequence may be an increase in the base for dividend payments. In general, by 2025, the company sets itself the task of doubling net profit and increasing EBITDA by 30% - apparently, due to new power buildings in the Far East, which should already be profitable.

In 2021, RusHydro expects its nominal net profit under IFRS to grow by 43%, to 47.86 billion rubles, according to the company’s draft business plan, which the board of directors will have to approve in January (available to Kommersant). Revenue according to the business plan for 2021 is expected to be 456.6 billion rubles, income from the sale of electricity and capacity is estimated at 69.5 billion rubles. EBITDA in 2021 could amount to 107.39 billion rubles, the debt to EBITDA ratio will reach 2.4.

In 2021, RusHydro's results will likely be above plan due to the ultra-high water content of Siberian rivers.

Thus, the current forecast for nominal net profit for 2021 is 33.4 billion rubles, for revenue - 437.63 billion rubles, EBITDA - 107 billion rubles. But in January-September the company increased its electricity production by 13.7%, to 112.7 billion kWh, and the output of hydroelectric power stations and pumped storage power plants increased by 17.2%. As a result, already in the first nine months of 2020, RusHydro’s net profit increased by 1.72 times, to 60.5 billion rubles, and revenue and EBITDA - to 311.2 billion rubles. and 90.5 billion rubles. respectively.

In recent years, the company's financial performance has been significantly affected by write-offs of capital costs for the construction of stranded assets in the Far East. But RusHydro reported that in 2021 there will be no significant write-offs, 2021 will also pass without them, which in the future will allow dividends to be increased by 1.6 times, to at least 25 billion rubles. in year. According to the dividend policy, the level of payments must be at least 50% of net profit according to IFRS and at the same time not be lower than the average level for the last three years. However, in 2022–2023, write-offs will return again due to the commissioning of the Pevek-Bilibino power line and the last hydraulic unit at the Ust-Srednekanskaya HPP.

RusHydro refused to comment to Kommersant on the draft business plan.

In 2022–2025, according to the company’s forecast, net profit will grow and in 2025 will reach a record 70.2 billion rubles, immediately increasing by 14.4% relative to 2024 (see chart). This will probably be associated with the start of receiving revenue from the launch of new Far Eastern projects of RusHydro - the reconstruction of the Vladivostok CHPP-2 and the construction of power units at the Khabarovsk CHPP-4 and the Yakutskaya GRES-2 (second stage). Artemovskaya CHPP-2 should also be launched in 2026. These projects are expected to receive long-term capacity payments that guarantee a return on investment. The investment program of RusHydro in 2021–2025 will amount to 502.8 billion rubles, the volume of new commissionings will be 1.4 GW.

RusHydro wants to invest 14 billion rubles over 12 years. repair of heating networks and boiler houses in the Far East

At the same time, the forward contract with VTB should expire in 2025, which could affect the company’s net profit both positively and negatively: RusHydro will have to sell 13% of its shares currently owned by VTB to a strategic investor - and if the sale price is is higher than the forward par value (1 ruble per security), then the difference is paid by RusHydro, if lower - by VTB. On January 10, RusHydro shares on the Moscow Exchange were trading at 0.79 rubles.

Vladimir Sklyar from VTB Capital expects a repeat of the successful 2021 in 2021: EBITDA should remain at the same level, and net profit should grow due to the absence of write-offs from the revaluation of commissioned energy facilities.

This should lead to an increase in dividends to RUB 24–25 billion. per year (which means 7.5% dividend yield). In fact, the analyst adds, the company expects net income to double and EBITDA to grow 30% over five years. The pace is similar to that set in the strategy of another energy state (EBITDA growth by 50% over five years) - and significantly exceeds the sector average. They can be achieved primarily by abandoning economically unjustified projects due to the fact that the company’s new investments in the Far East will have a guaranteed payback mechanism.

Tatiana Dyatel