Arbitrage, or cash and carry , is a strategy in which a trader takes advantage of the difference between the price of an underlying asset and the price of its derivative. The key to making a profit is restoring this discrepancy. This trading strategy allows an investor to take advantage of divergences in market prices. Typically, a trader is simultaneously long a security or commodity and short a related derivative, particularly a futures or options contract.

The trader holds the purchased security or commodity until the delivery date of the contract and uses it to cover the obligations of the short position. By selling a futures, the investor opens a short position and already knows how much he will receive on the delivery day and the value of the security thanks to the long position.

For example, in the case of bonds, the investor receives the coupon payments on the purchased bond, plus the income received from investing the coupons, as well as a predetermined value on the future delivery date.

The concept is quite simple.

- An investor finds two securities whose values do not match each other. For example, the spot price of oil and the price of oil futures diverge and create an arbitrage opportunity.

- The investor first buys oil at the spot price and sells an oil futures contract, then holds (“carries”) the spot oil until the contract expires and then delivers the commodity purchased at the spot price.

- Regardless of how much delivery costs, a profit is guaranteed if and only if the spot price plus the holding cost is less than the original selling price of the futures.

(the difference between the spot price of a commodity and the price of a futures contract for the same commodity). Often, carry trades resort to arbitrage trades to take advantage of the interest rates generated on positions, which may ultimately prove to be more profitable than borrowing or lending through traditional channels.

Basic moments:

- Cash and carry is an arbitrage strategy that exploits the discrepancy between the prices of an underlying asset and a corresponding derivative.

- Typically, an investor takes a long position in an asset and simultaneously sells a related derivative, particularly by shorting a futures or options contract.

- A profit is guaranteed if buying crude oil on the spot market, plus the cost of holding, turns out to be more profitable than initially selling the futures.

Example

Let's say the asset is currently trading at $100 while the one-month futures contract is priced at $104. In addition, monthly holding costs such as storage, insurance, and financing costs for this asset are $2. In this case, the trader will buy the asset (long) for $100 and simultaneously sell the monthly futures contract (short) for $104. The cost to buy and hold the asset is $102, but the investor has already locked in a sale for $104. The trader will then hold the asset until the futures expiration and deliver it to the contract, thereby generating an arbitrage or risk-free profit of $2.

What is arbitration in simple words

Arbitrage, in simple terms, is a low-risk trading technique in which the trader makes a profit regardless of the direction of price movement. Profit is formed due to the discrepancy in prices for the same asset on different trading platforms. This is just one of the subtypes of this tactic; derivatives ( futures and options)

), as well as the time factor.

Arbitrage is always a relatively small income; in trading there is always a direct relationship between the level of risk and profitability. In this tactic, the risk is reduced to a minimum, which also affects the size of the profit.

This approach is not a ready-made strategy; it is rather an idea, a foundation on the basis of which both manual and automated trading systems are created. The main difficulty in developing a trading system is the algorithm for selecting assets for arbitrage and automating the opening and closing of positions. Market inefficiencies usually disappear quickly and it is not always possible to “catch” them manually.

Arbitration operations

There are many different asset management strategies in the stock market, which are very highly ranked by risk level: from aggressive purchases of little-known third-tier companies to ultra-conservative investments in US government debt securities. Naturally, everyone wants to get maximum profitability with a minimum level of risk, and just one of the strategies that provides this opportunity is arbitrage operations, which will be discussed today.

Arbitration (from the French “Arbitrage” - fair decision) - several logically related transactions aimed at making a profit from the difference in prices for the same or related assets at the same time in different markets (spatial arbitrage), or in the same the same market at different points in time (time arbitrage). Arbitration strategies are rightfully considered one of the lowest-risk and most stable strategies in the financial markets; the vast majority of the world's financial corporations and banks do not hesitate to engage in them.

So, let’s try to demonstrate an arbitrage transaction using a practical example: as you know, in Russia there are several stock exchange platforms for trading shares: MICEX and RTS-Standart. The same shares of OAO Gazprom are traded on both sites, and the price of these shares at the same time on different sites due to completely different factors can differ quite significantly. In this case, so-called market inefficiency is formed, which is won back by “arbitrageurs”, after which, usually, in a very short time, prices converge again around the same value. It is at the moment of divergence in quotes that you need to buy Gazprom on one exchange at a low price and sell it as a “short position” on another exchange at a high price. The resulting difference minus exchange and broker commissions will be the investor’s profit. At the same time, there is no market risk as such: since in the event of an even greater divergence of quotes on different exchanges, the investor can easily “overtake” all positions in shares to one exchange, resulting in the total position “resetting to zero”.

Naturally, in pure classical arbitration it is already quite difficult for a private investor to survive (and sometimes almost impossible), because fighting multibillion-dollar industry giants in milliseconds is not a promising matter at all, but here other types of arbitration come to the rescue, which we will discuss further.

Pair trading is a type of arbitrage in which transactions occur not between two identical financial instruments, but between a pair of assets with similar dynamics (for example, a pair from the same sector of the Lukoil - Gazprom market, or two different grades of oil "Brent - Light Sweet" ). In the case of pairs trading, the investor makes the assumption that the prices of assets that are similar in structure have similar dynamics, and if one asset in a short period of time breaks away from the other, then they will soon “converge” again. Pair arbitrage provides much wider opportunities, both in terms of choosing a variety of traded pairs, and in retrospect, choosing options for setting up the strategy. At the same time, the risks of the strategy increase significantly, because Tradable instruments, under certain circumstances, may not even agree on price for a very long period of time, so it is imperative to use loss-limiting “stop orders.”

Another type of arbitrage strategy is the arbitrage of the spot-futures pair - this is a game on the discrepancy between the prices of an instrument on the spot market and the futures price for the same instrument (for example, Gazprom on the MICEX - a futures contract on Gazprom on FORTS). Well, perhaps the most popular direction among private investors is arbitration of “synthetic instruments” against index futures. In this case, the “synthetic instrument” is formed by the trader from a basket of securities included in the index (and the weights for each security are selected individually), after which the same game begins to widen and narrow the spread between the futures on the index and the personally assembled “synthetic” index.

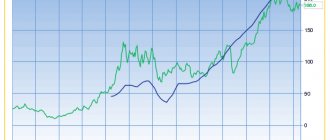

Professionals, including many hedge funds, actively use arbitrage strategies in the debt market, selling overheated securities and buying clearly undervalued securities of one issuer or one credit quality. In Russia, with the advent of futures on the OFZ basket, a good opportunity for arbitrage appeared in the public sector. I would like to consider in more detail the possibility of arbitrage between Russian shares traded on the MICEX and depositary receipts (ADRs) circulating in London for the same shares. As an illustrative example, let's take the shares of OJSC Gazprom on the one hand and the dollar ADRs of OJSC Gazprom on the other. The dynamics of these financial instruments for February 2012 can be seen in the figure below.

Obviously, the dynamics are almost identical, but small local deviations periodically occur, which provide the opportunity for statistical arbitrage. In order to plot the spread between Gazprom on the MICEX and depositary receipts on Gazprom on the LSE, we will make several assumptions: firstly, we will use the closing data of 10-minute candles, and secondly, we will synchronize the data over time in such a way as to include only those moments in time when both exchanges are open and operating normally, and thirdly, to convert the price of ADR into rubles (and initially they are denominated in dollars), we will use the exchange rate of the Central Bank of the Russian Federation on the previous trading day.

The resulting spread graph (i.e. the difference between Gazprom prices on different exchanges) can be seen in the picture below. We see that in February the spread freely “walked” by +/- 1.5%, while after some short time it certainly converged to the zero mark. Based on the dynamics of the spread spread, as well as the magnitude of transaction costs on both exchanges, we can conclude that it is advisable to begin arbitration in the event of price movements of 1% or more. In this case, in February we would have carried out at least 5 transactions and earned from this a “net” profit of at least 3% (we will include the remaining 2% as transaction costs for the purchase/sale of securities). This is 36% per annum, which, you see, is very good, given the virtually risk-free nature of arbitrage operations.

When working using this algorithm with real money, of course, it is still necessary to hedge the currency risk with a ruble/dollar futures contract, because after all, ADRs are denominated in foreign currency. But overall the strategy is quite working.

In conclusion, I would like to summarize some results and also outline the main advantages and disadvantages of arbitrage strategies. The most basic and important advantage that makes arbitration a “central” strategy among institutional investors is reliability and stability. We can fairly accurately predict future profitability based on current indicators, while there is virtually no risk of entering the unprofitable zone (which cannot be said about any other investment strategies).

Another important advantage is invariance to the market - i.e. It doesn’t matter at all whether the market is generally falling or growing, or maybe even in a narrow “sideways” zone; arbitrage will bring a stable “kopeck” in any market phase. Among the disadvantages, we note the high level of competition in this “clearing”: stable and risk-free profitability attracts a lot of players (primarily large ones), and periodically occurring price deviations necessary for arbitrage have a very specific monetary capacity, as a result of which the first arbitrageurs collect all the profitability , and the latter no longer gets anything. Technology comes to the fore: whoever is faster by a fraction of a second earns money. Plus, over time, markets become more efficient, which significantly reduces the profitability of arbitrage. So, if in 2008 the average profitability of the average arbitrage robot was at three-digit levels, then in 2011 it barely reached the level of 25% per annum.

Aponasevich Alexander

Is this popular in the cryptocurrency world?

Arbitrage has been around for centuries and is starting to gain popularity in cryptocurrency – but the opportunities may be short-lived.

Changes in supply and demand when cryptocurrency moves from one exchange to another can affect prices. Market volatility can mean that an arbitrage opportunity quickly disappears - but at the same time, unpredictable price changes often create new opportunities. With the right approach, you can theoretically earn a decent amount in a short time - and since there are more than two hundred exchanges, discrepancies in rates are inevitable.

Cryptocurrency trading - in miniature. Source: 2Bitcoin

Read on topic: Why 99 percent of traders cannot make money on the growth of Bitcoin and other cryptocurrencies?

There are also new approaches to cryptocurrency arbitrage that do not use exchanges. Paxful is a peer-to-peer Bitcoin exchange that directly connects buyers with sellers and allows you to buy BTC using over three hundred payment methods. It allows users in the US and Europe to be able to sell BTC to those in markets where it is more difficult or costly to buy - at a savings compared to the price on a local exchange.

The possibility of arbitrage on payment methods is also interesting. While it may be cheaper to purchase BTC via bank transfer, there is often a markup when using gift cards. Representatives of the platform claim that this gives the cryptocurrency community the opportunity to take advantage of this difference.

Legislative regulation of the activities of commissions

Exchange arbitration performs the functions of an arbitration court, and in its activities is guided by the requirements of the following regulatory legal acts:

- European (Geneva) Convention of 1961 “On Foreign Trade Arbitration”.

- Federal Law “On Arbitration Courts”, which came into force on July 24, 2002 No. 102-FZ.

- Federal Law “On International Commercial Arbitration”, introduced in 1993 on July 7 under No. 5338-1.

- The provisions of the arbitration commission, the relevant rules and the arbitration agreement between the parties to the proceedings.

The governing documents specified in the last paragraph are developed by exchange employees or external specialists. The regulations on the arbitration commission and the Rules of arbitration proceedings are approved by the supreme governing body of the exchange at a special meeting. An entry on this issue is made in the protocol and an appropriate decision is made.

Dispute resolution: mediation.

Mediation is an alternative method of resolving a dispute to the court. A mediator is an intermediary (an independent third party) who helps find a common language between the disputing parties through negotiations. Mediator services are subject to payment. As a rule, the party that initiates the appointment of a mediator pays. The parties may also agree to share these costs equally. It is worth noting that the costs of a mediator cannot be attributed to the losing party, as is possible when considering a dispute in the Arbitration Commission or in an economic court. To begin negotiations, the parties must select a mediator and enter into an agreement on the use of mediation.

From practice, it can be stated that the parties choose this method of resolving the dispute already in the process of considering the dispute in the Arbitration Commission or in the economic court, since before the trial it is often difficult for the parties to agree on something. When it comes to the use of mediation, in order to avoid wasting expenses on a mediator and not wasting time, the parties can come to a mutually beneficial agreement themselves, and in order to secure it, they can choose a mediator and sign a mediation agreement. In case of non-fulfillment of the mediation agreement, it is subject to compulsory execution in accordance with economic procedural legislation. At the current time, this method is not yet as popular as a reconciliation agreement or a settlement agreement, which is concluded during the dispute process in the economic court or the Arbitration Commission.

Is resolving stock exchange disputes your current problem? We will help resolve a dispute that arose during exchange trading of goods, represent your interests in the Arbitration Commission, prepare documents for the court and support the execution of the decision. Contact us!

Contact information for the service: Andrey Nikolaevich Skobey, licensed lawyer, you can contact him by phone (+37529 1102388) or by email ( [email protected] ).