How Putin controls Novatek. Who actually owns the company?

NOVATEK is the second largest gas production company in Russia. In first place, of course, is Gazprom.

Formally, NOVATEK is a private structure. However, not all so simple. What tasks does NOVATEK perform, and who owns it, we will analyze further.

#Russia #economy #energy #gas #Novatek

NOVATEK became known to a wide audience only a few years ago. The company's recognition is inextricably linked with the development of the LNG industry in Russia. NOVATEK is the first Russian company to carry out large-scale exports of LNG.

To date, NOVATEK is the fourth energy producing company in Russia in terms of capitalization:

Gazprom - 4.69 trillion. Rubles

Rosneft - 3.87 trillion. Rubles

Lukoil - 3.68 trillion. Rubles

Novatek - 3.17 trillion. Rubles

For a long time, the dominant rule in Russia was that only Gazprom could export gas. However, this only applied to pipeline exports. If we talk about LNG, NOVATEK received a similar privilege.

However, what is this connected with? The LNG market is highly competitive. NOVATEK's task is to bring Russian gas in the form of LNG to the markets of Southeast Asia (primarily India, South Korea, Vietnam and partly China). Roughly speaking, where Gazprom pipes cannot reach. The main competitors are the USA and Qatar. Accordingly, Russian LNG must be removed from possible sanctions, which are much more difficult to impose on a private company. Moreover, if the shareholders include a global company (the French Total, but more on that later), then it is almost impossible to impose sanctions.

However, on the other hand, the state cannot help but control the largest exporter of its LNG. Therefore, let's look at the shareholder structure. So, NOVATEK has this:

ADRs (free shares that anyone can buy) - 29%

Volga Group LLC - 23.3%

Total — 16.2%

SWGI Growth Fund (Cyprus) Limited - 14.3%

Gazprom capital - 9.9%

Levit LLC - 7.3%

On the first point, I think there are no questions. Shares rotate freely on the stock exchange.

Then. It is generally accepted that the main leader of the company is Leonid Mikhelson. Indeed, Mikhelson is the chairman of the board and the “face” of the company. SWGI Growth Fund (Cyprus) Limited and Levit LLC are affiliated with it. In total, this amounts to 21.6% of NOVATEK shares.

However, two other legal entities are much more important to us. These are Volga Group LLC and Gazprom Capital. ./

Volga Group LLC (23.3% of shares) belongs to Gennady Timchenko. This person performs a much more important function. Namely, it “looks after” NOVATEK. Timchenko has known Vladimir Putin for a long time. And the President trusts him. Timchenko is the proven “old guard” of the President. In fact, all key issues regarding NOVATEK go through Timchenko.

Gazprom capital (no need to explain what belongs to Gazprom) together with Volga Group control 33.2% of NOVATEK shares. So they have a blocking package. No decision that goes against public policy can be made without these two legal entities. I would like to note right away that Gazprom alone cannot even have a blocking stake, since then the company will be considered affiliated with the state and sanctions can be imposed against it.

In French Total there is hardly any need to explain either. This is a purely commercial share. Total does not even have a blocking stake and cannot influence strategic decisions. The Total function is to help you evade sanctions.

Thus, despite the formally private status of NOVATEK, the company is controlled by the state. Vladimir Putin was able to build a configuration in which the company would competently emerge from sanctions and, at the same time, work in the interests of the state, developing the LNG industry at a rapid pace.

Don't forget to like :)

Subscribe so you don't miss anything!

Read more ➤

Analysis of the issuer. Novatek

Novatek is the largest independent public gas producer in Russia.

The company is engaged in the exploration, production, processing and sale of natural gas and liquid hydrocarbons. Novatek is third in the world among public companies in terms of proven hydrocarbon reserves, which at the end of 2021 amounted to 15.1 billion barrels of oil equivalent (boe) according to SEC standards.

Compared to 2021, inventories increased by 12.8%.

The replacement rate was 435%. The reserves coverage indicator increased to 29 years. Thanks to new acquisitions of fields and licenses in 2018, reserves increased by another 0.45 billion boe. according to Russian standards. The company's direct production costs remain among the lowest in the world - $0.8 per boe. (1 boe ≈ 155 cubic meters of natural gas) The company's production is concentrated mainly in the Yamalo-Nenets Autonomous Okrug on the Yamal and Gydan Peninsulas. The asset includes 45 fields and license areas. All fields are located close to transport and production infrastructure, including in the area of the Unified Gas Supply System (UGSS), which increases the efficiency of the enterprise.

Strategy

At the end of last year, the company presented a new strategy until 2030, called “Transformation into a global gas company.” The new strategy was a consequence of the entry into the world market of liquefied natural gas (LNG). This market forms the basis of the company’s future business model, so a few words will be said below about its condition and prospects.

As competitive advantages, we can note the mutual proximity of deposits, processing capacities and an established sales infrastructure. In addition, Novatek patented its own gas liquefaction technology, Arctic Cascade. Low temperatures in the far north help increase the efficiency of the liquefaction process.

At the end of 2021, the 1st stage of Yamal LNG was launched - an integrated complex for the production, liquefaction, and transportation of LNG with a capacity of 5.5 million tons per year. The total capacity with 4 lines will be 17.4 million tons/year . The launch of the last Yamal LNG line, taking into account the new liquefaction technology, was planned in the fourth quarter of 2019, but it is quite possible that it will be done a little earlier. Each line could generate $1-1.2 billion in additional operating profit stream.

Based on the Yuzhno-Tambeyskoye field project, at the end of last year, proven reserves amounted to 683 billion cubic meters. m of gas and 21 million tons of liquid hydrocarbons (LHC).

As of March 31, the project was 92.5% complete. Long-term contracts have been concluded for 95% of the LNG from the project. Regular deliveries of LNG began this spring. The first products were delivered to the ports of Spain, India, and China.

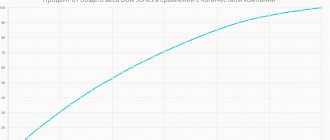

Below is the company's business plan for the rate at which it will reach its design capacity. Using this graph, you can evaluate the increase in the issuer's production indicators.

It should also be noted that Yamal LNG should generate $62 billion in operating cash flow until 2030. On average, you can count on $2.5 billion per year, taking into account that 20% of the project belongs to Total, 20% to CNPC and 9.9% Silk Road Foundation. Operating costs for the project will be $400-450 million per year . The company says that they will largely cover it by selling condensate.

To transport gas, the company uses the built infrastructure of the Sabetta port and new Arc7 class gas carriers, which are capable of transporting raw materials without icebreaking during summer navigation along the Northern Sea Route (NSR), both in the European and Asian directions.

At the same time, several transportation options are being considered, in particular, the delivery of raw materials to a transshipment point in Kamchatka (Asian direction) and in Belgium (European direction). Further reloading into ice-free gas carriers should significantly reduce the cost of the entire chain of transportation of products to Asian and European consumers. The company's calculations are shown below.

The commissioning of a transshipment point in Kamchatka is planned for 2022-2023. (share in the project can be sold). In addition, investments are also planned in another LNG production and transhipment terminal in Vysotsk on the Baltic Sea, as well as the construction of Arctic LNG-2, which will use the Yamal LNG transport infrastructure. These projects will be discussed below.

Along with the new strategy, the company rebranded and introduced a new logo. In connection with global ambitions, it was decided to replace the old distinctive sign in the shape of the letter “H” with a bright and modern logo, which, according to management, conveys two physical states of methane. The blue color symbolizes the gas, the red color symbolizes the energy and heat it provides. The new logo symbolizes the slogan “Transformation into a global gas play.”

LNG market prospects

The company's future and long-term prospects are directly related to the LNG market, which is undoubtedly expanding, displacing other types of fuel and “dirtier” energy sources. Moreover, Asia, and in particular China, promises to become the main player providing demand. Due to the gradual abandonment of coal and the active transition to more environmentally friendly fuels, current expectations of potential demand growth from China may be underestimated.

Data from global energy agencies and relevant committees indicate that gas is the only fossil fuel whose share in global consumption will grow. This is due to the relative cheapness, environmental friendliness and other parameters. We have a separate large review on the future of the gas market in several parts. The main contribution to demand growth will come from electricity generation, transport (gas motor fuel) and industry.

And these are not just forecasts, but an already established trend, especially considering China’s environmental policy. Chinese officials plan to increase gas consumption by more than 50% by 2021 - up to 320-360 billion cubic meters per year. Demand will grow by almost as much as Japan, Asia's second-largest importer, currently consumes annually. And by 2030, consumption is planned to increase to 480 billion cubic meters. LNG imports are growing exponentially every year.

Thus, the company operates in an expanding and promising market. The Yamal LNG and Arctic LNG-2 projects will allow us to take a significant share of growing Asian demand. At the same time, competitive advantages in the form of low costs for production and transportation along the Northern Sea Route should ensure sustainable growth in market share, production and financial indicators.

Separately, it is worth noting the prospects for small-scale LNG in the domestic market. The company estimates the potential for growth in consumption of LNG and CNG as motor fuel to be more than 20 billion cubic meters by 2030. And against the backdrop of a tax maneuver in the oil sector, the demand for gas motor fuel may greatly exceed forecasts due to the rapid rise in prices for traditional fuel. There will also be demand for gasification in areas remote from the gas infrastructure.

Investment program

In order to supply the growing market with gas, Novatek is implementing a large-scale investment program. The first project was Yamal LNG, the main criteria of which were described above. At the moment, we can talk about almost completed construction, so we will focus on future projects.

Launch of the North Russian group of fields

To compensate for the depletion of existing fields, Novatek is developing new production centers near the UGSS, which should ensure a stable position in the domestic market. At the end of last year, gas reserves of the North Russian group of fields amounted to 190 billion cubic meters, liquid hydrocarbon reserves - 29 million tons. There is a significant potential increase in reserves until 2030. Total capital costs for projects in the UGSS Zone are estimated at 700-780 billion rubles. until 2030

Arctic LNG-2

Of the upcoming implementation of LNG projects, Arctic LNG-2 should be noted first. It provides for three stages of gas liquefaction with a capacity of 6.6 million tons per year each.

The base for the project will be the Utrenneye field with gas reserves of 1,582 billion cubic meters and 65 million tons of liquid hydrocarbons, according to the Russian classification.

Design studies should be completed at the end of 2021. The first assembly of blocks for the liquefaction line is planned for 2021 (TsSKMS). The launch of the first stage is planned for 2022-2023. Launch of II and III in 2024 and 2025. respectively.

Meanwhile, in May 2021, it became known that the French Total had entered the project with an initial share of 10% and an option for another 5%. The project cost is $25.5 billion.

Novatek also does not rule out selling shares to other partners. In particular, Saudi Aramco is showing interest, with which a memorandum was signed on the development of international cooperation and joint investments in the gas industry.

LNG transshipment in Kamchatka

The project is designed to significantly reduce the cost of transporting LNG to Asia. Design surveys are planned to be completed in 2021. Commissioning in 2022-2023.

LNG terminal Vysotsk

In mid-2021, Novatek bought 51% in the Cryogas-Vysotsk project on the Baltic Sea. The remaining 49% remained with Gazprombank. This is an LNG production plant with a capacity of 660 thousand tons per year. There is also a port infrastructure. It is planned to build the 2nd stage with a capacity of 660-800 thousand tons per year. The launch of the first stage is scheduled for 2021 . The second line could be built by 2021.

Deepening processing in Ust-Luga

Now the complex in Ust-Luga processes stable gas condensate, which is supplied by rail from the Purovsky Plant and receives 14% of Marine Fuel. By deepening the processing, it can be used to obtain kerosene, light and heavy naphtha, which will increase the profitability of the project. All products of the complex are exported.

Thus, Novatek has quite a lot of projects in implementation or preparation. But most of them are aimed at entering and strengthening positions in the growing LNG market.

It is also worth noting serious tax incentives for the Yamal LNG and Arctic LNG-2 projects, namely:

— Zero mineral extraction tax rate on gas and condensate;

— Reduced income tax rate;

— No property tax;

— Zero export duty on LNG and condensate.

Total capital expenditures for the LNG sector until 2030 are planned at RUB 2.5-2.8 trillion. The implementation schedule for the main projects is given below.

Production figures

To begin with, it is worth noting the long-term stable dynamics of Novatek's main operating results. Total hydrocarbon production from 2011 to 2021 increased 1.4 times, with an average annual rate of 7.2%.

True, in 2021, the production indicators of the Novatek group showed a decrease. Natural gas production decreased by 6.3% YoY, to 61.4 billion cubic meters. Natural gas provides 81% of all production indicators of the company.

Production of liquid hydrocarbons decreased by 5.4% year-on-year, to 11.8 million tons. Approximately 40% of them are used for oil, the rest is condensate. About 70% of the oil produced goes to the domestic market.

The deterioration in results affected stock performance in the first half of 2021 and was associated with a natural decline in production from mature fields.

It is worth noting that production dynamics began to recover in the fourth quarter of 2021 thanks to the start of operation of the first stage of Yamal LNG (Yuzhno-Tambeyskoye field). Gas production in the first half of the year increased by 3.2% y/y.

Also in the future, support will be provided by an increase in production through the purchase of gas assets from Eurochem (Severneft-Urengoy) and gas assets of ALROSA.

We also note the prospects of a joint venture with Gazprom Neft - Arcticgas. The deposit at the heart of this project is already being developed. From 2021, gas production levels are expected to increase. From 2021, increasing the production of liquid hydrocarbons. Starting this year, the company is waiting for the first dividends from the joint venture.

Separately, it is worth mentioning the development of fields of the North Russian group. This investment project was discussed above. The start of production is scheduled for 2021. Novatek management predicts that projects in the UGSS zone by 2030 should produce about 820 billion cubic meters of gas, 107 million tons of condensate and 75 million tons of oil.

Together with the capacity of the Yamal LNG project, we can expect a serious increase in production indicators over the next few quarters.

Financial indicators

The company's long-term financial results are growing even faster than production indicators. EBITDA grew 2.8 times from 2011 to 2021, at an average annual rate of 23.3%. This is partly due to the devaluation of the ruble in 2014-2015.

With the first deliveries of LNG at the end of last year, revenue began to grow. Strictly speaking, year-on-year growth in the indicator began in the third quarter. In the first quarter of this year, the growth in the cost of liquid liquids also provided support.

Along with the recovery of operating indicators, EBITDA began to grow in the fourth quarter of 2017. It is expected that as the next stages of Yamal LNG are commissioned, operating profit growth will continue.

If we take the spot price of LNG in Asia, which is currently about $10 per million MBTU, we can assume that in 2018 Novatek’s operating profit should increase by more than 70 billion rubles. at the current ruble exchange rate. At the end of 2021, approximately another 175 billion rubles. That is, operating profit at the end of 2021 may double if the ruble exchange rate remains close to current values.

At the same time, based on an EBITDA margin of 40%, by the end of 2021 this figure could grow to more than 310 billion rubles, compared to 198.3 billion in 2021.

Net profit in annual terms has been declining since the beginning of 2017 due to deteriorating production performance. The company had to purchase more gas and liquid hydrocarbons to load processing capacity and fulfill contractual obligations. But despite the growth in revenue, as of the first quarter there is no similar reaction in profits. Actual profit was reduced by non-cash exchange differences on loans from Novatek and the joint venture in foreign currency. The ruble exchange rate weakened noticeably in the second quarter.

Despite high capex on projects, ] has positive free cash flow (FCF)[/anchor]. This is achieved, in particular, by attracting strategic foreign investors and a competent borrowing policy. FCF will also benefit from increased LNG supplies in the near future.

The project to deepen processing at the Ust-Luga facility should ultimately have a positive impact on financial performance.

Management gave forecasts for some indicators for 2021. Based on the reporting for the first quarter, the company exceeds indicators in a number of positions, including the net profit margin was equal to 26%, the EBITDA margin was 43%.

Debt load

Novatek's debt load is at a quite comfortable level. At the end of the first quarter, Net Debt/EBITDA was at the level of 0.4x. The company paid off debts throughout 2016-2017. However, taking into account new projects, in particular Arctic LNG-2, an increase in the debt burden cannot be ruled out. How much will depend on what part of the project will be sold to strategic investors. In any case, taking into account the growth in operating profit as new Yamal LNG capacities are commissioned, the issuer can afford to seriously increase its debt without deteriorating its profile.

At the end of the first quarter of 2021, the issuer had $750 million and 50 million euros in cash on its accounts. A credit line has also been opened with Russian banks for 167.5 billion rubles. A debt repayment schedule should not cause financial hardship. The debt portfolio includes both dollar Eurobonds and loans from the Chinese Silk Road Fund.

Dividends and buybacks

The dividend history is impressive , with long annual growth averaging 28% . The absolute growth, taking into account payments for 2021, is 16.6 times.

The dividend policy assumes the payment of at least 30% of Novatek's net profit under IFRS (adjusted for non-recurring gains (losses)). Another plus is that Novatek pays dividends twice a year. At the same time, the dividend yield over this period of time is not much higher than 1%, although the dynamics of the shares are impressively positive. This suggests that the company is growing rapidly and investors are pricing the stock into current high cash flow and future high dividends.

It is also worth noting the share repurchase program and GDRs, which the issuer has been implementing since July 2012 and extends every year. The buyout volume is $600 million per year. The program has been extended until June 7, 2021.

The redemption is carried out at market prices on the Moscow and London stock exchanges. At the beginning of May 2021, Novatek Equity (Cyprus) Limited purchased 22,691,120 shares and depositary receipts. This is approximately 0.74% of the company's total authorized capital.

Shares and capital structure

The dynamics of the company's shares speak for themselves. After the 2008 crisis, the security has been in a long-term growing trend. It is possible that quotes may correct in the short term, but given the prospects for the LNG market and the commissioning of new projects in 2018-2025, there is reason to expect the current trend to continue in the medium and long term. Dropping papers into the area costs 800 rubles. or below, in our opinion, may be interesting for purchases.

In 2021, Novatek shares were included in the FTSE4Good Emerging Index, and also became a member of the Vigeo Eiris Best Emerging Markets Performers rating of 100 best companies in emerging markets. Novatek's depositary receipts are included in the MSCI Russia and MSCI Russia 10/40 index.

The stock is currently trading at very high multiples. Based on the last 12 months, per share they gave more than 20 annual earnings (P/E LTM). However, high multipliers reflect the rapid pace of development of the company and the level of the issuer's attitude towards minority shareholders. And the low dividend attractiveness is partially compensated by the repurchase of securities at market prices.

Based on the Reuters consensus forecast, over the next 12 months. experts expect an almost doubling of profits. EBITDA could grow by more than 12%. The multiplier values are significantly higher than the industry average, which is not surprising for a developing business in a promising market. However, in the short term the stock may still be overvalued and we allow for the possibility of local corrections.

conclusions

Strengths

1. Promising market. Global gas consumption is growing, and new interesting niches are opening up, in particular the LNG market and the marine fuel market.

2. Low cost of gas production and liquefaction. Proximity of the fields to the UGSS.

3. Growth in production indicators and cash flow in the short and medium term as new fields are commissioned and Yamal LNG lines are launched.

4. Long-term growth potential from the Arctic LNG-2 project. Reduced construction costs (compared to Yamal LNG). The introduction of a transshipment point in Kamchatka will significantly increase the competitive advantage and reduce costs.

5. Tax benefits. There is no mineral extraction tax or export duties on LNG.

6. Large foreign shareholders and project lenders.

7. Flexible share repurchase program.

8. The securities occupy leading positions in the MSCI Russia index.

9. Prospective dividend policy.

10. A positive trend in the development of the domestic gas market, in particular liquefied and compressed gas. The prospect of growth in the gas motor fuel market, especially in light of the tax maneuver in the oil sector, which may cause an increase in prices for traditional fuel.

11. Low debt load.

12. The prospect of gaining access to pipeline gas exports.

13. Novatek is increasingly becoming an exporter, whose shares are protected to a certain extent from ruble devaluation.

Weak sides

1. Competition with American LNG. On the one hand, this may put pressure on fuel prices. On the other hand, the risks of sanctions are growing.

2. Still a high investment program.

3. Low, unattractive dividends in the short term.

4. High multipliers.

Thus, Novatek operates in a very promising market, in the developing direction of international LNG supplies. There are serious growth points in the domestic market: small-scale LNG and gas motor fuel.

The company has shown good financial results over the past few years. Although in 2016-2017. Novatek faced a decline in production indicators due to natural reasons; the implementation of the Yamal LNG project promises an increase in production and cash flow in the very near future. Arctic LNG-2 and the commissioning of a number of new fields will support revenues in the long term.

High multiples and rapid stock performance in the short term may cause caution among investors who would like to buy shares at current prices. But it is worth understanding that the expected increase in production and financial indicators will have a positive impact on the attitude of market participants towards securities in the future. A low and controlled debt burden, coupled with a promising dividend history and share repurchase program, provides a good basis for medium- and long-term investments.

Short term : neutral view

Medium term , long term : positive outlook

Konstantin Karpov

BCS Broker

Dividends on Novatek shares in 2021 - size and register closing date

Home → Dividends→ Novatek shares - forecast, payment history

A table with the complete history of Novatek's dividends, indicating the amount of payment, the date of closure of the register and the forecast:

| Payment, rub. | Registry closing date | Last day of purchase |

| 22.06 (forecast) | October 12, 2021 | 08.10.2021 |

| 23.74 | May 7, 2021 | 05.05.2021 |

| 11.82 | October 12, 2020 | 08.10.2020 |

| 18.1 | May 8, 2020 | 06.05.2020 |

| 14.23 | October 10, 2019 | 08.10.2019 |

| 16.81 | May 6, 2019 | 02.05.2019 |

| 9.25 | October 10, 2018 | 08.10.2018 |

| 8 | May 3, 2018 | 01.05.2018 |

| 6.95 | October 10, 2017 | 06.10.2017 |

| 7 | May 2, 2017 | 28.04.2017 |

| 6.9 | October 11, 2016 | 07.10.2016 |

| 6.9 | May 4, 2016 | 02.05.2016 |

| 6.6 | October 6, 2015 | 02.10.2015 |

| 5.2 | May 5, 2015 | 01.05.2015 |

| 5.1 | October 27, 2014 | 24.10.2014 |

| 4.49 | April 29, 2014 | 25.04.2014 |

| 3.4 | September 16, 2013 | 16.09.2013 |

| 3.86 | March 21, 2013 | 21.03.2013 |

| 3 | September 10, 2012 | 10.09.2012 |

| 3.5 | March 23, 2012 | 23.03.2012 |

| 2.5 | September 8, 2011 | 08.09.2011 |

| 2.5 | March 22, 2011 | 22.03.2011 |

| 1.5 | September 9, 2010 | 09.09.2010 |

| 1.75 | March 22, 2010 | 22.03.2010 |

| 1 | September 9, 2009 | 09.09.2009 |

| 1.52 | April 20, 2009 | 20.04.2009 |

| 1 | July 24, 2008 | 24.07.2008 |

| 1.52 | April 10, 2008 | 10.04.2008 |

| 0.83 | September 3, 2007 | 03.09.2007 |

| 1.1 | April 5, 2007 | 05.04.2007 |

| 0.00055 | July 31, 2006 | 31.07.2006 |

| 0.523 | April 21, 2006 | 21.04.2006 |

| 0.377 | October 31, 2005 | 31.10.2005 |

| 0.256 | April 25, 2005 | 25.04.2005 |

| 0.6428 | October 11, 2004 | 11.10.2004 |

| 0.2515 | April 25, 2004 | 25.04.2004 |

*Note 1: The Moscow Exchange operates on the T+2 trading system. This means that settlements for buying and selling shares occur within 2 business days. Therefore, to be included in the register of shareholders and receive dividends, you must be a shareholder 2 days before the cutoff.

*Note 2: Exact payout date varies by broker and issuer. The predicted nearest date for receipt of dividends to the brokerage account for Novatek JSC: October 25, 2021.

Total dividends of Novatek shares by year and changes in their size compared to the previous year:

| Year | Amount for the year, rub. | Change, % |

| 2021 | 45.8 (forecast) | +53.07% |

| 2020 | 29.92 | -3.61% |

| 2019 | 31.04 | +79.94% |

| 2018 | 17.25 | +23.66% |

| 2017 | 13.95 | +1.09% |

| 2016 | 13.8 | +16.95% |

| 2015 | 11.8 | +23.04% |

| 2014 | 9.59 | +32.09% |

| 2013 | 7.26 | +11.69% |

| 2012 | 6.5 | +30% |

| 2011 | 5 | +53.85% |

| 2010 | 3.25 | +28.97% |

| 2009 | 2.52 | 0% |

| 2008 | 2.52 | +30.57% |

| 2007 | 1.93 | +268.64% |

| 2006 | 0.52355 | -17.29% |

| 2005 | 0.633 | -29.22% |

| 2004 | 0.8943 | n/a |

| Total = 204.18085 |

The amount of dividends paid by Novatek for the entire period is 204.18085 rubles.

Average amount for 3 years: 35.59 rubles, for 5 years: 27.59 rubles.

DSI indicator: 0.93.

You can buy Novatek shares with minimal commissions from stock brokers: Finam and BCS. Free deposits and withdrawals. Online registration.

Dividend policy:

50% of adjusted net profit under IFRS.

Paid twice a year.

Brief information about the issuer PJSC NOVATEK JSC

| Sector | Oil Gas |

| Issuer's full name | PJSC NOVATEK JSC |

| Issuer's name is short | Novatek JSC |

| Ticker on the stock exchange | NVTK |

| Number of shares in lot | 1 |

| Number of shares | 3 036 306 000 |

| TIN | 6316030000 |

| Free float, % | 21 |

Other companies from the Oil/Gas sector

| # | Company | Div. profitability for the year, % | The nearest registry closing date | Buy before |

| 1. | Surgnfgz-p | 16,84% | 20.07.2021 | 16.07.2021 |

| 2. | LUKOIL | 9,32% | 05.07.2021 | 01.07.2021 |

| 3. | Gazprneft | 7,64% | 25.06.2021 | 23.06.2021 |

| 4. | SaratNPZ-p | 7,46% | 09.06.2021 | 07.06.2021 |

| 5. | Tatnft 3ap | 6,34% | 09.07.2021 | 07.07.2021 |

Calendar with upcoming and past dividend payments

| Immediate | Past | ||||

| Company Sector | Size, rub. | Registry closing date | Company Sector | Size, rub. | Registry closing date |

| RusAqua JSC Foodstuff | 5 | 27.05.2021 | MDMG-gdr Miscellaneous | 19 ✓ | 25.05.2021 |

| FGC UES JSC Energy | 0.016 | 29.05.2021 | TransK JSC Logistics | 403.88 ✓ | 24.05.2021 |

| SevSt-ao Metals and mining | 46.77 | 01.06.2021 | M.video Retail trade | 38 ✓ | 18.05.2021 |

| Tattel. JSC Telecoms | 0.0393 | 01.06.2021 | PIK JSC Construction | 22.51 ✓ | 17.05.2021 |

| SevSt-ao Metals and mining | 36.27 | 01.06.2021 | PIK JSC Construction | 22.92 ✓ | 17.05.2021 |

| GMKNorNik Metals and mining | 1021.2 | 01.06.2021 | Moscow Exchange Finance and Banking | 9.45 ✓ | 14.05.2021 |

| MOESK Energy | 0.0493 | 01.06.2021 | Sberbank Finance and Banking | 18.7 ✓ | 12.05.2021 |

View full calendar for 2021 »

7 Best Dividend Stocks for 2021

| # | Company | Sector | Dividend yield for the year, % | The nearest registry closing date | Buy before |

| 1. | Surgnfgz-p | Oil Gas | 16,84% | 20.07.2021 | 16.07.2021 |

| 2. | iMMTSB JSC | Miscellaneous | 15,24% | 09.06.2021 | 07.06.2021 |

| 3. | Unipro JSC | Energy | 15,08% | 22.06.2021 | 18.06.2021 |

| 4. | ALROSA JSC | Metals and mining | 14,99% | 04.07.2021 | 30.06.2021 |

| 5. | NLMK JSC | Metals and mining | 14,91% | 09.06.2021 | 07.06.2021 |

| 6. | Rusagro | Food | 11,85% | 18.09.2021 | 15.09.2021 |

| 7. | MMK | Metals and mining | 11,80% | 17.06.2021 | 15.06.2021 |

View the full company rating for 2021 »

Interesting read:

- How to purchase shares for an individual;

- How to enter the stock market;

- Investing in securities is a simple matter of complexity;

- How to create an investment portfolio from scratch;

- How to start living on dividends from scratch;

- How to buy Sberbank shares;

- What is the average return of stocks;

- Investing in Stocks - A Complete Guide;

← Return to main catalog