Holders of Mechel preferred shares are waiting for October. In August, the company did not pay dividends on preferred shares, as it is under a moratorium on bankruptcy, which ends in October. In the meantime, the company is hastily trying to solve financial problems: for example, Mechel took advantage of state support and took out a loan of five billion rubles in August as part of assistance to systemically important measures, becoming the first in its sector to decide on this. The loan will be used to replenish working capital, but will further increase the company’s debt burden, which it simply does not have time to digest. In April of this year, a debt restructuring agreement was already signed with Gazprombank and VTB, extending the repayment period of Mechel’s debts for seven years with the possibility of extending payments for another three years.

Mechel’s huge (427 billion rubles at the end of 2021) debt was formed mainly in the mid-2000s. Such group assets as Izhstal, Moscow Coke and Gas Plant, Yuzhno-Kuzbasskaya State District Power Plant, Kuzbassenergosbyt, Bratsk Ferroalloy Plant and a number of other expensive purchases were purchased with borrowed money. Moreover, the loans were taken in foreign currency. Let us recall that in 2004, Mechel entered the New York Stock Exchange; over the next few years, the company actively increased its production of coal and iron ore through the modernization of assets, and also increased the share of more expensive products in its output. But then the commodity markets went down, and the ruble followed suit. It became increasingly difficult to service foreign currency debts.

In recent years, Mechel's debts have been declining, but not fast enough. “Despite the sale of the Elga field and a decrease in the company’s net debt by 22 percent, the ratio of net debt to EBITDA remains at a high level (6.9 at the end of the first half of 2020 versus 7.5 at the end of 2021). For comparison: the similar indicator for other Russian steelmakers under our coverage ranges from 0.16 to 1.7,” explains the depth of the “debt quarry” in which Mechel is located, BCS Global Markets analyst Artem Bagdasaryan .

Why did the mining and metallurgical giant, one of the largest producers of coking coal (controls 25% of enrichment capacity in Russia), find itself in such a deplorable state from which there is no way out? According to the analyst, the issue is the collapse in prices for coking coal, which is a significant component of the company's revenue and EBITDA. The high debt burden, in turn, leads to a significant decrease in the cash flow produced by Mechel and insufficient investment in development. And large-scale projects like the Elginskoye field, which in theory can help get out of debt, in practice only drag the group into a debt hole.

If dividends for 2021 are not paid, the stake of Mechel's main shareholder Igor Zyuzin will become less than the controlling one

NAIL FATTAHOV/TASS

As a result, the company and its owner Igor Zyuzin (net worth in 2010 - $6.4 billion, in 2019 - less than $500 million according to Forbes; together with his family, he owns a 50.2 percent stake in Mechel and is the chairman of the board directors) are now in a very precarious position. The moratorium on bankruptcy, on the one hand, protects it and gives it time, on the other, does not allow it to pay dividends for 2021. And if dividends on preferred shares are not paid, then they will receive voting rights.

Mechel's authorized capital is divided into 416.27 million ordinary and 138.75 million preferred shares. The stake of Igor Zyuzin and his family is even slightly larger than the controlling stake, however, if the preferred shares become common, this controlling stake will be diluted.

“In the event of non-payment of preferred shares, the securities will indeed become voting until the accumulated dividends are paid to shareholders in full. The structure of voting shares in this case will change as follows: the share of Igor Zyuzin and his family (who do not own preferred shares) will decrease from 50.2 to 42 percent, the remainder will belong to minority shareholders. We can say that control will remain with the chairman of the board of directors,” Otkritie Management Company analyst Irina Prokhorova . The possibility of such an event is not that great, and it is definitely not a disaster. But Igor Zyuzin did not fight so much for Mechel in order to lose control.

Dividend policy

Accepted 01/20/2016. Principles of dividend policy:

- compliance with Russian legislation;

- balancing the interests of Mechel and the interests of shareholders;

- high standards of corporate governance;

- increase in dividends with net profit growth;

- transparency of payments;

- increasing the investment attractiveness of the company.

The basis for calculating Mechel's dividends is net profit. The share allocated for payments on ordinary shares is not fixed in the Charter. 20% of net profit is distributed among preference holders. If payments per JSC are greater than per AP, then dividends on preference shares should be increased.

The issue of the appropriateness of payments based on the results of the reporting period is considered by the Investment and Strategic Planning Committee of the Board of Directors.

Based on his recommendations, the board of directors considers the CEO's proposals regarding the direction of distribution of net profit and sets the share allocated for payments to shareholders.

This takes into account:

- net profit;

- Mechel's need for capital;

- external macroeconomic indicators and internal negative changes that may worsen operating performance.

At the AGM, holders of voting shares may disagree with the recommendations of the board of directors or refuse payments altogether.

What affects the stock price

The price of shares is influenced by fundamental analysis indicators, sales results, insider information, forecasts about the company, and the situation in the Russian and global economy.

Company prospects

Development prospects are largely related to resolving the issue of overdue debt to banks. Without taking into account penalties at the end of 2021, this amount was almost 468 billion rubles. Over the year, the debt was reduced by 0.8 billion rubles. That is, it actually remained at the same level, despite a successful financial year for the company.

Analytics and forecast for the security

From the point of view of technical analysis, let's look at the daily chart of Mechel. Source - TradingView.

At the end of September 2021, there were purchases on good volumes for two days in a row and there was hope for a break in the downward trend with the drawing of highs higher than the summer ones. But it didn't happen. Cunning bears appreciated the gift and opened new short positions. Since then, quotes have been declining clearly along the resistance line (red line).

Today it is being tested once again. Opening even medium-term longs in anticipation of growth is quite risky. Until this trend from autumn 2021 is broken. Plus, a clear signal can be the drawing of at least two consecutive local maxima by the bulls. So far, the picture on the chart is from the “bears in the logging” series.

If the recommendations, from the point of view of technical analysis, are “sell,” then the consensus forecast of analysts from investment structures unanimously advocates the purchase of the company’s shares. The forecast price for spring 2021 is from 79 rubles. (CitigroupInvestment) up to 125 rub. (BCS).

Growth factors:

- Operating results for 2021 exceeded expectations. The profit amounted to more than 12 billion rubles.

- Write-off of accounts payable in the amount of 17.5 billion.

- Increase in payments as a percentage per share in preferred shares. Based on the results of 2021, the dividend amount per 1 security may exceed 20 rubles.

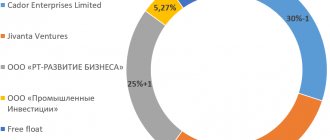

Alternative in this industry

Mechel's place relative to its competitors. From the company's presentation for 2021.

All company dividends for the last 10 years

Dividends on ordinary shares

| For what year | Period | Last day of purchase | Registry closing date | Size per share | Dividend yield | Closing share price | Payment date |

| 2011 | May 22, 2012 | May 22, 2012 | 12M 2011 | 8,06 ₽ | 3,99% | June 5, 2012 | |

| 2010 | April 20, 2011 | April 20, 2011 | 12M 2010 | 8,73 ₽ | 1,07% | May 4, 2011 | |

| 2009 | May 24, 2010 | May 24, 2010 | 12M 2009 | 1,09 ₽ | 0,16% | June 7, 2010 | |

| 2008 | June 4, 2009 | June 4, 2009 | 12M 2008 | 5,53 ₽ | 1,87% | June 18, 2009 | |

| 2007 | June 4, 2008 | June 4, 2008 | 12M 2007 | 26,38 ₽ | June 18, 2008 |

Dividends on preferred shares

| For what year | Period | Last day of purchase | Registry closing date | Size per share | Dividend yield | Closing share price | Payment date |

| 2019 | 15 Jul 2020 | 17 Jul 2020 | 12M 2019 | 3,48 ₽ | 4,1% | July 31, 2020 | |

| 2019 | 16 Jul 2019 | July 18, 2019 | 12M 2018 | 18,21 ₽ | 15,68% | 1 Aug 2019 | |

| 2018 | 16 Jul 2018 | July 18, 2018 | 12M 2017 | 16,66 ₽ | 12,27% | 1 Aug 2018 | |

| 2017 | July 7, 2017 | 11 Jul 2017 | 12M 2016 | 10,28 ₽ | 8,42% | July 25, 2017 | |

| 2016 | July 7, 2016 | 11 Jul 2016 | 12M 2015 | 0,05 ₽ | 0,14% | July 25, 2016 | |

| 2015 | 8 Jul 2015 | 11 Jul 2015 | 12M 2014 | 0,05 ₽ | 0,11% | July 24, 2015 | |

| 2014 | 9 Jul 2014 | 11 Jul 2014 | 12M 2013 | 0,05 ₽ | 0,2% | July 25, 2014 | |

| 2013 | May 17, 2013 | May 17, 2013 | 12M 2012 | 0,05 ₽ | 0,09% | May 31, 2013 | |

| 2012 | May 22, 2012 | May 22, 2012 | 12M 2011 | 31,28 ₽ | 16,09% | June 5, 2012 | |

| 2011 | April 20, 2011 | April 20, 2011 | 12M 2010 | 26,21 ₽ | May 4, 2011 | ||

| 2010 | May 24, 2010 | May 24, 2010 | 12M 2009 | 3,29 ₽ | June 7, 2010 | ||

| -1 | June 4, 2009 | June 4, 2009 | 12M 2008 | 50,55 ₽ | June 18, 2009 |

Exchange rate dynamics for all time

Ordinary shares:

Preference shares:

Consider the change in the price of the company's common shares since 2009.

In January, MTLR on the MICEX could be purchased for 120 rubles. Next is a three-year bullish trend with a pullback in the summer of 2010. Quotations showed a historical maximum share price of 984 rubles exactly three years after entering public trading - in January 2011. Having thoughtfully drawn a reversal figure, in March we decisively turned down.

The recoilless downhill movement continued until the fall of 2014 and the price reached 20 rubles per share. Loss 98%. Epicfail for investors who bought stocks at high levels. They lost almost everything. Then the shares, after standing at the same levels for a long time, corrected, reaching the level of 200 rubles. in November 2021. But that's all. With the beginning of 2021, the bears again took matters into their paws and reduced quotes for 2 years in a row.

Stock return

Mechel pays dividends once a year; there have never been interim dividends. Since 2013, payments have been made only on preferred shares.

The company has many problems that can lead to a worsening financial situation and reduced payments:

- risky business strategy;

- weak financial reporting;

- chronic underinvestment, lack of necessary modernization;

- high debt burden (16 times higher than capitalization on the Moscow Exchange);

- absolute dependence on state-owned creditor banks (they can file a bankruptcy claim, prohibit payments on preferred shares, begin alienating assets in their favor without compensation);

- projected decline in coal prices;

- a sharp increase in production costs (by 40%);

- lack of growth drivers;

- sale of the main Elga field, completion of production in Neryungri in 2029.

The roads we choose

The Elginskoye deposit is located in the southeast of Yakutia and is unique primarily for its reserves: 2.2 billion tons of high-quality coking coal. In addition, the deposit can be developed by open pit mining (such production is cheaper than mines). Production at the field began in August 2011, but its volumes were significantly limited by the capacity of the Elga-Ulak railway line. In fact, Mechel spent more than a decade building the infrastructure for exporting its extracted oil. The 321 km long railway he laid starts on the BAM, from the Ulak station of the Far Eastern Railway. One of the largest infrastructure projects launched by private business largely led to the fact that the field ultimately had to be sold under the hammer. In the region, the extremely difficult terrain, permafrost, and difficult natural conditions greatly complicate, and therefore increase the cost of, construction. In 2021, under pressure from financial obligations, Mechel had to sell 49% of the field. The buyer was Gazprombank, the package cost it 34.4 billion rubles. The sale of almost half of the field did not help Mechel much, and in April of this year the asset was finally sold to Albert Avdolyan and Sergei Adonyev for 89 billion rubles. An agreement previously signed between Gazprombank and A-Property allows the latter to collect 100% of Elga. In the meantime, A-Property is ready to invest 130 billion rubles right now to increase coal production.

The coal market again prevents Mechel from making money

But the complete abandonment of Elga did not help much - it did not seriously reduce Mechel’s debt burden. “Even before the sale of Elga, we believed that the company’s fundamental valuation was approaching zero. With the sale of the field, Mechel lost an asset that, at least theoretically, could help it reduce its debt burden in the future, so our view of the company remains unchanged,” Artem Bagdasaryan sums up the sale of the key asset.

Another capital-intensive project - a universal rail and beam mill (URBS) at the Chelyabinsk Metallurgical Plant (ChMK) - was launched in 2013. The complex, which produces hundred-meter rails and various styles of steel beams, for which about $715 million was spent, in theory looks very promising. This is the first production of long rails created in Russia from scratch using world-class technologies for rolling, hardening, straightening, finishing and quality control. A hundred-meter rail is manufactured in just 126 seconds. However, even here the railways failed. ChMK and Russian Railways agreed to supply rail products until 2030 in the amount of 400 thousand tons per year. But for the first few years, the new mill worked only for the construction sector - deliveries to Russian Railways did not begin. Then Russian Railways began purchasing, as did the Moscow Metro, which used ChMK rails in the construction of new lines. But it was not possible to reach the required supply volumes: from the moment of launch to the end of 2019, that is, in five years, the plant supplied about 1.3 million tons of rail products to Russian Railways, the metro, industrial enterprises and switch factories in Russia and abroad. While the total capacity of the mill is more than 1.1 million tons of products per year. Russian Railways still purchases most of its rails from Evraz.

If according to the results of the first half of 2019, ChMK received 3.4 billion rubles in profit, then this year the loss for the first half of the year has already amounted to 220 million. In addition, a scandal erupted around the plant with an electricity debt that reached two billion rubles, which went to court .

Things turned out really badly with the Donetsk Electrometallurgical Plant (DEMZ). Mechel acquired the plant from Alfa Bank in 2011 for $537 million. In 2012, the plant was shut down due to a drop in demand for products. Later, Mechel poured 18 billion rubles into DEMZ. And in July 2016, the plant came under the control of the DPR Ministry of Industry and Trade (to put it simply, it was nationalized).

How to buy shares and receive dividends

You can purchase Mechel securities only through a licensed broker with access to trading on MOEX by concluding an agreement. The broker will independently withhold 13% of the personal income tax; you will not have to fill out a declaration.

It is worth taking into account broker and exchange commissions, which reduce the final profitability. The company does not practice direct plans for selling shares. Purchasing securities from individuals and legal entities is associated with great difficulties.

Best brokers

List of licensed brokers that are trustworthy:

Reliable Russian brokers

| Name | Rating | pros | Minuses |

| Finam | 8/10 | The most reliable | Commissions |

| Opening | 7/10 | Low commissions | Imposing services |

| BKS | 7/10 | The most technologically advanced | Imposing services |

| Kit-Finance | 6.5/10 | Low commissions | Outdated software and user interface |

Warning about Forex and BO

Expert opinion

Vladimir Silchenko

Private investor, stock market expert and author of the Capitalist blog

Ask a Question

Work with real assets (Mechel shares) is carried out only on stock exchanges. Binary options and spot contracts on Forex are high-risk trading, leading to the loss of invested funds in 80% of cases. It is advisable to abandon such methods of earning money.

Severstal

Severstal is the most efficient metallurgist in terms of EBITDA margin, which allows the company to pay good dividends even in conditions of low product prices.

Since 2011, Severstal has been consistently paying dividends every quarter. In the current policy, the basis for calculation is free cash flow. Also, the amount of payments depends on the debt load, which is determined using the Net Debt/EBITDA ratio.

| Coefficient value | Payments |

| Net debt/EBITDA < 0.5 | >100% free cash flow |

| Net debt/EBITDA <= 1 | = 100% free cash flow |

| Net debt/EBITDA > 1 | = 50% free cash flow |

In recent years, the company's debt load has been at a good level, which allows it to pay 100% or more of FCF. In the first quarter of 2021, Net Debt/EBITDA decreased to 0.52.

Free cash flow is affected by capital expenditures. Severstal adopted a new investment program in 2021; peak CAPEX will occur in 2021 and 2021. To avoid cutting dividends sharply, the company said it would only take into account costs up to $800 million in its FCF calculation.

Based on this clarification and the forecast of financial results for 2021, the total dividends could be 187 rubles. , which implies a yield of 10.6% to current prices.

Final table

| Mechel PJSC | PJSC Severstal | PJSC MMK | PJSC NLMK | |

| Dividend for 2021, rub. | 4,7 | 187 | 6,2 | 29,7 |

| Dividend yield | 6% | 10,6% | 9,8% | 11% |

2021 could bring a lot of profit to metallurgical companies and good dividends to shareholders. Even though the company's shares have risen quite strongly since the beginning of the year, most will have returns of around 10%, according to the forecast.

A sharp correction in steel prices or actions by the Federal Antimonopoly Service could prevent the forecast from being fulfilled. At the beginning of the month, the regulator accused Severstal, MMK and NLMK of maintaining monopolistically high prices and threatened with a fine if confirmed. The fine is up to 2% of the companies’ total revenue, which is not that significant. But among the proposals to regulate the market, there were calls to limit the export of products, which could already significantly affect financial results. However, it will be difficult for the FAS to prove collusion due to the fact that export prices for steel, on which domestic prices depend, have also increased significantly.

In his next message to the Federal Assembly, the President of the Russian Federation hinted at increasing taxes for companies that direct all profits to dividends rather than investments. Severstal, MMK and NLMK may fall under the distribution. But it is not yet clear how the tax increase will be implemented and whether it will happen at all. Metallurgists, of course, direct all free cash flow to dividends, but at the same time, many have large-scale capital investments planned for 2021.