Nickel was discovered in the 18th century, but it was only towards the end of the next century that it began to be produced on an industrial scale, smelting as much as 600 tons in 1887 (in Saxony). The price of nickel grew along with the growing interest of mankind in this element, when its chemical properties were studied, thanks to which this metal, used as an additive to smelted iron, made new grades of steel, characterized by high corrosion resistance. In addition, in combination with other additives, the physical properties of steel changed, for example, strength increased.

Nickel is not the most abundant metal on the planet and naturally occurs in nature in a solid and concentrated state that allows it to be smelted into ore. Because of this, it is not cheap. Less than half of all reserves are located on land, and the share of economically recoverable volumes is still 2 times less. So the cost of nickel quite adequately reflects its relative rarity in nature and its demand in industry.

Currently, the price of nickel shows a high range of changes (from almost $4,600 per ton in 1998 to $37,200 in 2007), however, these fluctuations are very smooth and stretch over decades. The market strength of this asset, its characteristics, as well as investment potential are proposed to be considered on the pages of this article.

Geography of the corporation's presence

Taimyr Peninsula

One of the main production sites was located here. The resource saturation of this territory guarantees work for 80 years to come. The Talnakh and Norilsk ore clusters, the Oktyabrsky, Komsomolsky, Taimyrsky, and Mayak mines - the most productive assets of the corporation - are also located here.

Processing of mined ore is carried out in two stages. The primary process takes place at the Norilsk and Talkhanay concentrating plants, then the materials are supplied to the Mezhny and Nadezhdinsky metallurgical plants for final processing.

In the 3-4 quarters of 2021, part of the branch’s assets were transferred to Medvezhy Ruchey LLC in order to increase efficiency. This:

- Norilsk enrichment plant;

- Zapolyarny mine;

- tailings pond No. 1;

- tailings dump "Lebyazhye".

The bets were made on investments in the subsidiary, and they were supposed to have a positive effect and increase production capacity.

Kola Peninsula

Another “engine” of the company is based here – the Kola MMC. It is in charge of the development of the Zapolyarnoye, Zhdanovskoye and Kotselvaara fields. In 2021, together they produced over 7.5 million tons of raw materials. It is from here that the copper-nickel concentrate is supplied to the concentrating plant for briquetting, and the finished briquettes are transferred to the smelting shop.

Transbaikal region

Work is underway here at the Bystrinskoye deposit - this is the main one in the region where open-pit mining is used. For this purpose, the Bystrinsky Mining and Processing Plant (BGOK) was specially built in 2017. It will carry out work to enrich gold, copper and iron ore mined at the deposit. According to estimates, by the end of 2021 the plant will begin to operate at full capacity, and by 2022 production will be more than 10 million tons of ore per year.

Norilsk Nickel owns the Bystrinsky mining and processing plant, through its subsidiary LLC GRK Bystrinskoye. In it he owns a controlling stake of 50.01%

Finland

This country is home to one of the corporation’s main foreign assets – the Norilsk Nickel Harjavalta plant. Raw materials from the company's Russian production facilities are brought here for processing. Production capacity is 66 thousand tons per year. Norilsk Nickel Harjavalta is not a separate unit, but a link in the Norilsk Nickel technological chain.

South Africa

The representative office of Norilsk Nickel in South Africa is Norilsk Nickel Nkomati, the company is jointly owned with African Rainbow Minerals and is currently the only producer of nickel concentrate in the region. The advantage of Nkomati is a huge reserve of resources for conducting activities and the presence of two processing plants. Thus, at the end of 2021, about 7 million tons of ore were mined.

Australia

On this continent, Norilsk Nickel’s participation is noted in the very promising Honeymoon Well deposit, with projected resource reserves of 1.26 million tons of nickel.

Energy and gas assets

These include:

- JSC NTEC (Norilsk-Taimyr Energy Company) provides electrical and thermal energy using renewable sources (hydrogen generation) and gaseous hydrocarbons (natural gas). The company's activities include a full cycle of work: production, transmission and supply.

- JSC TAYMYRGAZ is developing the Pelyatkinskoye field on the Taimyr Peninsula, recognized as the richest in hydrocarbons in the region. The company's resources are sufficient to supply the entire industrial region of Norilsk.

- JSC NORILSKGAZPROM operates the Messoyakha, Yuzhno-Soleninskoye and Severo-Soleninskoye gas condensate fields.

- JSC NORILSKTRANSGAZ - spun off in 2021 from JSC NORILSKGAZPROM, provides logistics to the industrial areas of Norilsk.

Norilsk Nickel has its own transport and logistics complex:

- marine fleet of 5 container ships and a tanker, reinforced ice class;

- river fleet;

- aircraft fleet includes 15 airplanes and 18 helicopters;

- railway park.

Position of the company in the international market

Nickel

The corporation ranks second in the nickel market, after Vale with a 10% share. The gap is only 3%. Despite this, the company occupies a leading position in the primary nickel market.

Copper

The global copper market is quite saturated, but, nevertheless, the company is in the top 20 participants in this market with a result of 2%. Considering that the market's largest player accounts for only 9%, Norilsk Nickel's position can be considered successful. The largest volume of refined copper consumption is observed in China – 48%. The main volume is aimed at the production of electrically conductive materials.

Palladium

MMC Norilsk Nickel is a global giant in the production of palladium. Its share is 40% of the global volume. Palladium is consumed most actively in North America. 80% falls on the automotive industry for car exhaust gas purification systems.

Platinum

In the platinum market, Norilsk Nickel is one of the top 5 producers with a share of 11% of the global market. The main volumes of platinum are sent to Europe.

How to trade

The most common instrument for trading nickel on the exchange is a futures contract. The futures contract ticker on the LME (London Metal Exchange) is Ni (nickel). You can buy nickel on the stock exchange through a professional participant in the securities market - a broker.

But there are instruments that are more convenient than futures. For example, CFD (Contract For Difference). This type of contract implies a lower level of cost, and therefore greater accessibility for investors. Nickel CFDs are offered for trading by a limited number of brokers.

Major shareholders

The shareholders of MMC Norilsk Nickel are:

- Olderfrey Holdings Ltd1 – 30.4% (Vladimir Potanin)

- US Rusal Plc – 27.8% (Oleg Deripaska)

- Crispian Investments Ltd – 4.2%

The controlling shareholders are Olderfrey Holdings Ltd1 and US Rusal Plc. Relations between them are not the most friendly. It all started in 2008, when Oleg Deripaska acquired 25% of the shares; this conflict lasted 4 years and ended only in 2012 with the signing of a shareholder agreement. Roman Abramovich participated in resolving the conflict - he was appointed as an arbitrator.

At the moment, the shareholders' agreement is invalid due to its expiration, and the old conflict may break out with renewed vigor. It should be noted that the US sanctions policy did not bypass Oleg Deripaska, and sanctions were imposed on all his assets, including UC Rusal.

Forecast

Given that Indonesia will ban the export of nickel ore from January 2021, we should expect high market volatility for this metal in the 4th quarter.

A nickel surplus is unlikely in 2020–21 as growth in the electric vehicle market may exceed expectations. However, the global economic downturn suggests a general downward trend in stock market value.

Based on this, prices may remain at the average price level in 2019. The negative impact of the trade war on nickel market fundamentals will be limited. There may be a risk of metal shortage after 2021. The structural deficit of the nickel market will persist in the medium term.

Financial indicators

Asset dynamics

There is a positive dynamics of asset growth until 2021; in 2017 there is a slight decline.

Capital and liabilities

Borrowed funds significantly exceed equity capital, and their growth occurs every year. Experts attribute this to the payment of dividends; at certain periods of time their value exceeded 100% of the company’s profit, and significant investment projects were also implemented. There is an inversely proportional relationship between capital and liabilities: during the period when borrowed funds increase, capital decreases and vice versa.

Revenue

The company's revenue follows the trend line of its assets: stable growth in the period 2013-2016 and decline in 2021.

Net and operating profit

Net and operating income are in the growth stage until 2016; in 2021, both indicators are falling. Experts are betting that in 2021 these indicators will be rehabilitated and begin to grow. Favorable factors for this will be the growth of operating indicators, rising metal prices and the weakening of the ruble.

Cash flow

Cash flow has positive dynamics and is at a high level. However, since 2015 there has been a decline of approximately 30 million rubles.

Dynamics of dividend payments

Dividend payments had a negative trend only in 2016. By 2021, their level has recovered. In its dividend policy, the company uses the following benchmark: at least 30% of EBITDA or 60% if the NetDebt/EBITDA ratio is less than 1.8x.

EREPORT.RU

Sometimes the question is raised about whether there is a danger of depleting the planet's natural resources. In the case of nickel, there appears to be little cause for concern. Nickel is the fifth most abundant element on Earth. Only iron, oxygen, silicon and magnesium are more abundant. However, the reserves that can be extracted economically are of course more limited. Nickel reserves refer to proven reserves in onshore deposits. Nickel resources (estimated to be twice the size of nickel reserves) cover sub-economic reserves, i.e. not extracted profitably. The development of new technological processes will lead to the transformation of some of these resources into a reserve base. Ongoing exploration continues to add volumes to both reserves and resources. According to some sources, nickel resources on the seabed are many times greater than those located on land. Land resources are believed to last more than 100 years at current rates of extraction.

Nickel production in the world

Strong global economic growth through 2007 supported growth in primary nickel metal production. In 2007, global production of primary nickel was 1.411 million tons. However, the economic crisis led to a decline in nickel production worldwide between 2008 and 2009, and production of the primary metal fell to 1.316 million tons. Production quickly recovered in 2010 to 1.442 million tons, and further increased to 1.602 million tons in 2011. The annual average growth in production between 2001 and 2011 was 3.1%.

A new product, nickel pig iron (NPI), began production in China in 2005 in various forms and grades. Production increased slowly over the first few years: in 2010 it was estimated at more than 160 thousand tons, and in 2015 it was about 390 thousand tons. Basically all this product is used in the domestic market in China in the production of stainless steel and has replaced traditional products such as nickel metal and stainless steel scrap. In addition to NPI's new products in China, several other nickel projects have begun operations around the world. Examples are Barro Alto and Onca Puma in Brazil with a total capacity of about 95 thousand tons per year. The Ambatovy project with a capacity of 60 thousand tons began operating in Madagascar. Myanmar launched its first nickel project at Tagaung Taung, which began production in 2013. In New Caledonia, the 57,000 capacity Goro Vale project is currently in ramp-up phase. Global production of primary nickel was 1.98 million tons in 2014. During the period 2011-2015, the annual growth rate averaged 5.5%.

As of 2015, the world leader in nickel production is the Brazilian-Canadian company – Vale Inco Ltd., with a production volume of 291 thousand tons per year. Next in terms of production volume are MMC Norilsk Nickel (Russia) and the Chinese Jinchuan Group Co. Ltd, whose nickel production volume in 2015 was 266.4 thousand tons and 150.0 thousand tons, respectively.

The largest primary nickel producing countries are China, Russia, Japan, Australia and Canada. Moreover, China has made a real breakthrough in recent years. Thus, if in 1994 Chinese enterprises produced only 30 thousand tons of primary nickel, then in 2004 the volume of production of this metal was already approximately 75 thousand tons. In 2015, the volume of production of nickel products in China amounted to more than 550 thousand tons, including approximately 390 thousand tons of nickel cast iron and more than 150 thousand tons of cathode nickel.

Top five largest nickel producers in the world, thousand tons/year

| № | Company | Years | ||||

| 2011 | 2012 | 2013 | 2014 | 2015 | ||

| 1 | Vale Inco Ltd. | 241,5 | 237,0 | 260,2 | 275,0 | 291,0 |

| 2 | MMC Norilsk Nickel | 295,1 | 300,3 | 285,3 | 274,2 | 266,4 |

| 3 | Jinchuan Group Co. Ltd. | 130,0 | 135,0 | 143,0 | 128,0 | 150,0 |

| 4 | Glencore International AG | 105,9 | 106,9 | 98,4 | 100,9 | 96,2 |

| 5 | BHP Billiton | 144,7 | 156,1 | 111,2 | 93,7 | 78,5 |

World nickel consumption

In the nickel market, it is customary to distinguish between primary and final consumers. Primary consumers are those industries that directly consume nickel. End users are the industries that produce final nickel-containing goods. The main primary consumers of nickel are stainless steel producers. They account for about 2/3 of total consumption in the world. Nickel is also used in the production of special steels and alloys, in electroplating (nickel plating), catalysts, batteries, etc.

The main end consumers of nickel are transport, mechanical engineering, construction, chemical industry, production of tableware and other household products.

The main countries (groups of countries) consuming nickel are China, the European Union, Japan, the USA, Taiwan and South Korea. It should be clarified that since 2009, China has been in first place in the world in terms of the volume of use of refined nickel (52% of global demand in 2015).

It is interesting that in the country’s nickel market, the main producers of this metal, with the possible exception of Japan and China, are not its main consumers.

According to INSG, nickel consumption in 2015 increased to 1.94 million tons from 1.87 million tons in 2014, mainly due to increased demand in Asia and America.

Consumption of nickel in the world has been growing in recent years, mainly due to an increase in demand for this metal from Chinese producers of stainless steel, for the production of which about 2/3 of the nickel produced in the world is used.

With fairly stable demand for nickel from China, in recent years there has been growing activity in nickel purchases in other Asian countries, as well as in the United States. In Europe, the demand for metal remains quite moderate.

Balance of the world nickel market in 2006-2015, million tons*

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

| Production | 1,35 | 1,42 | 1,37 | 1,32 | 1,44 | 1,60 | 1,76 | 1,96 | 1,99 | 1,98 |

| Consumption | 1,40 | 1,32 | 1,29 | 1,23 | 1,47 | 1,61 | 1,67 | 1,78 | 1,87 | 1,89 |

| Balance | -0,06 | +0,09 | +0,08 | +0,08 | -0,02 | 0,00 | +0,09 | +0,18 | +0,13 | +0,09 |

* Data from International Nickel Study Group

In 2015, according to INSG experts, there was a surplus of 20 thousand tons on the global nickel market, with a production volume of 1.98 million tons and a consumption level of 1.89 million tons.

World nickel prices

Nickel prices have shown significant volatility over the past forty years. The late 1980s saw a peak in nickel prices. In the first half of the 1990s, the economic collapse of the former "Eastern Bloc" countries led to a surge in nickel exports, which caused nickel prices to fall below production costs, resulting in a decline in nickel production in the "West". Until 2003, the price of nickel remained below 10 thousand dollars/t. The price reached 14 thousand dollars/t. in 2005 and then jumped sharply in 2006 before peaking at $52,179/t. in May 2007. Nickel prices then declined until the end of 2008, when the average spot price reached a low of $9,678/t in December. At the beginning of 2009, nickel prices began to rise again and reached $24,103 thousand/t. by the end of 2010. In 2011, the price continued to rise and reached a peak in February at $28,247 thousand/t, and did not decrease until the end of 2013, when it fell below $14 thousand/t. The initial reaction to Indonesia's ban on raw ore exports in January 2014 pushed nickel prices to almost $20,000/t. in July 2014, but since then the price has dropped almost every month.

In 2015, nickel price quotes experienced the bitterness of defeat. On average, metal prices for the year amounted to about 11.8 thousand dollars/t, which is much lower (16.9 thousand dollars/t) than a year earlier.

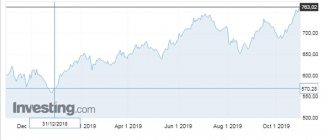

Nickel prices continue to develop a bearish trend against the backdrop of a slowing economy in China, the largest consumer of industrial metals. The debt crisis in the Eurozone in recent years has significantly affected the volumes of Chinese exports - accordingly, China's demand for metals and raw materials in general is falling. In the first half of 2021, nickel prices dropped to $8.3 thousand/t, but then increased slightly.

World prices for nickel, dollars/t

Source - London Metal Exchange

Other nickel market indicators

LME nickel reserves were relatively stable between 2001 and 2005 at around 20 thousand tonnes. Inventories increased slightly in 2005 and fell again in 2006. During the period from 2007 to 2009, stocks quickly increased to more than 158,000 tons at the end of the period. In 2010 and 2011, there was a decrease in reserves, which at the end of December 2011 reached 91,000 tons. From the beginning of 2012 to March 2021, there was a long period of inventory growth. In June 2015, LME nickel reserves reached over 470,000 tonnes. In the second quarter of 2015, the Shanghai Futures Exchange (SHFE) launched a nickel contract, and inventories there rose to 73,000 tons in March 2021. As of the end of March 2016, the combined reserves of LME and SHFE were over 500,000 tons. However, LME inventories fell slightly to 377,000 tonnes in mid-2021.

Prospects for the global nickel market

According to the forecast of the International Nickel Study Group (INSG), the surplus in the global primary nickel market will level out in 2021 compared to the situation in 2015, as demand growth outpaces metal supply growth. INSG forecasts a nickel deficit of about 49 thousand tons, compared to a surplus of about 90 thousand tons in 2015. Nickel production will fall 3.5% year-on-year in 2021, with production volumes at 1.91 million tonnes, while nickel consumption is expected to increase by 3.8% to 1.96 million tonnes in 2014 Global nickel production decreased by 0.3% year on year, while demand increased by 0.6%.

Indonesia's 2012 ban on nickel ore exports has caused real supplies of the material to decline in China, according to INSG's observations, although the country's production of nickel pig iron (a raw material for stainless steel production) is falling more slowly than predicted two years ago.

According to Morgan Stanley's forecast, the price of nickel will be $10,692 thousand tons in 2021 and $12,236 thousand per ton in 2021.

Other articles in the “Commodity Markets” section

Main risks

These include:

- The risk of developing a corporate conflict between major shareholders. Historically proven fact. Such a conflict can lead to uncontrolled repurchase of shares with an unpredictable outcome. Dividends may fall, since RUSAL is interested in growing cash flow and receiving large dividend payments for its own needs.

- Risk of falling metal prices. Metals are the main product of Norilsk Nickel's activities; financial stability is too dependent on its price. The trades of speculators, as well as a real decrease in the cost of metals, will have a negative effect on profits and revenues.

- Risk of dollar depreciation . A decline in the dollar will lead to a drop in revenue, since all payments are made in foreign currency, and costs are in Russian. If the ruble strengthens, the company's financial performance will decrease.

- Production and technological risks . Production disruptions, downtime, and accidents will reduce production capacity, and additional costs will arise, which will affect income.

- Political risk . The company exports, has production abroad - the political situation has an impact on its activities. Constantly growing prohibitions in the form of sanctions limit the activities of the corporation and the attraction of foreign investment. On the territory of the Russian Federation, the greatest risk is from the current tax policy and possible changes in it.

Price forecast

No matter how much the metal in question is in demand in the world, there is only one financial platform on the entire planet for determining its current price. Only the London Exchange (LME) nickel rate is an objective valuation indicated in all supply contracts. It is in London that numerous factors shape the resulting price trend.

Based on current analytics, the price forecast for the metal in question is subject to several of the most significant impacts:

Supply factors

- Expansion of the resource base. No breakthrough discoveries of new deposits are being made. However, taking into account the growth of consumption, the existing dynamics of reserve growth, nevertheless, allows us to constantly estimate their level for approximately a hundred years of operation at current consumption volumes.

- Increase in production capacity. The only market participants that are increasing production volumes are the Chinese and Brazilian-Canadian absolute world leader Vale Inco Ltd.

In general, we can talk about the lack of extensive development in the industry. However, there is an intensification of production, expressed in the emergence of technologies for wider processing of scrap nickel-containing metals.

Demand factors

- Since the final products that use nickel are highly processed goods with a high share of added value, the intensity of consumption of such goods depends entirely on the availability of liquidity in the pockets of buyers. And the solvency of the latter is closely related to crisis phenomena in the economy, and in general, to the rate of economic growth. The economic crisis reduces the solvency of the entire chain of consumers, so the nickel market is the first to suffer from recessionary trends.

- Recently, data from China has had a huge impact on the market for raw materials (both energy and metals), since this state represents the largest economic system in the world. And the pace of development of this economy is beginning to increase again.

It turns out that in the best case, with a constant resource base, as well as a not sufficiently growing production volume, we have demand increasing year by year at a higher rate (see Table). Hence the conclusion: there are fundamental prerequisites for the price of 1 kg of nickel to rush to the highs of 2007.

Short term forecast

Below are recommendations on 4 short timeframes from 5 minutes to one day, obtained using technical analysis indicators.

Carefully! These recommendations are received “automatically” and are nothing more than a hint. Only you yourself will be responsible for the decisions you make!