Economic analysis allows us to identify economic patterns from the facts of economic reality. Economic analysis involves the breakdown of the economy into separate components (economic categories) and is associated with:

- with the study of economic processes in their connection with each other;

- with academic justification of business plans, with an objective assessment of their implementation;

- with the disclosure of positive and negative factors and quantitative measurement of their impact;

- with the identification of trends and relationships in economic development, with the identification of unused on-farm reserves;

- with the generalization of best practices, with the adoption of optimal management decisions.

Economic analysis is a system of special knowledge based on the laws of development and functioning of systems and aimed at understanding the methodology for assessing, diagnosing and forecasting the financial and economic activities of an enterprise.

Economic analysis , a globally recognized tool for substantiating business decisions, is widely used to assess the financial performance of an enterprise in modern conditions.

The main goal of analytical processing is to reveal the causal relationship and measure the influence of factors on a particular indicator. Analytical processing of economic indicators is carried out using mathematical, statistical and other methods. The results of the analysis are summarized to evaluate the activities of the enterprise for the reporting period and identify the reasons, both positive and negative, affecting the overall results.

The subject of economic analysis is the economic processes of companies, societies, associations, socio-economic returns and the final financial results of their activities, which are formed under the influence of objective and biased factors, reflected through the system of economic information, the economic activities of companies, their structural divisions, associations, associations and the effectiveness of their activities, reflected in the system of indicators of the plan, accounting and reporting.

Classification of types of economic analysis

Classification is important for a correct understanding of its content and objectives. The basis of any classification of types of economic analysis is the classification of management functions, since economic analysis is a necessary element in the performance of each function.

Table 1. Classification of types of economic analysis

| Grouping characteristics | Types of analysis |

| Role in management | 1. managerial; 2.financial |

| Control object | 1.functional and economic; 2.technical and economic; 3.socio-economic; 4.financial and economic |

| Analysis users | 1.internal; 2.external |

| Time of the analyzed period | 1.operative; 2.current; 3.promising (forecast) |

| Time to make a management decision | 1.strategic; 2.tactical |

| Scope of analysis | 1.thematic; 2. by area; 3.comprehensive analysis |

| Spatial feature | 1.on-farm; 2.interfarm |

| Methodology for studying objects | 1. comparative; 2.diagnostic; 3.factorial; 4.margin |

| Purpose of analysis | 1. identifying reserves for increasing production volumes; 2. analysis of improving product quality; 3.reducing production costs and saving capital costs, etc. |

| Ways to compare data | 1. comparison with planned indicators; 2.with the results of the work of advanced domestic and developed foreign enterprises; 3. with the performance indicators of the analyzed object for the corresponding previous period |

| Frequency of analysis | 1.periodic; 2.one-time |

| Contents of the analysis | 1.complete (or comprehensive); 2. thematic (or local) |

| Degree of coverage of the analyzed object | 1.solid; 2.selective |

| Degree of mechanization or automation of economic analysis work | 1.automated; 2.mechanized; 3.manual |

There are various classifications of methods and techniques of economic analysis , one of which is presented to your attention.

1. Elementary methods of microeconomic analysis:

- balance method;

- acceptance of chain substitutions and arithmetic differences (deterministic factor analysis);

- integral method (more details here).

2. Traditional methods of economic statistics:

- grouping and comparison method;

- index method.

3. Mathematical and statistical methods for studying connections (stochastic modeling): correlation and regression analysis.

The listed techniques and methods are based on fairly strict formalized analytical dependencies. A more detailed description of them, as well as examples of their use, can be found in specialized literature, in particular in manuals on mathematical statistics, general theory of statistics, theory of economic analysis, and in monographic literature on certain sections of economic research.

Dynamic assessment of investment projects

The main indicators of dynamic assessment are:

- Net present value of investment NPV.

- Return on Investment Index PI.

- Internal rate of return of an investment project IRR.

- Discounted payback period of DPP.

The analysis of investment projects is carried out precisely according to these indicators.

The net present value of an investment shows the income from an investment, reduced to a specific date of its calculation, minus the investment in this project.

If investments are not made at once, then the investments are also brought to the settlement date. The reduction of cash flows to a specific date is carried out using the discount rate.

The discount rate is defined as the rate of hypothetical placement of investments in other projects on the calculation date, such as the bank's deposit rate, the bank's lending rate, the cost of capital of the investee, the average financial market rate. They are all compared and the maximum bet is selected. Most often, the basis for determining the discount rate is the cost of capital of the invested object, i.e. return on his capital. It is, as a rule, higher than other rates and both the investor and the investment consumer are guided by it, since their main criterion is the growth of the cost of capital. But it may happen that it will be lower, then the investor is guided by the financial market rate, and the investment consumer is guided by the banks’ lending rate.

The formula for calculating NPV is as follows:

Here:

- Io - initial investment;

- CFt – flow of income from investments in t-year;

- r – discount rate:

- n – life cycle of the investment project.

If investments were made in several periods, the formula takes the following form:

Where:

- It-year;

- T is the investment period.

For participants in an investment project, maximizing this indicator is the main goal; they use this indicator to evaluate the economic efficiency of the investment project. Therefore, if NPV <= 0, the project is removed from consideration by the investor.

Another dynamic assessment indicator, the return on investment index PI, reflects the profitability of a unit of investment in percentage terms and is determined by the formula:

This indicator is especially useful when comparing investment options with the same or similar NPV values. The option with a higher profitability index will be preferable. Under the obligatory condition PI>=0.

The internal rate of return of an investment project IRR is a very important indicator when evaluating and analyzing investments. It shows the maximum permissible rate of return of the project at its lower limit, therefore it is used in evaluation as a discount rate and is sometimes called a barrier rate. This indicator is used to estimate the expected rate of return for the entire life cycle of the project. For example, if IRR

The internal rate of return is determined by iterative calculation methods, selecting a rate at which the sum of incoming cash flows and cash outflows is equal to zero. In mathematical form it looks like this:

Where,

NPVirr is the net present value of investments calculated at the IRR rate.

This indicator is widely used when comparing the effectiveness of investment projects of different scale and duration.

The disadvantages of this indicator include the fact that with differently variable cash flows it gives an incorrect assessment of profitability.

To eliminate this drawback, it is necessary to determine it over separate periods of time, where there are no changes in signs in cash flows.

The discounted payback period DPP serves as a replacement for the PP payback period in dynamic assessments of investment projects.

If the investment is long-term in nature, the formula becomes:

This formula discounts not only incoming cash flows, but also investment investments in it.

If you compare PP and DPP for one option, then DPP will always be greater than PP.

This indicator more accurately reflects the investor's financial risk due to discounted cash flows. The main thing here is to correctly determine the discount rate.

Objectives of economic analysis

The main tasks of economic analysis:

- Increasing the scientific and economic validity of business plans and standards in the process of their development (implemented in the course of a retrospective analysis of economic activities).

- An objective and comprehensive study of the implementation of business plans and compliance with standards for the quantity, quality and range of products, works, and services is carried out according to accounting and reporting data.

- Determining the economic efficiency of the use of labor, material and financial resources determines the economic efficiency of the use of labor, material and financial resources, the use of means and objects of labor. Analysis of the use of material, labor and financial resources is directly linked to the analysis of the use of natural resources, with strict compliance with certain environmental requirements.

- Monitoring the implementation of commercial calculation requirements and evaluating the final financial results. The entire production cycle and final financial results depend primarily on compliance with the principles of commercial calculation.

- Identification and measurement of internal reserves (at all stages of the production process). Reserves can be identified through a comparative study of the implementation of the plan by the internal divisions of the enterprise.

- Testing the optimality of management decisions (at all levels of the hierarchical ladder).

Economic analysis is the division of the studied economic phenomena into economic categories (their individual parts), the study of these categories, the causes and factors that influenced their changes, the determination of the correspondence of these changes to economic laws, and also, based on all this, the development of recommendations for making management decisions on eliminating identified deficiencies and increasing efficiency.

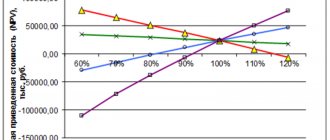

Investment project example with calculations for Mini-CHP on peat

The creation of mini thermal power plants is possible even in the absence of main gas. One of the small-scale energy investment projects proposes the creation of such a power plant on peat mines to provide electric energy for the development of peat deposits and provide the settlement with electricity. The power plant is based on four Jenbacher GE type 620 generators, running on gas from peat combustion at the PEAT PLANT. The power plant generates 13 MW of electricity per year, this is enough to operate industrial units in peat mining and provide electricity to peat bog villages. The calculation is made in euros, since imported equipment is purchased for this currency.

Initial data Project "Mini thermal power plant on peat"

Calculation of the economic efficiency of the project “Mini thermal power plant on peat”

An assessment of an investment project using the example of a mini-thermal power plant on peat shows that the economic efficiency of the investment project is acceptable, especially in isolated areas where the delivery of electricity is difficult, as well as the delivery of other energy resources. This is the peculiarity of the evaluation of investment projects, when the project is recognized as effective with relatively low indicators of its effectiveness. Other efficiency criteria come to the fore, such as social efficiency, the need to use local resources as energy carriers, etc. factors. At the same time, in this project the internal rate of return is higher than the level of the loan rate, and the payback period for the given conditions of the project is quite suitable. NPV for the life cycle of the project will be 32.62 million euros.

Stages of economic analysis

In the most general case, the process of applied economic analysis includes the following stages and procedures:

- defining the problem and goals of the analysis, including identifying the needs for performing the analysis, defining the problem, and articulating the goals of the analysis;

- developing analysis plans, including choosing analysis methods, determining the type of information required and sources for obtaining it, determining methods for collecting the necessary data, developing or selecting forms for collecting and presenting data, developing a sampling plan and determining sample sizes;

- Implementation of the analysis execution plan, including necessary data collection and data analysis;

- interpretation of analysis results and presentation to users: preparation and presentation of the final report to the stakeholder making a decision based on the results of the analysis.

Table 2. Algorithm for economic research

| Preparatory work | Monitoring | Diagnostics |

| Analysis of the object being studied | ||

| 1. Determination of the purpose and objectives of the study | 6. Checking the accuracy and reality of the information | 11. Comparison of effective and estimated performance indicators of the object under study with data from the plan and the previous period (year) |

| 2. Study of the methodology of regulatory documents related to the object under study | 7. Preparation of materials and information for study | 12. Determination of the dynamics of performance and evaluation indicators over a number of years, identifying patterns of change |

| 3. Determination of economic categories, methods of their assessment, existing methodology for the object under study | 8. Assessment of the quality and performance indicators of the object being studied | 13. Determination of the influence of factors and causes of the internal and external environment on the performance and evaluation indicators of the activity of the object under study |

| 4. Development of a research plan and program | 9. Comparison of estimated indicators with data from the plan, standards and the previous period | 14. Calculation of the influence of factors on the effective and estimated performance indicators of the studied object |

| 10. Establishing a diagnosis of the object being studied (conclusion based on monitoring results) | 15. Grouping of factors and reasons according to their positive and negative impact on the performance and evaluation indicators of the activity of the object being studied | |

| 16. Study of each of the factors and reasons | ||

| 17. Grouping of factors and reasons that depend and do not depend on the activities of the enterprise management | ||

| 18. Development of recommendations for making management decisions (conclusion based on the results of the analysis) | ||

Static methods for evaluating investment projects

Static methods for assessing investment projects are characterized by simplicity of calculations, therefore they are often used for preliminary assessment. The visibility of the indicators also adds to their attractiveness. However, their assessment is of an auxiliary nature.

The most popular indicator is the return on investment or its payback period. The latter is determined if several investors, and each of them determine the effectiveness of their own investments.

This indicator shows the investor after what period of time the funds he invested will return to him in the form of net profit. It can be calculated in two ways. If cash flows in the form of net profit are regular and their fluctuations during the analyzed periods are assumed to be insignificant, then the calculation of the indicator looks like the quotient of dividing the initial investment by the average monthly or average annual net profit from sales. Or as a formula:

Where:

- PP - payback period in years (months);

- Io – initial investment;

- CFcr – average annual (average monthly) net income.

This assumption is often not met, so the general calculation formula looks like this:

PP = min t at which

In other words, when the accumulated profit from an investment equals the amount of the initial investment, this moment is its payback period.

An example of calculating the payback period

It is planned to introduce an automated quality management system at the rolling mill, which will reduce the yield of defective products and increase revenue by 5%.

The average monthly revenue from rental sales is 100 million rubles. The investment project is estimated at 24 million rubles. Additional revenue will be 5 million rubles per month. Net profit from this revenue is 1.2 million rubles.

The payback period for investments is determined as the quotient of dividing the investment by the average monthly net profit from a given event, namely:

PP = 24/1.2 = 20 months.

The general calculation method is used by enterprises whose products are irregular in nature, for example seasonal, such as a thermal power plant producing electric and thermal energy, whose heating season falls on the cold periods of the year.

The inverse of the payback period is called the efficiency ratio or sometimes return on investment.

The investment efficiency ratio ARR is calculated as the ratio of the average annual net profit to the volume of initial investment:

This indicator is more often called return on investment. And the indicator determined by the formula:

efficiency coefficient, here If the residual value of the investment project at the end of its life cycle or when its implementation is stopped.

So if we take the previously considered investment example, then the ARR for it will be equal to:

ARR =1.2*12/24=0.6 or as a percentage of 60%. The return on investment is 60%. If we assume that the residual value of the project is 0.5 million rubles, then the investment efficiency is equal to:

ARR = 1.2*12/(24+0.5)/2=0.293 or as a percentage 29.3%.

These indicators (PP and ARR), in addition to the advantages of clarity and ease of calculation, have significant disadvantages that narrow the scope of their use, especially when analyzing the effectiveness of investments.

Firstly, they do not take into account the time factor in the value of money; to calculate them, it doesn’t matter when the ruble is spent, this year or in the future. Accordingly, cash flows of profit also do not take this factor into account. Although it is well known that the value of money changes over time, and everyone whose salary is stable feels this. You can say that it is inflation that changes the value of money, yes it is, and not only that. Inflation is taken into account using calculation methods, and the cost of money is taken into account by discounting cash flows.

The second disadvantage of the payback period is the limitation of its validity to the billing period. Everything that happens after determining the payback period is not described by the indicator. When comparing several investment projects with equal payback periods, it is impossible to determine which one is more effective. The amount of accumulated profit over the life cycle of an investment may differ significantly. The efficiency ratio cannot give an answer to this either, since the average annual profit is determined not for the entire life cycle, but only for the payback period of investments.

Therefore, these indicators are largely complementary to the dynamic assessment of investment performance.