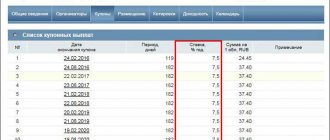

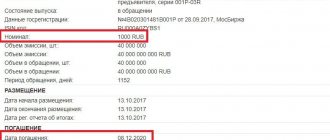

Bonds: Russia, 29006 (OFZ-PK)29006RMFS, RU000A0JV4L2, OFZ 29006

The Russian domestic government securities market is represented by federal loan bonds (OFZ). OFZs are placed at auctions held by the Ministry of Finance or through closed subscription. The auction schedule with information on the dates and planned volume of placements is published on the Ministry’s website quarterly.

The Ministry of Finance of the Russian Federation determines the main directions of the state debt policy of the Russian Federation. The document of the same name is published on the website of the Ministry of Finance.

The Ministry of Finance issues the following types of OFZ:

• OFZ-PD – federal loan bonds with constant (fixed) income. The coupon rate is determined before placement and is fixed until maturity.

• OFZ-PK – federal loan bonds with a variable coupon. The coupon rate is tied to the RUONIA rate. From 2021, coupon income is calculated based on the average value of RUONIA rates for the current, and not the expired coupon period as for previous OFZ-PK issues, with a small “technical” time lag of 7 calendar days.

• OFZ-IN – federal loan bonds with an indexed par value. To index the denomination, the Russian Federation Consumer Price Index, published monthly by Rosstat, is used.

• OFZ-AD – federal loan bonds with debt amortization. The face value of these bonds is redeemed in installments.

• OFZ-n – federal loan bonds for the population. Only individuals - citizens of the Russian Federation can purchase OFZ-n directly through agent banks: Sberbank, VTB, Promsvyazbank and Post Bank. OFZ-n are not traded on the stock exchange.

Previously, the Ministry of Finance issued the following types of securities (today they are in circulation):

• GSO – government savings bonds. Interest rates on such bonds were set constant - GSO-PPS (a single interest rate is determined for all coupon periods) or fixed - GSO-FPS (for all coupon periods the interest rate is determined, but does not coincide). GSO were intended for residents, large institutional investors. The last placement took place in October 2012.

A description of other types of government bonds that the Ministry of Finance has issued in the past is available in the “Glossary” section of the Cbonds website.

The maximum amount of external loans is determined in the Program of State External Borrowings of the Russian Federation in the Appendix to the Federal Budget of the Russian Federation for each financial year. The Russian Federation places Eurobonds denominated in dollars and euros on the Irish, London, Berlin and Luxembourg stock exchanges. Placement is carried out in the form of open or closed subscription with the involvement of placement agents (organizers). Potential purchasers are individuals and legal entities, residents and non-residents of the Russian Federation.

Federal loan bonds for the population

*In connection with the new tax regime, when an individual presents OFZ-n for redemption before the expiration of 12 months from the date of acquisition, a situation is possible in which the total amount of funds received as a result of redemption, taking into account coupon payments received during the period of ownership of OFZ-n, will be less than the amount of funds spent on the purchase of bonds by the amount of tax withheld from the received and accumulated coupon income.

Brokerage services are provided by PJSC Sberbank (Bank), general license of the Bank of Russia for banking operations No. 1481 dated August 11, 2015, license for the provision of brokerage services No. 045-02894-100000 dated November 27, 2000.

You can obtain detailed information about the Bank's brokerage services by calling 8-800-555-55-50, on the website or at the Bank's branches. This website also contains the current conditions for the provision of brokerage and other services. Changes in conditions are made by the Bank unilaterally.

The contents of this document are provided for informational purposes only and do not constitute an advertisement of securities and/or other financial instruments and/or financial services. Nothing contained herein is or should be construed as an offer by the Bank to buy or sell any financial instruments, products or services to any person. No financial instruments, products or services mentioned herein are offered or sold in any jurisdiction where such activity would be contrary to securities laws or other local laws and regulations or would subject the Bank to compliance with registration in such jurisdiction. In particular, we would like to inform you that a number of states (in particular, the United States and the European Union) have introduced a sanctions regime that prohibits residents of the relevant states from acquiring (assisting in the acquisition) of debt instruments issued by the Bank. The Bank invites you to ensure that you are eligible to invest in the financial instruments, products or services mentioned herein. Therefore, the Bank cannot be held liable in any way if you violate any prohibitions applicable to you in any jurisdiction.

Nothing in this information material constitutes or should be construed as individual investment advice and/or the Bank's intention to provide investment advisory services. The Bank cannot guarantee that the financial instruments, products and services described therein are suitable for persons who have read such materials. The Bank recommends that you do not rely solely on the information you have been provided with in this material, but rather make your own assessment of the relevant risks and, if necessary, engage independent experts. The Bank is not responsible for financial or other consequences that may arise as a result of your decisions regarding financial instruments, products and services presented in the information materials.

The Bank makes reasonable efforts to obtain information from sources it believes to be reliable. However, the Bank makes no representation that the information or estimates contained in this information material are true, accurate or complete. Any information provided in this document is subject to change at any time without notice. Any information and estimates contained herein do not constitute terms of any transaction, including any potential transaction.

Financial instruments and investment activities involve high risks. This document does not contain a description of such risks, information about the costs that may be required in connection with the conclusion and termination of transactions related to financial instruments, products and services, as well as in connection with the performance of obligations under the relevant agreements. The value of shares, bonds, investment shares and other financial instruments may decrease or increase. Past investment performance does not determine future returns. Before entering into any transaction in a financial instrument, you must ensure that you fully understand all the terms of the financial instrument, the terms of the transaction in such instrument, and the legal, tax, financial and other risks associated with the transaction, including your willingness to bear significant losses.

The bank and/or the state does not guarantee the profitability of investments, investment activities or financial instruments. Before making an investment, you must carefully read the conditions and/or documents that govern the procedure for its implementation. Before purchasing financial instruments, you must carefully read the terms and conditions of their circulation.

The Bank draws the attention of Investors who are individuals to the fact that funds transferred to the Bank as part of brokerage services are not subject to the Federal Law of December 23, 2003. No. 177-FZ “On insurance of deposits of individuals in banks of the Russian Federation.

The Bank hereby informs you of the possible existence of a conflict of interest when offering the financial instruments discussed in the information materials. A conflict of interest arises in the following cases: (i) the Bank is the issuer of one or more financial instruments in question (the recipient of the benefit from the distribution of financial instruments) and a member of the Bank’s group of persons (hereinafter referred to as the group member) simultaneously provides brokerage services and/or (ii) a group member represents the interests of several persons simultaneously when providing them with brokerage or other services and/or (iii) a group member has his own interest in performing transactions with a financial instrument and simultaneously provides brokerage services and/or (iv) a group member acts in the interests of third parties or interests another group member, maintains prices, demand, supply and (or) trading volume in securities and other financial instruments, including acting as a market maker. Moreover, group members may have and will continue to have contractual relationships for the provision of brokerage, custody and other professional services with persons other than investors, and (i) group members may receive information of interest to investors and participants the groups have no obligation to investors to disclose such information or use it in fulfilling their obligations; (ii) the conditions for the provision of services and the amount of remuneration of group members for the provision of such services to third parties may differ from the conditions and amount of remuneration provided for investors. When resolving emerging conflicts of interest, the Bank is guided by the interests of its clients. More detailed information on the measures taken by the Bank regarding conflicts of interest can be found in the Bank’s Conflict of Interest Management Policy, posted on the Bank’s official website: (https://www.sberbank.com/ru/compliance/ukipk)

What does the OFZ yield curve say? In Russia, Dollar, News, OFZ, Ruble, Medium-term trends

Government bond yields affect a large number of Russian market instruments, including ruble quotes. Meanwhile, since the beginning of the crisis, the yield curve of Russian debt instruments has undergone many changes and carries important signals.

A bond yield curve (state, municipal, or corporate) is a graphical representation of the relationship between the yields of different bond issues depending on their maturity. It is often also called the zero-coupon yield curve or G-curve. In general, the G-curve represents changes in interest rates in the economy.

As a rule, there are three main types of curve: normal, inverse and flat.

a) Normal curve

In the first case, as the maturity of securities increases, the yield increases against the background of correspondingly increasing temporary risks. This shape of the curve, as a rule, corresponds to the normal state of a growing economy, where inflation risks increase as the business cycle develops. Short-term interest rates are expected to be higher in the future.

As time passes until maturity, the rate of increase in yield slows down. The curve becomes flatter. Yields are approaching their long-term average.

b) Inverse curve

An inverse (reverse) curve is characterized by high short-term yields, which decrease as the maturity of the securities increases. The rate of decline of the curve is also slowing down. Yields are approaching their typical long-term average.

The inverted curve characterizes short-term investor fears. They can be caused either by an approaching recession, a decrease in economic activity, or by problems that have already occurred in the economy of a state or enterprise. The slope of the curve indicates significant short-term inflation risks. But over time, investors expect rates in the economy to return to long-term averages.

c) Flat curve

The business cycle in the economy involves successive periods of rising and falling rates. In this case, the yield curve, for example, government bonds, will transform from normal to inverse and back.

The third type of curve, intermediate, is called flat. It is characterized by almost identical bond yields, almost regardless of the maturity date.

There are two principles for forming such a curve.

bcs-express.ru

OFZ Bond 26221 (RU000A0JXFM1) Yield, Price

- Ribbons

- Topics Promotions

- Quotes

- Calendar Information Books

- Members of the Mood

OFZ bond 26221 now costs 958.0 rubles or 95.80% of the par value. The bond will be fully repaid at par on 2033-03-23. If you buy one bond now, you will pay the seller the accumulated coupon income of 25.52 rubles, and the next coupon will be paid to you on 2018-10-10 in the amount of 38.39. In this case, the first coupon payment for you will be 12.87 rubles, which implies a yield of the first coupon of 1.3% .The current bond yield to maturity is 8.36% per annum.

Price and yield of bond OFZ-PD 26221 03/23/33

| Name | OFZ 26221 |

| ISIN | RU000A0JXFM1 |

| maturity date | 2033-03-23 |

| Years to maturity | 14.67 |

| Next date payments | 2018-10-10 |

| Denomination | 1000 |

| Currency | rub |

| Ext. coupon, per annum from no. | 7.68% |

| Coupon, rub | 38.39 RUR |

| NKD | 25.52 RUR |

| Coupon payment, days | 182 |

| Bond name | OFZ-PD 26221 03/23/33 |

| Name, English | OFZ-PD 26221 |

| Reg. number | 26221RMFS |

| Issue size | 350 000 000 |

| In circulation | 350 000 000 |

| Lot size | 1 |

| Price step | 0.001 |

| Where is it traded? | T+: Bonds - no address. |

| Status | A |

| Listing level | 1 |

| Profitability | 8.36% |

| Price of afterbirth | 95.802 |

| Changes per day, % | -1.02% |

| Volume per day, rub | 166 032 833 |

| Last time deals | 18:39:57 |

| Duration, days | 3168 |

smart-lab.ru

OFZ Bond 26212 (RU000A0JTK38) Yield, Price

- Ribbons

- Topics Promotions

- Quotes

- Calendar Information Books

- Members of the Mood

OFZ bond 26212 now costs 928.5 rubles or 92.85% of the par value. The bond will be fully repaid at par on 01/2028/19. If you buy one bond now, you will pay the seller the accumulated coupon income of 1.74 rubles, and the next coupon will be paid to you on 2019-01-30 in the amount of 35.15. In this case, the first coupon payment for you will be 33.41 rubles, which implies a yield of the first coupon of 3.6% .The current bond yield to maturity is 8.32% per annum.

Price and yield of bond OFZ-PD 26212 01/19/28

| Name | OFZ 26212 |

| ISIN | RU000A0JTK38 |

| maturity date | 2028-01-19 |

| Years to maturity | 9.48 |

| Next date payments | 2019-01-30 |

| Denomination | 1000 |

| Currency | rub |

| Ext. coupon, per annum from no. | 7.03% |

| Coupon, rub | 35.15 RUR |

| NKD | 1.74 RUR |

| Coupon payment, days | 182 |

| Bond name | OFZ-PD 26212 01/19/28 |

| Name, English | OFZ-PD 26212 |

| Reg. number | 26212RMFS |

| Issue size | 358 927 588 |

| In circulation | 350 000 000 |

| Lot size | 1 |

| Price step | 0.001 |

| Where is it traded? | T+: Bonds - no address. |

| Status | A |

| Listing level | 1 |

| Profitability | 8.32% |

| Price of afterbirth | 92.85 |

| Changes per day, % | -0.43% |

| Volume per day, rub | 1 602 544 890 |

| Last time deals | 18:45:25 |

| Duration, days | 2533 |

smart-lab.ru

Help a beginner understand the choice of OFZ

Help a beginner understand the choice of OFZ

Good afternoon, dear forum users!

I'll start with a short preamble:

Two years ago, my wife and I started saving, but so that the money wouldn’t just lie under our pillow, we decided to open a deposit in a bank, eventually we reached a fireproof amount in one bank and, to diversify the risks of bankruptcy, we opened an account in another bank, in August we should reach fireproof amount in the new bank. I am a rather conservative investor and I don’t have time to follow quotes/news and other things necessary for successful trading in the stock/forex market. I thought about how else I could balance my investment portfolio, and after a little “smoking” on the topic, I found the idea of buying bonds, namely OFZs, acceptable to me.

And now the actual ambulatory:

The question arose with the choice of bonds of one issue or another. Again, after reading various articles on the Internet where fundamental analysis was described, I made the following conclusions related to the current state of affairs on the market:

1) When interest rates fall, you should buy bonds with a longer duration.

2) You should buy bonds with a larger premium to the OFZ yield curve, as they have a higher potential for price growth

After analyzing the OFZ yield curve, I concluded that now the best choice would be to buy bonds of issue: 29012, 29006, 29007.

There are also bonds, for example issue 29010, with a higher yield, but they are sold at a price significantly higher than the face value, in connection with this I had the following questions:

1) How correct is my approach to choosing OFZ?

2) Is it worth overpaying for OFZs now in order to get higher returns in the future?

Considering our unstable situation in the country, I’m unlikely to hold bonds until maturity and most likely will be a speculator, selling somewhere “in the middle,” so when buying, I also focus on the potential increase in price.

Thanks in advance for your help and advice!

smart-lab.ru