Last week, Rosstat reported a 12% year-on-year increase in the producer price index (PPI) in May, which was noticeably higher than the consensus forecast. Although spikes in producer price movements do not always lead to increased consumer price inflation, some market participants may be wondering about financial instruments that are protected from inflation shocks. Federal loan bonds with an indexed par value (OFZ-IN) are just such an instrument, with yield linked to actual inflation with reliability properties corresponding to the class of sovereign bonds. We decided to explore what OFZ-INs are and what kind of profitability they can provide to investors in different macroeconomic scenarios.

Pros and cons of the release

A clear advantage of issue 26217 is reliability: coupons of 7.5% per annum are paid regularly and twice a year. Confidence in the asset is confirmed by the reputation of the state: there has not yet been a case of delay or non-payment of coupons by the issuer over the past 20 years for all of its obligations.

A significant advantage of the instrument is the very convenient lot size - 1000 rubles, which makes OFZ 26217 accessible to investors with small accounts.

A small minus is the decreased yield to maturity. The value of the Central Bank as of November 1, 2019 is 102.75% of the nominal value. This reduces the profit of OFZ series 26217 to 5.93% per annum.

OFZ-IN – main parameters

Sources: Bloomberg, Moscow Exchange, Ministry of Finance of the Russian Federation State. reg. issue number 52001RMFS 52002RMFS

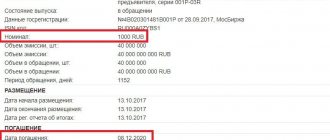

| Stock code | SU52001RMFS3 | SU52002RMFS1 |

| ISIN | RU000A0JVMH1 | RU000A0ZYZ26 |

| Posting date | July 2015 | March 2021 |

| Volume of issue in circulation | 171 billion rubles. | 60.5 billion rubles. |

| maturity date | 16.08.2023 | 02.02.2028 |

| Denomination as of placement date | 1000 rub. | |

| Indexation of denomination | daily according to the consumer price index with a lag of 3 months. | |

| Coupon | 1.25% of the nominal value every six months | |

| Moody's rating | Ba1 | — |

| S&P rating | BBB | — |

| Fitch rating | BBB- | — |

Best brokers

Reliable Russian brokers

| Name | Rating | pros | Minuses |

| Finam | 8/10 | The most reliable | Commissions |

| Opening | 7/10 | Low commissions | Imposing services |

| BKS | 7/10 | The most technologically advanced | Imposing services |

| Kit-Finance | 6.5/10 | Low commissions | Outdated software and user interface |

Inflation modeling

The most recent assessment of future consumer price inflation, announced following the June meeting of the Central Bank of the Russian Federation, assumes an increase in inflation to 3.5% - 4.0% this year, with the possibility of growth to 4.0% - 4.5% in 2021. and stabilization at 4.0% in 2020. In our model, we focused on the upper limit of the Central Bank’s forecast range for inflation and assumed a constant inflation rate starting in 2021. and until the OFZ-IN redemption inclusive. We considered three scenarios that differ in the level of inflation after 2021. – let’s call this level “long-term inflation”, CI. Scenario A (conservative) assumes stabilization of inflation at the level of 4.0% (CI = 4.0%), scenario B (baseline) – at the level of 5.0%, scenario C (shock) – at the level of 8.0%. Note that inflation forecasts for long periods are extremely unreliable, since actual inflation depends on a huge number of parameters, including external price shocks. Over the past five years, for example, inflation at the end of the year (Rosstat data) ranged from 2.5% to 12.9% (the range is even wider if we look at monthly data).

Forecast of annual inflation for the purpose of calculating the yield of OFZ-IN:

Source: OLMA Investment Fund estimates Period Scenario A Scenario B Scenario C

| 2018 | 4.0% | 4.0% | 4.0% |

| 2019 | 4.5% | 4.5% | 4.5% |

| 2020 | 4.0% | 4.0% | 4.0% |

| 2021 – 2028 (CI) | 4.0% | 5.0% | 8.0% |

We calculated the expected flow of payments on OFZ-IN bonds (coupons + par value to maturity) in three forecast scenarios and estimated the corresponding expected yield (in annual %) based on current OFZ-IN prices on the Moscow Exchange.

Estimation of yield on OFZ-IN in three scenarios:

Source: OLMA Investment Fund estimates Tool Scenario A Scenario B Scenario C

| 52001RMFS (2023) | 6.8% | 7.2% | 8.6% |

| 52002RMFS (2028) | 7.1% | 7.8% | 10.0% |

Other issues of the issuer

| Name | Profitability | Price | Years to maturity | Coupon, rub | NKD, rub | Coupon payment date | maturity date |

| OFZ 24020 | 0.0% | 99.82 | 1.2 | 0 | 2.75 | 2021-07-28 | |

| OFZ 24021 | 0.0% | 99.102 | 2.9 | 0 | 2.75 | 2021-07-28 | |

| OFZ 25083 | 5.4% | 100.9 | 0.6 | 34.9 | 29.72 | 2021-06-16 | |

| OFZ 26207 | 6.7% | 107.2 | 5.7 | 40.64 | 22.11 | 2021-08-11 | |

| OFZ 26209 | 5.7% | 102.2 | 1.2 | 37.9 | 24.99 | 2021-07-21 | |

| OFZ 26211 | 5.8% | 102.047 | 1.7 | 34.9 | 21.67 | 2021-07-28 | |

| OFZ 26212 | 6.9% | 101.324 | 6.7 | 35.15 | 21.82 | 2021-07-28 | |

| OFZ 26215 | 6.0% | 102.289 | 2.3 | 34.9 | 17.64 | 2021-08-18 | |

| OFZ 26217 | 5.2% | 100.553 | 0.3 | 37.4 | 18.91 | 2021-08-18 | |

| OFZ 26218 | 7.2% | 110.62 | 10.4 | 42.38 | 11.64 | 2021-09-29 | |

| OFZ 26219 | 6.7% | 105.013 | 5.3 | 38.64 | 12.1 | 2021-09-22 | |

| OFZ 26220 | 5.7% | 102.555 | 1.6 | 36.9 | 32.85 | 2021-06-09 | |

| OFZ 26221 | 7.2% | 104.732 | 11.9 | 38.39 | 9.07 | 2021-10-06 | |

| OFZ 26222 | 6.3% | 102.593 | 3.4 | 35.4 | 5.64 | 2021-10-20 | |

| OFZ 26223 | 6.2% | 101.002 | 2.8 | 32.41 | 13.89 | 2021-09-01 | |

| OFZ 26224 | 7.0% | 100 | 8.0 | 34.41 | 31.95 | 2021-06-02 | |

| OFZ 26225 | 7.2% | 101.15 | 13.0 | 36.15 | 34.96 | 2021-05-26 | |

| OFZ 26226 | 6.7% | 106.095 | 5.4 | 39.64 | 7.84 | 2021-10-13 | |

| OFZ 26227 | 6.3% | 103.341 | 3.2 | 36.9 | 24.33 | 2021-07-21 | |

| OFZ 26228 | 7.1% | 104.748 | 8.9 | 38.15 | 6.08 | 2021-10-20 | |

| OFZ 26229 | 6.5% | 102.906 | 4.5 | 35.65 | 0.2 | 2021-11-17 | |

| OFZ 26230 | 7.3% | 105.3 | 17.9 | 38.39 | 9.07 | 2021-10-06 | |

| OFZ 26235 | 7.1% | 92.148 | 9.8 | 29.42 | 9.21 | 2021-09-22 | |

| OFZ 26236 | 7.0% | 93.747 | 7.0 | 30.61 | 29.67 | 2021-05-26 | |

| OFZ 29006 | 5.0% | 101.301 | 3.7 | 26.78 | 15.6 | 2021-08-04 |

Denomination indexation and coupon calculation

The nominal OFZ-IN is indexed daily in accordance with the inflation rate reflected in Rosstat statistics (https://www.gks.ru/bgd/free/b00_24/IssWWW.exe/Stg/d000/I000650R.HTM) as of the month for three months before the date of calculation of the face value. For example, during June the bond par value is indexed in accordance with the inflation rate recorded in March of the same year. Here is an example of calculating the par value for bonds 52001RMFS:

Rosstat data for 2021:

Period The value of the price index compared to the average annual prices of 2000. Inflation in annual terms

| January | 553.1 | 2.2% |

| February | 554.2 | 2.4% |

| March | 555.8 | 2.4% |

| April | 557.9 | 2.4% |

| May | 560.0 | 2.4% |

The OFZ-IN coupon is set as a percentage of the face value and in ruble terms changes along with changes in the face value. For example, the next coupon for 52001RMFS (2023) will be paid on 08/22/18. Knowing the inflation rates for May, we can calculate that the par value of the bond as of 08/22/18 will be 1149.23 rubles, and the size of the semi-annual coupon = 1.25% * 1149.23 rubles. = 14.36 rub.

Indexation of OFZ-IN denomination:

Date i X(i) Denomination 52001RMFS

| 01.06.18 | 1 | 554.20 | 1 138.61 |

| 02.06.18 | 2 | 554.25 | 1 138.72 |

| 03.06.18 | 3 | 554.31 | 1 138.83 |

| 04.06.18 | 4 | 554.36 | 1 138.93 |

| 05.06.18 | 5 | 554.41 | 1 139.04 |

| X(i)=554.2+(555.8-554.2)*(i-1)/30 (30 – number of days in June) | |||

| Denomination (i) = Denomination (i-1)*X(i)/X(i-1) |

Investor reviews

It’s nice that the consciousness of our compatriots in terms of investing is steadily increasing. Their remarks indicate that OFZs are a good choice for adherents of the “buy and hold” strategy.

There are also well-founded opinions against – but not against OFZs in general, as you can see. It’s just that episode 26… didn’t suit a specific person. This is about the question that it is still better to think with your own head.

How to calculate income on OFZ bonds

As you know, OFZ bonds are securities, by purchasing which you lend Russia a certain amount. And the state, after a predetermined period, returns it to you with a percentage, which is called coupon income or simply a coupon.

However, the yield is not limited to one coupon, since you can buy bonds cheaper and sell them more expensive. This is the market (current) return. This method can be used if you want to buy securities for a short term and repay them early when the most favorable situation arises.

Thus, the income consists of the coupon and the difference between the sale and purchase prices. Of course, from the resulting value you also need to subtract the broker’s commission (usually it is small, about 1%), as well as taxes: personal income tax is never withheld from the coupon, but is collected from the current yield.

For reference

However, if you opened an IIS, bought bonds and applied a type B tax deduction, then personal income tax will not be withheld from you. However, in this case, you will not be able to return 13% of the contribution (type A deduction), since you can only choose one of two benefits.

How has the sovereign debt market changed?

After reaching its peak at the end of April 2021, the OFZ market found itself in a sideways trend for a long time: prices of issues with a constant coupon changed within a narrow range amid a shortage of driving factors. However, as the new year began, volatility began to increase sharply. The quotes were affected by both the growing yield of the main world benchmarks (the rate of 10-year US Treasury bonds increased by 40 bp from the beginning of January, to 1.3%), and the continued rise in consumer prices in Russia. Geopolitical risks remained on the agenda, limiting the influx of foreign capital (in the first half of February 2021 alone, the outflow of non-resident funds amounted to about 76 billion rubles). Against this background, the Bank of Russia began to review its monetary policy management tactics. At the first key rate meeting of 2021 on February 12, the regulator sharply “tightened” the rhetoric, which provoked new sales in the OFZ market. The Central Bank noted the presence of persistent inflation risks, the effects of which may last longer than initially expected. As a result, the inflation forecast for the current year was raised to 3.7-4.2%. The most important change in the regulator's statement was the disappearance of the signal about a possible rate reduction in the future. On the contrary, the Central Bank announced for the first time that it would assess the timing of the transition to a neutral policy (implying a key rate in the range of 5-6%), although in the base scenario it expects this no earlier than next year. Under the influence of all these factors, the ruble sovereign debt market could only continue to decline. OFZ yields have been growing rapidly since mid-January, while the scale of the sale has not yet diminished, despite the support of such traditional demand factors as rising oil prices and the strengthening of the ruble. The most serious losses were suffered by the middle section of the curve, where yields increased by 55-65 bps. In general, securities with maturities over 10 years are now at approximately the same level as in the first half of April 2021. At the same time, it is important to note that the key rate at that time was 6%, i.e. was higher by 175 bp. Thus, current spreads look much more attractive, which is an important argument in favor of buying these instruments. Also noteworthy is the sharply increased slope of the curve - the difference in rates is now at its maximum since the beginning of last year (spread 2-20Y) and exceeds 235 bp.

OFZ curve in dynamics

Source: MICEX, ITI Capital

Yield difference along the OFZ curve, bp

Source: MICEX, ITI Capital

OFZ with maximum coupon yield

Let me make a reservation right away: it is not always possible to say which OFZs have the highest coupon. On the one hand, a large percentage is given by long-term securities, but we do not know what inflation will be, i.e. how much the denomination will sink. On the other hand, OFZ-IN saves us from inflation. But their coupon is very small: only 2.5%.

It turns out that the rating of OFZ bonds by yield can only be compiled on the basis of specific bond issues. Let us analyze, for example, OFZ-PD.

| release | coupon, % per annum |

| Russia-2028-7t | 12,75 |

| 26218 | 8,50 |

| 26207 | 8,15 |

| 26219 | 7,75 |

| 26221 | 7,70 |

| 26205 | 7,60 |

| 26217 | 7,50 |

| 26220 | 7,40 |

| 26225 | 7,25 |

| 26222 | 7,10 |

| 26224 | 6,90 |

| 26214 | 6,40 |

In the case of OFZ-PK and OFZ-IN, it is quite difficult, if not impossible, to make a comparison in terms of profitability. Of course, we can guess about the amount of inflation and the Central Bank rate, but we cannot say for sure.

Important!

Variable coupon and index-linked bonds are not suitable for beginning investors. It is better for them to recommend OFZs with a constant income. Their coupon is about the same or a little less, but it is known in advance.

How to calculate OFZ yield: formula

You can calculate profitability using this simple formula:

D = N*K/2

Where:

- D is profitability;

- N – bond par value (1000 rubles);

- K – coupon size in % per annum.

To understand how to determine the profitability of OFZ, I will give a simple example. You bought 1 security for 1000 rubles with a 7% coupon. Then 1000*7% = 700 rubles. This amount must be divided in half, since coupon income is paid every six months. Therefore, during this period you will receive 700/2 = 350 rubles.

Where can I buy?

As stated above, to purchase OFZ-PD you need to arrange service with a broker company by opening a brokerage account . After this, access to the exchange is usually provided using the QUIK trading terminal. But many brokers have other ways to buy bonds. For example, through an application. Purchasing OFZ-PD is no different from purchasing other debt securities. The main thing is to calculate in advance the total cost of the bond along with the accumulated coupon income.

For example, let's look at the purchase process through QUIK. After setting up the bond table. The list of our securities is located in “MB FR: T+ Bonds” in the data source settings for the table. Double-click on the security you like to open the quote book (you can only buy it on a trading day when the exchange is open).

Find the security you like in the QUIK table and open the quote book

If you are ready to buy at the market price, then select the minimum price in the red column (the top one) - these are sell orders. But most often, it is more profitable to buy by placing your price in the green column of purchase orders.

Submit a purchase request and set the desired price

In this case, we simply set an adequate price that would suit you, and wait for someone to sell you OFZ-PD based on this application.

Advantages and disadvantages

Government bonds of all types have the following advantages:

the greatest reliability among all investment assets;- fixed income;

- high liquidity;

- possibility of inheritance;

- exemption of profits received from coupon payments from personal income tax.

OFZ-n, unlike other types of OFZ, are not an attractive instrument for experienced investors.

This is caused by the following disadvantages of this type of paper:

- regulated price;

- low profitability.

You can return the money invested in OFZ-n ahead of schedule only by contacting the bank where the purchase was made. At the same time, it will be possible to sell them at the same price at which they were purchased only if it does not exceed the face value.

Therefore, such an investment can serve as a tool for speculation. It will not be possible to benefit from rising bond prices, which is traditionally accompanied by a reduction in the key rate. However, this rule makes the risk of investing in OFZ-n minimal even compared to other types of government bonds.

Another disadvantage of OFZ-n is that they can only be purchased using a regular brokerage account. You cannot purchase this asset using an individual investment account and receive a tax deduction on the amount invested in it.

An important advantage of OFZ-n of the fourth issue compared to previous assets traded on the stock market is that no commission is charged for transactions performed with it.

Effective OFZ yield to maturity: what is it?

One of the advantages of bonds is that you receive coupon income not at the end of the term (as is the case with bank deposits), but every six months. Those. the money is withdrawn to your account, and then you can do with it as you please. And if you decide to invest (reinvest) the received amount in bonds, you will receive the greatest profit, which is called the effective yield of the OFZ.

Those. if you do not spend the income received, but immediately invest it in the purchase of new securities. In this case, you will probably be able to earn even more. Therefore, we can say that the most profitable OFZs are bonds with a reinvested coupon.