Published with the assistance of the International Financial Holding "FIBO Group, Ltd."

Scientific editor V. Bashkirova

Project manager O. Ravdanis

Proofreaders E. Aksenova, E. Chudinova

Computer layout A. Abramov

Design by V. Molodov

Art director S. Timonov

The cover design uses an image from the photo bank shutterstock.com

The Intelligent Investor – Revised Edition.

© 1973 by Benjamin Graham. New material

© 2003 by Jason Zweig. All rights reserved. Published by arrangement with HarperCollins Publishers.

There are also two acknowledgment lines for reprinted material: “The Superinvestors of Graham-and-Doddsville,” by Warren E. Buffett, from the Fall 1984 issue of Hermes, Magazine of Columbia Business School. Reprinted by permission of Hermes, Magazine of Columbia Business School, copyright © 1984 The Trustees of Columbia University and Warren E. Buffett.

“Benjamin Graham,” by Warren E. Buffett, from the November/December 1976 issue of Financial Analyst Journal. Reprinted by permission of Financial Analysts Federation.

© Publication in Russian, translation, design. Alpina Publisher LLC, 2014

* * *

Through vicissitudes everything

We strive through all trials...[1]

Virgil. Aeneid

The beginning of a smart investor

After graduating from Columbia University in 1914, Graham went to work on Wall Street. During his 15-year career, he was able to raise a large personal nest egg. Unfortunately, Graham, like many others, lost most of his money in the 1929 stock market crash and subsequent Great Depression.

This experience taught Graham lessons about minimizing downside risk by investing in companies whose shares were trading well below the companies' liquidation value. Simply put, his goal was to buy a dollar's worth of assets for $0.50. To do this, he used market psychology by exploiting market fears in his own interests. These ideals inspired him to write Security Analysis, which was published in 1934 with co-author David Dodd. The book was written in the early 1930s, when both authors were professors at Columbia Business School. Graham's methods for analyzing securities are described.

In Security Analysis, Graham's first task is to help stock market participants distinguish between investments and speculation. After careful analysis, it should be clear that the investment will protect the principal and provide adequate returns. Anything that does not meet these criteria is speculation. Graham also advocated a different view regarding share ownership; shares provide partial ownership of a business. For Graham, in the short term, the stock market acts as a voting machine, and in the long term, the stock market acts as a weighing machine, so in the long term, the true value will be reflected in the stock price. price.

Investors should always try to determine the value of the operating company behind a stock. Security analysis provides several examples where the market has undervalued certain stocks that were out of favor, which ultimately became an important opportunity for the savviest investors. These and other concepts in including "margin of safety" and "financial crisis period", helped lay the groundwork for Graham's later work in The Intelligent Investor and helped develop some of his key investment concepts.

Why is the book worth reading?

In his book, Graham focuses on techniques, principles of investing and investor behavior, emotions and important analytical mechanisms. On this page, click the link below to download the updated edition, complete with contemporary examples from Jason Zweig that illustrate the relevance of investing principles.

Quote from a book about long-term investing:

To have a reasonable chance of beating average stock market returns over time, an investor must pursue policies that are, first, clear and attractive, and, second, unpopular among stock market participants.

Quote from a book about choosing what to invest in:

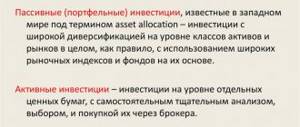

For a long time, real estate was considered a reliable long-term investment, guaranteed to be protected from inflation. Unfortunately, its cost also undergoes significant fluctuations: serious mistakes can be made in choosing the location, cost, etc.; Or buy into certain tricks of realtors. Finally, for the average investor, portfolio diversification is not practical except when it comes to different types of mutual investments and investing in new issues of securities, sometimes associated with special opportunities (which, in fact, is not much different from investing in stocks). .

What You Can Learn from a Smart Investor

Graham began teaching value investing as an investment approach at Columbia Business School in 1928 with David Dodd. In 1949, Graham and Dodd published The Intelligent Investor. Here are some of the key concepts from the book.

Mister Market

Graham's favorite allegory was that of Mr. Market.

This imaginary man, "Mr. Market", appears every day at the shareholder's office, offering to buy or sell his shares at a different price. Sometimes the prices offered make sense, but other times the prices offered are not realistic given current economic realities. Individual investors have the right to accept or reject Mr. Market's offers on any day, giving them an advantage over those who feel obligated to invest at any time, regardless of the security's current valuation. Investors are advised to focus on their companies' actual performance and dividends they receive, rather than paying attention to the changing sentiments of Mr. Market that determine the value of shares. An investor is neither right nor wrong if others share the same feelings as him; only facts and analysis can make them right.

Value investing

Value investing is about capturing the intrinsic value of a common stock regardless of its market price. Analyzing a company's assets, earnings and dividend payments can help determine a stock's intrinsic value, which can then be compared to its market price. If the intrinsic value exceeds the market value - in other words, the stock is undervalued in the market - the investor should buy and hold until mean reversion occurs. Mean reversion theory states that over time, the market price and the domestic price will converge. At this stage, the share price will reflect its true value.

Short review

Buy only stocks that sell for two-thirds of their NAV. Net-net is a value investing method developed by Benjamin Graham that values a company based solely on its net current assets.

When an investor buys a stock below its intrinsic value, they are essentially buying it at a discount. Once the stock is actually trading at its intrinsic value, they should sell.

Margin of safety

Graham also advocated an approach to investing that provides a margin of safety—or room for human error—for the investor. There are several ways to achieve this, but the most important is to buy undervalued or unwanted stocks. Investor irrationality, inability to predict the future, and stock market fluctuations can provide investors with a margin of safety. Investors can also provide a margin of safety by diversifying their portfolios and buying shares of companies with high dividend yields and low debt-to-equity ratios. This margin of safety is intended to reduce the investor's losses if the company goes bankrupt.

Benjamin Graham Formula

Typically, Graham only bought stocks that traded at two-thirds of their NAV as a way to establish his margin of safety. Net net worth is another value investing method developed by Graham that values a company based solely on its net current assets.

Benjamin Graham's original formula for determining the intrinsic value of a stock was:

Graham later revised his formula to include both the risk-free rate of 4.4% (the average yield on high-grade corporate bonds in 1962) and the current yield on AAA corporate bonds, represented by the letter Y:

Dividend shares

Many of Graham's investment principles are timeless—they remain as relevant today as when he wrote them. Graham criticized corporations for their unclear and irregular financial reporting practices, which made it difficult for investors to get an accurate picture of a company's health. Graham would later write a book on how to interpret financial statements, from balance sheets and income statements to financial ratios. Graham also advocated for companies to pay dividends to their shareholders rather than keeping all their profits as retained earnings.

Benjamin Graham (1896–1976)

When Benjamin Graham was about 80 years old, he told one of his friends that he wanted to do something stupid every day, create something new, and be generous.

This original formulation of life's purpose testifies to the amazing ability to express one's thoughts simply and modestly, in a very delicate manner, without moralizing or falling into a mentoring tone.

Those who have read Graham are well aware of how innovative his ideas were. It is not often that students and followers fail to surpass the teacher and author of a new theory. But today, 40 years after the publication of the book that brought a logical and systematic explanation to such a messy and confusing field as investing, it is unlikely that any securities analyst can compare with Graham. In a field where ideas become obsolete within months, Benjamin Graham's principles remain unshakable. Moreover, in times of financial turmoil that sweep away other, shakier logical structures, the value of these principles only grows and becomes even more obvious. Graham's advice always helps those who follow it, and allows even less able investors to outperform their more gifted brethren, who often make mistakes because they follow the instructions of fashionable and popular experts.

Oddly enough, Graham's authority as an investor was not at all the result of a deliberate concentration of mental effort on solving a single problem. Graham was not a narrow professional. Rather, he was a thinker in a broad sense, and his theory was a kind of "by-product" of a powerful intellect - an intellect that no one I knew possessed. He remembered literally everything, was obsessed with a thirst for new knowledge and knew how to use it to solve problems that, at first glance, belonged to completely different areas. Whatever he was talking about, following the flight of his thoughts was a real pleasure.

Graham had one more quality that set him apart from the crowd. I'm talking about generosity. For me he was a teacher, employer and friend. No matter who he had to deal with - students, subordinates, friends - he always behaved absolutely openly, freely shared his thoughts, sparing neither time nor effort for people. Do you want to figure something out? Go to Ben. Need support or advice? Ben will definitely help.

Walter Lippmann [2] spoke with admiration of people who plant trees in the shade of which other people will rest. Ben Graham was just such a man.

Financial Analysts Journal,

November–December 1976

The Intelligent Investor and Warren Buffett

Of The Intelligent Investor, legendary investor Warren Buffett, whom Graham made famous, called it "by far the best book on investing ever written." In fact, after reading it at age 19, Buffett went to Columbia Business School to study under Graham, with whom he became a lifelong friend. He later worked for Graham at his investment company, Graham-Newman Corporation, until Graham retired.

$25,250

The price of a signed Warren Buffett copy of The Smart Investor sold at auction in 2010.

All of Graham's students eventually developed their own strategies and philosophies, but they all shared the core principle of building a margin of safety.

In general, Buffett follows the principles of value investing, which looks for securities that are priced unreasonably low based on their intrinsic value. Buffett also considers a company's performance, debt, profit margins, whether companies are public, how dependent they are on commodities and how cheap they are.

capital gains. Rather, his goal is to own quality companies that are eminently capable of generating profits; Buffett doesn't care if the stock market ever recognizes the value of a company. Despite this, Buffett said that no one has ever lost money following the methods Graham.

Ideas and quotes

1. Separate investment and speculative accounts. Speculative ideas and investments should not be mixed. This fact applies not only to the trading account, but also to thinking, because these are completely different directions. It is difficult to watch an investment deal hang around for several months without changes. Unlike speculative ones, which are constantly up and down.

2. Nobody knows when the stock market will start to fall or rise. There are too many active forces in the market that push it in different directions. Therefore, one should not blindly trust analysts; many economically significant events happen in the world every day, and even supercomputers cannot yet calculate the consequences of each.

3. The author offers the legendary “investment formula”. Buy assets every month for the same amount. This is a great way to gain a position at an average price and at the same time not bite your elbows by buying expensively for the whole cutlet at once.

4. Portfolio diversification. Distribute investments between the stock and foreign exchange markets. No one cancels crisis periods, during which a reasonable investor shifts most of the portfolio into bonds or other less risky securities (it is useful to track the yield on 2 and 10 year US bonds). It is worth considering safe haven assets: gold, cryptocurrency.

5. Look at the P/E ratio. Shows how many years the return of capital due to dividends will be. For example, the Apple company. The stock price is $200, earnings per share (EPS) are $11.93, which means P/E = 16.76. This means that if you buy a share and the price does not rise, you will receive 100% income from it only after 17 years. The task of a smart investor is to find reliable companies and preferably with a small P/E value. In life, everything is different, over the past 5 years, Apple's price has increased 2.5 times and this is a company with growth shares, so the P/E ratio is given less importance here.

To analyze the history of dividend payments and profitability, I recommend using the website dividend.com

Intelligent Investor: Frequently Asked Questions

What does being a smart investor teach you?

The Intelligent Investor is widely considered the definitive text on value investing. Graham said investors should analyze a company's financial statements and operations, but ignore market noise. The whims of investors - their greed and fear - are what create this noise and fuel daily market sentiment.

Most importantly, investors should look for price-value discrepancies when a stock's market price is less than its intrinsic value. Once these opportunities are identified, investors should make a purchase. Once the market price and intrinsic value match, investors should sell.

The Intelligent Investor also advises investors to keep a portfolio of 50% stocks and 50% bonds or cash to avoid the pitfalls of day trading, to take advantage of market swings and market volatility, to avoid buying stocks just when they are trendy, and to look for ways to which companies can manipulate their accounting practices to inflate the value of earnings per share.

Is the smart investor suitable for beginners?

The Smart Investor is a great book for beginners, especially since it has been continually updated and revised since its original publication in 1949. It is considered a must for new investors who are trying to understand the basics of how the market works. The book is written for long-term investors. For those interested in something more glamorous and potentially more fashionable, this book may not appeal to you. He gives a lot of common sense advice on how to make short-term profits through day trading or other commonly used trading strategies.

Is “The Smart Investor” Outdated?

Even though this book is over 70 years old, it is still relevant. The advice to buy with a margin of safety is as sound today as it was when Graham first taught his philosophy. Investors should do their homework (research, research, research) and, once they have determined what a company is worth, buy it at a price that will provide them with support if prices fall.

Graham's advice that investors should always be prepared for volatility also remains very relevant.

What type of book is right for the smart investor?

First published in 1949, The Intelligent Investor is a well-known book on value investing. Value investing is designed to protect investors from significant harm and teaches them to develop long-term strategies. The Smart Investor is a practical book; he teaches readers to apply Graham's principles.

How can I become a smart investor?

Benjamin Graham encourages anyone who wants to succeed as an investor to adhere to the twin principles of judgment and patience. To determine the true value of a company, you must be willing to do the research. Then, once you buy shares of a company, you must be prepared to wait until the market realizes it is undervalued and bids its price higher. If you only buy companies that are trading below their true value or intrinsic value, even when the business is suffering, the investor has a cushion. This is called a margin of safety and is the key to investing success.

Jason Zweig Thanks

I express my heartfelt gratitude to everyone who helped prepare the new edition of Benjamin Graham's book. This is Edwin Tan (HarperCollings), whose support and inexhaustible energy helped bring the project to fruition. Money magazine

– Robert Safyan, Denis Martin and Eric Gelman, who actively, patiently and unselfishly helped me.

This is my wonderful literary agent, John Wright, and the tireless Tara Kalvarski of Money

.

These are Theodore Aronson, Kevin Johnson, Martha Ortiz and other employees of the investment consulting firm Aronson + Johnson + Oritz, who made a number of valuable comments and suggestions. I am also grateful to Peter L. Bernstein Corporation President Peter Bernstein, William Bernstein (Efficient Frontier Advisors), John Bogle (founder of Vanguard Group), Charles Ellis (co-founder of Greenwich Associates), and Lawrence Siegel (Director of Investment Policy Research at the Fond Foundation). I am deeply grateful to Warren Buffett and Nina Munk, as well as the tireless employees of Time Inc. Business Information Research Center; FridsonVision LLC CEO Martin Fridson; President of the Center for Financial Research & Analysis Howard Shilit; Inside Information

editor and publisher Robert Veres; Daniel Fuss (Loomis Sayles & Co), Barry Nelson (Advent Capital Management); employees of the Museum of Financial History of the United States; Brian Mattes and Gus Sauter (Vanguard Group); James Seidel (RIA Thomson); Samilla Artamura and Sean McLaughlin (Lipper); Alex Auerbach (Ibbotson Associates); Anette Darson (Morningstar); Jason Bram (Federal Reserve Bank of New York) and one investment fund manager who wishes to remain anonymous.

But most of all I am grateful to my wife and daughters, who suffered for so long because I worked day and night. Without their love and patience I would not have been able to do anything.

The essence

While details of Graham's specific investments are not available, he has reportedly averaged about 20% annual returns over his years of money management. His method of buying stocks with low risk and high return potential made him a true pioneer in the field of financial analysis, and many other successful value investors have his methodology to thank.

Although he is best known for the books he published in the field of value investing, most notably The Intelligent Investor, Graham was also instrumental in developing elements of the Securities Act of 1933, a law requiring companies to provide financial statements certified by independent accountants.