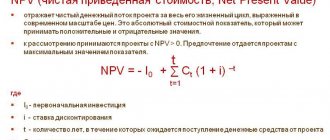

Net cash flow is a quantity widely used in financial and investment analysis to determine the remaining funds after deducting all expenses. In simple terms, net cash flow is the difference between money coming in and money going out.

Net cash flow is easy to calculate from the balance sheet, but it is preferable to use management reporting data, where all the company’s actual costs are deciphered. Today we will analyze two methods of calculating it - direct and indirect, and give examples of analysis using the NPV indicator.

What is net cash flow

So, net cash flow is an indicator calculated as the difference between income and expenses calculated using the “cash method”. I already mentioned once that net cash flow does not depend on the amount of accrued depreciation, because... accrued depreciation of assets does not affect their market value and does not require the expenditure of “real” money, therefore this cost item does not participate in the calculation of NCF.

It is immediately necessary to clarify the following. The legislation provides for the calculation of profit “by shipment”, i.e. Revenue accounted for on the balance sheet is the amount of goods shipped or services actually rendered. The sales amount does not depend on whether these goods (services) are paid for or not. It is from this amount that expenses are subtracted and the financial result is formed.

There is, of course, a small percentage of enterprises that consider profits on a “cash basis”, i.e. how much money was received into the cash register or bank account and how much was spent. But such companies belong to micro-enterprises; they, as a rule, exist autonomously, without attracting external investors.

As for medium and large companies, revenue is always accounted for by shipment. Let’s figure out how to link this with the concept of net cash flow (NCF). First, let's look at the structure of the NPV.

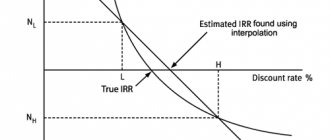

Discounting cash flows: what and why...

However, due to the fact that investment projects are often quite lengthy, they cannot but be subject to inflation.

Inflation is inherent in any country and affects the depreciation of the money supply. Consequently, cash flows are also depreciated due to inflation. And with 1000 rubles in 5 years, the investor will be able to buy much fewer goods.

Therefore, for a more accurate assessment of the effectiveness of investments, taking into account the time factor, it is customary to discount the project flows. To do this, you need to use a discount rate (rate of return).

In particular, by determining such indicators as: net present flow (NPV, NPV) , discounted payback period (Current, DPB), discounted profitability index (ID, DPI) , etc. or net income (NH, NV) , payback period (Current, PB), profitability index (ID, PI) , etc.

Components of net cash flow

So, NCF includes the following components, or cash flows (CF):

- DP from operating activities (Operation Cash Flow). This is the largest component of the NPV structure, because Any enterprise is aimed at making a profit primarily from current or operating activities. The OCF includes:

- receipt of money from customers;

- payments to suppliers;

- rent;

- wages and contributions to the budget;

- current expenses (transport, business expenses, storage of goods, advertising, etc.).

Thus, OCF is profit from operating activities calculated on a cash basis.

- DP from financial activities (Financial Cash Flow) includes payments for receipt and repayment of loans and interest on them, payment of dividends and other expenses made from net profit. In other words, FCF changes the structure of equity and debt capital.

- DP from investment activities (Investing Cash Flow) is an enterprise’s investments: placement of funds on deposits, income and expenses for the acquisition of securities of other companies, receipt of dividends and interest on these securities. ICF also includes any operations with fixed assets: acquisition, modernization, sale and payment of interest on loans issued for the acquisition of non-current assets.

So, net cash flow is equal to the sum of these three components - NCF, OCF and FCF.

Free Cash Flow. What is it and how to count it

Almost all companies in their presentation of financial results for the reporting period indicate such an important indicator as “free cash flow”. Understanding how it is calculated and what it is used for is essential for every investor.

What is FCF

By definition, FCF (Free Cash Flow) is the cash for a certain period that a company has after investing in maintaining or expanding its asset base (Capex). It is a measurement of a company's financial performance and health.

There are two types of free cash flow: free cash flow to the firm (FCFF) and free cash flow to shareholders (FCFE).

Free cash flow (FCF) is the cash flow available to all investors in a company, including shareholders and creditors.

This indicator is not a standardized accounting indicator, i.e. you won't be able to find it in the company's reporting. Company management can calculate FCF separately and uses it to visualize the company's financial position. Most often, the calculated FCF can be found in a company presentation, press release, or management's analysis of the company's financial condition and results of operations (MD&A).

There are 3 main methods for calculating FCF

The choice of calculation method depends on how deeply you want to analyze the company’s cash flows and on what data the indicator is calculated (historical or forecast).

Method 1 is the simplest, designed for the initial assessment of the company’s cash flows based on actual data:

FCF = Net cash flows provided by operating activities - capital expenditures (Capex).

That is, from the money received during the period from core activities, we subtract capital costs for maintaining or expanding production.

Let's calculate free cash flow for the first quarter of 2021 using an example.

We can take all the calculation values from the company's cash flow statement.

We can find capital expenditures in the investment activity report. In this case, they consist of two articles - Acquisition of fixed assets + acquisition of intangible assets.

(The figure corresponding to the line in the reporting above is signed in brackets).

Method 2 is more complex, which reveals in more detail the reasons for changes in free cash flow:

FCF = EBITDA - income tax paid - capital costs (Capex) - changes in working capital (NWC, Net working capital change)

That is, we clear the “dirty indicator” of cash flow (EBITDA) from taxes and changes in working capital. Please note that the calculation takes into account the actual income taxes paid, which are reflected in the company’s cash flow statement. This is due to the fact that FCF shows real money that remains in the company, while paid and paper taxes can diverge several times.

In terms of change in working capital, a company must maintain net current assets each period to carry on its operating activities. If it wants to increase revenue, it will be forced to increase working capital, which in turn requires raising additional cash from operating flow to purchase additional assets.

The change in working capital is also taken from the statement of cash flows, however, companies do not always report it there. Then we can calculate NWC change independently from the company’s balance sheet, by calculating changes in current assets and liabilities relative to the previous period.

Calculation of FCF in the second way for:

The result was greater than in the first case. Don't forget that EBITDA may contain non-cash items for which free cash flow must be adjusted.

Method 3 is similar to the second method, but is used for forecasting purposes:

FCF = EBIT*(1-tax) + depreciation - capital costs - changes in working capital

This method differs from the previous one solely by taking into account taxes. Since it is used for forecasting purposes, we do not know what taxes actually paid will be. Then the method uses the effective average tax rate (tax), calculated on historical data.

The listed formulas are basic formulas in the classical sense. In practice, the FCF calculation is adjusted for non-recurring or non-cash items. Examples include deductions related to contributions to a company pension fund, or the purchase of other businesses (which are not part of capital expenditures).

Thus, for each company it is necessary to modernize the standard formulas to take into account all aspects related to the company, as well as country or industry characteristics.

In the presentation you can find a detailed calculation of the FCF indicator:

Company management deviates from the classic formula and deducts interest paid, as well as other adjustments. So in a theoretical sense, it's more like the FCFE metric, which we'll talk about next.

Why do we need FCF?

Now let's figure out why everyone needs this FCF indicator so much and why most Western companies tie dividend payments to it.

Free cash flow reflects the amount of money a company earns from operating activities. Unlike profit, FCF shows how much a company can generate cash flows (excludes paper income), which can be used for the following purposes:

1. Payment of dividends

2. Buyback of shares from the exchange (Buyback)

3. Paying off debt

4. M&A transactions, purchase of non-core assets

5. Saving money on your balance sheet

Let us remind you that one of the ways to estimate the fair value of a company is the DCF model (discounted future cash flows of the company). That is, FCF and its dynamics determine the market value of the company's shares, since the more significant the cash flows, the more reasons investors have to expect larger dividends (there are exceptions).

However, many companies stick to the latter option because they are afraid that if they start increasing dividend payments, they will soon face liquidity problems.

Do not think that FCF is a Western indicator that is not suitable for Russian realities. It is conceptual and its meaning is not lost under any circumstances. However, if the company reports only according to RAS, it will be much more difficult to calculate it.

FCFE (Free cash flow to equity) indicator

FCFE is a type of free cash flow that shows how much of the FCF goes to shareholders. This value is a rather conditional estimate, since shareholders receive only dividends.

The main difference between FCFF and FCFE is that the lender's portion of the money is deducted from the FCFF. The formula for this indicator is as follows:

FCFE = FCF - interest paid - (debt repaid for the period - debt issued for the period)

That is, if a company has increased debt over a period, then it has increased free cash flow, which shareholders can dispose of. The FCFE indicator shows the amount of money for a period that shareholders can use for their needs (payment of dividends, buyback) without harming the company's operating activities.

We can also find the interest paid in the cash flow statement. The change in debt is either in the financial activity section of the general income tax balance, or is reflected as a change in total debt from the company’s balance sheet to the previous period.

For the FCFE indicator is equal to:

However, free cash flow attributable to shareholders has its drawbacks:

1. FCFE is much more volatile over time, and therefore less predictable in financial modeling.

2. The change in debt over the period has a great influence on the FCFE indicator. The problem is that most often a company cannot use debt for any purpose (except for lines of credit). Typically, there are strict conditions that limit company management from using raised money, for example, to pay dividends. Otherwise, creditors have veto power.

Although the FCFE indicator is more theoretical, it is also useful as FCFF for analyzing the financial performance of a company.

Open an account

BCS Broker

For whom is NCF calculated?

Who needs to calculate net cash flow? The answer is simple - to all interested parties, namely:

- company owners, senior managers;

- investors;

- creditors, incl. banks when considering a loan application;

- competitors (for comparative analysis purposes);

- tax authorities (to obtain detailed information on the movement of funds in current accounts).

The organization's net cash flow is clearly presented in the “Cash Flow Statement” appendix to the balance sheet. This form is submitted to the tax authority once a year by all legal entities, with the exception of small businesses.

Cash flow statement ratios.

The cash flow statement contains information that can be analyzed over time (that is, changes over time) to gain a better understanding of a company's past performance and its future prospects.

This information can also be used effectively to compare the performance and prospects of different companies within the same industry, as well as across different industries.

There are several generally accepted ratios based on cash flow from operating activities that can be useful in this analysis. These ratios are usually categorized as 'performance / profitability ratios' and 'coverage / solvency ratios' for cash flow .

See also:

CFA - Financial Ratio Analysis.

Figure 16 summarizes the calculation and interpretation of some of these coefficients.

Illustration 16. Cash flow statement ratios.

Profitability ratios

| Index | Formula | Economic meaning of the indicator |

| Cash flow to revenue | CFO/Net Revenue | Operating cash flow received for each unit. revenue |

| Cash return on assets | CFO/Average Total Assets | Operating cash flow received for each unit. investment in assets |

| Cash flow to equity | CFO / Average equity (shareholder) capital | Operating cash flow received for each unit. investments of company owners |

| Cash flow to operating profit (Cash to income) | CFO / Operating profit | A company's ability to generate cash flows from profits generated from operating activities |

| Cash flow per share a | (CFO - Dividends on preferred shares) / Number of common shares outstanding | Operating cash flow per 1 ordinary share |

Coverage or Solvency Ratios

| Index | Formula | Economic meaning of the indicator |

| Debt coverage ratio | CFO/Total Debt Obligations | Level of financial risk and financial leverage |

| Interest coverage coefficient b (Interest coverage) | (CFO + Interest paid + Taxes paid) / Interest paid | Ability to meet interest repayment obligations |

| Reinvestment ratio | CFO / Payments for (investments in) non-current assets | Ability to acquire fixed assets and other non-current assets using operating cash flow |

| Debt payment ratio | CFO / Payments to repay long-term debt obligations | Ability to repay long-term debt obligations through operating cash flow |

| Dividend payment ratio | CFO / Dividend payments | Ability to pay dividends from operating cash flow |

| Investing and financing ratio | CFO / Cash outflows from investing and financing activities | The ability to acquire non-current assets, pay off debts and pay dividends. |

Notes:

a If a company reports under IFRS and includes dividends paid in the operating activities section of the statement of cash flows, then the total dividends reported must be added to CFO and then subtracted dividends on preference shares.

Let us remind you that CFO in cash flow statements prepared in accordance with US GAAP and IFRS may differ due to the reflection of interest and dividends received and paid in different sections.

See also more details from this:

CFA - Preparation of the Cash Flow Statement (Part 1): Relationship to the Balance Sheet and Operating Activities.

b If a company reports in accordance with IFRS and includes interest payments in the financing activities section, then interest payments must be excluded from the numerator.

Types of cash flows

There are several classifications of types of DP. We have already discussed one of them (by area of activity): NCF is the sum of net cash flows from current, financial and investing activities. How else are NCFs classified?

- In relation to the company's activities, DPs are divided into internal and external. Internal DPs are the movement of funds within a company (holding), while external ones, accordingly, reflect mutual settlements with counterparties.

- Based on the direction of movement, flows are divided into positive and negative. In simple words, positive DPs are revenues, and negative DPs are cash expenditures.

- By volume, DPs are classified as excessive, sufficient or deficient. An excess of funds indicates that the company has poorly developed investment activities and steps should be taken to ensure that the money works and is not eaten up by inflation. For example, place funds on deposit or purchase securities of another company.

Cash flows from the main activities of the enterprise

Cash flows of an enterprise in its core activities represent their receipt and use, ensuring the functioning of the enterprise (production, trade, services, etc.). The main source of profit of an enterprise is its main activity, which should also be the main source of cash receipts.

Most taxes are calculated on cash proceeds from the sale of inventory (work performed, services rendered). If sales revenue does not dominate the incoming cash flow, then you should think about what type of activity of the enterprise should be considered the main one.

In most cases, the next most important source of cash flow is the payment of receivables in cash. This is not surprising, because the amounts after repayment of this debt turn into sales proceeds.

Another source of cash receipts for the main type of activity is advances (prepayments) received from buyers and customers for inventory items (work performed, services rendered).

What kind of cash flows for core activities do the enterprise have?

The main direction of spending funds of any organization is payment to suppliers and contractors for inventory items (works, services) purchased from them. Production is, in principle, impossible without raw materials. The same goes for trading: in order to sell something, you must first buy it. Enterprises performing work and providing services purchase equipment, consumables, tools, etc. from suppliers.

The next most important area of spending money for core activities is the payment of wages to employees of the enterprise. Here, too, everything is clear: without labor resources, it is impossible to carry out any activity, as well as without raw materials, materials, purchased products and goods, obtaining external services, etc.

Payments to the budget and extra-budgetary funds occupy an important place in the structure of spending money. Some of them directly depend on the amount of accrued wages (we are talking about payments, the amounts of which are calculated from the wage fund).

If an enterprise uses loans, then one of the cash flows is the payment of interest for the use of these funds. Expenses for this item are relatively easy to plan: the amount of interest that a company must periodically pay is usually calculated in advance, when applying for a loan or immediately thereafter.

Another area of spending money that relates to the main activity of the enterprise is contributions to the social sphere (sick leave payments, maternity leave, etc.)

Formula for calculating net cash flow

Now let's talk about how to calculate net cash flow. There are two formulas for calculating this indicator. The general NCF formula looks like this:

\[ NCF=\displaystyle\sum_{i=1}^{n} (CFI_i – CFO_i),where: \]

\( CFI \) – incoming cash flows;

\( CFO \) – outgoing DS flows;

\( i \) – period number;

\( n \) – number of periods.

Let's assume we need to calculate NCF for 2 years. Let's take the initial data from the table:

| Period | DS received, thousand rubles. | DS sent, thousand rubles. |

| Year 1 | 1000000 | 800000 |

| Year 2 | 2000000 | 1650000 |

\[ NCF = (1000000 – 800000) + (2000000 – 1650000) = 550000 thousand rubles. \]

This formula is used if you want to calculate net cash flow without breaking it down by activity. And if you need to draw up a report on the movement of capital, the formula for calculating the NPV on the balance sheet is used:

\[ NCF = CFO + CFF + CFI, where: \]

\( CFO \) – DP – from current activities;

\( CFF \) – DP from financial activities;

\( CFI \) – DP from investments.

Each of the components of this formula is calculated using the algorithm given above.

FCFF (Free Cash Flow to the Firm) indicator

The “Free Cash Flow to the Firm” (FCFF) indicator literally translates as “free cash flow of a firm” - this is cash flow minus taxes and net investments in fixed and working capital.

The formula for a firm's free cash flow is:

FCFF = EBITDA × (1-Tax) + DA - CNWC - CAPEX

Where:

- Tax — income tax rate;

- EBITDA - earnings before interest and tax;

- DA - depreciation of tangible and intangible assets (Depreciation & Amortization);

- CNWC - change in net working capital;

- CAPEX - capital expenditures (Capital Expenditure);

Cash flow can be calculated using the following types of prices:

- Current;

- Forecast (take into account inflation and forecast of production levels and other factors);

- Deflated (taking into account inflation at current prices);

Discounting Cash flow

Since money depreciates every year, the cash flow today is not as solvent as tomorrow. To make adjustments to the future value of money, a cash flow discount factor is used:

CF = 1/(1 + DS) × Time

Where:

- DS – discount rate;

- Time – time period;

I recommend checking out:

- Discount rate - formula;

Calculation methods

There are two methods for calculating NCF - direct and indirect. Direct is used when drawing up a report on the movement of capital and characterizes the state of working capital on the company's current accounts. In other words, the direct method is reminiscent of calculating profit using the cash method. To make it more clear, let me explain: when planning personal finances, the direct method is used - you count how much money you received and how much you spent. The remainder will be equal to your personal NCF. You can include this money in next month's expenses, put it aside for a rainy day, or invest it. If you do not intend to spend these funds, they will be called free cash flow.

The indirect method is consistent with modern financial reporting standards and allows you to obtain more detailed information about the volume of free cash flows and the structure of their cash flow items. With the indirect method, NCF is calculated based on net profit adjusted by certain amounts. We know that net profit is an indicator in monetary terms, representing the balance of funds after the fulfillment of all obligations. This amount is distributed at the discretion of the company's owners: it can be used to increase equity capital, or it can be spent on something useful or paid income to persons who have shares in the authorized capital.

Next, we will analyze each method in more detail.

Direct method for calculating NPV

To find net cash flow using the direct method, it is enough to use accounting registers:

- cash book;

- bank statements;

- balance sheets and analyzes of cash accounts by items of movement.

What is Cash flow in simple words

Cash flow (from the English “Cash flow” - “cash flow”) is the totality of cash in a company, which includes all inflows (profit) and outflows (costs). Compiled according to approved form No. 4 (form code according to OKUD 0710004).

To determine a company's performance, cash flow can provide a lot of useful data for investors. The most commonly used simple indicator is “net cash flow”:

Net cash flow (from the English “Net Cash Flow”, NCF) is the difference between receipts and expenses in a particular period. This value can be either positive or negative.

Net cash flow formula:

NCF = ∑CFi+ - ∑CFj-

Where:

- CFi+ - receipts to the company’s account;

- CFj- — debits from the company’s account;

A positive NCF value means that the company is doing well: there is free money, which means the business is working in plus.

Well-known investor Warren Buffett considers the Cash Flow indicator to be one of the key indicators when evaluating a company's shares.

- Free Cash Flow - what is it;

Estimation of NCF indicator values

Net cash flow refers to the difference between funds received and funds spent. To characterize a company or project as an attractive direction for cooperation or investment, this value must be positive. The larger it is, the higher the degree of trust in the enterprise on the part of creditors, current and potential investors.

If the NCF is negative, then the company is experiencing a shortage of funds. Cooperation, investments or loans will most likely be refused.

When performing a comparative analysis of several companies or projects, the NCF value plays an important role. Most likely, a project with a higher NCF will be preferable for any type of placement of funds - be it a loan, investment or shipment of goods with deferred payment.

How to calculate cash flow from core activities

To calculate various types of cash flows, two methods are usually used: direct and indirect. The difference between them lies in a number of parameters, including initial data on the movement of money through the company’s accounts. The items considered in finding operating cash flow include items that are not included in the calculation of profit, such as depreciation, taxes, capital expenditures, advances, borrowings, debts, and penalties.

The direct method is based on studying the movement of finances through the company's accounts. It makes it possible to study the main directions of outflow and sources of inflow of money, analyze flows for various types of activities and the mutual relationship between revenue for a certain period and sales of products.

Operating cash flow is calculated using the direct method using the following formula:

NDP(OD) = B + AVP + PP - OT - SM - DRIVE - NALPL

wherein:

- B – the amount of revenue from the sale of products, services or work;

- AVP – advances transferred by customers and buyers;

- PP – other receipts from customers and buyers;

- SM – funds used to purchase material assets for organizing production;

- NAPL – taxes paid and contributions to various extra-budgetary funds;

- Labor costs are money spent on staff salaries;

- PRVOD – other payments that may arise in the course of the main activity.

Let's try to calculate the cash flow from the internal activities of the enterprise, based on the following inputs (all indicators in rubles):

- revenue from products sold – 1 million;

- advances from buyers - 100 thousand;

- other receipts from customers - 40 thousand;

- wage fund – 100 thousand;

- costs of raw materials and maintenance of the production process - 400 thousand;

- fees and taxes – 250 thousand;

- other expenses - 70 thousand.

NPV(OD) = 1,000,000 + 100,000 + 40,000 - 100,000 - 400,000 - 250,000 - 70,000 = 1,140,000 - 820,000 = 320,000 rubles.

With the indirect calculation method, the data from the balance sheet and the financial statements are taken as the basis. The calculation is performed by type of economic activity, and the relationship between changes in the value of assets for a certain period and net profit is clarified.

Calculation by the indirect method can be demonstrated using the following formula:

NDP(OD) = NPR(OD) + AM + ΔKRZ + ΔDBZ + ΔZAP + ΔDBP + ΔFV + ΔAVP + ΔABB + ΔRPP + ΔRBP

Where:

- NPR(OD) – net profit from internal activities;

- AM – wear and amortization;

as well as a number of changes indicated by the Δ sign, relative to:

- Δ KRZ – amount of accounts payable;

- Δ DBZ – amount of accounts receivable;

- Δ ZAP – inventory values;

- Δ DBP – income expected in future periods;

- Δ FV – financial investments;

- Δ WUA – advances received;

- Δ АВВ – advances issued;

- Δ RPP – reserve for payment of payments and expenses in the next period;

- Δ RBP – expenses for upcoming periods.

Let's predict the accounting report indicators for the previously mentioned enterprise (in thousands of rubles) and find the operating flow using the indirect method:

- undivided profit – (+) 400;

- depreciation and wear – (+) 100;

- creditor – (+) 150;

- receivable – (-) 120;

- stock dynamics – (-) 60;

- future income – (+) 130;

- financial investments (-) 90;

- advances received – (+) 30;

- advances issued – (-) 70;

- reserves – (-) 180;

- upcoming expenses – (-) 110.

NPV(OD) = 400 + 100 + 150 – 120 – 60 + 130 – 90 + 30 – 70 – 180 – 110 = 180.

Consequently, the cash flow from the main activities of the company, calculated by the indirect method, is 180 thousand rubles.

How is cash flow analysis performed?

The direct method of calculating NPV allows you to assess whether the company has enough working capital. Perhaps, to do this, it is enough just to calculate the net cash flow from operating activities using the classic formula given above for the reporting period. If the NCF is negative or close to zero, this means that the company does not have enough money. In the near future, there is a high risk that there will be delays in the payment of wages, delays in paying taxes and, as a result, the likelihood of bankruptcy will increase.

As for the indirect method, it is necessary for a more detailed study of the structure of net profit. Having identified the difference between retained earnings and NPV, it is not difficult to understand where the money goes. Or why, despite a large amount of funds, the company has a low financial result based on the results of its activities. This situation is possible with long-term projects: buyers make an advance payment, and the proceeds from sales will be reflected later. In this case, competent cost management is necessary.

The net cash flow from investing activities is subject to comparison with the discounted cash flow at a certain point in time. This is necessary to calculate the payback period of investments and calculate the return on investment. Read more in the article “Discounting Cash Flows”.

Formula for calculating Free Cash Flow - 3 options

There are three ways to calculate free cash flow. All data is taken from the company’s standard reporting according to RAS or IFRS.

Free Cash Flow formulas:

Option #1

FCF = [Operating Cash Flow] - [Capex] Free Cash Flow = - [Capital Expenditures]

Option No. 2

FCF = EBITDA - [Income tax paid] - [Capex (Capex)] - [Changes in working capital (NWC, Net working capital change)]

Option #3

FCF = EBIT*(1 - Taxes) + [Depreciation] - [Capital Expenditures] - [Changes in Working Capital]

Note One-time proceeds from sales are not included in the calculation. They are indicated in the reporting documents in a separate section “Cash flow from investment activities”.

Future value of the company

Free Cash Flow is one of the ways to assess the future capitalization of a company. This model is based on discounting the company's future cash flows. The idea is that a positive FCF allows stockholders to expect future dividends.

- How to live on dividends;

- How to make money on stocks;

- Dividends on Russian shares - yield and size;

Example calculation in Excel

First, we will calculate net cash flow using the direct method. The initial data is taken from the report on the movement of DDS, compiled on an accrual basis from the beginning of the year.

| Operation | Investing | Financial | |

| CFI | 620256 | 35 | 2370 |

| CFO | 382382 | 47 | 165 |

| CF | 237874 | -12 | 2205 |

| Cf(total) | 240067 |

In the report, the results of cash receipts are highlighted in green, and payments are highlighted in red. The calculation results for all NCFs are marked in yellow.

Line 4400 reflects the final NCF value, which was obtained by summing lines 4100, 4200 and 4300.

In the table below, the same values are calculated using formulas in Excel.

Net cash flow is determined by the indirect method as the amount of net profit adjusted for depreciation and changes in certain lines on the balance sheet. Let's present the initial data in the table and calculate NCF using the formula:

\[ NDP = PE + A + ΔDZ + ΔTMC + ΔKZ + ΔFV + ΔAV + ΔAP + ΔDBP + ΔRBP + ΔRF, where: \]

| 31.12.2020 | 31.12.2019 | Change | |

| Net profit | 17115 | X | |

| Depreciation | 43 | X | |

| Accounts receivable | 30569 | 39701 | -9132 |

| Reserves | 34077 | 33460 | 617 |

| Accounts payable | 42665 | 48802 | -6137 |

| Financial investments | — | — | — |

| Advances received | 412 | 235 | 177 |

| Advances issued | 1552 | 658 | 894 |

| revenue of the future periods | — | — | — |

| Future expenses | 5481 | 4337 | 1144 |

| Reserve Fund | 1080 | 1350 | -270 |

| NCF | 4451 | ||

In both cases the value turned out to be positive. Now let’s do a little comparative analysis using the data from the second example - what determines the difference between net profit and NPV?

Firstly, during the reporting year, accounts receivable and payable decreased, and, consequently, the balance sheet currency. The main reasons may be:

- a drop in sales and, as a consequence, a reduction in working capital;

- changing the terms of contracts: reducing deferred payments, using factoring.

What influences Cash flow

There are external and internal factors that ultimately influence the results of cash flow calculations.

External factors:

- Conditions of the commodity and stock markets;

- Taxation;

- Practice of lending to suppliers and buyers of products;

- Carrying out settlement transactions of business entities;

- Availability of financial credit;

- Possibility of attracting gratuitous targeted financing;

Internal factors:

- Life cycle;

- Duration of the operating cycle;

- Seasonality;

- Investment programs;

- Depreciation;

- Operating leverage ratio;

- Corporate governance;