Risk-free assets

Let's figure out what are reliable or risk-free assets and what kind of profitability can be obtained from them. Traditionally, the definition of risk-free assets includes assets with a high reliability rating. Such ratings, for example, can be assigned by national and international rating companies, etc. For example, Sberbank has an international rating of Aa1 as part of its deposit activities . ru

from Moody's agency, which corresponds to the second level (the highest rating in this category,

Aaa. ru

, was held by Sberbank from 2005 to 2014). But these ratings can sometimes be politicized, so it is important for the investor to understand the fundamental reasons characterizing the risk or reliability of a particular asset.

As a rule, investments in any assets that meet all of the following criteria can be considered a reliable investment:

- Fixed income.

- No negative fluctuations in asset prices or low fluctuations in asset prices.

- A high degree of safety of the asset, if it is a material object, or high financial stability and economic strength of the entity acting as a guarantor of the safety of the asset, if it is a financial asset or securities.

- High liquidity of the asset – i.e. the ability to quickly sell an asset or convert it back into money without a significant loss in value.

So, reliable investments are investments in assets that will provide, on the one hand, a fixed or stable return, and on the other hand, there are long-term guarantees of the safety of our capital. Also, relatively risk-free assets may include assets with a low level of price fluctuations and clear and transparent prospects for price growth in the long term.

Let's look at examples of assets that are the least risky today, analyze their pros and cons, and find the most profitable ones among them.

How to manage investment risks?

It is impossible to completely eliminate investment risks. However, any investor is able to manage risks, reducing the likelihood of losses and maximizing profits.

The diversification of the investment portfolio contributes to the distribution of risks and the level of profitability in the ratio that is most comfortable for the investor. The old adage about not putting all your eggs in one basket holds true when building a stock portfolio.

By investing in various financial assets, the investor balances the risks. At a time when the yield of some securities is falling, other financial instruments allow the investor to make a good profit.

Diversification of assets and competent management of financial instruments allow an investor to effectively invest savings, reduce investment risks and obtain maximum profit.

Bank deposits

This is perhaps the most common risk-free financial instrument, which everyone knows about and does not need any special introduction. At the moment, the most interesting indicator is the return on bank deposits. Of course, a lot here depends on the conditions, and specifically on the available amounts and deadlines. In our example, we will start from an amount of 400,000 rubles and a period of 1 year. As a result, we have access to a line of bank deposits with yields ranging from 3.3% to 10.7% per annum. At the same time, the upper level of profitability is provided by frankly problematic banks.

As elsewhere, in the case of bank deposits, profitability is directly related to risks. Therefore, when choosing a deposit, you must be extremely careful about the reliability of the bank. Even taking into account the fact that all deposits are insured by the state, it will be very unpleasant if, due to problems at the bank, your savings “hang” there for some time. And in the worst case, more negative scenarios are possible...

Pros.

The simplest and most understandable tool in terms of predicting future profitability. Easily accessible. There is also a very large selection of deposits. In the example, according to our requirements with an amount of 400 thousand rubles. and for a period of 1 year, 167 deposits were accepted.

Minuses:

The main disadvantage today is the general tension in the banking sector, caused by the increasing incidence of banking problems and reorganizations. Therefore, you can no longer choose a bank for a deposit without caution, but you should conduct a preliminary analysis of the bank (we described how to do this in the article “how to choose a bank”). As a result, only top banks, where deposit rates are at the level of 5-7% per annum, now actually meet all the criteria for reliable investments.

Risk-free approximate trading options

The type of option purchased depends on the direction of the asset price movement:

- a call is purchased during a bullish movement;

- put when the trend is bearish.

It is better to complete operations at the beginning of an active movement; acquisitions are carried out in the direction of the trend. There are traders who open a couple of options in different directions at once, this allows them to prepare for a market reversal. You can get rid of transactions that are not the most profitable for a deposit. This approach requires monitoring market conditions.

For novice traders, dealing centers have services for providing risk-free transactions. Thanks to this instrument, after profit you can return the bet amount or interest to your balance. When the operation has worked completely, then the profit comes in full. But the number of companies providing such services is small.

Government bonds

Government bonds are the most reliable financial instruments in any country. In our country, federal loan bonds, or OFZs for short, can be considered the most reliable.

OFZ is the most reliable Russian financial instrument for investment. OFZ is issued by the Ministry of Finance of the Russian Federation, i.e. state. Accordingly, the state also bears obligations under them. At the moment, the state is the richest payer in Russia. Although in many ways our trust in the state was undermined by the crises of 1993 and 1998, now we can say with confidence that the Russian Federation is a reliable payer.

As in the finances of an enterprise, the debt load in the state economy plays a major role. More debt means more risks.

In order to understand the current situation, let's evaluate the level of public debt for the largest developed and developing countries. To do this, compare the level of government. debt from the country's GDP.

We see that in Russia the level of debt as a percentage of GDP is the minimum among the countries represented (only 18% of GDP). This means that the state's debt burden is very low and payment of obligations is not in doubt. This indicator can also be used to assess the riskiness of investments in a particular country.

This once again demonstrates to us that Russian OFZs today have nothing in common with the defaulted bonds of the 90s, the yield on which reached 150% per annum.

The current market conditions are such that at the moment OFZs on average have a yield of about 10%-11% per annum. The yield on bonds is fixed as well as on deposits, because At the time of purchasing bonds, you already know the redemption price and interest payments. Moreover, unlike deposits, OFZs can meet various investment requirements, because There are OFZs of various types. In particular, they can protect against inflation (OFZ with a variable coupon linked to the consumer price index) and bring increased profitability with active reinvestment (OFZ with depreciation). You can read more about this in our article about OFZ (How to choose OFZ).

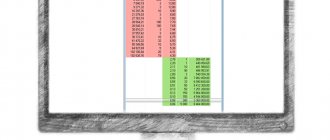

The table below presents a list of OFZs currently available for purchase on the Moscow Exchange, indicating their maturities and current yields.

Along with OFZs, bonds of some individual subjects of the federation can also be considered reliable investments. Since the economies of some municipalities, for example the city of Moscow, and large stable regions are comparable in their degree of reliability to the state as a whole. Therefore, investing in their bonds can also be considered. At the same time, the profitability of such investments will increase on average by 1% - 1.5%. However, here it is still worth taking a more careful approach to the choice of a subject of the federation or a municipality, having first assessed its financial stability. The main indicators here will be the level of debt of a federal subject or municipality and whether it is subsidized. If the region has a surplus and debt levels are low, then you can buy their bonds.

Also, highly reliable bonds include bonds of large corporations, such as Gazprom, Rosneft, the Magnit retail chain, etc. The yield on them at the moment will also be around 10-11%. We talked more about working with bonds, as well as how to choose them, in the article “Bonds are an excellent alternative to deposits.”

Pros.

Reliability is ensured by the state, while the level of debt in the Russian Federation is currently at an extremely low level. The yield on OFZs is higher than the yield on deposits in large banks. OFZs are traded on the stock exchange, the minimum lot amount is only about 1 thousand rubles, which makes this instrument as accessible as possible. With the help of OFZs it is possible to achieve various investment goals: obtaining a stable fixed income, complete protection against inflation, increased profitability on reinvestment. It is very easy to exit OFZs; you can simply sell your bonds on the stock exchange and not wait for the main maturity date. Income from OFZs is not taxed. In addition, when investing in OFZs, you can significantly increase your profitability if you take advantage of the state program. support for investors - individual investment accounts (IIA). As a result, the total return on investment in OFZs using IIS can reach 19-24% per annum (we’ll talk more about this in our free master classes).

Minuses.

The only disadvantage is the need to enter the stock exchange and the associated actions. But at the moment this is no longer something difficult and inaccessible.

What is the risk and return of securities?

Profitability is the level of profit that an investor will receive from invested capital in relation to the size of the capital itself

This indicator is usually calculated as a percentage, and for low-risk investments as an annual percentage, and for high-risk investments as a percentage per month.

Risks are considered to be different probabilities of not achieving the planned result, the most serious of which is the probability of loss of capital

This indicator is also measured as a percentage and is never equal to zero (risks always exist).

Risk and return are something that every person must evaluate when deciding to invest money in something. This applies equally to both the purchase of exchange-traded assets and the opening of a bank deposit.

You may also be interested in: How to take your first steps on the stock exchange?

Reliable Bond Funds

These are investment funds of the so-called collective investment, such as mutual funds and their foreign analogues traded on the Moscow Exchange - ETF, which literally stands for “exchange trade funds”. The line of such funds necessarily includes funds that specialize in investing in risk-free and reliable assets, i.e. in bonds, deposits, etc. This determines in advance the profitability that these funds show. In this case, it is impossible to say exactly what the future return of the fund will be, however, with a very high degree of probability it can be assumed that it will be a return comparable to the return on the bond market and bank deposits as a whole.

At the same time, investments in such funds are protected in advance from investment mistakes of “newbies” in the stock market, because they are managed by professional managers. Also due to the fact that these are collective investment funds, i.e. they invest collectively; ordinary investors with a small investment amount have access to all the tools of professional investors, such as expensive lots of Eurobonds, etc.

Here we present the performance results of all mutual funds specializing in bond investments over the past 3 years.

ETFs are much less represented on the Russian market. Only 3 exchange-traded funds of the management company FinEx, specializing in investments in bonds, are traded on the Moscow Exchange.

These are funds that invest in short-term US Treasury bonds, ruble Eurobonds of Russian companies and dollar Eurobonds of Russian companies.

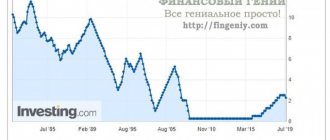

In order to understand that these are funds that invest in reliable fixed income instruments, just look at the graph of the value of their share.

Here we give an example of the dynamics of FXMM exchange-traded fund, which specializes in investments in short-term US Treasuries.

Let's summarize what are the pros and cons of investing in bond mutual funds and ETFs.

Pros.

The main advantage is that these are collective investment instruments, i.e. firstly, they are under the management of a professional manager represented by a management company, and secondly, due to the principle of collective investment, many professional investment instruments become available, such as corporate Eurobonds, government debt securities of various foreign countries. Moreover, due to this, you can invest in both ruble and foreign currency bonds, thereby eliminating the risk of currency fluctuations. At the same time, these instruments are available for investment to the ordinary private investor and the entry threshold for the investment amount is only a few thousand rubles.

Minuses.

Profitability is not fixed. We know that we will receive an income comparable to the bond market, but we cannot say a specific return figure, as in the case of buying a bond. As a result, as can be seen from the table above, profitability can vary from 1.4% to 47% per annum. Another disadvantage is commission costs when purchasing mutual funds, which can amount to up to 3-4% of the cost of the mutual fund and significantly reduce the profitability of such investments.

Which assets are the most risky?

There is a classification of assets according to their risk level. Financial instruments can be distributed in order of increasing risk level:

- cash;

- bonds;

- real estate and other property;

- shares and shares.

Cash is the safest type of investment. Shares are among the riskiest financial instruments.

Each asset class is divided into subcategories. The level of risk depends on the specific type of asset. For example, when investing in the shares of one company, an investor takes a lot of risk. Choosing a collective investment fund that deals with shares of many companies and has professional managers significantly reduces the likelihood of losses.

Relatively risk-free assets

Even among seemingly traditionally risky investment instruments like stocks, you can find good, reliable investments.

Here we can distinguish shares of 2 main groups:

- Stocks with low beta, i.e. these are the stocks that are least susceptible to market-wide periods of decline. When the overall stock market declines, shares of those companies fall more slowly or move at all independently of the overall market.

- Stocks with high dividend yield. Now the dividend yield of many companies looks favorably against the backdrop of the yield of the bond market, for example, the dividend yield in 2021 of such shares as Surgutneftegaz preferred and ordinary shares of the company PROTEK amounted to 16.71% and 16.33%, respectively.

Also relatively risk-free investments include such assets as real estate funds, so-called REITs and real estate mutual funds. Their reliability is determined directly by the investment object, i.e. real estate. However, we classify them as “relatively reliable” due to the fact that the price of real estate is subject to fluctuations (as practice has shown in 2014-2015, drops in value of up to 30-40% are possible) and, as a result, this is not a fixed income.

Minuses.

In this case, these investments are not at all similar to investments in fixed income instruments. It is impossible to say an exact figure for future profitability. A more thorough analysis of such assets is required to ensure the prospects for profitability.

Pros.

Possibility of obtaining additional profitability due to the increase in the market value of shares and funds. The low threshold barrier to entry into such investments is about several thousand rubles.

Forex currency market

The next financial instrument is the FOREX market. FOREX is an interbank currency exchange market at free prices, where quotes are formed without restrictions and fixed values.

This means that regardless of today’s exchange rate of the Central Bank of the Russian Federation, you can buy a dollar much cheaper and sell it much more expensive. You can trade on FOREX by opening an account with a FOREX broker. The only commodity in this market is the currencies of different countries.

How does the Forex market work?

The main feature of trading on the FOREX market is that, as a rule, the broker offers leverage. Leverage can be of different levels: 1/20, 1/50, 1/100, 1/500 or 1/1000. Leverage allows you to trade more money than you have in your account by taking out a loan from a broker.

This can help increase profit or loss if the price goes against the investor's position. However, we should not forget that leverage not only gives an advantage in making a profit, but also proportionately increases the risk of a trader or investor.

Forex market

The advantage of FOREX is the rapid movement of quotes and, as a result, a quick opportunity to make high profits. The downside is the statistically extremely low probability of success. There are two reasons for this: the novice trader’s low awareness of all the news, one way or another, affecting exchange rates and technical aspects (decreasing the value of the portfolio).

Risks of investing in gold

In this case, we present this example as an exception from the list of reliable investments. After all, many believe that buying gold or other precious metals is a kind of analogue of guaranteed income. But this is not true at all. Gold is a common commodity, just like stocks or oil. And prices fluctuate for it with exactly the same amplitude as for shares, and sometimes even more.

If you look at the gold price chart, it will immediately become clear that this is not a fixed income instrument.

If an investor had bought gold at the end of 2012, then at the beginning of 2016 the loss of his capital would have been more than 40%. Currently, losses would be reduced to 22%, which is also not an acceptable result.

Thus, gold has nothing to do with a reliable investment. It pays no dividends, does not provide any form of fixed income, and is subject to all the same factors as stocks or other commodities. The only option when gold can be used as a protective asset is to purchase gold as one of the tools for diversifying the risky part of your portfolio.

How to determine the financial risks of the market

The demand for risky assets necessitates an analysis of the size of possible cash losses. To assess the likelihood of income, banks use quantitative and qualitative methods.

Quantitative assessment is based on statistical data. Using mathematical formulas, the most expected result, the probability of losses and other values are calculated. The accuracy of the result depends on the completeness of statistical information, which is often insufficient.

Qualitative assessment involves the use of several tools:

- analogy method;

- Delphi;

- decision tree;

- Monte Carlo method;

- others.

The analogy method is the use of information about the operation of systems or phenomena similar to existing ones. Applicable when an organization does not have reliable data on the use of an asset.

The Delphi method is the process of obtaining opinions from experts on a specific list of questions. A risk assessment is based on the most popular answers from experts.

A decision tree is used when the development of events depends on the choice of one of the options by an authorized person. The situation can develop in several directions, each of which is characterized by certain factors for reducing or increasing profits.

The Monte Carlo estimation method involves studying the results of decision-making in similar cases. Based on the data, many scenarios are simulated. It is used in the most difficult cases for forecasting.

To manage risks, banks usually use several methods in combination.

Reinvestment risk

Although they are not risky in terms of probability of default, even risk-free assets can have an Achilles heel. And this is known as reinvestment risk.

For a long-term investment to remain risk-free, any required reinvestment must also be risk-free. And often the exact rate of return can be unpredictable from the very beginning throughout the life of the investment.

For example, suppose a person invests in six-month Treasury bills twice a year, replacing one installment as it matures with another. The risk of achieving each specified rate of return within the six months covering the rise of a particular Treasury bill is essentially zero. However, interest rates may change between each reinvestment. Thus, the rate of return on the second T-bill that was purchased as part of the six-month reinvestment process may not be the same as the rate on the first T-bill purchased; the third bill may not be equal to the second, and so on. There is some risk in this regard in the long term. The return on each individual Treasury bill is guaranteed, but the return over a decade (or however long the investor sticks with the strategy) is not.

Creating a securities portfolio

The return and risk of securities are the main concern of the investor. The point of creating a portfolio of assets is to try to achieve the required level of return while trying to reduce risk.

An investment portfolio includes a number of securities and can be owned by an individual, a company or several people/organizations on an equity basis

The assets in the portfolio can be of the same type (for example, only stocks) or very different (stocks, bonds, futures, options, real estate, precious metals).

Types of investment portfolios

The risk and return of each asset and their relationship with each other determines the overall type of investment portfolio. The asset income source divides the financial instrument into a growth portfolio and an income portfolio.

Growth Portfolio

It consists of companies' securities that are rising in price. An investor, creating such a portfolio, expects an increase in the price of the asset and the payment of dividends.

There are three types of growth portfolios:

- Aggressive growth portfolio. The purpose of purchasing such assets may be the hope of maximizing their value in the future. This usually includes securities of young but actively developing companies. The risk here may be high, but the return on assets has a chance to please.

- The following portfolio assumes conservative growth. Usually it includes securities of large companies - the so-called “blue chips”. There may not be high profits in a short time. However, this method of investing is deservedly considered low-risk, its composition often does not change for a long time, and the goal is, first of all, to preserve the invested funds.

- Finally, a definite middle ground and the most popular type of investment vehicle is the mid-growth portfolio. It combines the properties of the two above, since it combines both high-risk assets and reliable securities. Such a connection is designed to ensure average rates of capital growth with average investment risks.

Income Portfolio

Such a portfolio is created with the aim of providing a good current income and receiving interest and dividend payments.

Income portfolios can be of two types:

- with regular income, for which purpose it includes the most reliable securities that bring a fairly average income, but promise the smallest risks.

- a portfolio made up of income-generating securities, which include high-yield corporate bonds and high-yield, medium-risk assets.

At the same time, both the growth portfolio and the income portfolio have the same goal - to protect investments and, if possible, avoid losses that may arise both as a result of a decrease in market value and as a result of a decrease in interest payments.

Therefore, an investor should regularly assess the state of the market and the composition of the portfolio in order to timely replace assets that bring low returns or are unprofitable with high-yield securities.