Greetings!

Traditionally, the most reliable securities traded on the stock exchange are bonds or, in other words, bonds. The yield on these securities is low, and one way to increase it is to save on taxes.

That is why taxation of bonds for individuals is a relevant issue for every private investor who wants to work with this financial instrument. Today I will tell you about the basic aspects of this case, as well as its important little-known nuances.

What taxes are charged on corporate bonds?

It is customary to divide papers by release date. If bonds issued after 01/01/2017 are considered, then personal income tax is calculated as follows.

Income from coupons is exempt from personal income tax. But it should be remembered that if profitability increases above the stated values by more than 5%, you will have to pay 35% of the share of income in excess of the planned values to the budget.

Attention! There is a condition that should be taken into account. If a bond is held by the owner until maturity, then returning it to the issuer for the final price is tax free.

If the sale takes place at least one day earlier, you will have to pay 13% of the difference in prices before and after the sale.

If the securities were issued before 01/01/2017, then personal income tax is paid in the amount of 13% of all types of profit generated.

Taxation procedure

Individuals pay personal income tax calculated from the tax base.

The personal income tax rate for tax residents of the Russian Federation is 13%, for non-residents - 30%. In some cases, for both categories of taxpayers it can be 35%. The tax base is calculated as income minus expenses. Income for individuals from bonds can be as follows:

- received from their sale (repayment);

- coupon;

- accumulated coupon income (ACI);

- discount;

- from the difference in exchange rates.

When taxing different types of bonds, the income that forms the tax base is different.

Expenses on transactions with bonds are recognized as expenses for their acquisition, as well as for the fulfillment of other obligations under these transactions. These could be expenses for brokerage services, exchange commissions, etc. All expenses must be documented to facilitate taxation.

Personal income tax is written off upon withdrawal of money from the account or at the end of the tax period: it is equal to one calendar year.

Ruble bonds

From the point of view of a Russian investor, the taxation system for ruble bonds can be considered basic. All transactions on them and the entire taxation process for individuals are calculated in rubles; there are no difficulties with converting currencies in the face of changes in their exchange rates, and this is the main advantage.

I note that for legal entities, a minimum tax rate of 15% is established on profits from ruble bonds, and here individuals find themselves in an advantageous position.

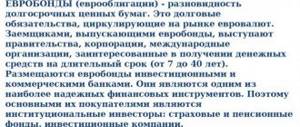

Eurobonds

Eurobonds, or “Eurobonds,” are denominated in foreign currency, but their taxation for individuals is carried out in rubles.

The taxation of federal, subfederal (regional) and municipal Russian Eurobonds for individuals is almost similar to the taxation of ruble OFZs. When dealing with corporate Eurobonds, the situation is somewhat more complicated.

The fact is that if an individual buys such Eurobonds, their value is converted into rubles at the Central Bank exchange rate on the date of this purchase. At the time of sale, the cost is also recalculated, but at the exchange rate on the date of the transaction.

And if between these dates the exchange rate of the ruble against the currency in which the Eurobonds were purchased fell, income arises from the difference in exchange rates, on which individuals pay 13% personal income tax.

Example: Papazyan bought one Eurobond for 100 US dollars. At the Central Bank exchange rate, 1 dollar was worth 50 rubles at that time, and the ruble value of the Eurobond at the time of its purchase was 5,000 rubles.

A month later, Papazyan needed money, and he sold this Eurobond for the same $100. However, the ruble exchange rate fell during this time, and 1 dollar was already worth 60 rubles. It turns out that the ruble value of the Eurobond at the time of its sale was 6,000 rubles.

Thus, lucky Papazyan earned 1000 rubles from the difference in exchange rates, and now he, as an individual, must pay 13% personal income tax on this amount, that is, 130 rubles.

At the same time, whether Papazyan will actually transfer his 100 dollars into rubles or not is not taken into account when carrying out taxation. You need to pay in any case.

Coupons and discounts on corporate Eurobonds are subject to personal income tax of 13%. Otherwise, the taxation of corporate Eurobonds for individuals is identical to the taxation of corporate ruble bonds.

Tax deductions through IIS

An individual investment account (IIA) allows individuals to conduct transactions with bonds and other financial instruments traded on Russian stock exchanges and receive a personal income tax deduction when using it. Only tax residents of the Russian Federation can use IIS.

Type A deduction will allow you to return previously paid personal income tax on any income in the amount of 13% of funds invested through IIS, but not more than 52,000 rubles. in year.

Type B deduction will allow you to carry out exchange transactions through an individual investment account without paying personal income tax on income from them. However, you can use the amount exempt from taxation only when closing the account, i.e. no earlier than 3 years later. You can receive this type of deduction only if you have not previously received a type A deduction.

Investments through IIS are made only in rubles, and the amount is limited to 1 million per year.

How and to whom to pay taxes

Buying and selling bonds with the help of a Russian broker allows you to shift the responsibility for paying personal income tax to that broker. The broker's responsibilities include the obligation to make payments on securities, complying with tax laws on the handling of securities for individuals.

If the activity is carried out apart from the broker, then the responsibility for paying taxes lies with the investor himself.

Risks and expenses of bondholders

Individuals are at risk in the following cases:

- Possible credit risk due to the bankruptcy of the issuer or in the event of a technical default with deferred payments.

- A decline in the market value of bonds may result in a loss in the value of the security.

- The liquidity of bonds must be ensured by money, fixed assets and other property. If it is impossible to answer for one’s debts to an investor, the likelihood of an individual’s losses increases.

- If there are variable rates on coupons, there may be risks of reducing the size of payments.

Attention! There may be other risks associated with:

- with lower interest rates;

- due to inflation of the domestic currency;

- with events that lead to dramatic changes in the economy or society.

What is considered the issue date?

The date of issue of bonds is recognized as the date of state registration of the issue for circulation.

Are there any restrictions on the coupon value?

If the income from coupons exceeds the Central Bank refinancing rate by 5% or more, then personal income tax is calculated from the amount that exceeds this threshold.

Attention! An option is possible when the refinancing rate is reduced so that the coupon income becomes higher by more than 5%. Then, for profits above a limited threshold, an individual will have to pay tax.

Who performs the functions of a tax agent?

When working through a broker, the duty of a tax agent rests with the broker. When working independently in the securities market, the investor himself is a tax agent. He is obliged to submit information about income to the tax authorities.

Federal loan bonds (OFZ)

In order to attract investment in relation to OFZs, the state has established the most attractive tax regime for individuals. All types of income from OFZs are exempt from duty, except those that arise due to an increase in their value.

At the same time, the taxation of OFZ, subfederal (regional) and municipal bonds is no different.

Coupons

At this point, taxation for the investor is simply a balm for the soul: coupons, income tax and the OFZ discount for individuals are not taxed.

Cost growth

Income of individuals from the sale (redemption) of OFZs, arising as a result of an increase in their value, is subject to personal income tax of 13%.

Exchange difference

Individuals can carry out transactions on federal Eurobonds and receive income from differences in exchange rates without paying personal income tax.

Example: Andreev had 5,000 rubles. He bought 100 dollars with them at the Central Bank exchange rate, which at that moment was 1 dollar = 50 rubles. Then Andreev used this money to buy one federal Eurobond at a price of $100 apiece.

And a week later, the Central Bank informed Andreev that the ruble exchange rate against the dollar had fallen: 1 dollar = 60 rubles.

Andreev, don’t be a fool, sold his federal Eurobond on the same day for the same 100 dollars (without receiving any profit from the Eurobond itself), and then sold these 100 dollars for 6,000 rubles.

Thus, Andreev received income from the difference in exchange rates of 1000 rubles. But since he carried out transactions specifically with the federal Eurobond, the state does not take tax on his earnings.

Is it possible to avoid paying taxes and what will happen?

When working with a broker, it is impossible to avoid taxes. The broker is obliged to comply with the requirements of the legislation of the Russian Federation.

If work on the securities market is carried out without intermediaries, then you will have to answer on your own. If large sums are concealed, criminal charges may be brought, which include long prison terms and confiscation of property.

In table provides information about risks and taxes for different methods of placing money.

Tax optimization of coupons

If you still need to hold bonds, and not shares of a bond fund, then to minimize losses, the most profitable options are securities with a minimum coupon income. In Russia, there are practically no zero-coupon bonds (discount bonds) as a class. But you can still find bonds with a small coupon. If the yield to maturity is the same, to minimize the tax, you should choose a bond with a lower coupon. These bonds typically have a larger discount when purchased, and most of the profit will be realized when the security is sold or redeemed.

Pros and cons of CO

This type of debt securities is popular among experienced investors and novice traders.

The reason for this is the significant advantages:

- Different types of KOs, the choice is up to the investor.

- The issue is carried out by companies in different industries. By controlling the market, you can regularly invest money in enterprises whose activity and profitability are at their peak.

- Wide risk range. The stock exchange offers to take both reliable corporate bonds, for example, from Sberbank or AHML, and high-risk ones with increased profitability.

- KOs are traded during the circulation period; it is not necessary to hold them until maturity; they can be sold and bought at any time.

- Attractive profitability. Bonds issued by commercial organizations are almost always more profitable than GKOs, OFZs, and municipal central banks.

- Taxation of corporate bonds is a set of several articles of the Tax Code of the Russian Federation. They are easy to understand even without accounting knowledge. With the right approach and opening an IIS, you can be exempt from a number of taxes.

The investment instrument also has disadvantages:

- The safest securities are those with low volatility (profitability). This is the main disadvantage of CO: the financial benefit is directly proportional to the risk. Reliability reduces speculative interest - such bonds are practically not traded because the market price rarely changes.

- A large number of bonds with different parameters and issuers complicates selection and analysis.

- Speculation on the stock exchange during the period of circulation of a security requires the investor to have at least basic knowledge of valuation and analytics. Playing blindly can quickly lead to unprofitability.

Individual entrepreneur taxes

Entrepreneurs using the simplified tax system can choose operations with securities as their type of activity (OKVED 64.99.1 – investments in securities). The Ministry of Finance explained in letter No. 03-11-06/2/58917 dated August 6, 2021 that the income of an entrepreneur on a simplified market is:

- income from the sale of goods and property rights (revenue);

- non-operating income,

and the bonds purchased by individual entrepreneurs relate to goods and the income from their sale is revenue as part of the base under the simplified tax system. Interest income is included in non-operating income.

If the simplified taxation system of 15% of profit is chosen, then expenses from transactions with securities are taken into account in the financial result according to clause 23, clause 1, article 346.16 of the Tax Code of the Russian Federation.

It is impossible to combine 2 types of objects according to the simplified tax system, for example, to apply 6% for turnover, and 15% for income with expenses. All activities on the simplified market are considered according to one of the methods for determining the tax base. Letter of the Ministry of Finance No. 03-11-06/2/63 dated April 21, 2011 speaks about this.

Risks and expenses of bondholders

Despite the fact that bonds (ruble and EO) are considered low-risk financial instruments, it is important to remember the existence of external risks from which no company is insured.

Bond prices can change at any time, influenced by macroeconomic events. This risk is called market risk.

Situations are possible when there are delays in payments (principal amount at face value and/or coupons), or the issuer defaults on payments for various reasons. This risk is called credit risk.

All issuers are regularly assessed by rating agencies, which assign certain levels of reliability. Investors are advised to monitor the rating position of their bonds.

The future investor should also remember that in addition to taxes, he will pay a commission for all transactions to the exchange and broker.

Thus, before starting trading on the stock market, when choosing a broker and financial instrument, you should familiarize yourself with:

- with exchange and broker tariffs for operations

- with tax rates on the types of securities of interest.

Which regional bonds to pay attention to

From May to August, seven Russian regions have already entered the market with new bond issues. In total, they raised more than 63 billion rubles from investors.

In September, four more regions - Bashkiria, Lipetsk region, Belgorod region and Tomsk region - announced that they were preparing new bonds.

Yango.Pro has collected in one place a list of fresh investment ideas in the municipal bond market that are worth paying attention to today.

Moscow region

AA+(RU)/Stable from ACRA Ba1/Stable from Moody's BBB-/Stable from Fitch Ratings

The Moscow region is one of the most advantageous regions of the country from an economic point of view. In 2021, it was in second place among the constituent entities of the Russian Federation in terms of gross regional product (GRP) (4.76 trillion rubles). Its absolute advantage is its proximity to Moscow, which easily guarantees both a stable sales market and demand for labor resources (and this guarantee of low unemployment in the region).

The growth rate of industrial production in the region in 2016–2019 significantly exceeded the Russian average (at least 10% per year with the national average of 2–3%). The industry is dominated by food production (22%). The Moscow Region is also one of the largest agricultural producers in the Central Federal District (6th place).

At the same time, tax revenues to the budget are not tied to one large taxpayer: historically, the maximum share of one taxpayer in budget tax revenues is less than 4%.

The Moscow region has traditionally been conservative in terms of fiscal policy: in 2021, the budget deficit was 14% of domestic revenues, the level of budget self-financing was 87%, and the debt burden was 34%. In 2021, the region expects to reach a budget deficit of 13% and self-financing of 88%.

The Moscow region has been placing bonds since 2021. At the end of last year, bonds accounted for about 49% of the region's debt. Currently, the Moscow Region has 5 bond issues in circulation with a total outstanding par value of RUB 96.75 billion. Thanks to the accumulated experience of public loans, the region has no problems with debt refinancing, since there is always open access to all sources of debt financing on attractive terms.

Sverdlovsk region

ruAA-/Stable from Expert RA A+(RU)/Stable from ACRA BB+/Stable from Fitch Ratings

Classic industrial region. Industry forms the basis of the regional economy (the region is a leader in the volume of shipped products in metallurgy and ranks 4th in terms of manufacturing output. For example, among the largest enterprises in the region are companies such as MRSKA of the Urals, Uralvagon.

Over the four years since 2014, domestic budget revenues grew by 57%. The region ended last year with a deficit of 14.3 billion rubles. (6.5% of domestic revenues). In the regional budget for 2021, officials have included a deficit of 29.4 billion rubles. (12.5%).

Until now, the Sverdlovsk region has managed to maintain a very moderate level of debt burden. Last year the debt to domestic revenue ratio was 35%. By the end of this year, the debt burden should increase to 43%.

Meanwhile, in terms of the quality of regional financial management, the region is included in the “green group of regions” according to the Ministry of Finance classification.

The region traditionally finances most of the budget deficit with commercial loans; bonds account for almost 33% of the debt. In total, the region currently has 6 bond issues in circulation with a total outstanding par value of 47 billion rubles.

Ulyanovsk region

ruBBB+ from Expert RA

More than a quarter of the region's GRP is formed by the manufacturing industry. Leading industries include mechanical engineering, automobile manufacturing and aircraft manufacturing.

At the end of 2021, the share of non-residents in the region amounted to 76.7%. In the structure of tax revenues, the largest share is occupied by excise taxes - 35.1%, corporate income tax - 24.6%, personal income tax - 25.4%.

Last year, the regional budget was executed with a deficit of 2.3 billion rubles, or 5.0% of the total income. In 2021, a deficit budget is also expected (2.1 billion rubles, or 4.3% of the total income). The region plans to cover the deficit through bond issues and bank loans.

True, the crisis situation amid the pandemic may spoil the picture and lead to an increase in the debt burden. As of January 1, 2020, the region’s debt burden was 53.4%, and the total debt level reached 24.9 billion rubles. At the same time, the majority of the portfolio was accounted for by bank and budget loans. The share of bonded loans was 20.1%.

Samara Region

BB+ from S&P Ba2 from Moody's AA(RU) from ACRA

The basis of the region’s economy is manufacturing and oil production (22% and 20.8% of GRP in 2021, respectively). At the same time, the structure of the manufacturing industry is dominated by the production of vehicles (42.5%).

The region's debt burden last year was 33%. The region will try to maintain approximately the same level at the end of the current year. However, according to ACRA, due to a possible decrease in tax and non-tax revenues in 2021, the ratio of its debt to current income may increase to 34% (in 2022, the region promises to reduce its debt burden to 28%).

The structure of the region's debt is dominated by bonds (about two-thirds of the debt), the rest is budget loans. Thanks to this, the annual volume of repayment (refinancing) does not exceed 18% of the current debt volume (no more than 8.7 billion rubles).

The Samara region closed 2018 and 2021 with a budget surplus. However, this year the budget is expected to be executed with a deficit of about 8% of the total income, which is planned to be covered mainly from funds accumulated in previous years.

The region regularly places funds on deposit in an amount that exceeds average monthly budget expenses in 2021. As of April 1, 2020, funds in bank deposits were more than twice the amount of the region’s debt obligations that it will have to repay this year.

Belgorod region

AA-(RU) from ACRA

The Belgorod region ranks 2nd in the Central Federal District in terms of GRP per capita after Moscow. More than 40% of the country's proven iron ore reserves and 80% of the iron ore of the Kursk magnetic anomaly are concentrated in the region.

The share of NND in total budget revenues was 78% last year.

The last time the region's budget ended the year with a surplus was in 2018. Last year the budget turned out to be in deficit (-1.8 billion rubles). The deficit at the end of this year should already reach 11.7 billion rubles.

As of September 1, the region's debt amounted to 30.9 billion rubles. By the end of the year, according to officials' forecasts, it should increase to 34.2 billion rubles. This means that the region's debt burden will increase to 49% from 38% at the end of 2021.

Yaroslavl region

BB from Fitch ruBBB from Expert RA

In terms of GRP production volumes (per capita), the Yaroslavl region is in 6th place among the regions of the Central Federal District. The main industries in the region are mechanical engineering and metalworking, chemistry and petrochemistry, as well as the food industry.

One of the advantages of the region is the low dependence of the regional budget on federal transfers and a stable base of tax and non-tax revenues: their share in regional budget revenues consistently exceeds 80%. At the end of 2021, it amounted to 82.5%.

In the structure of tax revenues, the largest share is occupied by corporate income tax - 31.9%. True, the share of the largest taxpayer, the branch of PC Baltika LLC - Beer, accounts for 10.1% of the tax revenue, which means that the region’s budget is quite dependent on the financial condition of the company.

At the end of 2021, the region’s budget was executed with a deficit of 1.5% of the total income, this is by 0.6 percentage points. below 2021 levels.

The region traditionally prefers to finance the deficit by issuing bonds. It was planned that in 2020–2022 the region’s budget would be deficit-free. However, at the end of 2021, according to the forecasts of regional officials, it is still impossible to avoid a deficit - it is expected to amount to 918 million rubles. (1.5%)

Considering that the region relies quite heavily on bonds (their share in the debt portfolio is 52.3%), its debt burden is quite high: as of January 1, 2021, it was 65.9%. By the end of 2021, the region expects to reach a debt volume of 38.3 billion rubles. and a debt burden of 61%.

The Republic of Sakha (Yakutia)

BBB- from Fitch ruАА- from Expert RA

Yakutia is the largest subject of the Russian Federation by area, occupying a fifth of the entire territory of Russia. According to the rating of total reserves of all types of natural resources, the Republic of Sakha (Yakutia) ranks 1st in Russia. The main industry of the republic is mining.

Yakutia produces 95% of all Russian diamonds and 24% of gold. Globally, its share in diamond production is 25%.

Last year, republican budget revenues amounted to 220 billion rubles. of which 132.2 billion rubles. - internal. The share of tax and non-tax budget revenues amounted to 60.08% at the end of 2021. At the same time, the republic has a higher share of subsidies from the federal budget compared to individual constituent entities of the Russian Federation.

At the end of last year, the state budget of the republic was executed with a deficit of 1.9 billion rubles. (1.4%), this year it will also be in short supply.

The Republic is historically included in the first prosperous group of subjects of the Russian Federation with a high level of debt sustainability. The volume of government debt at the beginning of 2021 was 49.2 billion rubles. The level of debt burden is 37.2%.

Yakutia is the oldest issuer on the regional bond market. The republic made its debut on the public debt market back in 2002 and has already issued more than 20 loans in total. It currently has 8 bond issues in circulation.

Bashkiria

BBB from Fitch Ba1 from Moody's ruAA+ from Expert RA

The largest industrial center of the country. The region is one of the 10 leaders in oil production (currently there are 1,300 fields on the state balance sheet). In addition, the republic is one of the largest regions for the production of agricultural products in Russia (mainly in livestock farming).

The region's calling cards are companies such as Bashneft and the Bashkir Soda Company.

The Republic of Bashkortostan is a conservative in terms of budget policy: from 2017 to 2021, the region maintained a moderate level of budget surplus (on average 4% of domestic revenues) and a high level of self-financing (on average 77%). Debt leverage stood at a low 9% at the end of 2021. At the same time, from 2021 to 2021, Bashkiria reduced its debt by 26% - to 13.5 billion rubles. At the end of 7 months of 2021, the debt amounted to 15.5 billion rubles, the debt burden was 10%. 77% of the debt was represented by budget loans and only 10% by bonds.

As of August 1, the republic had liquid funds that were 2.4 times higher than its debt obligations.

Tomsk region

BB-/Stable from S&P ruBBB+/Stable from Expert RA BBB(RU)/Stable from ACRA

Industrial region in the southeast of Western Siberia. The region has a fairly high level of socio-economic development due to oil production and the status of Tomsk as one of the leading centers of science and education.

The estimated GRP growth in 2021 was 1.4% y/y. In the structure of industrial production, oil and gas production and refining play a key role (Tomskneft, GPN-Vostok, Vostokgazprom, Russneft).

In 2021, the region had a moderate deficit (6.9% of domestic revenues), for seven months of 2021 it was high, 14% of domestic revenues. Expenses increased by 20%, while income increased by only 8%. The budget's own revenues fell by 10% (8% on average in Russia, 9% in the Siberian Federal District) - mainly due to a reduction in income tax revenues by 34% (18% in Russia, 22% in the Siberian Federal District) amid the COVID-19 crisis and lower oil prices.

The region’s debt over the eight months of 2021 increased by 17% to RUB 37.9 billion. from 32.3 billion rubles. by the end of 2021. The growth was mainly due to an increase in budget loans by RUB 5.5 billion.

The region has a comfortable debt repayment schedule: about 16% of debt is repaid within a year, and the peak of bond and commercial loan repayments occurs in 2022–2023. At the same time, based on the budget, in 2021 the debt burden should be 61%.

Lipetsk region

BB+ from Fitch AA(RU) from ACRA

The region's economy is focused on the industrial sector with an emphasis on ferrous metallurgy. In 2021, the region's 10 largest taxpayers contributed 41.5% of total tax revenues to the budget (among them are NLMK, Cherkizovo and Indesit International). By the way, the share of the Lipetsk region in the Russian production of household refrigerators and freezers is 26%.

In 2016–2019, total regional budget revenues increased by 25% - to 64.2 billion rubles, almost entirely due to tax and non-tax revenues of the region.

Thanks to the very conservative budget policy of the Lipetsk region, it was possible to significantly reduce the level of debt burden - the debt/equity income ratio decreased from 44% in 2021 to 29% at the end of 2021. Now, according to this indicator, the region is in 24th place in the Russian Federation.

One of the weaknesses in the region’s financial indicators is the large share of short-term debts. 50% of the region’s direct debt matures in 2020–2021. True, the regional Ministry of Finance emphasizes that this fact is smoothed out by a good supply of liquidity and a moderate level of debt in general (as of August 1, it amounted to 14.3 billion rubles and was 34% represented by bonds.

Taxation of transactions through IIS

By using an individual investment account, investors have the opportunity to receive a tax deduction and get some of their money back. This refund option has been available to individuals since 2015.

Currently reading: What is the price of 1992 Soviet bonds?

Tax deductions through IIS can be of two types:

- personal income tax refund from the sale of assets;

- tax refund on income from stock trading.

To apply for a personal income tax deduction you must:

- Submit a personal income tax return.

- Draw up a paper confirming the fact of receipt of income.

- Provide documents confirming the transfer of funds to the investor account.

- Demonstrate the tax agreement for opening an account.

- Write an application for a refund.

You can submit a package of documents to the tax office:

- through the tax service website;

- via Russian Post;

- in person by visiting the Federal Tax Service office.

Filing tax returns can be done at any time.

Refund of tax on income from exchange trading is carried out by providing the broker with a certificate from the tax service confirming the fact of non-use of deductions under IIS.

Each investor chooses the type of deduction independently. Novice investors, as a rule, try to return funds given under the personal income tax, and experienced investors often return tax on exchange trading.

Best Municipal Bonds 2019

Let's look at the issues of the best municipal bonds of 2021, with a par value of 1,000 rubles in circulation. But it’s worth noting that the issuer’s assessment of those described below is approximate.

When the economic situation changes during times of sanctions and unstable oil prices, changes can quickly move a player from reliable to “near-bankrupt”.

Of course, we are not talking about Moscow, St. Petersburg, or raw materials regions.

| Issue name | maturity date | Coupon payments | Market price, % | Efficiency yield, % | ||

| % | Frequency, per year | NKD | ||||

| Belgorod Region-34009-ob | 30.06.2020 | 12,65 | 4 | 8,63 | 102,27 | 8,63 |

| Volgograd-34007-ob | 10.10.2019 | 12,26 | 4 | 4,3 | 101,19 | 8,39 |

| Volgograd-34008-ob | 19.10.2020 | 13,58 | 4 | 6,7 | 105,5 | 8,53 |

| VolgogradRegion-35007-ob | 02.06.2024 | 8,90 | 4 | 3,66 | 101,11 | 8,45 |

| KaliningradRegion-35002-ob | 17.12.2024 | 7D | 4 | 1,3 | 98,32 | 8,58 |

| Karach-Cherkess Rep-35001 | 18.12.2024 | 8,7 | 4 | 1,19 | 101,04 | 8,7 |

| Karelia Rep-35018-ob | 15.10.2023 | 8,00 | 4 | 10,8 | 99,38 | 8,47 |

Maturity date is the day on which the issuer transfers the face value of the bond to the investor's account. Coupon payments are distinguished by % (percentage accrued per year from the nominal value), frequency of payments (4 - 4 times a year, that is, quarterly), ACD - accumulated coupon, it is included in the market value.

This year, municipal bonds were issued only once, but its conditions were unfavorable. Therefore, this summary shows securities on the secondary market.

Accordingly, the purchase price depends on the economic situation . Here its cost is given as a percentage; 100% is taken at 1000 rubles.

Effective yield reflects the potential profit taking into account reinvestment. If the accrued profit is withdrawn to bank accounts, the actual benefit will be 5-15% lower.

About municipal bonds of Moscow and the region

Calculations taking into account NKD

Non-zero coupon income is fully taxed. It is quite simple to calculate the amount of funds alienated in favor of the state. Let's look at an example:

An individual purchased a bond with a par value of 2 thousand Russian rubles for 98% of the cost, that is, for 1960 rubles. The coupon size is 35 rubles.

After two payments, the citizen decided to sell the asset to another investor. The investor did not wait exactly half of the time until the next payment. Thus, the tax amount is: 35\2 * 0.18, that is, 3 rubles 15 kopecks.

Who performs the functions of a tax agent?

A tax agent, in accordance with Article No. 226.1 of the Tax Code of the Russian Federation, may be:

- The depository that pays the income. This tax agent is relevant for OFZ, municipal bonds and corporate bonds, the registration of which was made after January 1, 2012.

- Issuer. Tax agent for securities registered before January 1, 2012.

All Russian brokers operating on domestic financial markets are tax agents. They independently calculate the amount of tax based on the profit received by the investor for the reporting period.