Good day, dear reader! Let's talk today about the price of ChTPZ shares, as well as what will happen to them in the future. The ChelPipe Group, one of the top ten world leaders in the production of pipe products, was formed in the early 2000s on the basis of Chelyabinsk Pipe Rolling Plant OJSC.

Less than 3 years ago, in the presence of Russian President V.V. Putin's company launched a line using nanotechnology. More than 70% of the largest operating domestic pipelines are made from the plant's pipes. The most famous projects are the Nord Stream 2, Power of Siberia, etc. gas pipelines.

Securities data

The authorized capital of the ChTPZ group today is about 472.5 million rubles, divided into the same number of shares. Their nominal value is 1 Russian ruble.

Information about the company's securities is presented in the table.

| Promotion parameter | Meaning |

| Name | Ordinary registered share |

| Number of securities in circulation, pcs. | 472 382 880 |

| Par value of the share | 1 RUB |

| Ticker | CHEP |

| Trading platforms and trading times | Moscow Exchange PJSC, Monday – Friday: from 9:30 to 19:00 |

| Dividends | Eat |

| Year of foundation | 12/12/2008 |

| Headquarters | Moscow |

Exchange rate dynamics for all time

The metallurgical industry occupies one of the leading positions in the Russian economy. The performance indicators of metallurgical companies, including ChTPZ, are largely determined by:

- The ability of management to competently use the assets that are at their disposal.

- Demand for the products offered.

The graph clearly shows the development of the issuer. Minimum quotes in 2014 – 20 rubles. - are associated with information from law enforcement agencies about the economic fraud of the board of directors of an industrial group, as well as the imposition of sanctions by the West. All this affected the share price.

The stock price reached its peak in April–May 2021. This is most likely due to the construction of a number of new pipelines to Asia and the West, and the lifting of sanctions by a number of Western companies. The price of shares reached 255 rubles.

I will add that the company’s operating results, which today turned out to be significantly better than predicted, can significantly increase investor interest in ChelPipe.

About company

The history of ChelPipe begins at the end of the 19th century with the construction of a workshop of the Nikopol-Mariupol Mining and Metallurgical Society for the production of pipes in Mariupol. With the advent of Soviet power, the plant developed as a mechanical engineering enterprise. A number of new workshops appeared at the plant: new pipe, thick sheet, etc.

In 1941, the plant was rebuilt for military needs. Due to the proximity of the advancing German units, the most important technical equipment was dismantled and transported to Chelyabinsk. Within a few months, the first products rolled off the assembly line of the newly created Chelyabinsk Pipe Rolling Plant.

In the early 90s. ChTPZ was transformed into a joint-stock company and privatized. In 2002, the plant was transformed into the ChTPZ group, which in 2004 included the Pervouralsk New Pipe Plant after ChTPZ purchased 57% of its shares.

In 2008–2009 The company bought a scrap metal processing company to supply the steelmaking complex in Pervouralsk with its own raw materials. At the same time, Rimera JSC along with its subsidiaries, whose specialty was oil equipment, became part of ChTPZ.

The company's staff today is approximately 25 thousand people, its headquarters are in Moscow.

Production of the company

ChelPipe Group today sells a wide range of pipe products - more than 25 thousand pipe sizes. ChelPipe's warehouse complex includes 5 divisions, 13 territorial departments and 15 warehouse sites. Main products:

- pipes (oil and gas, casing, hot-deformed, boiler, bearing, profile);

- pipeline connecting parts (plugs, transitions, tees);

- shut-off and control valves (valves, taps, gate valves);

- drilling equipment;

- special equipment, cylinders, spare parts.

Main shareholders

Major shareholders today:

- 50% – entrepreneur A. I. Komarov, former member of the Federation Council of the Russian Federation, co-chairman of the Pipe Industry Development Fund;

- 35% – JSC “Pervouralsk New Pipe Plant”;

- 7% – member of the board of directors of ChTPZ Fedorov P.A.;

- 6% – BOUNCEWARD LTD;

- 2% – other shareholders.

Key figure and her role

The leading role in the development of ChelPipe rightfully belongs to the chairman of the board of directors and main shareholder, businessman Andrey Komarov.

At a difficult time, he found himself at the head of an industrial group. During his reign he managed to:

- Launch an educational program to train qualified personnel for ChelPipe.

- Unite staff into a sustainable team and inspire people with a sustainable philosophy. The company has a proven mentoring system.

- To bring to life such global ideas as “Height 239”, “Iron Ozone 32”, “Eterno”, etc. These are breakthrough technologies in metallurgy, where a metallurgist can keep his uniform white in a hot shop.

Affiliated companies

The ChelPipe Group today includes the following subsidiaries:

- Novotrubny plant in Pervouralsk;

- production of pipeline fittings in the Czech Republic;

- scrap processing;

- GC "Rimera";

- division for sales of products of TD "Uraltrubostal".

Company plans for the future

Among the priority areas for the development of the ChelPipe Group today I will highlight:

- Providing the oil and gas and other industries with high-quality pipe products for new and existing pipelines.

- Improving the quality of products, increasing their service life, creating new properties of the metal.

- Training of young highly qualified personnel.

Dividend statistics

| For what year | Period | Last day of purchase | Registry closing date | Size per share | Dividend yield | Closing share price | Payment date |

| 2019 | 4 sq. | 5 Jan 2021 | 10 Jan 2021 | 9M 2020 | 6,55 ₽ | 2,57% | 22 Jan 2021 |

| 2019 | 4 sq. | June 10, 2020 | June 15, 2020 | 12M 2019 | 8,18 ₽ | 3,9% | June 29, 2020 |

| 2018 | year | 6 Jan 2020 | 9 Jan 2020 | NP | 4,37 ₽ | 2,13% | 23 Jan 2020 |

| 2017 | year | 6 Jan 2020 | 9 Jan 2020 | 9M 2019 | 5,45 ₽ | 2,66% | 23 Jan 2020 |

| 2016 | year | 5 Jul 2019 | 9 Jul 2019 | 12M 2018 | 15,38 ₽ | 10,05% | July 23, 2019 |

| -1 | May 7, 2018 | May 10, 2018 | 12M 2017 | 11,56 ₽ | 4,61% | May 24, 2018 | |

| -1 | May 4, 2017 | May 10, 2017 | 12M 2016 | 10,05 ₽ | 6,74% | May 24, 2017 |

Currently, I have not been able to find complete information about ChelPipe’s dividend policy on the Internet. According to the company's Charter, dividends are paid to shareholders in accordance with the legislation of the Russian Federation. The organization has the right to pay them quarterly, every six months, 9 months, based on the results of the reporting year. The decision on payment is made by the general meeting of shareholders.

There is no information on periodic dividend payments to shareholders. For the first time, shareholders received dividends in 2021 and 2021. Payments amounted to 10.05 rubles. and 11.56 rubles. respectively for each share. According to forecasts, in 2021 shareholders will be able to receive 15.38 rubles. for each share.

Interesting facts about the company

The company was the first in the world to implement the principle of “white metallurgy” in a new pipe production workshop. In 2010, ChelPipe introduced a new standard: such pipes can be used to lay pipelines in areas with permafrost, seismic zones, and along the seabed. The enterprise has enough capacity to produce up to 600 thousand such pipes annually.

ChTPZ. Promising dividend chip in the third tier

About company

Chelyabinsk Pipe Rolling Plant (ChTPZ) is a group of ferrous metallurgy enterprises specializing in the production of pipe products.

The company occupies about 49% of the Russian market for seamless industrial pipes, 18% of the domestic market for seamless oil and gas pipes and 31% in the large-diameter pipe segment.

ChelPipe Group is vertically integrated and includes:

– Pipe division: Chelyabinsk Pipe Rolling Plant, Pervouralsk New Pipe Plant; – Scrap procurement division: “META”; – Trunk equipment: “SOT”, “ETERNO”, MSA (Czech Republic); – Oilfield services division: Rimera Group of Companies.

The company's ordinary shares are traded on the Moscow Exchange (ticker CHEP). The securities are included in the third level of listing of the exchange.

Shareholders

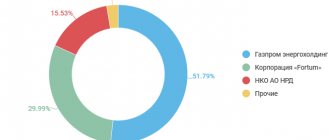

The controlling shareholder of ChelPipe is the Chairman of the Board of Directors, Andrey Komarov. He directly and indirectly (through 100% in Bounceward LTD.) owns 86.54% of the company's shares. Board member Pavel Fedorov controls another 10.67% of the company's shares. The share of free float is very low and amounts to about 2.79%.

Financial indicators

About 85% of ChelPipe's revenue at the end of 2021 came from the pipe division. 37% of the indicator was formed through the sale of seamless pipes, 15% - large diameter pipes (LDP). In total, export supplies accounted for 36% in the structure of ChelPipe shipments in 2021.

Consolidated revenue at the end of 2021 increased by 8% YoY and reached RUB 192.3 billion. The growth in the indicator was due to an 8% increase in shipment volumes at the end of the year in international markets.

Adjusted EBITDA at the end of 2021 increased by 13% year-on-year and amounted to RUB 31.8 billion. Profitability increased by 0.8 percentage points. due to an increase in the share of high added value products in the sales structure.

In the EBITDA structure, 86% comes from the pipe division. The oilfield services segment accounts for 11% of EBITDA and is one of the most marginal areas. The trunk division provided about another 3% of EBITDA at the end of 2021.

Net profit in 2021 amounted to RUB 9.96 billion, an increase of 29% YoY against the backdrop of EBITDA growth and improved margins. LTM indicator at the end of 2021 reached a historical maximum.

Capital expenditures in 2021 amounted to 7.6 billion rubles, which is 37.6% higher than the same figure for 2021. According to Komarov, the company is now at the end of the investment cycle. This suggests that capex should not rise in the near future, which could have a positive impact on free cash flow.

Free cash flow (FCF) at the end of 2021 amounted to 11.1 billion rubles, which is 10.6% more than at the end of 2021. In recent years, in the first half of the year, FCF went into negative territory; in the second half of the year, cash flow was strongly increases. Such dynamics are associated with the seasonality of working capital - in the first half of the year, inventories are replenished, which is reflected in FCF.

At the end of 2021, net debt amounted to RUB 67.1 billion, the ratio of net debt to EBITDA was at 2.1x.

The company's debt burden has been consistently decreasing in recent years. The company's interest costs are also falling due to the refinancing of loans amid lower interest rates. Over the next 5 years, ChTPZ intends to reduce the ratio of net debt to EBITDA to 1.5x.

In the debt structure at the end of 2021, 72.2% corresponded to ruble obligations, 27.2% to foreign currency obligations. The currency breakdown approximately corresponds to the company’s revenue structure, which allows minimizing currency risks.

Brief summary: the debt burden is gradually decreasing, debt refinancing allows you to reduce interest costs and increase profits. An increase in capital expenditures is not expected in the near future; the FCF indicator is growing, increasing the dividend base.

Dividend policy

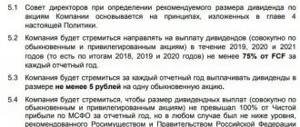

At the beginning of February 2021, ChelPipe approved a new dividend policy. Payment of dividends is planned at least twice a year. The procedure for calculating dividends depends on the ratio of net debt to EBITDA.

– The company plans to allocate at least 100% of net profit under IFRS or free cash flow to dividend payments, whichever is greater if the net debt/EBITDA ratio is less than 1.5x;

– The Company intends to allocate for dividend payments at least 70% of net income under IFRS or at least 100% of free cash flow, whichever is greater if the net debt/EBITDA ratio is greater than or equal to 1.5x and below 2.5x;

– The Company intends to allocate at least 50% of IFRS net income or at least 75% of free cash flow to dividend payments, whichever is greater if the net debt/EBITDA ratio is greater than or equal to 2.5x and below 3.5x;

– If the net debt/EBITDA ratio is greater than or equal to 3.5x, the recommendation to pay dividends remains at the discretion of the board of directors;

The new dividend policy will be applicable for the calculation of dividends for the full year 2021 and beyond.

In the presentation on the results of 2021, the company also announced that as part of the new dividend policy, a minimum level of payments was established in 2020-2021. at a level of at least 7.5 billion rubles. Based on the results of the first half of 2021, 9.82 rubles have already been paid. per share.

Thus, based on the results of the second half of 2021, at least 14.7 rubles must be paid. per share. The dividend yield in this case could be 7.7%.

At the same time, based on the adopted dividend policy, payments at the end of the year should be higher. At the end of 2021, the net debt to EBITDA ratio was at 2.1x. This means that 100% of free cash flow can be used for dividends at the end of the year. In terms of per share, this implies RUB 26.6. minus 9.82 rubles paid. and assumes 13.9% dividend yield for the second half of the year.

The dividend yield looks impressive, but there is a factor that can reduce the potential payout.

Additional placement of shares

In an interview with Vedomosti, Andrei Komarov, Chairman of the Board of Directors and the largest owner of ChelPipe, said that if favorable conditions develop, the option of additional placement of shares on the stock exchange may be considered. Regarding the volume of supply, Komarov noted that investors usually focus on placing 25% of the share capital.

In recent years, ChelPipe's investment case has noticeably improved: the company began paying dividends, reduced its debt burden, and increased the predictability of its dividend flow. All this can be regarded as consistent steps to increase the attractiveness of the company's shares for investors and preparation for additional placement.

At the end of December 2021, ChTPZ approved a decision on an additional issue of shares in the amount of 76.4 million shares, which is exactly 25% of the capital.

It can be assumed that when market conditions stabilize, the company will conduct an additional placement, diluting capital. In such a situation, potential dividends per share may be reduced. At the same time, the issue of shares can increase the liquidity of trading, which should have a positive impact on investors’ attitude towards the asset and market capitalization. In addition, the additional placement will help raise capital to further reduce the debt burden.

At the moment, it is difficult to predict when additional placements might take place. Before the stock market crash, the environment was favorable for attracting capital, but now the timing may be postponed for an indefinite period.

If an additional 76.4 million shares are placed, dividends per share may be reduced to RUB 9.8. upon payment of the minimum specified 7.5 billion rubles. or up to 19.3 rubles. per share upon payment of 100% of FCF. The dividend yield in the first case can be 5.1% , in the second - 10.1%.

In our opinion, the most likely scenario is the payment of 100% of the FCF while maintaining the same number of shares, that is, 26.6 rubles. per share. It is important to say here that the option is the basic one in the event that volatility in the stock markets continues until the payment of dividends, and the company will have to postpone the additional placement. If the markets stabilize faster and the placement is made, then you should focus on 19.3 rubles. per share.

In 2021, in the worst-case scenario, with an additional placement and payment at the minimum level, dividends could amount to 19.2 rubles. per share, which corresponds to a 10.3% dividend yield at current quotes.

Important points

A significant disadvantage of ChTPZ shares is their extremely low liquidity. The average daily trading turnover over the past year is about 2 million rubles, for comparison, the same figure for its closest competitor TMK is approximately 115 million rubles. Entering and exiting securities in low liquidity conditions can be difficult.

Important: the pipe products market may come under pressure from the collapse in oil prices and the consequences of the fight against the spread of coronavirus. In the face of reduced economic activity and lower energy prices, many oil and gas companies will reduce investment programs, which could lead to a drop in demand for pipe products from oil producing companies. The company's diversified profile can partially mitigate the negative effect - 33% of revenue comes from the oil segment. Another 30% and 37% of revenues are generated by the gas and industrial segments.

It is also worth noting that Gazprom’s major projects: Nord Stream 2, Power of Siberia, in which ChTPZ participated in 2021, have been completed or are close to completion. This means that locally, LDP sales may decline in 2021 against the backdrop of a high base for 2021. Some of the lost volumes may be offset by repairs of existing pipelines.

“We have a huge number of kilometers of pipelines, they were increasingly implemented in the 1970–1980s. The cycle of repair and maintenance needs is suitable. We see quite a lot of demand there,” noted the head of the company, Boris Kovalenkov, in March 2020, reports Reuters.

Let's sum it up

ChelPipe is a promising dividend stock with the potential to reduce debt burden and increase profits. The expected dividend yield in 2021 exceeds the market average.

The end of the investment cycle assumes that the company's free cash flow will increase, which, with the current dividend policy, can lead to an increase in dividends.

The main problem that reduces the attractiveness of shares is low liquidity. However, after additional placement the problem can be solved. An increase in liquidity and free-float can have a positive impact on the attractiveness of ChelPipe for large investors who, in the current realities, cannot enter into the paper. It is quite possible that the negative effect on the profitability of securities from dilution of the capital of existing shareholders will be much less than the positive effect from the influx of investors and capitalization growth.

The uncertainty in ChelPipe's investment case is also related to the current situation on the oil market. If low prices persist in the medium term, demand for the company's products may decline, which could negatively affect profits and dividends. However, from the February highs, shares fell by 19.4% - on par with the market as a whole, partially incorporating a negative scenario into the quotes.

BCS Broker

Where and how to buy shares today

Shares of the ChTPZ group can be bought/sold on stock exchanges through intermediaries - brokers who make transactions on behalf of clients. To purchase shares you will need to follow the following sequence:

- choosing a broker with suitable conditions;

- contacting him and concluding an agreement;

- refill;

- selection and purchase of securities.

After the transaction, you are the official owner of the securities and can count on dividends. It is better to use trusted brokers to protect yourself from scammers.

Through a Russian broker

There are a number of reliable domestic brokers through which you can purchase securities not only from Russian issuers, but also from foreign ones. I have selected the most reliable, proven Russian brokers for you.

Reliable Russian brokers

| Name | Rating | pros | Minuses |

| Finam | 8/10 | The most reliable | Commissions |

| Opening | 7/10 | Low commissions | Imposing services |

| BKS | 7/10 | The most technologically advanced | Imposing services |

| Kit-Finance | 6.5/10 | Low commissions | Outdated software and user interface |

Via bank

Most banks are not involved in the stock market, but some banks are engaged in the sale of securities, although this is associated with additional costs.

Buying shares through a bank is quite simple today. It is enough to come to a credit institution that deals with stock trading and get acquainted with its offers. Here is a list of banks where you can purchase ChelPipe shares.

Directly from a company, individual or firm

Theoretically, it is possible to buy shares directly from the issuer; in this case, you do not need a broker, but there are pitfalls:

- If shares are lost, their restoration will be impossible, as will the right to them.

- Shares purchased from the issuer have a fixed price, that is, when the transaction is completed, it has already been determined and trading is impossible.

An over-the-counter option is available to purchase shares from individuals or organizations. There are also risks here: it is one thing to conclude a transaction with an acquaintance, and quite another to buy from unverified persons, especially if the cost is disproportionately low. There is a high probability of encountering scammers.

Dividends on ChelPipe shares in 2021 - size and register closure date

Home → Dividends→ Shares of ChTPZ JSC - forecast, payment history

A table with the full history of dividends of the ChelPipe company, indicating the amount of payment, the date of closure of the register and the forecast:

| Payment, rub. | Registry closing date | Last day of purchase |

| 17.95 | June 15, 2021 | 11.06.2021 |

| 8.18 | June 15, 2020 | 10.06.2020 |

| 4.37 | January 9, 2020 | 07.01.2020 |

| 15.38 | July 9, 2019 | 05.07.2019 |

| 11.56 | May 10, 2018 | 07.05.2018 |

| 10.05 | May 10, 2017 | 05.05.2017 |

*Note 1: The Moscow Exchange operates on the T+2 trading system. This means that settlements for buying and selling shares occur within 2 business days. Therefore, to be included in the register of shareholders and receive dividends, you must be a shareholder 2 days before the cutoff.

*Note 2: Exact payout date varies by broker and issuer. The predicted nearest date for receipt of dividends to the brokerage account for the company ChTPZ JSC: June 28, 2021.

Total dividends of ChTPZ JSC shares by year and change in their size compared to the previous year:

| Year | Amount for the year, rub. | Change, % |

| 2021 | 17.95 (forecast) | +43.03% |

| 2020 | 12.55 | -18.4% |

| 2019 | 15.38 | +33.04% |

| 2018 | 11.56 | +15.02% |

| 2017 | 10.05 | n/a |

| Total = 67.49 |

The amount of dividends paid by ChTPZ JSC for the entire period is 67.49 rubles.

Average amount for 3 years: 15.29 rubles, for 5 years: 13.5 rubles.

You can buy shares of ChTPZ JSC with minimal commissions from stock brokers: Finam and BCS. Free deposits and withdrawals. Online registration.

Brief information about the issuer ChTPZ PJSC

| Sector | Metals and mining |

| Issuer's full name | "ChTPZ" PJSC JSC |

| Issuer's name is short | ChTPZ JSC |

| Ticker on the stock exchange | CHEP |

| Number of shares in lot | 10 |

| Number of shares | 305 696 336 |

| Free float, % | 7 |

Other companies from the Metals and Mining sector

| # | Company | Div. profitability for the year, % | The nearest registry closing date | Buy before |

| 1. | ALROSA JSC | 14,99% | 04.07.2021 | 30.06.2021 |

| 2. | NLMK JSC | 14,91% | 09.06.2021 | 07.06.2021 |

| 3. | MMK | 11,80% | 17.06.2021 | 15.06.2021 |

| 4. | TMK JSC | 10,87% | — | — |

| 5. | SevSt-ao | 10,31% | 01.06.2021 | 28.05.2021 |

Calendar with upcoming and past dividend payments

| Immediate | Past | ||||

| Company Sector | Size, rub. | Registry closing date | Company Sector | Size, rub. | Registry closing date |

| RusAqua JSC Foodstuff | 5 | 27.05.2021 | MDMG-gdr Miscellaneous | 19 ✓ | 25.05.2021 |

| FGC UES JSC Energy | 0.016 | 29.05.2021 | TransK JSC Logistics | 403.88 ✓ | 24.05.2021 |

| SevSt-ao Metals and mining | 46.77 | 01.06.2021 | M.video Retail trade | 38 ✓ | 18.05.2021 |

| Tattel. JSC Telecoms | 0.0393 | 01.06.2021 | PIK JSC Construction | 22.51 ✓ | 17.05.2021 |

| SevSt-ao Metals and mining | 36.27 | 01.06.2021 | PIK JSC Construction | 22.92 ✓ | 17.05.2021 |

| GMKNorNik Metals and mining | 1021.2 | 01.06.2021 | Moscow Exchange Finance and Banking | 9.45 ✓ | 14.05.2021 |

| MOESK Energy | 0.0493 | 01.06.2021 | Sberbank Finance and Banking | 18.7 ✓ | 12.05.2021 |

View full calendar for 2021 »

7 Best Dividend Stocks for 2021

| # | Company | Sector | Dividend yield for the year, % | The nearest registry closing date | Buy before |

| 1. | Surgnfgz-p | Oil Gas | 16,84% | 20.07.2021 | 16.07.2021 |

| 2. | iMMTSB JSC | Miscellaneous | 15,24% | 09.06.2021 | 07.06.2021 |

| 3. | Unipro JSC | Energy | 15,08% | 22.06.2021 | 18.06.2021 |

| 4. | ALROSA JSC | Metals and mining | 14,99% | 04.07.2021 | 30.06.2021 |

| 5. | NLMK JSC | Metals and mining | 14,91% | 09.06.2021 | 07.06.2021 |

| 6. | Rusagro | Food | 11,85% | 18.09.2021 | 15.09.2021 |

| 7. | MMK | Metals and mining | 11,80% | 17.06.2021 | 15.06.2021 |

View the full company rating for 2021 »

Interesting read:

- How to buy shares as a private person;

- How to start trading on the stock exchange - a guide;

- How to make money on stocks;

- Investment portfolio - how to create it;

- How many shares do you need to buy so that you can live on dividends?

- How to buy Gazprom shares and receive dividends;

- What does stock return consist of?

- Investing in shares - step-by-step instructions;

← Return to main catalog

What affects the stock price

The price of shares is influenced by the following factors, divided into 3 main groups:

- Events taking place in the entire market as a whole.

- Events taking place in the industry.

- Results of work and prospects of the company itself.

There is an unspoken rule among brokers: 30 – 30 – 40. Events in the market itself determine 30% of the value of shares, the situation in the industry - 30%, the work of the company itself - 40%.

Company prospects

ChelPipe has mastered the production of innovative products - pipes and connecting parts using laser welding. It was the first among domestic companies to begin producing import-substituting products - split tees, which make it possible to repair pipelines without stopping the pumping of gas or oil products.

These facts indicate the company's potential. Already today, the company is rightfully the leader in the Russian Federation in the production of pipeline products, and also has everything necessary to climb to the world Olympus.

Analytics and forecast for the security

I believe that in the near future the development of ChelPipe will allow its shareholders to receive a decent profit. The demand for steel pipes is growing: according to statistics, over the past 15 years, sales volume has increased by 60%. Among the company's products there are products that have no analogues throughout the world.

Alternative in this industry

In addition to ChTPZ, the main players in the pipe rolling market today are two more domestic companies - the Pipe Metallurgical Company and the United Metallurgical Company. Certain shares of the Russian market are occupied by the Izhora Pipe Plant and the Ukrainian one.

The thing is a pipe. Will ChTPZ become an example of replaying the privatization of the 90s?

The largest Russian manufacturer of pipes for the oil and gas industry - the Chelyabinsk Pipe Rolling Plant group (the largest assets are the plant of the same name in Chelyabinsk and the Pervouralsk Pipe Rolling Plant in the Sverdlovsk Region) - may come under the control of structures close to Gazprom. This story mixed everything - pipes, gigantic money, the interests of business owners from the top lines of Forbes, the names of famous leaders who are traditionally called Vladimir Putin’s .

Nakanune.RU collected all available information about the largest transaction on the pipe market, talked with market participants and also presents its own version of the development of events.

K and F sat on the pipe

The ChelPipe Group is one of the ten largest manufacturers of pipe products in the world. The predecessor of the now private holding was a state enterprise - the Chelyabinsk Pipe Rolling Plant, founded in 1942 on the basis of the Mariupol Pipe Plant evacuated to Chelyabinsk. It was transformed into a joint-stock company in 1993 and subsequently privatized. The owners of the group are the former senator from the Chelyabinsk region, chairman of the board of directors of PJSC ChTPZ Andrey Komarov and shareholder of PJSC ChTPZ Alexander Fedorov , both Chelyabinsk residents by place of birth or training and future career. In December 2008, ChTPZ acquired 100% of the shares of another once state-owned asset - Sverdlovsk PNTZ. This, in short, was the way to privatize a large piece of state property in the pipe industry.

In the future, we must pay tribute, the owners did not squeeze the cream out of the assets and carried out a serious modernization of the enterprises, in particular, they launched at ChelPipe the “white metallurgy workshop” that became famous throughout the country - “Vysota 239” , where it is not a shame to bring the president. In general, Komarov and Fedorov’s career and business as a whole developed along an upward trend. At the same time, the construction of a new workshop worth $880 million is also considered to be a starting point for the company’s problems. The whole point was that the group was heavily indebted.

Rumors about the sale of part of the stake in Chelyabinsk Pipe Rolling are indirect, because all participants in the proposed transaction are the shareholders of ChTPZ, top managers of Gazprombank and the owners of Zagorsk Pipe Cinderella of the pipe industry

The RBC publication, without disclosing sources of information, insists that the interested parties in the acquisition of a large stake in ChTPZ are the owners and top managers of ZTZ. The plant, which in just a few years took over the initiative from Russian pipe manufacturers in the production and especially supply of LDP.

ZTZ today claims to be the main supplier for Gazprom and the main Russian oil companies. At the same time, Safin (by the way, almost everyone is inclined to regard him as a “nominee”, and among the real business owners there are even more prominent names) and his Zagorsk plant are pursuing a very, very aggressive policy of buying up assets in the industry.

Last winter, for example, it was reported about negotiations between the owners of ZTZ and Alisher Usmanov , who today supposedly prefers to spend most of the year outside Russia and is focused on leading the World Fencing Federation (FIE). The purpose of the negotiations is the purchase of Denis Safin's ZTZ Ural Steel by Usmanov, which is a specialized plant for the production of pipe blanks, strips and other items. At that time, analysts estimated the possibility of selling Ural Steel at approximately 32 billion rubles; whether the deal took place and what package Safin could receive is still unknown.

Many have wondered and are wondering - where did the owner of a small, for the time being, enterprise near Moscow get the money for such expenses and purchases? And why are the leaders of the Russian banking sector such as Sberbank and VTB ready to lend and then finance Safin to buy up assets and create production facilities, the products of which, let’s say, are not really needed by the market due to the presence of other players on it for a long time and firmly? Many have asked and are still asking a reasonable question: how did this even become possible?

The rise of the prospects and opportunities of the owners and beneficiaries of ZTZ, an enterprise that actually began to be built only in 2014 and carried out the first commercial shipment of pipes in 2015, was similar to the classic story about Cinderella, where the last one was known until recently only to a narrow specialists from a small factory near Moscow, and as the “prince” - Gazprom and its long-term leader Alexey Miller .

As the press service of ZTZ explained to us, the business of the enterprise is “production of large diameter pipes at an objective cost.” The owner of ZTZ was and is now businessman Denis Safin, who in 2017 was caught in a criminal case for fraud with subsidies from the Russian Ministry of Industry and Trade. As business media reported at that time, the amount of damage seemed to be estimated at a relatively small amount - just over 133 million rubles, but, for obvious reasons, Safin could move from his office to a completely different place even for such an act. However, here comes the partner of the law firm “Egorov, Puginsky, Afanasiev and Partners” Nikolai Egorov , who is called “Putin’s classmate” and one of the most influential Russian lawyers in the business sphere.

This legal structure was created back in 1993, now has an extensive network of branches from Moscow and Kyiv to London, and specializes in supporting large businesses. In short, entrepreneurs and businessmen of more or less high profile, officials of various departments and ministries in Moscow, are well aware of the lobbying abilities of representatives of this bureau. This, as they say, is for understanding... And also for understanding - Egorov was named among the co-owners of ZTZ.

contracts worth 13 billion rubles from Gazprom .

In general, as our interlocutors say (the interlocutors make assumptions and, for obvious reasons, do not want to identify themselves), even large and long-standing players in the pipe industry market at that time did not quite understand the scale of the danger that threatened them. Like a bolt from the blue, at the end of the same 2021, the decision of the Gazprom board to cancel the tender for the supply of OCTG in the amount of 60 billion rubles . As a result, a rumor spread throughout the market that Gazprom (that is, Miller) was going to transfer an order for 41 (out of a 60 billion tender!) billion rubles. for the supply of pipes specifically to ZTZ, which, to put it mildly, caused misunderstanding and shock among other long-established players in the industry.

The further fate of this amazing contract turned out to be classified, but we don’t need these details now. We simply provided open source data and data gleaned from informal conversations to convey the atmosphere in the pipe market recently.

It's time to return to ChelPipe and the strategy of Andrei Komarov himself, who supposedly has been looking for and is looking for investors for his business for some time (in).

Won't a mosquito hurt your nose?

54-year-old Andrei Komarov himself is a very remarkable personality and, probably, perfectly fits the definition of successful businessmen from the galaxy of the early 90s of the last century and the beginning of the present century. Like many people of his generation, he was engaged in business in Moscow, including trade in rolled metal, until in 1996 he became deputy director of Chelyabinsk Pipe Rolling Plant OJSC. One way or another, after a few years, Komarov becomes the head of this pipe giant, having managed to consolidate, according to some sources, up to 80% of the shares of ChelPipe to himself and his offshore companies! For five years, in 2005-2010, Komarov became the governor’s representative in the Federation Council of Russia; the governor of the Chelyabinsk region was then the late Pyotr Sumin . The status of a senator is already, as you understand, the “major league” in the Russian power elite, of course, not in terms of powers and capabilities, but this is exactly what a status is.

Let us repeat, both in Moscow (for example, in line ministries), and in the homeland of his main asset in Chelyabinsk, and in general in the Urals, Komarov’s business was excellent during this period; he carried out a whole series of successful transactions for the sale of non-core assets. So, in 2009, Komarov sold to Igor Altushkin and Andrey Kozitsyn a package of “Chelyabinsk zinc self-made-man,” as the Americans put it, only in the Russian version, well, adjusted for the national characteristics of privatization in the 90s.

In March 2014, employees of the Main Directorate for Combating Economic Crimes and Anti-Corruption of the Ministry of Internal Affairs . The position of the prosecution at that moment was very confusing, including points about alleged fraud with money allocated to maintain mobilization capacities at the enterprise; we fully indicated the name of the law enforcement unit so that the reader could understand the level of the persons who put forward claims against Komarov at that moment. The following summer, 2015, it got to the point that the Prosecutor General’s Office refused to approve the charges brought against him; later, by the way, the investigators themselves were held accountable for falsifications in the case, etc. In a word, the whole “Komarov case” strongly resembles a banal “assault.”

To summarize all of the above (and also leaving behind a number of other, no less important circumstances), in the summer of 2021 ChelPipe withdrew its pipe service in its subsidiary Rimera-Service from the pipe division. Around this time (summer - autumn 2019), vague rumors began to spread around the market about Komarov’s possible sale of part or the entire business to third-party structures.

The fact is that in different years, it has been known about this since at least 2011, Komarov was one way or another looking for buyers for his ChTPZ asset. I tried to go public to pay off the company’s debts, which arose due to measures to modernize production, then the crisis of 2008-2009, etc. Negotiations were and are being conducted with the aim of restructuring ChelPipe’s external debt, the size of which is not known for certain, but still represents an impressive amount. Perhaps today, through the “leader” in the pipe market, that is, ZTZ Denis Safin, Andrei Komarov found the most profitable option to exit the business? The whole question, of course, is the price for the company that Komarov wants to get.

Still, the general state of the global and Russian economy, the presence of competitors, the pandemic, the curtailment of large-scale projects and the fall in demand for oil and gas, whatever one may say, “hit” the price of any asset. On the other hand, if a large-scale redistribution has really begun in the Russian pipe market in favor of as-yet unnamed beneficiaries using all business methods (from forceful to anti-competitive), perhaps it really makes sense to get rid of the asset at least for some real cost.

Without “closing” the deal

To be fair, it is worth noting that, in fact, the Russian pipe market, due to historical reasons, has indeed become super-competitive since the early 2000s, and the built/modernized capacities of Soviet enterprises at some point began to greatly outstrip the needs of gas and oil workers. Large gas projects such as Nord Stream (first line), Eastern Siberia - Pacific Ocean (ESPO) and smaller ones provided income to all pipe workers in one way or another; later plans appeared for the unrealized Bulgarian Stream and the completed Turkish Stream...

It is no coincidence that the same Komarov, back in 2002, created and headed the Pipe Industry Development Fund, which at one time tried to act as a kind of “regulator” of the market, however, without success. What kind of regulation can there be if so many players in the industry with good opportunities and money are annually “cut” for multi-million and multi-billion dollar contracts? There is no middle ground in such disputes, either you received a contract and “lost” your competitor, or he beat you, or you were both left out because of someone else.

Literally in June, Nakanune.RU talked about an inspection of the Russian Antimonopoly Service (FAS) regarding a complaint about the largest purchase of pipes by Gazprom in the amount of over 95 billion rubles. Interestingly, based on the results of consideration of applications, top managers of the gas monopolist this time made a truly “Solomon” decision, recognizing all... five companies as winners. The proportions in the deal are not disclosed, but the claims of any of the pipe suppliers are not yet known.

Analysts from the industry magazine Neftegaz.RU recently cited two reasons for the current state of affairs: increased competition and a shrinking market for large-diameter pipes (LDP). According to the calculations of Komarov’s Pipe Industry Development Fund, orders for pipe supplies from Gazprom in 2021 could be reduced by 10% (the forecast was made even before the pandemic and the fall in commodity prices!), from 2.09 million to 1 .8 million tons.

Then the reader can predict for himself who, in the conditions of market redistribution, will miss those almost 0.3 million pipes in the form of orders, and who may be forced to sell the main asset.

However, not everything may be as gloomy with the market and the division of orders on it, as it seems at first glance. Refusing to assess the situation on the pipe market, Alexey Gromov , head of the energy department of the Institute of Energy and Finance Foundation, pointed out to us that high-profile projects for 2021 are not closed at all. Bearing in mind the situation, first of all, with the completion of the Power of Siberia and, naturally, with the long-suffering Nord Stream 2 .

“We will have to sharply accelerate the Power of Siberia project due to problems with the supply of gas from the Chayandinskoye field to the pipeline; without connecting the Kovyktinskoye field, the project has now turned out to be “non-working.” And the Chinese side quite rightly makes claims, and this is geopolitics,” the expert noted.

The interlocutors are confident that due to the need for urgent completion of the Power of Siberia, as well as the resumption of work on Nord Stream 2, apparently, a significant “subsidence” of the pipe market will not occur. Plus renovations and those projects that have been launched and about which all the professionals say that “it’s easier to complete them than to abandon them in the middle.”

“I said and continue to say that we have entered a new era, the era of neo-mercantilism. Where both the size of the business and the connection of this business with the top of the bureaucracy are very important. In order to become stronger in the external market, we need to capture the internal one, elements of which we are seeing today,” says Vasily Koltashov , head of the Center for Political Economic Research at the Institute of a New Society.

The interlocutor recalls that what is happening is partly reminiscent of President Roosevelt forced mergers and consolidation of businesses was created in the United States , which, for obvious reasons, did not and could not please many businessmen and bosses.

“We are moving in the same direction, but it is necessary to understand that in this new system of neo-mercantilism, not everyone will have a place in the Sun. Especially for characters from the previous, neoliberal era, when capital was amassed and assets were acquired for next to nothing,” the interlocutor adds, explaining that he does not mean the specific situation only with the sale of ChelPipe.

Vladislav Zhukovsky , an expert in economics, a member of the presidium of the Stolypin Club, sees the pending “deal of the century” in the pipe industry somewhat differently.

“I think we are seeing some oligarchs from the Forbes list being “devoured” by others who are more successful and influential today. It’s simple - resources in the food chain are declining, due to the crisis, no growth in the Russian economic system is expected for the next 5-7 years, so there is naturally a concentration of capital, a concentration of assets by people whose names we all know very well. I mean those who have recently been implementing the most large-scale projects in the oil and gas industry and infrastructure construction,” says the expert.

According to him, businessmen from the “ten” or “twenty” richest people in the country have seriously paid attention to the business of regional oligarchs or those who are inferior to them in financial capabilities or influence in government and security structures. And since the ruling elite does not yet have clear recipes for solving the crisis, this tendency to replay the results of the privatization of the “big companies” of the 90s will, apparently, only increase.