Thermal coal

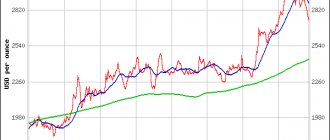

In the first quarter of 2021, the downward trend that formed in the summer of 2021 on the global thermal coal market continued. After almost three years of growth, the coal market has turned around and is currently characterized by an unfavorable price environment.

Average quarterly quotations of thermal coal in key world ports showed another decline both quarterly and year-on-year. Thus, according to the results of the first quarter of 2021, quotations of Australian thermal coal (FOB Newcastle) dropped to $95 per ton (-6.9% y/y). The average quarterly price for Russian thermal coal (FOB Vostochny) was $94 per ton (-6.9% yoy), for South African coal (FOB Richards Bay) - $85 per ton (-10.2% yoy .), for Colombian coal (FOB Bolivar) - $72 per ton (-13.0% y/y).

The fundamental factors of supply and demand and market imbalances in one direction or another remain decisive for the thermal coal market. The geographic centers of the coal market are China and India, and the Asian region as a whole, where market participants primarily look and where the main trade flows are formed.

China. Coal production in China increased by 0.3% year-on-year in the first quarter of 2021. - up to 812 million tons. The output of thermal power plants increased by 2% year-on-year, hydroelectric power plants – by 12%, nuclear power plants – by 26%, renewable energy sources (wind, solar) – by 7%. Coal imports decreased by 1% y/y. and amounted to 74.63 million tons. However, if the import of thermal coal decreased to 58.21 million tons (-8% yoy), then the import of coking coal, on the contrary, increased to 16.42 million tons (+36% yoy).

Coal reserves at Qinhuangdao, the main transhipment port in North China, have increased from 5.65 million tons since the end of December 2021 to 6.4 million tons at the end of March 2021. As of March 2021, the reserves were 6.35 million tons. The total inventories in North China's main seaports of Caofeidian, Qinhuangdao and Jingtang amounted to 16.2 million tons at the end of March 2021, up 2 million tons from March 2021.

Delays in customs clearance of Australian coal at ports persist in China, which market participants believe is a consequence of deteriorating bilateral political relations between Canberra and Beijing in recent years. In addition, China uses coal import restrictions as a tool to regulate domestic prices (when domestic prices are high, restrictions are relaxed to help the domestic energy market; when domestic prices are low, import restrictions are tightened to support Chinese producers).

India. Coal production in India increased by 1.7% YoY in Q1 2021. - up to 207 million tons. Coal imports also increased to 46.6 million tons (almost +4% yoy). Increased production, decreased demand (decrease in thermal power plant output) and increased coal imports led to a rapid increase in fuel reserves. Total power plant inventories increased from 16.6 million tonnes at the end of December 2021 to 30.9 million tonnes at March 2021.

India summed up the results for 2018-2019 (Apr.18 - Mar.19): coal imports increased to 233.56 million tons (+8.8% yoy), including energy - 164.21 million tons (+13% y/y, 144.99 million tons), coking – 47.73 million tons (47.22 a year earlier).

At the same time, the state corporation Coal India is negotiating with the country's power plants on plans to reduce coal imports in order to replace imports with domestic supplies.

Coal imports to Japan and South Korea in the first quarter of 2021 decreased by 6.5% and 5.4% year-on-year, respectively.

Europe. Coal reserves in the ARA (Amsterdam-Rotterdam-Antwerp) region stood at 6.8 million tonnes at the end of March 2021, up from 6.5 million tonnes at the end of 2021. The increase in reserves is due to a warm winter in the region. In March 2021, coal reserves at regional terminals were estimated at 4.1 million tons. Thus, inventories are currently at their highest level since 2013.

Forecast of world prices for thermal coal

Short-term forecast. The average price for thermal coal on delivery terms FOB Australia (Newcastle) was $95 per ton in the first quarter of 2019. According to the consensus forecast of banks, during 2019 thermal coal quotations will be stable, with average quarterly values not falling below $90 per ton. However, for now the situation is developing rather according to a pessimistic scenario.

Thus, at the beginning of April 2021, thermal coal prices recorded the sharpest decline since the global financial crisis of 2008/2009. (up to 20%), the lowest level since May 2017.

The drop came days after Glencore and Japan's Tohoku Electric Power reached an agreement to supply Australian thermal coal from April 2021 to March 2020. The companies agreed on a fixed price of $94.75 per tonne of premium Australian coal ($109. 77 per ton in October 2018). This price is a reference point for other companies in negotiations this year.

According to market participants, the decline also occurred against the background of a slowdown in industrial production in Asia, Europe and North America, which raises concerns about a possible global recession.

In addition, the decline in coal prices followed a 60% drop in prices in Asia for liquefied natural gas (LNG), which is a direct competitor to coal as a fuel for thermal power plants.

High coal reserves in both Asia and Europe also put pressure on coal prices.

After the collapse of coal prices in early April 2021, the expected correction took place in the market. Subsequently, thermal coal prices remained stable. As a result, at the end of April 2019, the average price for thermal coal on terms of delivery FOB Australia (Newcastle) was just over $86 per ton, and in May prices remained at $85 per ton.

The short-term forecast for thermal coal prices remains bearish. Factors: Rainy weather in China, which will ensure strong performance in hydropower in the coming months, accumulated coal reserves in India and Europe, low gas prices in Europe due to warm winter and high storage stocks, Ramadan in Muslim countries (decline in trade activity from buyers in the B.Vostok). The stock could be supported by cool weather in North-West Europe (lower wind and solar generation), increased imports to China to replenish inventories ahead of the summer (in addition, Chinese power plants will adhere to a new strategy: replenish stocks throughout the year to avoid purchasing during the peak season, especially during the replenishment period in the fourth quarter), India will intensify purchases of imported coal ahead of the monsoon season. The high probability of seasonal deterioration in weather (rainy season) in the mining regions and planned repairs of railway tracks may also support quotes. During the month-long Ramadan period, which began on May 6, Indonesia's coal production will fall 10-20% from the previous month, which could also help keep thermal coal prices stable.

Long-term forecast. We can talk about weak price forecasts for thermal coal in the medium and long term against the backdrop of growing domestic fuel supplies in China and India, an increase in the share of nuclear energy in Japan and South Korea, and the abandonment of developed economies from coal generation in order to reduce emissions. Uncertainty in commodity markets is caused by the ongoing trade war between the United States and China, the mutual introduction of new import duties on goods, uncertainty regarding Chinese port restrictions on coal imports, as well as tightening environmental policies.

Coking coal

In the first quarter of 2021, coking coal prices remained at fairly high levels, although they showed a decline both quarterly and year-on-year. Thus, at the end of the first quarter of 2021, the average price of hard coking coal delivered from Australia (FOB DBCT) was $181 per ton, which is 5.4% lower than the same figure in the first quarter of 2021. The cost of premium grades was $206 per ton, decreasing by almost 10% year-on-year.

At the beginning of 2021, prices for coking coal were supported by strong demand for imported raw materials from Chinese consumers (after the lifting of import restrictions established in November 2018), a return to purchases by Indian metallurgists who had lost hope of cheaper raw materials, as well as temporary disruptions with supplies from Australia.

The rise in quotations at the end of January, following the prices of other metallurgical raw materials, primarily iron ore, was the result of a disaster in Brazil, when a break in the tailings dam of the Corrego do Feijao mine led to large casualties and the shutdown of a number of enterprises of the Vale corporation, which caused a stir on world raw materials markets.

However, at the same time, it became known about problems and delays with customs clearance of Australian coal in Chinese ports. This fact brought negative sentiment to the market. Amid restrictions on imports of Australian coal, Chinese companies are abandoning purchases under long-term contracts and are switching to domestic sources or purchasing raw materials in Mongolia, Russia and North America. If China continues its policy towards Australian coal, Australian suppliers will face serious sales problems.

In March, low coke prices in China put pressure on coking coal prices. After the winter, metallurgists accumulated large stocks of coke, which resulted in a decrease in demand and prices for raw materials. Then the market experienced a sharp correction and price recovery. Volatility in the Chinese coke market may help keep domestic prices high, while rising steel production in China this year will boost import demand.

It should be noted that at the end of the first quarter of 2021, global steel production amounted to 443 million tons, which is 4.3% more than a year earlier. However, the growth of the indicator was ensured by China. In the first quarter of 2021, China increased its steel production by 9.4% year-on-year. – up to 229.9 million tons, despite production restrictions in winter to reduce air pollution (softer restrictions than a year earlier). The current increase in steel production in the country worries even Chinese steelmakers themselves, who fear excess supply and the resulting fall in prices on the domestic market.

Forecast of world prices for coking coal

Short-term forecast. In the first half of April 2021, prices for coking coal decreased, following prices for basic metallurgical raw materials against the backdrop of a stagnant steel market. Further, prices strengthened against the backdrop of a price rally for metallurgical coke on the Chinese domestic market.

Currently, the Vale corporation has not been able to return to operation the capacities that were stopped after the accident at the beginning of this year. This again pushes up prices for iron ore and other metallurgical raw materials, including coking coal. Adverse weather conditions limiting exports from Australia also help.

At the same time, the slowdown in the global economy and weak demand for steel products do not support the growth of commodity prices.

In general, for the second quarter of 2021, banks predict that current price levels will remain the same or even slightly increase relative to the first quarter. The rise in coking coal prices will be driven by demand for replenishment of reserves from China and India to meet the needs of steel producers. However, in the third and fourth quarters of this year, we should expect a decline in quotes by 4-5% to current levels.

Long-term forecast. After a strong 2021, the global economy is slowing, with global trade showing signs of weakening and manufacturing slowing in the US, Europe and China. Markets for metallurgical raw materials will contract due to the cyclical downturn and concerns about political uncertainty.

When setting world prices for coking coal, the main factors will be the relationship between supply and demand for coking coal in key markets in Asia and Europe, the results of the trade war between the US and China, China and Australia, the US and Turkey, the expansion of protectionist practices on the part of China and India for import substitution of coal supplies. World prices are traditionally influenced by prices for coking coal, coke and steel on the Chinese domestic market.

In the long term, an increase in supply and a decrease in demand for imported raw materials in China (the transition to local coal) will lead to a decrease in world prices for coking coal. According to bank forecasts, in 2021 the price will drop to $161 per ton, in 2021 – to $152 per ton. However, in the next 2 years, strong demand will keep quotes from falling to the lows of 2015-2016. Steel production will be stable in 2021 and will begin to decline in 2021 on expectations of slower global economic growth.

Parameters and designation

The main exporters of coking fuel in the world are the USA and Australia. Therefore, as the main price reference, we will consider coking coal futures traded on the CME.

| Security | Area | Contract type | Tickers | Months |

| CME Globex: ACM CME ClearPort: ACM | CME Globex CME ClearPort ICE | Settlement/delivery | ACM | FGHJKMNQUVXZ |

| CME Globex: MFF CME ClearPort: MFF | MFF |

On which exchanges can this futures be traded?

The coking coal futures in question are traded on the Chicago Mercantile Exchange (CME). Initially, this trading platform focused on agricultural goods, but today it covers many areas (and in particular energy).

Following the acquisition of CBOT and NYMEX, the Chicago Exchange became the largest trading platform in the world, executing tens of millions of trading contracts per day.

Advantages and disadvantages of this futures

An important advantage of a coal futures contract is the forward rate. That is, the futures are purchased at the current price, and the exchange is made on a predetermined date. Therefore, the asset can be used both for speculation and for hedging risks.

Other advantages of coking fuel futures:

- simple transaction scheme

- leverage

- relatively high liquidity of the asset (coking coal is used in the energy sector, metallurgy, chemical industry and many other areas)

- guaranteed fulfillment of obligations.

Disadvantages of coking fuel futures:

- low growth potential (futures for it are not the best choice for long-term investments)

- complex forecasting (demand depends on many factors, so it is difficult to predict the exact price movement).

Indicators of the Russian coal market

Let's summarize the main results of 2021:

— Russia’s share in world coal production (preliminary) is 5.4%. Russia's share in global thermal coal production is 4.9%; in world coking coal production – 8.7%. [1]

— Russia’s share in global coal exports is 16.4% (versus 15.3% in 2019). Russia's share in global thermal coal exports is 18.6%; in global coking coal exports – 9.4%. [2]

— Coal production in Russia decreased by 8.1% year-on-year. and amounted to 401.4 million tons, including energy grades - 311.6 million tons (-7.9% y/y), coking grades - 89.8 million tons (-8.4%). 220.7 million tons were produced in Kuzbass (55% versus 57.3% in 2021)

— Supplies to the domestic market decreased by 8.6% - to 165.4 million tons, export supplies fell by 9% - to 212.2 million tons. If the export of thermal coals lost 5.9% on an annual basis - to 183.1 million tons, then coking, on the contrary, increased by 9.7% - to 29.1 million tons. Coal exporters significantly improved their profitability due to rising prices and lower rates for wagons.

— Coal imports to Russia turned out to be 1.3% lower than in 2021. We are talking mainly about energy grades from Kazakhstan and Ukraine.

— Coal loading by rail amounted to 353.3 million tons, of which 199.6 million tons were exported (or 56.5% of the total volume of coal loading). The share of coal loading in the total volume of production in the country is 88%. Coal cargo turnover in 2021 is 1,094.6 billion tkm (43% of the total cargo turnover). Average range – 2,844 km

— The volume of coal transshipment in seaports amounted to 188.6 million tons (+7.1% compared to 2021).

— The share of profitable coal mining organizations as of November 2020 was about 43%.

— The issue of ensuring the export of coal products remains one of the key issues on the agenda. Russian Railways is trying to improve the revenue structure of freight traffic, citing the fact that coal transportation spoils the monopoly’s financial indicators and the market for ESG bonds. The transition to long-term binding contracts for the transportation of coal is being discussed. The government, in turn, intends to accurately determine the volume of coal that will be exported by rail to the east in the coming years, and to coordinate production with this figure.

Forecast of the Ministry of Energy.

Considering the impact of the crisis due to the pandemic, it expects a decrease in coal production and exports, as well as tax payments to the budget from the coal industry in 2021 and 2021. on 10%. The domestic market is almost exhausted, especially in light of the country's large-scale gasification program. There is still hope that after 2021 Russia will be able to achieve growth in coal exports (although starting from the end of 2021, Russian coal companies are seeking to take advantage of the favorable price environment on the world market by increasing sales abroad). In the coming years, coal exports from Russia may fall as a result of a decrease in its consumption in European countries and the inability to fully compensate for the falling volumes by increasing supplies to the East - to the countries of the Asia-Pacific region - due to the insufficient capacity of the railways of the Eastern range.

The Ministry of Energy still hopes that Russian coal miners will actively increase exports of products through the Asia-Pacific region in the coming years. By 2025, supplies to the Asia-Pacific region will increase to 174 million tons - this is 42% more than was exported in 2021. The demand for coal in the Indian countries will grow at the fastest pace - more than 2 times compared to last year. ocean (India, Vietnam, Malaysia, Indonesia, Thailand, etc.). In 2025, Russian coal exports in this direction may reach 57.5 million tons.

Forecast

General characteristics and features of the underlying asset

Coking coal is a good fuel. It is distinguished by low ash content, high calorie content and a minimal amount of harmful impurities. But this is negated by such disadvantages as the high cost of production and limited reserves.

In general, the product is atypical, and the price per ton depends on a lot of factors, in particular, on the specific calorific value of coal from a new batch, logistics, stability of supply, etc.

Analysis and influencing factors

The key problem of the coal industry is environmental damage and high costs. To adhere to modern environmental standards and protect production from methane emissions, serious investments in infrastructure and equipment are needed. This reduces profitability and demand.

Coal is affected by several factors at once. On the one hand, these are renewable energy sources. For example, wind and solar generation greatly reduce the demand for coal in developed countries. In turn, developing countries are abandoning coal in favor of gas. In general, long-term futures forecasts are not the most rosy.

Thermal coal

Thermal coal prices remained low throughout much of 2021 due to the decline in industrial production caused by Covid-19. In the second quarter, regional benchmarks updated multi-year minimums: in Europe - below $40 per ton, in Asia - below $50 per ton. However, by September, European prices rose to highs in almost a year, since gas prices almost quadrupled since the summer and disruptions began. coal supplies from Colombia (against the backdrop of a strike at Cerrejón). In November-December 2020, markets expected lower demand from China, as in previous years, as the import quota for coal was exhausted. In addition, the second wave of Covid-19 and new partial lockdowns in Western Europe suggested a decrease in electricity demand relative to seasonal norms. However, unexpectedly low temperatures and increased Chinese imports of non-Australian thermal coal have led to sharp increases in prices and widening spreads between regional benchmarks.

According to some market participants and experts, at the end of 2020, the thermal coal market, having completed a phase of low market conditions, entered an upward trajectory

within the framework of the concept of cyclicality of the world economy and commodity markets. However, these statements are probably premature, since the formed structural and price imbalance in regional coal markets was more likely the result of the influence of such uncontrollable non-market factors as low temperatures in the Northern Hemisphere in the winter of 2020-2021. and politically motivated trade restrictions by China, which have led to a redistribution of trade flows in both the Pacific and Atlantic basins. If weather conditions have a limited impact during the heating season, tensions between China and Australia will bring further uncertainty to the market.

Of course, parallels emerge with 2021, when “euphoria” in the coal market also came from China, where internal restrictions on production by the country’s government against the backdrop of a cold winter forced the market to turn upward.

However, then production in the country decreased for the third year in a row, and at the end of 2021, China was able not only to maintain, but even slightly increase coal production, although the industry will still experience safety problems and financial difficulties. At the same time, China continues to reform the industry, including consolidation, consolidation of players, and development of railway infrastructure. The first National Coal Trading Center opened in October 2021 and its shareholders account for 45% of coal production, 55% of coal consumption and 75% of coal transportation in the country. At the same time, China's coal-fired power capacity grew by another 33.39 GW in 2021, with another 34 GW of coal-fired capacity approved, three times more than a year earlier. This brings the total capacity under construction to 88 GW, with 247 GW of coal projects in development.

“Green” rhetoric and the prospects for the transition of developed countries to carbon-neutral energy are increasingly weighing on the coal industry:

The US is moving towards a “green” agenda, D. Biden is returning the US to the Paris climate agreement, EU leaders have reached an agreement to reduce greenhouse gas emissions by 55% by 2030 compared to 1990 levels. Although the cold winter of 2020-2021 again raises the issue of adaptability and acceptability of “green” energy technologies to extreme and unstable climatic conditions, as well as the overall reliability of energy systems based on renewable energy sources. For example, coal generation in Western Europe in January 2021 increased by more than 10% compared to the same month last year as a result of low temperatures. In Germany, the topic is being actively discussed that the country is forced to again rely on traditional energy (coal, gas, nuclear), since wind turbines and solar panels cannot be operated safely. However, turbines actually consume electricity at these temperatures because they use electric heaters in their gearboxes to keep the oil in the casing from freezing. Solar energy is even less reliable in harsh weather conditions. With the onset of Arctic frosts, Texas (USA) faced chaos in the energy market and blackouts as a result of the shutdown of wind turbines and freezing of gas wells while the demand for electricity sharply increased. In light of the transition to green energy, an interesting forecast from the US Energy Information Administration (EIA) is that coal production in the country will grow in the next two years (by 9% in 2021 and 1% in 2022). This increase reflects higher projected demand for coal in the country's electricity sector due to rising natural gas prices.

Forecast.

The upward trend will lose momentum in the first half of 2021, after the return of moderate temperatures. The short-term supply contraction will end in early 2021 as rising prices since September have stimulated the recovery of production at some coal assets that were shut down in 2021. The pricing environment in the first half of 2021 resulted in about 25% of thermal coal exports being unprofitable , as a result, the decline in global thermal coal production is estimated by the IEA at 450 million tons.

In Australia, weak sales to China have led to a significant increase in inventories at the country's ports. This excess inventory will increase supply in the marine market and weaken the current price rally. Prices are expected to retreat to lower levels by mid-2021 as supply increases. China's coal demand and imports will decline after Chinese New Year due to rising temperatures and normalization of production.

Following the end of a long strike by workers at the Colombian Cerrejón coal mine on November 30, coal shipments resumed in December 2021, although problems arose in delivering cargo to the port in January 2021 due to a blockade of the railway line.

We expect that prices for thermal coal will remain at acceptable (from the point of view of economic feasibility of production) levels in the coming years. Supply growth will be limited due to problems with financing new projects and the current activities of coal miners, the availability of logistics infrastructure in key exporting countries, and the departure of major players. In addition, energy security priorities and the political difficulty of raising electricity tariffs to pay for cleaner but more expensive sources of electricity will constrain the growth of alternative energy sources, thereby supporting demand for thermal coal.