Even the most successful investment idea requires confirmation of its reliability and profitability. For the customer, the project may be vital, but the investor should conduct a detailed analysis of the investment project in order to protect himself from losses and predict possible benefits. Below we will look at how to analyze the effectiveness of an investment project and what factors are taken into account.

What is investment analysis

To make it easier to understand the intricacies of investing, you must first know the basic definition.

So, the comprehensive application of methods and techniques for assessing the economic feasibility of financing any projects, which investors rely on to make the right decision, is called investment analysis.

The process of such analysis always occurs dynamically and has two directions: substantive and temporal. The subject carries out analysis in order to determine basic investment decisions taking into account various factors.

These factors include:

- economic environment;

- goals and objectives set for investment;

- environmental Safety;

- the significance and impact of the project on the social infrastructure of the region;

- determining the presence of financial risks;

- plans of investors on issues of financing, organization, marketing, etc.

The above aspects are worked out during the preparation of the project itself, and then, during the analysis, they are taken into account for making decisions and introducing corrective measures.

The temporary direction considers work that begins from the moment the idea arises and lasts throughout the life of the entire project, because it ensures its continuous development so that upon its completion investors receive a profit not lower than the expected level.

Essence

Investment analysis is a completely independent area of analysis with its own methods and tools, techniques and techniques. Of course, some of its elements are borrowed from financial analysis, some from the analysis of the economic activities of enterprises and organizations, but in general, investment analysis is an independent section of investment theory.

The main task of any business is the task of stable profit making, which is possible under one indispensable condition - constant updating of the production apparatus, if we are talking about real production of products, and not about financial speculation.

Investments in the development of productive capital, which increases the mass of profits, are investments in the real sector of the economy. This process is discrete in nature, since each investment project has its own life cycle, after the end of which production is updated with the help of a new investment project. Investment projects may overlap each other, creating longer life cycles, but the discrete nature of innovation remains.

Functions

The main functions of investment analysis are:

- Creation of an authorized organization that will collect information and coordinate the process of implementing the goals of the investment project.

- To make a choice of the most suitable investment systems, the organization makes a decision based on preliminary analyzes taking into account alternative options and determines the order of the necessary activities.

- Timely identification and resolution of technology, financing, environmental or social problems that may arise during project implementation.

Why analyze a project

Analysis of the effectiveness of an investment project allows you to obtain results that can be evaluated and compared with other similar ones. These results will help determine:

- The feasibility of investing in this particular project.

- The most profitable investment option if there are several investment objects.

- The degree of significance of the project compared to others.

- Potential profitability.

- Acceptable risks.

Project analysis affects not only the financial side. This process takes into account:

- Efficiency and methods of project implementation.

- Calculation of economic benefits.

- The ratio of the necessary costs for the implementation of the project to the profit received.

- Social significance.

- Environmental Safety.

For an investor, the most important indicators are the numbers that express the effectiveness and profitability of the project. At the same time, efficiency is not only the amount of income received, but rather the profitability/risk ratio. The higher this indicator, the more attractive the project will be for the investor. If several projects have equal indicators of this ratio, investors will give preference to the project with a minimal level of risk.

The customer, as a rule, pays attention to other components - social significance and environmental safety. Ignoring possible problems in these areas can lead to force majeure or sudden closure of the project.

Similar articles:

- where and how to find an investor for a business

- how to become an investor

- types of business investments

Tasks

Analysis of investment activity is aimed at finding solutions to the following problems:

- comprehensive assessment of the necessary conditions for investment;

- justification of prices for necessary activities and selection of a source of financing;

- precise determination of external and internal objective and subjective aspects that may lead to negative changes in investment results;

- comparison of losses from possible risks acceptable for investors with expected income;

- mandatory final monitoring of the project to introduce measures that improve the results of further investment.

Stage of forecasting production volumes and profits

At this stage, the project developer, based on the possible volume of sales, determines the size and technological level of the enterprise. It is important to keep in mind the scale of available funding sources. Then prices and terms of payment for equipment are analyzed; alternative options are compared (equipment purchase or leasing); the rental (purchase) market for the required premises is analyzed; number, qualifications and payment of attracted personnel, etc.

If all previous work can be done, for example, by the marketing service of an enterprise, then at this stage an accountant-analyst should be involved in the development of the project. Having received information about all possible costs, he/she, having classified them, calculates the planned cost of production. Information about projected sales prices and production volumes allows you to calculate planned profits. A necessary tool at this stage is break-even analysis.

ALSO SEE: The value of money in illustrative examples

So, the result of the work at this stage is a forecast of sales volumes, their costs and profits. If the size of the planned profit is less than a certain threshold value set by the company, then the project may be rejected already at this stage of development. If the profit margin is considered acceptable, then further analysis is advisable.

Investment analysis methods

Now we need to consider in detail how exactly investors increase their capital.

Analysis of investment attractiveness is necessary for corporate managers to provide reliable information about the objects in which they plan to invest. Since there are a huge number of ways to conduct these events, it is better to consider in detail all the options according to their popularity and frequency of use.

If a corporation wants to purchase shares of other companies, then the following investment analysis methods will be used:

- Cost analysis using replacement takes into account the capital construction of an object from scratch at current prices, but discounts are applied (usually 10-20%) from the cost of a new one to roughly calculate the cost of a currently operating enterprise.

- Relative analysis of an acquisition transaction, where one corporation buys another company, taking into account the book value of assets and stock prices.

- Comparative analysis of companies is the process of comparing the economic performance of one company with similar enterprises.

- Discount cash flow analysis is a procedure for evaluating a company by determining the estimated income from the acquisition of securities that confirm ownership of part of the company.

Estimation of discount flows of funds (DFS)

This assessment procedure is a general methodology used in the assessment of companies. Given the appropriate quality of information, the method in question is usually the first choice for use by the corporation as a potential buyer.

Let us briefly consider some of the main steps of this algorithm. Determination of the discount rate. The return received by equity and debt holders is the value of the debt obligation, which depends on the market value of that obligation, and the value of the stock, which depends on the market value of those shares. The average value determined according to the market value is called the weighted average cost of capital (CAC). Projected free cash flows are discounted in accordance with the FSC.

Factor analysis

Since the profitability of investment projects is influenced by a number of factors (profits from sales, financial leverage, capital turnover), they are necessarily taken into account when conducting factor analysis. This is exactly how it is defined: what specific changes in some indicators lead to changes in other aspects of the project. Then you can find out which factors have the greatest impact on the income from investing in the project.

Stage of assessing types and levels of risks

At this stage, all previously obtained information regarding achievable sales and production volumes, selling prices for products, cost levels, etc. are subject to critical analysis. and conclusions drawn from them. Various options for worsening the situation are being considered. This is achieved through sensitivity analysis as part of break-even analysis.

To obtain a complete and objective picture, various possible options for changing the situation towards improvement are also analyzed. There are methods (their contents are disclosed below) that allow you to judge, based on sensitivity analysis, how risky investing in a given project is.

As a result, the developer receives an answer to the question of whether the level of risk associated with a given project is acceptable. If not, the project is rejected; if yes, it is subject to further analysis.

Expert assessment method

Analysis of investment projects cannot ignore or neglect such important points as identifying and assessing risk factors for financial losses. But performing this procedure is not easy due to the wide variety of risk factors, so the method of expert assessments helps to cope with the tasks. It takes into account numerous criteria and possible options when financial risks affect the value of an investment.

A complex of mathematical and logical calculations is used in the method of expert assessments and serves to obtain the necessary information, preparatory analysis, generalization, after which specialists will be able to make rational and effective decisions. The very essence of this method comes down to the fact that qualified specialists perform an intuitive and logical analysis of possible problems and, based on the processed results, form their own qualitative and quantitative assessment.

To cope with assigned tasks and achieve the right solution, experts use mathematical algorithms in combination with logical thinking and intuition. To make it convenient to conduct an investment analysis of an enterprise and to more easily assess risks to the value of an investment project, managers draw up a questionnaire that has a universal form.

After carefully processing the information received and solving numerous optimization problems, experts directly identify and evaluate specific types of financial risks of the project, and also draw up the necessary list of measures to minimize possible losses and adjust the structure of the investment portfolio.

It was in the process of research in the field of forecasting that most methods of expert assessments were developed. The most famous among them are the Delphi method and the method of working with scoring matrices, which are collapsed through the use of linear weight coefficients in each individual option. However, there is always one main problem that is very difficult to cope with: each of the investment analysis experts speaks on the basis of their personal experience, so all decisions made are quite subjective.

Similar shortcomings occur in the method of paired comparisons. To begin with, criteria are formulated, and then they are given a certain weight of influence on the investment project, so that in the future it is possible to streamline all the important factors of financial risks.

Specifics of valuation of shareholdings

Taking into account the specifics of the Russian market, two more methods can be proposed to significantly bring the initial price of a block of shares closer to market quotes:

- Calculated capitalization method.

- Grouping method.

The essence of the methods is as follows: If the shares of the acquired company are not quoted on the stock market, then the determination of market value can be carried out using the following initial data:

- financial statements of the analyzed company;

- financial statements of companies in the industry whose shares have a market value (quoted on the market);

- market quotes for the shares of these companies.

Subjects and objects of IA

The content and structure of investment analysis is largely determined by its subjects, subject and objects. By subjects of IA we will understand the persons who directly carry out the analysis and the circle of participants in whose interests it is performed. At the same time, we will divide the performers into persons participating in strategic IA and persons performing investment analysis related to project selection and implementation of real investments. The analysis prior to the development of an investment strategy involves:

- Director of Development;

- financial director;

- Commercial Director;

- Chief Engineer;

- managers representing investment centers in companies.

In IA performed at the project level, the named managers are assigned a more supervising function, and the direct execution of the analysis is carried out by:

- financial and economic service;

- accounting;

- marketing service;

- chief technologist service;

- capital construction department;

- other services related to the project.

The structure of services participating in the IA of projects can be universal and formed under the campaign of selection and selection of projects into the portfolio, or it can be created for each project in a unique format. IA is also performed by specialized units of external stakeholders: banks, consulting and insurance companies. Subjects making decisions based on the results of the completed IA include:

- investors;

- head of the company;

- strategic planning session group;

- bank credit committees;

- suppliers and buyers (in some cases);

- representatives of other interested organizations and authorities.

The subject of IA is determined by the cause-and-effect relationships of financial processes occurring as a result of the company’s investment activities, and the parameters of the accompanying socio-economic efficiency. The results of the conducted research make it possible to correctly assess the direction and size of investments, justify business plans, and find reserves for improving processes. The objects of IA are the results of actions at the corresponding level.

- Model of a company's strategic investment position.

- Strategic investment plan.

- Structure and composition of the enterprise's investment portfolio.

- Project programs.

- Local projects.

- Individual investment transactions, for example in the financial sector.

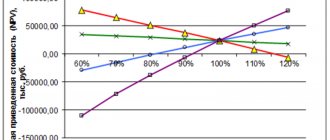

The structure of IA system options in a company depends on the industry of activity, the scale of the enterprise, and the level of development of regular management. As a rule, it is built from top to bottom from the strategy and from the current moment to the future, in which a retrospective analysis is carried out upon the implementation of project tasks. An example of the composition and relationships of the IA is shown below.

Variant of the composition and relationships of the information agency of a mid-level company

Investment performance indicators in more detail

Payback period for initial investment

(payback period) is the time period that is necessary for the receipt of funds from invested funds in an amount that allows you to reimburse initial expenses.

With sufficient investment efficiency, the project’s payback period (the starting point from which net income begins to be positive) occurs faster.

The method of analyzing the effectiveness of investments using the payback period indicator is quite simple and therefore is often used. The scheme for calculating it depends on how evenly the projected income from investment is distributed. For example, if you have distributed the expected income over the years, then the payback calculation will look like this:

The payback rate (PP) is equal to the ratio of the initial investment (IC) to the value of the annual cash inflow (CFt) over the recovery period t.

There is a certain rule according to which it is decided whether it is worth implementing a project: if the payback period that you calculated turns out to be less than the maximum acceptable, the project is accepted, otherwise it is rejected.

In the case when the receipt of financial resources varies from year to year, the payback period is determined by directly calculating the years during which the total income will become equal to the volume of the initial investment.

This performance assessment indicator does not take into account the time factor in the calculation, which is a significant drawback. However, there is an alternative method of calculation that excludes it - the discounted payback period.

Discounted payback period

Discounted Payback Period (DPP) - the time period required to recoup the discounted value of an investment using the present value of future financial earnings. This indicator can be determined by dividing the investment by the net discounted cash flow.

When you use discounting, the payback period of the project increases, in other words, the ratio always looks like DPP > PP. Ultimately, an investment project may satisfy the PP criterion, but at the same time be ineffective from the point of view of the DPP criterion.

Both of the above criteria are used when assessing the effectiveness of investments in cases where:

- The project pays off and it is accepted;

- The payback period for investments is calculated to be less than its maximum threshold (according to the organization), the project is accepted;

- There are several project options for investment; the project with the shortest payback period is accepted.

It is the DPP and PP criteria (as opposed to the NPV, IRR and PI indicators) that can help roughly evaluate a project in terms of liquidity and possible risks.

Net present value

(NPV) can be determined in different ways:

- By deducting from the current value of the investment project the current cost of costs, which are discounted by using the weighted average price of the company’s entire capital (that is, debt and equity);

- By subtracting from the present value of financial inflows the present value of outflows from shareholders, discounted at a rate that is equal to the monetary opportunity cost;

- By calculating the present value of economic profit, which is discounted at a rate equal to lost opportunity costs (that is, opportunity cost).

All of the above methods will help reveal the essence of net present value from the point of view of economic benefit. In this case, the net present value indicator can be calculated using the following formula:

where CF is discounted cash flow; IC – initial investment (in the zero period); t – year of calculation; r – discount rate equal to the weighted average cost of capital (WACC); n – discount period.

Read the article: Countertrade and its features

In order for this model to be effective and successfully applied, the following conditions must be met:

- The entire investment volume is accepted as completed;

- The entire investment amount is taken into account for evaluation at the time of analysis;

- Once the deposit is completed, the withdrawal process begins.

- To determine the discount rate (r) you can use:

- Bank loan rate;

- Cost of capital (weighted average);

- Opportunity cost of capital;

- The organization's internal rate of return.

Thus, the NPV indicator allows us to determine the return on the implementation of an investment project from an economic point of view. That is, if its goal is to make a profit, and the value of this indicator in the calculations turns out to be negative, then already at this stage of the analysis you can finally reject the project.

Internal rate of return

(IRR) characterizes the maximum cost of capital to finance an investment project.

Since the equation for determining the IRR criterion is not linear, there are several values for this indicator. The effectiveness of investments during the review process can be examined from the point of view of the expected income from the project using this feature. Therefore, IRR is a very valuable criterion in the framework of the analysis of investments and their effectiveness and can be interpreted in different ways (depending on the point of view).

There is a certain rule on which decisions regarding an investment project are based according to the IRR criterion: if its value is less than the financing rate of the investment project, then it is not worth accepting, and if it is more, the project is worthy of attention and can be considered.

Modified internal rate of return

(MIRR) is a discount rate that equates the value of future cash flows over the life of the project and is calculated by the cost of capital (financing rate) in relation to the current cost of investment in the project (which, in turn, is also calculated by the cost of capital).

where OFt is the outflow of funds in period t; IFt – inflow of funds in period t; r – financing rate; n – project duration.

In order to evaluate an investment project in terms of real profitability, it is better to use MIRR. But at the same time, the NPV indicator will be more correct in order to analyze alternative projects that will differ in scale. This is because NPV can demonstrate how much a maximally optimal project would increase the overall value of an organization.

The concept of return on investment

P

is directly related to

the profitability index PI

.

Investment return index

represents the income that accrues per unit of funds invested by the company. It can be determined by the following formula:

It is important to understand that the profitability index is a relative indicator. In other words, it only characterizes the profitability of the project per unit of cost. Thus, the higher the index value, the greater the return on each cost unit that was invested in a specific project.

That is why the PI criterion is very convenient for choosing one of several alternative projects for investment (when these projects have approximately the same NPV indicators). It is also convenient to use PI when assembling an investment portfolio to achieve the maximum total value of the NPV criterion.

To understand the profitability of an investment project, there is a simple rule: the higher the profitability, the better the project. In this case, the minimum rate of return must be shown by an index that is greater than one. If the index is one, then the net present value is zero. If the indicator is below this indicator, it does not meet the minimum rate of return.

Read the article: Product market analysis is the first step to an effective marketing strategy