What the

Gazprom Neft (sometimes also written as Gazpromneft, but according to the Charter it is Gazprom Neft) is a Russian vertically integrated oil company that specializes in oil production and refining. Technically, this is a “daughter” of Gazprom, the gas giant of Russia (Did you think that gas giants are Jupiter, Saturn, etc.? But no, it’s Gazprom!).

Gazprom owns 95.68% of Gazprom Neft shares, the rest is in free circulation on the stock exchange.

Here are the company's financials:

The company is among the TOP 3 largest domestic oil companies along with Lukoil and Rosneft. Gazprom Neft is the first company to begin oil development on the Arctic shelf. Its assets include proven 2.84 billion tons of oil equivalent, and the company processes about 35-40 million tons of oil annually. In short, a very cool office.

The official website where you can find out more is https://ir.gazprom-neft.ru.

By the way, Gazprom Neft (written together like this) is a network of gas stations through which Gazprom Neft (this is the name of the office, written separately) supplies its fuel (gasoline, diesel, liquefied gas) for sale.

Mining

NLMK, Severstal and MMK

The “Big Three” metallurgists – NLMK, Severstal and MMK – in my opinion, will increase their dividends in 2021. Prices for rolled metal products are steadily rising, companies are at the peak of their development, capital costs are under control. We will definitely see double-digit dividend yields from all three, and it is difficult to say who will have a higher dividend yield. And this is even taking into account the fact that quotes are at their maximums: fundamentally, metallurgists are still undervalued.

You also need to remember that metallurgists pay dividends quarterly. Therefore, buying their dividend shares in 2021 could be a very good purchase. Most likely, it is metallurgists who will pay the largest dividends in 2021.

However, it must be taken into account that NLMK and Severstal's net debt is growing rapidly. If net debt exceeds EBITDA by a multiple, companies can reduce dividends by 2 times. MMK has no net debt, but a more expensive raw material base and low margins. Plus NLMK and Severstal can make more profit due to currency revaluation, since they export more of their products than MMK.

If you are interested, you can read a detailed review of the “Big Three” metallurgists on my paid channel.

Norilsk Nickel

The main share in Norilsk Nickel's production is no longer nickel, but palladium, which is at historical highs. Therefore, Norilsk Nickel, despite the crisis, makes decent profits and may well increase dividends in 2021.

However, pressure on dividends comes from the need to set aside a reserve to eliminate the consequences of a number of accidents (including the sensational one at CHPP-3) and to pay off fines. While specific figures on the fine have not been announced (the investigation has not yet been completed, but the amount mentioned is $147.7 billion), I think that Norilsk Nickel has already reserved the maximum amount for this case. They will force you to pay the maximum - ok, they will not force you - they will distribute the remainder among the shareholders.

Another thing stops it: in 2021, the dividend agreement between Norilsk Nickel’s two largest shareholders, Vladimir Potanin and Oleg Deripaska, expires. The parties cannot agree on the new development policy: Potanin wants to cut dividends and increase CAPEX (to modernize the company), but Deripaska needs money. It is still unclear what the two sworn friends will agree on.

It is difficult to name specific figures for Norilsk Nickel's dividends in 2021, but taking into account net profit, current divisional policy and the reserves allocated for fines, a dividend of 1,100-1,400 rubles can be predicted (there are two amounts: Potanin proposed limiting the final dividends for 2021 to $1 billion, and this is 442 rubles per share, the second amount is dividends for the 1st half of 2021, if the same dynamics of palladium prices continue). At the current share price of 24,115 rubles, the yield is quite small: 4.5-5.8% per annum.

Alrosa

This diamond among Russian companies is doing well: the diamond crisis in India is coming to an end, prices for rough diamonds are rising again, the government is ready to provide support. Alrosa successfully overcame the crisis year.

It is clear that you should not expect very large dividends based on the results of 2021. But in 2021, Alrosa could easily pay 5.4 rubles per share, which at the current price of 91.85 rubles gives a yield of 5.87%.

A full analysis of Alrosa is available on boosty.to.

Mechel

You shouldn't expect dividends from Mechel. It was a difficult year – I wish I could get rid of my debts.

Dividend policy

Since Gazprom Neft is a subsidiary of Gazprom and Gazprom is its main shareholder, it is Gazprom that is interested in high dividend payments. Minority shareholders don't decide anything here at all. This must be taken into account when purchasing Gazprom Neft shares.

The dividend policy involves paying one of two things - 15% of net profit under IFRS or 25% of profit under RAS, whichever is greater. But in the last three years, 25% has been consistently paid according to IFRS - i.e. greater than the declared value.

And here’s another interesting article: Rosseti dividends in 2021: size, payment period and purchase procedure

You can see the total payments by year in the table:

| Year | Dividend (in rubles) | Changes from previous year |

| 2018 | 27.05 | +30.8% |

| 2017 | 20.68 | +3660% |

| 2016 | 0.55 | -92.92% |

| 2015 | 7.77 | -21.59% |

| 2014 | 9.91 | -25.99% |

| 2013 | 13.39 | +83.42% |

| 2012 | 7.3 | +64.41% |

| 2011 | 4.44 | +24.37% |

| 2010 | 3.57 | -33.89% |

| 2009 | 5.4 | 0% |

| 2008 | 5.4 | -33.19% |

| 2007 | 8.08 | +2.31% |

| 2006 | 7.9 | -43.21% |

| 2005 | 13.91 | n/a |

Yes, dividends are paid twice. Interim, based on the results of 9 months - in December, final (balance) - in June-July.

And some diagrams and valuable information from the site dohod.ru:

In the long term, the company will try to increase payments to 50% according to IFRS, like any state-owned company. In light of the increase in production, income and the fall of the ruble, this could be a good driver for the growth of dividends and, accordingly, the share price. If only oil didn't fall.

Stock return

If we take the period of the last 10 years, there have been no sharp rises or falls in the price of Gazprom Neft shares. In 2009, after emerging from the crisis, it was 61 rubles and then began a gradual increase, being in the corridor between 101 rubles and 299 rubles in 2021. The last 2 years have seen a significant increase in price to 371 rubles.

If we roughly estimate the average annual growth estimate, it will be 31 rubles: (371-61)/10 years.

During the year, the share price fluctuates within 50 percent.

Gazprom Neft dividends for 2018

On April 19, the Board of Directors of Gazprom Neft recommended the annual meeting of shareholders to pay 30 rubles per share. Taking into account the fact that for 9 months of 2021 the company has already paid out 22.05 rubles per share (the register was closed on December 28, 2018), this year investors will receive 7.95 rubles each.

The total amount of payments will be 142.2 billion rubles, which corresponds to the distribution of 37.8% of net profit under IFRS.

With a share price of 369.05 rubles, this gives a yield of 2.15%. Taking into account dividends already paid – 8.12%.

Thus, if you buy shares now, you will receive only a small fraction of dividends for 2021 - the company made the main payments in December. But there is good news -

According to analysts' forecasts, by the end of 2021 the company will pay approximately 20 rubles per share. Payment will be made, as usual, in December.

All company dividends for the last 10 years

Officially, the Gazpromneft Charter does not provide for the division of shares into ordinary and preferred. All issued securities – registered and uncertificated – have the same nominal value. Contrary to popular misconceptions, preferred shares have never been issued.

| For what year | Period | Last day of purchase | Registry closing date | Size per share | Dividend yield | Closing share price | Payment date |

| 2019 | June 23, 2021 | June 25, 2021 | 12M 2020 | 10 ₽ | 2,73% | 9 Jul 2021 | |

| 2019 | 25 Dec 2020 | 29 Dec 2020 | 9M 2020 | 5 ₽ | 1,57% | 12 Jan 2021 | |

| 2018 | June 23, 2020 | June 26, 2020 | 12M 2019 | 19,82 ₽ | 5,6% | 10 Jul 2020 | |

| 2018 | 16 Oct 2019 | 18 Oct 2019 | 6M 2019 | 18,14 ₽ | 4,24% | 1 Nov 2019 | |

| 2017 | June 27, 2019 | 1 Jul 2019 | 12M 2018 | 7,95 ₽ | 1,97% | 15 Jul 2019 | |

| 2017 | 26 Dec 2018 | 28 Dec 2018 | 9M 2018 | 22,05 ₽ | 6,13% | 11 Jan 2019 | |

| 2016 | June 22, 2018 | June 26, 2018 | 12M 2017 | 5,00 ₽ | 1,6% | 10 Jul 2018 | |

| 2015 | 27 Dec 2017 | 29 Dec 2017 | 9M 2017 | 10,00 ₽ | 4% | 12 Jan 2018 | |

| 2014 | June 22, 2017 | June 26, 2017 | 12M 2016 | 10,68 ₽ | 5,55% | 10 Jul 2017 | |

| 2014 | June 23, 2016 | June 27, 2016 | 12M 2015 | 0,55 ₽ | 0,34% | 11 Jul 2016 | |

| 2013 | 14 Oct 2015 | 16 Oct 2015 | 6M 2015 | 5,92 ₽ | 3,9% | 30 Oct 2015 | |

| 2013 | June 18, 2015 | June 22, 2015 | 12M 2014 | 1,85 ₽ | 1,32% | 6 Jul 2015 | |

| 2012 | 15 Oct 2014 | 17 Oct 2014 | 6M 2014 | 4,62 ₽ | 3,1% | 31 Oct 2014 | |

| 2012 | June 19, 2014 | June 23, 2014 | 12M 2013 | 5,29 ₽ | 3,45% | July 7, 2014 | |

| 2011 | 25 Aug 2013 | 25 Aug 2013 | 6M 2013 | 4,09 ₽ | 3,09% | 6 Sep 2013 | |

| 2010 | April 23, 2013 | April 23, 2013 | 12M 2012 | 9,30 ₽ | 6,93% | May 7, 2013 | |

| 2009 | April 24, 2012 | April 24, 2012 | 12M 2011 | 7,30 ₽ | 4,71% | May 8, 2012 | |

| 2008 | April 25, 2011 | April 25, 2011 | 12M 2010 | 4,44 ₽ | 3,03% | May 9, 2011 | |

| 2007 | May 14, 2010 | May 14, 2010 | 12M 2009 | 3,57 ₽ | 2,6% | May 28, 2010 | |

| 2006 | May 15, 2009 | May 15, 2009 | 12M 2008 | 5,40 ₽ | 5,46% | May 29, 2009 | |

| 2005 | May 15, 2008 | May 15, 2008 | 12M 2007 | 5,40 ₽ | 3,05% | May 29, 2008 |

Where and how to buy

Gazprom Neft shares are traded on the Moscow Exchange under the ticker SIBN. At the time of writing, the cost of one share was 368 rubles.

Shares are sold in lots, with one Gazprom Neft lot containing 10 shares. Thus, the minimum purchase amount is 3,680 rubles. By purchasing such a lot now, you will receive 79.5 rubles in dividends in July, and approximately another 200 rubles in December (excluding taxes).

The purchase is carried out through any broker operating on the Moscow Exchange. For example, Tinkoff investments. Follow the link, open an online brokerage account and start buying. Or choose from brokers with minimal commissions.

How to buy shares and receive dividends

The scheme for receiving dividends is extremely simple: you need to open a brokerage account, go to the trading program, indicate the company name (Gazpromneft) or ticker. The minimum purchase is one lot, which is equal to 10 shares.

Best brokers

A broker is an intermediary company that provides access to the exchange. This is an experienced securities market player with an appropriate license from the regulator. I bring to your attention a selection of the best brokers with the help of which you will increase your own capital.

Reliable Russian brokers

| Name | Rating | pros | Minuses |

| Finam | 8/10 | The most reliable | Commissions |

| Opening | 7/10 | Low commissions | Imposing services |

| BKS | 7/10 | The most technologically advanced | Imposing services |

| Kit-Finance | 6.5/10 | Low commissions | Outdated software and user interface |

Warning about Forex and BO

Forex, although it is called foreign exchange markets, has nothing to do with genuine stock trading. It is impossible to purchase shares there, even of Gazprom Neft, or of any other company, and there is no talk of dividends at all. Options, without the prefix “binary,” are an exchange instrument that is little used by ordinary traders. And BO is, in fact, a type of online casino. You can lose all your money there in a single moment, but you are unlikely to make any money. Be careful and don’t fall for scammers’ tricks.

Are there any prospects?

I already wrote partly about this above. An increase in dividends can be a good driver for growth in stock prices. But there are also positive factors:

- oil production is increasing, which means increasing profits;

- the capital investment season has ended, and Gazprom Neft can allocate more funds to dividends;

- Gazprom's quotes have increased, and the “pulling up” of its subsidiaries is quite expected.

But there are risks that you should not forget about:

- Gazprom Neft is a subsidiary, and Gazprom can receive money from it in other ways, bypassing shareholders (for example, by receiving an interest-free loan);

- falling oil prices;

- strengthening of the ruble.

So think for yourself whether you need it. If the portfolio is large, then, in my opinion, it is worth adding Gazprom Neft shares for diversification. If it is small, then it is better to choose other oil companies, such as Bashneft, Rosneft or Lukoil, where there is not such a strong dependence on other companies and the economic situation. Good luck, and may the money be with you!

Rate this article

[Total votes: Average rating: ]

Disclaimer

I made a forecast for dividends of leading Russian public companies based on available publicly available information, in particular, from published financial statements for 2021. But, since 2021 has not yet ended, there are no final financial results for the year. Therefore, actual dividends may differ (and will differ) from those predicted.

Share prices are given at the time of writing the review and therefore may differ from current ones.

Everything written below does not constitute individual investment advice.

Constructive criticism and polite expression of your opinion in the comments are welcome.

Petrochemical and refining

Kazanorgsintez, NKNKH and Saratov Refinery showed conflicting results for 2021. On the one hand, their expenses have decreased due to low oil prices, on the other hand, their income has not grown much due to the crisis and decreased demand for their products. Therefore, you should not expect explosive growth in dividends, but payments will remain above average.

Based on current profits, you can expect the following dividends:

- Kazanorgsintez - 4 rubles for joint-stock companies (about 4% of the yield), 0.25 rubles for up;

- Saratov Oil Refinery up – 1400-1500 rubles (9.1%-9.8%);

- NKNKH - 8 rubles for each type of share (about 10%).

Overall, quite interesting. Both SNPZ and NKNK remain attractive dividend stories, but this is the third echelon, and anything can happen here.

Banks

Sberbank (sorry: Sber) abandoned its ambitious plan to earn a trillion rubles in 2021: in 3 quarters it managed to earn “only” 557 billion rubles. There are no financial results for the 4th quarter yet, but most likely the final profit will be at the level of last year (in 2021, Sber earned 845 billion rubles). Therefore, dividends will most likely remain at the same level - not lower than 16-18 rubles. The dividend yield of shares due to the strong growth of Sber's quotes in December 2021 turned out to be small: a maximum of 5.7% for ordinary shares and 6.3% for preferred shares.

However, Sber has put quite a lot of funds into reserves. Therefore, he may well “print out” this stash and increase the dividends up to 20-22 rubles.

VTB... Oh, it's VTB! In 2021, it reduced dividends to 10% of net profit under IFRS (although it had to pay 50% as a state company). So in 2021 I expect anything from the most unexpected bank in the Russian Federation. But let's assume that there will be no childish surprises, and the bank will pay, as expected, 50% of net profit. Given the record decline in profits in 2021, dividends will only increase slightly compared to this year's 10 percent: to approximately 0.00109-0.00110 rubles, depending on the financial results of the 4th quarter of 2021 (versus 0.00077 paid previously ). And if the bank again makes a trick with its ears, then... But let’s not talk about the bad...

Tinkoff Bank (a subsidiary of TCS Group) may pay record dividends in 2021. 2021 was a very successful year for Tinkoff, despite the crisis: net profit for 9 months of 2021 amounted to 31.8 billion rubles (and for the whole of 2021 - 36.1), the profit forecast for the whole of 2020 was 43 billion rubles. Tinkoff pays dividends quarterly, so it is difficult to accurately predict payments for 2021. But if the same profit dynamics are maintained, we can expect total dividends at the level of 70-80 rubles. By the way, in 2021 Tinkoff paid only 15% of net profit, and in 2021 it intends to pay 30%, so there will be an increase in dividends in any case.

Telecoms

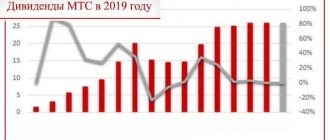

Everything here is stable and predictable. MTS and Rostelecom not only did not suffer during the pandemic, but also grew their customer base. In addition, their profits did not fall - and MTS’s FCF actually doubled.

I also expect stability in dividends: MTS will pay at least 28 rubles per share in accordance with its dividend policy (8.79% dividend yield), and Rostelecom - at least 5 rubles for each type of share (5.76% for ap and 5.18 % for ao).

I am not considering MGTS - dividends in 2021 against the backdrop of record profits. Therefore, in 2021, you may again not pay anything. Perhaps the company is preparing to be taken over by its “mother” company, MTS (or to be sold to someone else).

I’m also not considering Central Telegraph. The real estate for sale seems to have run out, and the company is not making a profit.

Dividend price per Gazprom share in 2021

After 2021 the situation will improve noticeably. First of all, against the backdrop of lower costs, the start of pipeline gas exports to China. For a long time, Gazprom with a dividend yield above 5% looks like a good story. Current multiples remain at low values: EV/EBITDA LTM – Z.6, P/E – Z.9. The key player in the Asian region is already China. By 2021, demand will increase by 14% y/y.

It is expected that by 2035, gas imports into KHP will double. Gazprom plans to take a 10-12% share of the Chinese market by 2025, and >13% by 2035. After Power of Siberia reaches its designed capacity, Gazprom will receive 20% additional supplies to the export volume. The start of deliveries is scheduled for the end of 2021.

Registry closing day – the day on which the organization will look at the register. Gazprom has a register closing date set for April 20 - this means that on April 20, at the close of trading on the exchange, Gazprom will register this list to shareholders They consume all the income that has accumulated over the year.

They will also have the right to vote at the shareholders' meeting. PJSC Gazprom is a global energy company in Russia, actively operating in the domestic and foreign markets.

Engaged in exploration, production, processing and transportation of hydrocarbons, mainly natural gas. It is a reliable supplier of raw materials, satisfies about half of the gas demand in the domestic market, and supplies more than 30 countries of the world. The company has the world's largest proven reserves of natural gas – 17%. Currently implementing a major investment program.

Gold miners

The price of gold is slightly adjusted, but in 2021, the growth of the precious metal, in my opinion, will continue along with rising inflation. There is a limited amount of gold in the world, so its value reacts quite well to inflation. In addition, if there is an economic recovery in 2021, then the demand for jewelry will increase. Consequently, gold will rise again.

It is difficult to predict the size of dividends from gold miners, but given that the companies received record profits in 2021 and will distribute them among shareholders, we can assume that they will also be record ones (the dividend yield is indicated in parentheses):

- Lenzoloto up – 110-120 rubles (2.8-3%) versus 13.87 in 2020;

- Polymetal – 130-140 rubles (8-8.3%) versus 70 in 2020;

- Polyus - 500-600 rubles (3.5-4.2%) versus 484 in 2021.

Seligdar, as always, will most likely pay 2.25 rubles per preference for each half-year.

But gold mining is still an increase in market value, not dividends. So it’s worth taking shares of these companies if you believe in the further growth of gold and are willing to take on additional company risks (as, for example, in the case of Petropavlovsk: a corporate conflict led to courts and the freezing of dividends).