What are the technical and economic indicators of a project and which of them are most important for planning and organizing a business? Using technical and economic indicators, one can draw conclusions about how efficiently the enterprise uses resources, whether the quality of the products is high enough, and whether there are optimization ways to increase productivity. This information can be used to analyze existing production, or can become the basis for preparing a feasibility study for a project.

Key indicators for assessing project effectiveness

It is advisable to use the following as key project performance indicators:

- net income;

- net present value;

- internal rate of return;

- the need for additional financing (other names - PF, project cost, risk capital);

- cost and investment return indices;

- payback period;

- a group of indicators characterizing the financial condition of the enterprise participating in the project.

Conditions for financial feasibility and performance indicators are calculated on the basis of cash flow Фm, the specific components of which depend on the type of performance being assessed.

At different stages of calculations, in accordance with their goals and the specifics of the PF, financial indicators and conditions for the financial feasibility of the individual entrepreneur are assessed in current or forecast prices. Other indicators are determined in current or deflated prices.

Next, we will consider each of the indicators of the economic efficiency of the project.

What is the feasibility study of the project?

A project feasibility study (feasibility study) is a document that describes the feasibility of creating a new product, a new service, a new production, etc. It is developed not for an existing business, but for one being created, launched, or entering the market. Its main purpose is to show investors how profitable or unprofitable a project that has not yet been implemented is. A feasibility study may be required by the customer, the new head of the company or one of the founders of the project.

There are no strict requirements for what the justification will contain. In each individual case, this is a unique set of parameters and characteristics that objectively describe the project. A feasibility study should not be confused with a startup pitch or a business plan. It contains the most objective data and does not include a marketing component, subjective assessments and hypothetical assumptions.

A feasibility study is a system of maximally objective data that are directly dependent on each other.

The calculation of technical and economic indicators involves the use of the same indicators - the cost of funds, the number of products produced, etc. The basis for the justification will be the indicators presented in the table from the previous section. Which of them should be included and which should be excluded is decided directly by the developers.

Net present value

The most important indicator for calculating the effectiveness of a project is net present value (other names: NPV, integral effect, Net Present Value, NPV). This is the accumulated discounted effect over the billing period. NPV is calculated using the formula:

| NPV = SUM Фm ALPHAm(E) m |

NPV and NPV characterize the excess of total cash receipts over total costs for a given project, respectively, without taking into account and taking into account the inequality of effects (as well as costs, results) relating to different points in time.

The difference between the BH and NPV is sometimes called the project discount.

To recognize an investment project as effective from the investor’s point of view, it is necessary that the NPV of the project be positive. When comparing alternative projects, preference should be given to the project with a large NPV value (if the condition of its positivity is met).

Sample feasibility study

To better understand what a feasibility study is and what stages of creation it goes through, let's look at an example. It should be taken into account that in each individual case the stages and their content may differ. Creating a feasibility study can be compared to preparing a report or business plan: the general sequence of actions is approximately the same, but the specifics of the project fill them with different content.

Sample feasibility study for an enterprise producing crumb rubber:

The idea of the project is the processing and disposal of rubber waste (mainly rubber tires) for the purpose of earning money.

Resume : small business with up to 15 employees. There are 1-2 competitors on the market, but the demand for rubber recycling is generally high, and the current situation is conducive to making money in this industry. The information in this section is based on market analysis in the region, so it is necessary to first collect and process a large amount of information.

List of necessary premises and equipment for business:

- shop;

- warehouse for storing raw materials;

- mixer for crumb rubber;

- packaging line.

In this section, developers list everything they will need for the job, and also find the total cost of equipment and real estate. The result of the section should be a specific amount with which you can start the project from scratch.

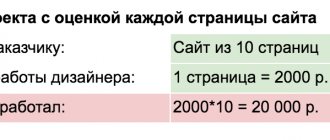

When the list of necessary equipment has been prepared, it is necessary to calculate how many products it will produce. In this project we are talking about crumb rubber, the quantity of which will directly depend on 2 factors: uninterrupted supply of raw materials (rubber waste) and the power of the mixer. You can find out exactly how much crumb the mixer can process per shift from the technical documentation or after a full day of work. The second option is preferable because it provides for the dependence of the indicator on the speed of work of employees.

When the maximum and actual production capacity are known, they calculate how many products the company will produce per shift, week, month. The cost, optimal trade margin and market price of the crumbs are calculated. Based on these amounts, the company's revenue and profit for the first month and all subsequent periods are calculated.

Project developers can go further and calculate several options for the development of the project: in workshops of different sizes, for different models of equipment, for different team sizes.

As a result, there should be a complete justification for why the project is viable or unviable, or is worth or worth investing money and effort into its implementation.

Internal rate of return

Its other names are IRR, internal discount rate, internal rate of return, Internal Rate of Return, IRR.

Typically, in investment projects that start with (investment) costs and have a positive BH, the internal rate of return is called a positive number of Ev if:

- at the discount rate E = Ev, the net present value of the project turns to 0,

- this is the only number.

In a more general case, the internal rate of return is such a positive number Ev that at the discount rate E = Ev the net present value of the project turns to 0. For all large values of E it is negative, for all smaller values of E it is positive. If at least one of these conditions is not met, the GNI is considered not to exist.

To assess the effectiveness of an investment project, the value of IRR must be compared with the discount rate E:

- investment projects with IRR > E have a positive NPV and are therefore effective;

- projects with IRR < E have a negative NPV and are therefore ineffective.

VND can also be used:

- for the economic assessment of design solutions, if acceptable values of IRR (depending on the field of application) are known for projects of this type;

- to assess the degree of stability of the IP based on the difference in GNI – E;

- for project participants to establish the discount rate E based on data on the internal rate of return of alternative areas for investing their own funds.

To assess the effectiveness of the project for the first k steps of the billing period, it is recommended to use the following indicators:

| Current net income (accumulated balance) | k BH(k) = SUM Фm m=0 |

| Current net present value (accumulated discounted balance) | k NPV(k) = SUM Фm ALPHAm (E) m=0 |

| Current internal rate of return (current IRR) | This is the number of IRR(k) that at the discount rate E = IRR(k) the NPV(k) value becomes 0, for all large values of E it is negative, for all smaller values of E it is positive. For individual projects and values of k, the current IRR may not exist. |

Indicators of financial condition and additional analytics

The project is related to the current and future financial condition of the company. Investments are not always able to bring benefits to the project-organizing enterprise. If you are not careful, your financial condition may be subject to a number of risks of deterioration of your credit history and even bankruptcy. Therefore, the analysis uses special criteria for the risk-free implementation of investment in individual entrepreneurs. They define five subgroups of indicators, for the calculation of which information from the BBL and BDR of the project is used.

The first subgroup is responsible for assessing the solvency of the company. By this we mean the ability to meet the existing long-term obligations of an enterprise without the need to liquidate long-term assets. These indicators allow us to assess the risk of bankruptcy. These include the following criteria.

- DAR (Dept Ratio to Assets Ratio). The ratio of a company's total liabilities to its total assets, showing how much the company's assets are supported by borrowed capital. The formula below allows you to calculate the indicator.

- DER (Total dept to Equity Ratio). The ratio of borrowed funds to equity of a company shows how many total liabilities of the company fall on one ruble of its own funds. In Russia, this indicator is called the financial independence ratio or financial leverage (see formula below).

- TIE (Times Interest Earned Ratio). Interest coverage index. This is an indicator of the company's debt service. In domestic financial management, the indicator is often called the interest coverage ratio (see formula below).

Formulas DAR, DER, TIE in a comprehensive assessment of the effectiveness of individual entrepreneurs

The second subgroup of indicators is responsible for assessing the company's liquidity. This subgroup includes the criteria of current and absolute liquidity. By asset liquidity we will understand the rate at which an asset is converted into cash without a significant loss of value. The first indicator makes it possible to assess the company’s ability to meet requirements for short-term obligations using current assets, and the second - the most liquid of them. The qualitative differences between these indicators are not so great, however, they exist. To implement the calculations, the formulas presented below are used.

Formulas for current and absolute liquidity

The remaining three subgroups of indicators are even further from investment analysis than profitability, solvency and liquidity. However, for a holistic view of the reliability of project implementation for the overall health of the company, they also matter. We are talking about the stability of the company, the state of relations with customers (accounts receivable), analysis of break-even and financial leverage. The stability of the company is determined by the dynamics of such criteria as its own working capital and net working capital. An equally important role is played by the parameters of sales volume at the break-even point and the level of the company’s profitability reserve in connection with the planned IP. Finally, the effect of financial leverage helps to understand how the changed capital structure caused by the attraction of additional sources to the project can affect the financial result as a whole.

Payback period

The payback period (“simple” payback period) is the duration of the period from the initial moment to the moment of payback.

The starting point is indicated in the design task (usually this is the beginning of the zero step or the beginning of operational activities). The payback moment is the earliest point in time in the calculation period, after which the current net income of BH(k) becomes and subsequently remains non-negative.

When assessing efficiency, the payback period, as a rule, acts only as a limitation.

The payback period taking into account discounting is the duration of the period from the initial moment to the “payback moment taking into account discounting”.

REFERENCE

The payback moment, taking into account discounting, is the earliest point in time in the calculation period, after which the current net present value NPV (k) becomes and subsequently remains non-negative.

Structure and content of justification

Officially, there are no strict requirements for the structure and style of presentation of the business case. This means that the form and procedure for presenting information depends on the specifics of the company’s activities, as well as the intended readership. However, all these documents are quite similar. Their approximate content looks like this:

- The purpose of justification. At this economic point, it is necessary to explain why the company needs the project, what functions it will perform and what benefits it will bring. This point should be disclosed in as much detail as possible, because it most often depends on it whether the work will be accepted and funded.

- Method of implementation. Having explained the economic goal, you need to name possible ways to achieve it and describe which method was chosen for this. It is also necessary to compare the selected methods with alternative ones and justify why they are the most effective. In addition, it is worth providing a description of the selected technical solutions.

- Economic data. It is necessary to describe in detail all income and expenses from the project, indicate the amount of initial investments and the method of receiving them. Support the information with calculations of all parameters.

- Execution plan. It is necessary to justify the minimum and maximum deadlines for completing the project, as well as describe the amount of labor and financial costs for its implementation. For convenience, you can divide the entire economic period into stages (for example, the purchase of equipment, its delivery, installation and configuration, personnel training and the start of production of new products) and analyze each of them. It is also necessary to describe all factors that could create a delay in the implementation of the project or speed it up.

- Responsibilities of employees. Indicate how many people are needed to implement the idea and what tasks each of them will have. In addition, justify the need for each employee to complete the assigned task.

- Performance forecasts and assessment of attractiveness for investors. Calculated based on economic data.

- Conclusions. Recommendation for implementing the project or sending it for further refinement to find more effective solutions.

A correctly drawn up economic proof will be useful even if the justification is not approved - the collected information will help to find shortcomings and correct them before the company suffers losses. The specifics of its content depend on the specifics - for example, in construction you will need an estimate and calculation of materials, and in the production of food products - data on their shelf life and storage equipment.

Need for additional funding

The need for additional financing (PF) is the maximum absolute value of the negative accumulated balance from investment and operating activities.

The PF value shows the minimum amount of external financing for a project required to ensure its financial feasibility. Therefore, PF is also called risk capital. It should be borne in mind that the actual amount of required financing does not have to coincide with the PF and, as a rule, exceeds it due to the need to service the debt (see example in Appendix 10).

Also see “How to choose a financial model for the feasibility of an investment project.”

The need for additional financing taking into account the discount (DFT) is the maximum value of the absolute value of the negative accumulated discounted balance from investment and operating activities.

The DPF value shows the minimum discounted amount of external financing for the project necessary to ensure its financial feasibility.

Algorithm for creating feasibility studies for various objects

As a rule, the creation of a feasibility study for projects goes through the same stages, regardless of the area in which their implementation is expected. The format of the justification largely depends on its addressee: a presentation with a detailed text report is suitable for investors, a short summary will be more interesting to the lender. The addressee should be the key criterion when creating a justification.

The development of a feasibility study goes through the following stages:

- Idea and brief description of the project. Developers write down exactly what they want to create and how it will work.

- Compiling a list of necessary equipment, facilities, raw materials, suppliers, personnel. The developers describe how and with what help their project will work.

- Calculation of production capacity. At this stage, it is necessary to calculate how much, in what volume and at what speed will be produced, and also calculate whether this is enough to compete in the market.

- Economic justification. The authors of the project calculate the cost of production, monthly and annual revenue, and profit.

- Assessing prospects. Based on all the calculations, the developers draw a conclusion about the prospects of their project. Justification helps to see the real picture of the project’s competitiveness and attract lenders and investors.

Development of a feasibility study will take a lot of time and require the involvement of several specialists

Revenue and sales forecasts

In order for the company to gain a foothold in the market, in the first months of operation we plan to set a markup on manufactured products in the range of 40-60%. The wholesale price per kilogram of polyethylene granules varies in the range of 25.1-28.7 rubles. To implement the project, a one-time injection of financial resources (purchase of equipment) is required.

The payback period for the project is 2.1 years, subject to slight changes in prices for electricity, rent, and utilities.

Mandatory justification data

Regardless of the structure and order of presentation of the economic argumentation, it is imperative to include all the basic data on the financial relationships of the project. Examples of required information:

- a general description of the rationale, its objectives at the enterprise, impact on the development of the economy (both an individual company, a region or a country);

- analysis of market conditions and the project’s adaptability to them;

- economic costs;

- characteristics of the changes being introduced, from the point of view of profitability;

- payback period taking into account all interest and inflation (it is important that investing in a project is more profitable than simply keeping money in a deposit account);

- assessing the attractiveness of the project for investors.

These rationale points remain the same in the economic rationale for a company in any industry. They can be supplemented with new sections and subsections, depending on the characteristics of the enterprise and the interests of the intended circle of readers.

Calculations

Economic feasibility is an important point, without which you cannot start organizing your own production. When calculating costs, we took into account the cost of manufactured products, the markup on granulated polyethylene, and the payment of tax deductions.

To implement the project under consideration, it is necessary to rent a non-residential premises with an area of about five hundred square meters with a concrete floor and a ceiling height of at least seven meters. The rented building is equipped with water supply, heating, industrial sewerage, and electrical supply (up to 300 kW).

There is also a space allocated in the room for unloading waste, sorting, and storing finished granules. Economic feasibility is an assessment of the profitability of an enterprise. Considering that serious preparatory work is required to install a line for processing polyethylene waste, it is advisable to conclude a lease agreement for a period of five years. The project uses equipment (Japan), the average service life of which is five years. Commissioning and installation work is carried out by specialists from a Japanese company; certain costs are included in the budget.

| Expenditures | Amount, thousand rubles |

| 1. Expenses for paying specialists involved in production | 230 000 |

| 2. Travel plan expenses | 45 000 |

| 3. Materials required for production | 30 000 |

| 4. Organizational costs | 30 000 |

| 5. Unforeseen company expenses | 15 000 |

| Grand Total | 350 000 |

Example of mathematical calculations within a company

The economic feasibility of the activity of the created enterprise is an important aspect. We offer a calculation option for a project related to the processing of polyethylene waste.

Justification of economic feasibility was carried out on the basis of formulas.

The main task is to create a production facility for recycling polymer waste (polyethylene) on the territory of the Russian Federation.

The volume of required financial investments is 100,000 euros. The economic feasibility of the enterprise was calculated at the exchange rate of 68.4 rubles.

The formation of an integrated enterprise for processing polyethylene waste based on innovative technologies will solve the problem of their systematic removal to a landfill. New jobs will appear in the country. Secondary raw materials obtained through recycling will turn from an unprofitable form into an effective income option.

After the start of operation of the analyzed complex, additional financial profits will go to budgets of different levels, so the social and economic feasibility of the enterprise is indisputable.

The installed complex for processing polymer waste will become competitive in the global economic market.

The economic feasibility of the project is that its payback period is limited to 25 months. This project can be implemented in any region of the Russian Federation, which confirms its uniqueness and timeliness.

Specifics

The economic feasibility of production is confirmed by an analysis of the market situation. Monitoring was carried out on the territory of Russia, and the situation in this sector of the economy in other countries was also considered.

Recently, there has been an increase in prices for raw materials for the manufacture of polyethylene products. This situation significantly reduces the financial and economic indicators of small-scale industries that focus on creating a specific range of goods. That is why manufacturers of polyethylene products are looking for ways to reduce the cost of the goods they produce.

Sales market

Economic feasibility is an indicator without which the organization of new production is impossible. The filling level of the secondary raw materials market in the Russian Federation is, according to various estimates, 5 - 10%. This is explained by the lack of industries processing polyethylene waste.

The price for imported secondary raw materials is about 33 rubles/kg, which is significantly lower than the prices for original raw materials. When analyzing enterprises involved in processing polyethylene waste in the Northwestern Federal District, several companies were identified. Most of them are located in St. Petersburg, focus on working under direct contracts, and produce secondary raw materials in granular form.

Production costs

The fixed costs for this project will be payment for cellular communication services, fax use, and the Internet. This article also includes payment of utilities, rental of modern equipment, premises, and creation of advertising materials. Fixed costs include obtaining licenses, patents, and monthly salaries of employees. We calculate depreciation using the linear method, taking the cost of equipment 40.965 euros (1 euro - 68.35 rubles) with an operating life of 5 years.

Depreciation charges are determined by the formula: K = (1/ n) * 100%, where K is the standard depreciation rate in%; n is the useful life of the fixed asset, expressed in years.

K = (1/5) * 100% = 20%, depreciation charges: A = (2800000 * 0.2) / 12 = 46,660 rubles.

Variable costs of the created production are associated with material costs for raw materials, materials, payment for electrical energy, fuel, components, as well as other types.

Cost of production: S = (VC+FC)/N = (810600+ 971380) / 100000 = 17.92 rubles.

Financial and economic risk is possible with a sharp drop in consumer demand, the development of an alternative product, a decrease in the solvency of ordinary consumers, an increase in taxes, and the pricing policy of closest competitors.

In order to minimize such unpleasant situations, company specialists must promptly respond to any changes observed in this segment of the economy.

Technical risks take into account the decommissioning of main equipment, low-quality raw materials, as well as the need to purchase new mechanisms.

To minimize this type of risk, preventive work is planned and control is carried out at each stage of production.