Why US oil production is not growing

In 2021, due to falling oil prices, shale producers were forced not only to curtail expansion, but also to close some already launched projects that were unprofitable in the new price realities. At the beginning of 2021, oil prices returned to pre-pandemic levels, as a result of which the break-even point for all shale projects was passed, and the forecast cash flow was sufficient to increase production. However, there is no growth.

Below is a chart of production costs for new oil projects around the world, prepared by IHS Markit for presentation to the Saudi Aramco IPO at the end of 2021. The chart clearly shows that almost all onshore and most offshore projects in the United States are profitable at current prices.

If at the beginning of the year the passivity of shale producers could be explained by vague prospects due to COVID-19, at the moment market participants’ view of demand prospects is exclusively bullish. Prices have stabilized at high levels and allow you to hedge supplies at a comfortable price for the year ahead.

Drilling activity is still below pre-pandemic levels, but it is quite sufficient to maintain stable production and, albeit slightly, increase production. The number of active oil rigs in the United States, according to Baker Hughes, at the beginning of May is 344 installations. with 280–300 mouths required for stable production. (Rystad Energy estimate).

Meanwhile, we are seeing stagnant production, which is hovering around 11 million bpd, and forecasts are gradually being lowered. The US Department of Energy in its May Short-Term Energy Outlook (STEO) once again lowered its estimate of American production in 2021, to 11.02 million bpd. Earlier in April, the department forecast 11.04 million bpd, and in March - 11.15 million bpd.

What is the reason for the lack of production growth? Let's consider the possible reasons and try to assess whether they will remain relevant in the second half of 2021.

Pressure from shareholders.

Shale shareholders, even before the COVID-19 pandemic, were pushing to slow expansion, reduce debt burdens and ensure higher cash flow to shareholders. Against the backdrop of a pandemic and mass bankruptcies in the sector, the only way to maintain the goodwill of investors was to change course to the changes listed above. At the end of 2021, most oil majors announced their intention to focus on margins and increase the share of free cash flow distributed to shareholders.

“The latest earnings season shows that even with rising oil prices, companies continue to prioritize accelerated balance sheet improvements and higher investor returns over increased capex and growth costs,” Rystad Energy said in a press release. “From a cash flow perspective in the upstream [exploration and production] segment, we see that this year reinvestment rates will drop to 57% in the Perm region and to 46% in other oil regions.”

Policy of the new US administration

The new US President Joe Biden and his team pay great attention to environmental initiatives, among which quite ambitious goals have been set to reduce CO2 emissions. At the beginning of the year, the president canceled some of the benefits for the development of new fields on federal lands, which prevented medium and small independent oil producers from increasing production.

It is not yet clear what other initiatives the new administration might take to curb dirty energy. In addition, Biden's announced tax increases could have a serious impact on companies' cash flow. Rystad Energy estimates that at an average price of $55 per barrel WTI in 2021, the shale industry could generate about $43.8 billion in free cash flow, of which about $9.1 billion could be spent on debt servicing. The remaining $34.6 billion represents an impressive amount, which could be enough to both reward shareholders and expand production. However, increasing the federal corporate tax rate from 21% to 28% would reduce this amount by $4.1 billion (-12%), and the potential elimination of tax deductions would take another $2.9 billion (-8%) away from the sector.

What will happen to production in the second half of 2021?

Given the regulatory risks, most companies can take a wait-and-see approach and refrain from aggressive expansion. At the same time, persistently high oil prices and optimistic forecasts for the industry may lead to some companies taking cautious steps towards increasing production; production may mainly increase in the Permian Basin, where margins are highest.

Taking into account drilling activity forecasts, companies' investment plans and moderately optimistic price forecasts, it can be assumed that by the end of the year, US production could rise to 11.3-11.4 million bpd, which is approximately the same as the market consensus forecast. At the same time, it is worth closely monitoring leading indicators, such as weekly statistics on drilling activity from Baker Hughes and the monthly Drilling Productivity Report from the US Department of Energy. In my opinion, there are still risks of exceeding the forecast.

BCS World of Investments

Oil prices

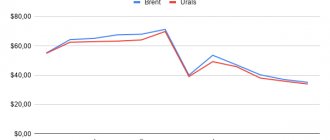

According to EIA estimates, the average price for Brent crude oil in 2021 was $41.69/bbl. against 64.34 US dollars/barrel. in 2019. WTI oil prices fell to $39.17/barrel. from $56.99/bbl. The EIA raised its forecast for oil prices in 2021 and also announced expectations for 2022. The forecast for the average price of Brent oil in 2021 was raised from $48.53/barrel. to 52.70 US dollars/barrel. For WTI oil, the price forecast for 2021 was increased from $45.78/barrel. to $49.70/bbl. In 2022, the average price for Brent oil will be $53.44/barrel, WTI - $49.81/barrel.

World situation

Oil is the most important strategic resource that everyone needs. Exporters are in a more advantageous position; they dictate prices, and importers depend on them. Each country strives to acquire either its own large deposit or a reliable supplier who will provide them with everything they need.

The situation in the world is constantly changing. Until recently, England and Norway only imported oil and petroleum products, and only in the 1970s did they begin to export it to other countries. Many small states take advantage of their advantageous location, and if oil transits through their territory, they reduce their tariffs on raw materials.

The Middle East initially made large supplies, but under the pressure of American policy and sanctions it is now in a deplorable situation. But Saudi Arabia and the UAE, on the contrary, were able to emerge from severe pressure from America and become one of the leaders in oil exports.

Who are the main oil exporters now? They can be easily divided by the regions they occupy in the world:

- Asia is Saudi Arabia, UAE, Iraq, Iran, Qatar.

- Europe – Russia, Norway and Great Britain.

- America – this includes Mexico, Canada and Venezuela.

- Africa is Angola, Algeria and Nigeria.

We have collected original reviews on this topic here, reviews from real people, many comments, worth reading.

As you can see, the largest countries in the world are about a dozen, which is not as many as we would like. At the same time, the situation on the world stage is very changeable.

History of development

The oil refining industry is a branch of heavy industry, including the refining of oil and petroleum products. The history of the development of this industry in the United States is quite new. Its appearance and establishment in the states is associated with the strategic need of the country and the satisfaction of needs and requirements. It was the progress in the field of motor transport that accelerated and strengthened the country’s activity towards the extraction and processing of black gold (On the topic: The origin of oil and its properties).

- 1859 - a well was drilled in the Pre-Appalachian Basin. It became the first well for the United States;

- 1920-1930 - expansion and development of the oil refining industry, in connection with the use of the internal combustion engine;

- 1970s – the share of oil consumption increased to 45%.

Interesting to know! The maximum volume of oil production in the United States was recorded in 1972 - 528 million tons of oil.

US oil giants

Largest US oil companies:

- Exxon Mobile Corporation. A global corporation created in 1999 by the merger of Exxon and Mobile. Oil production is concentrated in many countries, including the United States, Canada, and the Middle East. The company's official reserves are 22.4 billion barrels.

- Chervon Corporation. Created in 1879 in Pino Canyon, California. Today the company owns a large number of processing plants and gas stations. The company's official reserves are 13 billion barrels.

- Amoco Corporation (formerly Standard Oil Company). The largest oil and gas producer in the United States and in the world market. The company was founded in Indiana in 1889. Later, in 1998, it merged with the BP company (UK).

Largest oil fields in the USA: Texas, New Mexico, Louisiana, Oklahoma. The supply of black gold from these states accounts for about 70% of the total flow.

Natural gas production in the world by country

State of the Oil Refining Industry

US oil refining is in first place in the world. Refineries are located near the main consumers, and not near the oil fields. Thus, the main capacities are located on oil pipelines, near port terminals and industrial hubs.

Geographically, the centers of the oil refining industry are:

Oil production in the USA

- In central and southern California;

- Along the Atlantic coast;

- Near the Gulf of Mexico.

The total length of oil pipelines throughout the country is about 300 thousand km. Most of the pipelines are concentrated near the Gulf of Mexico. It is here that the distribution network connects the fields with ports and refineries.

The United States is a leader not only in the production of petroleum products, but also in their consumption. The low cost of American petroleum products is ensured by a developed pipeline system and a high level of development of road transport infrastructure. Competition within the country, the correct location and a sufficient number of refineries also contribute to lower prices. It is impossible not to note the successful government policy in this matter.

According to statistics, the United States produces about 24% of the world's petroleum products.

The US oil industry produces:

- Lubricants and electrical insulating materials;

- Motor oil of all types;

- Automotive fuel;

- Raw materials for the chemical industry;

- Solvents.

In the production sector, motor fuel occupies the largest niche, which is associated with the maximum number of personal cars among Americans. This category includes diesel, jet and gas fuel, high-octane gasoline, and kerosene for aviation.

America's Leading Oil Refiners

The US oil refining complex operates on the principle of reducing the number of enterprises while increasing the capacity of existing refineries. The bottom line is that small oil refineries find themselves uncompetitive next to the industry giants and are forced to close.

US refinery capacity is measured by annual production output in millions of tons. As a result, the largest companies were recognized as:

- Exxon Corporation from Louisiana, whose production capacity is 22 million tons.

- with a location in Texas, the city of Port Arthur. Its figure is 20 million tons.

- Exxon Corporation's second production site, located in Houston, with a production capacity of 19.7 million tons.

- Amoco Oil from Texas (Texas City) with a production of 16.4 million tons.

The US oil industry is concentrated in the hands of 10 oil and gas monopolies, which own 60% of oil and gas refineries and production wells. This “ten” owns the main oil pipelines and a fleet of tankers, as well as points of sale of petroleum products around the world.

World leadership is held by the Exxon Mobil corporation, created by Rockefeller.

TOP largest oil importing countries

Countries that purchase raw materials for their needs are called importers. Traditionally, the largest regions include regions with developed economies that need constant replenishment of their technological resources, automotive and other industrial sectors.

Who is the current import leader:

- China – 459.3 million tons,

- USA – 247.8 million tons,

- India – 226.6 million tons,

- South Korea – 151.3 million tons,

- Japan – 149.3 million tons,

- Germany – 85.2 million tons,

- Spain – 68.2 million tons,

- Italy – 63.4 million tons,

- Netherlands – 56.9 million tons,

- France – 52.8 million tons.

If you look at the ranking of countries that are leaders in oil consumption, the indicators will be somewhat different. Most of these states combine importers and exporters, balancing their needs and supplies.

You might also be interested in these articles:

As you can see, the rating of the largest exporters and importers of oil and gas depends on how economically developed the country is, what reserves it has, and how favorable its geographical location is.

09.10.2020 Information about the authors | Category: Miscellaneous