Lazy Investor Blog > Stock Exchange

Recently, conservative instruments with predictable returns have become increasingly popular among investors. Since the topic rose to the top of my most requested by subscribers, I decided to make another review. We continue to dive into the topic of debt securities, this time into amortizing bonds.

Bonds and their types

To begin with, let me very briefly remind you what bonds are.

A bond is a debt obligation that is issued to borrow money from investors for a fee. Bonds can be issued by the state, municipal authorities, public and private companies. I wrote more about what bonds are in the article Stocks and bonds: main differences.

Based on the method of payment of remuneration, bonds can be of two types:

- Interest bonds. According to them, the investor is paid a pre-agreed coupon income, which is calculated as a percentage of the par value of the security, within a specified period of time.

- Discount bonds. They are sold to investors at a price below par value, and are redeemed within a specified period at par value. The difference in price is the investor's income.

How to make money from them

OFZs, like many similar securities, provide good opportunities to earn money. The most attractive thing is the constant, guaranteed payment of the coupon rate or interest.

The interest income received can be reinvested or invested every 6 months in:

- to purchase new bonds, increasing your interest income;

- in the acquisition of shares of highly reliable issuers (companies) to receive income from the growth in the value of shares and dividend payments received on them;

- accumulation on bank deposits.

Drawing. Scheme of investment capital operation according to the “Combine” bond strategy.

The second type of income is when the value of OFZs on the market increases. Then they can be sold profitably. However, it is worth remembering that “folk” ones are not traded on the secondary market. They can only be sold at a profit from the bank - agent or broker through whom they were purchased.

How is the OFZ rate calculated?

The nominal OFZ interest rate or its coupon income is expressed in % per annum. However, in reality there is a concept called the “effective interest rate”. This rate takes into account the fact that interest earned on income in the first year is reinvested in the second year, etc.

Those. capitalization of investments occurs through the accrual of interest on interest. This rate is calculated using the well-known compound interest formula.

What is the profitability

The yield or coupon yield of OFZs depends on the periods in which they were placed and in what tranche. As practice shows since 2021, the average percentage profitability of OFZs is in the range from 7.1% to 10.5%.

Risks

It should be noted that the acquisition of even highly reliable bonds does not relieve the investor from risks. Such risks may be:

- the issuer's default or failure to fulfill its obligations to repay the debt. No one expected the government to default in 1998, but it happened and investors lost their investments;

- depreciation of the national currency - the ruble;

- risks associated with storing bonds purchased in paper form.

Are they taxable?

You can make good money on government bonds. Moreover, this earnings are supplemented by tax deductions in the amount of 13% personal income tax. This deduction is provided only if the investor has not sold his bonds for 3 years.

The minimum investment amount should be 400 thousand rubles per individual investment account. Thus, the amount of tax deduction will be 52,000 rubles for 3 years. If the investor decides to sell his bonds before the expiration of the 3-year investment period, then he will have to pay a tax on the interest received in the amount of 9%.

Is it profitable to buy

It is always profitable to invest money in Russian government securities. This is even proven by the fact that almost 40% of OFZ buyers are foreign investors - non-residents.

Why are OFZs attractive? The fact that the investor receives a state-guaranteed financial flow of profit for several years, and even with the provision of tax benefits and deductions.

Is it possible to buy on IIS?

Almost all OFZs can be bought and sold through your open IIS account. The only exceptions are those denominated in euros (eurobonds). These bonds are intended for non-resident investors, and the minimum lot for such securities is 100,000 euros.

Where can I see the list of products available for purchase?

OFZ-N can only be purchased through banks.

The general list, as well as the rating, current and future OFZ issues can be viewed on several resources. This is, first of all:

- website of the Moscow Exchange MOEX - www.moex.ru;

- on the website of the RBC consulting agency www.quote.rbc.ru;

- on the websites of brokerage companies;

- on numerous websites and forums dedicated to the topic of trading and investment, for example, https://smart-lab.ru/q/ofz/.

How much does 1 piece cost?

About 1030 rubles.

The cost of OFZ-N is not equal to the face value. As a rule, the true price of OFZ on the market is determined by the current market conditions, supply and demand. Therefore, it may differ from the face value by percentages and even tens of percentages.

Bonds with debt amortization

Debt amortization bonds are a type of interest-bearing bond. Throughout the entire period of circulation of these securities, not only coupon income is paid, but also partial repayment of the debt itself is made. This is reminiscent of the depreciation of fixed assets in an enterprise, which is why such bonds received this name.

In other words, debt amortization bonds are bonds in which the debt is repaid in installments, and the income is paid in coupon payments, with each coupon payment calculated on the balance of the debt.

Amortization of bonds is a phased partial repayment of debt on them to the investor.

In simple words, amortization of bonds occurs in the same way as repayment of a loan with a standard repayment scheme: the body of the debt and interest accrued on the balance of the debt are repaid according to an established schedule.

To make it even clearer, let's look at this with an example.

How is such a bond repaid?

Bond depreciation repayment follows the same schemes as coupon payment and full bond repayment:

- the depreciation date arrives;

- the issuer transfers money to the broker;

- the broker pays the investor.

For OFZ and municipal bonds, settlement is made same day; for corporate bonds, sometimes there is a delay of 2-3 days, but usually the broker transfers money to investors the very next day.

As a rule, the date of the next amortization coincides with the date of coupon payment, so the investor immediately receives part of the bond's face value and accrued income.

Calculating bond amortization: example

Suppose an investor purchases a bond with debt amortization worth 30,000 rubles with a yield of 10% per annum, a circulation period of 3 years, annual debt amortization repayment in the amount of 1/3 of the par value and annual payment of coupon income. How to calculate investor income?

After 1 year, the investor will be paid a coupon income of 10% of 30,000 rubles = 3,000 rubles and the first depreciation repayment - 1/3 of 30,000 rubles = 10,000 rubles .

After 2 years, the investor will be paid a coupon income of 10% of the debt balance of 20,000 rubles = 2,000 rubles and the second depreciation repayment - 1/3 of 30,000 rubles = 10,000 rubles .

After 3 years, the investor will be paid a coupon income of 10% of the debt balance of 10,000 rubles = 1,000 rubles and the last depreciation repayment - 1/3 of 30,000 rubles = 10,000 rubles .

In total, the investor will return the invested funds in the amount of 30,000 rubles and earn 3000+2000+1000= 6000 rubles .

The investor's income for the entire period of holding the bond will be (6000/30000)*100% = 20% . In terms of annual yield, this is 20/3 = 6.67% per annum .

The real yield of 6.67% per annum is less than the stated 10% per annum, but at the same time, the investor’s investments were returned not at the end of the term, but annually, in parts, and he, if desired, could further reinvest them, for example, in other similar bonds, which would increase the total return on investment.

If these were not bonds with debt amortization, but ordinary interest-bearing bonds, then the investor would receive 9,000 rubles of income (10% of the nominal value annually), but would also return the investment amount in a lump sum at the end of the term.

How to choose

You need to pay attention to the maturity date, yield and type of coupon (more on that below). The repayment date should be selected for the moment when the money will be directly needed for targeted purchases, while it is important to remember that the longer the period, the higher the profitability, recommends Sergei Korolev, Investment Director of VTB Bank.

A bond may be worth more or less than its face value. The price at a given time is indicated as a percentage of its face value. Thus, OFZ with a nominal value of 1000 rubles can at some point be purchased for 99%, or for 990 rubles. If you buy, this can be profitable, but if you sell, there is a risk of losing some money. The cost of paper can vary depending on a variety of factors, but it is always repaid at par, so a correctly chosen repayment period will help avoid price fluctuations, recalls Sergei Korolev.

For example, now an income of 7% seems attractive because it exceeds the maximum rates on bank deposits, which remain at the level of 4-5%. But if in three or five years the Bank of Russia raises the key rate and interest on deposits rises, then the yield on OFZ will no longer differ from deposits, this may lead to a decrease in the price of securities, warns Veniamin Kaganov.

Benefits of bond amortization for the issuer

Why are bonds with debt amortization interesting for the issuer? The main benefit is that by depreciating and partially repaying the debt, the issuer reduces its fees for using borrowed funds.

Why does a company issue bonds? To attract borrowed funds and invest them in your business. The invested funds begin to work and gradually pay off. This allows the issuer to immediately begin partial repayment without waiting for the end of the term, thereby reducing its costs.

Profitability calculation

The coupon of this type of bond is constantly changing, in addition, part of the par value may not cover every coupon payment.

This makes it very difficult to calculate the yield of such bonds. It makes sense to look at the stated annual interest rate if you buy a security on the issue day and plan to hold it until maturity. If it is already in circulation, which is most likely, then the QUIK terminal and the rusbonds website (in the “Yield” tab) will show you the calculated yield to maturity.

If you plan to buy them for a short period (relative to the life of the entire bond, for example, 2 years is also short), then you will have to carefully count each payment separately manually, adding everything up gradually to get two figures: how much you invested and how much you will receive. And from this you can calculate the annual percentage.

Benefits of Bond Amortization for the Investor

What are the benefits of bond amortization for an investor? At first glance, it may seem that such securities are unprofitable for an investor, since their real yield is less than the declared one. But it all depends on how to use this tool.

If, upon receipt of amortization of bonds, the funds received are immediately reinvested in the same instrument, then the yield as a whole, as a rule, is higher than the yield of ordinary interest-bearing bonds. Because rates on bonds with debt amortization are higher than rates on regular interest-bearing bonds.

Investments in bonds with debt amortization become especially profitable when the key rate in the country is expected to increase. Because after it the price of loans and bond yields will rise. If an investor has ordinary bonds in his portfolio, the invested funds will be frozen for a long period. If the bonds have debt amortization, they will gradually return, which will make it possible to invest in new bonds with higher returns.

Let's summarize all of the above and highlight the main advantages and disadvantages of bonds with debt amortization.

Types of bonds on the Russian market

The debt market is the oldest of the financial markets, which today is represented by a wide variety of instruments. The Russian bond market is no exception in this sense. It is easy for an inexperienced investor to get confused in the first couple of days in the variety of debt securities.

How does a variable bond coupon differ from a floating coupon? What yield should we focus on: current, at maturity or at the offer date? How are municipal bonds different from government bonds? What is junior debt and how to avoid the risk of subordinated bonds? What is debt amortization? We will answer these and other common questions in this article.

Classification of bonds by presentation currency

According to the law, all payments on the territory of the Russian Federation are carried out in rubles. Accordingly, the vast majority of bonds traded on the domestic market and available to private investors are denominated in national currency. The par value of bonds is most often 1000 rubles, income is paid in the form of coupons and they are traded mainly on the Moscow Exchange.

Bonds denominated in foreign currencies (mostly euros and US dollars) are called Eurobonds. The main trading volumes of Eurobonds take place on the over-the-counter market, but some securities are also available on the Moscow Exchange.

When investing in such securities, it is necessary to take into account tax features. The calculation base for personal income tax for them is not only the main income, but also income from exchange rate differences. The Ministry of Finance of the Russian Federation is currently developing a bill that will exempt investors in government Eurobonds issued after January 1, 2021 from personal income tax on income from exchange rate differences.

Classification of bonds by type of issuer

Based on the type of issuer, bonds on the Russian market can be divided into three large categories: state, corporate and municipal.

Government bonds

The most common securities in this category are federal loan bonds (OFZ), which are described in detail in the article OFZ: How they differ and which ones to buy. OFZs have good liquidity, a wide range of investment terms, a low probability of issuer default, and the coupon income on them is exempt from personal income tax. Most often, the coupon is paid on these securities once every six months, but there are exceptions. Among the disadvantages, one can note the low profitability, which is compensation for the low credit risk.

Corporate bonds

This category of securities represents debt securities of individual companies. They are distinguished by higher profitability than OFZ. Often the coupon for them is variable. Income, both coupon and increase in market value, is subject to income tax, but there are exceptions in the form of corporate securities issued after 2017 inclusive, for which coupon income is exempt from personal income tax. A list of such papers can be found in the following article.

It is necessary to separately note subordinated bonds of corporate issuers. A subordinated bond is a loan from a company that ranks below other loans and borrowings in the event of liquidation or bankruptcy of the company, so-called junior debt.

In other words, holders of subordinated bonds will be the last ones, other than shareholders, to receive their share of the company's assets in bankruptcy. Such securities are a riskier investment, and are rightly accompanied by higher returns.

To calculate the risk of a portfolio, it is necessary to know for sure whether it contains debt securities of subordinated issues, the credit risk of which is higher. A private investor can find these bonds among bank debt securities, since for them this form of raising capital is convenient for a number of reasons. The list of subordinated bonds of Russian banks can be found here.

Subfederal and municipal bonds

This type of debt securities can be issued by constituent entities of the Russian Federation (subfederal) and municipal entities (municipal). The market for these bonds is small relative to other types of securities, which in turn affects liquidity. About half of the entire market is made up of issues from Moscow, the Krasnoyarsk Territory, the Samara and Nizhny Novgorod regions. Coupons on these bonds are not subject to personal income tax, while the yield on the securities is slightly higher due to lower reliability. Quite often, such bonds provide for debt amortization.

Important! State and municipal bonds are not identical in terms of credit risk. Of course, the state will do its best to help the region fulfill its obligations if the latter finds itself in a difficult financial situation. But a default by the issuer is still possible, including if the state is solvent, so the risk of such investments is higher than when investing in ordinary OFZs. It is not correct to buy regional bonds because of higher yields and consider them equal in reliability to state bonds.

Classification of bonds by type of income generation

Discount (zero-coupon) bonds

Bonds of this type do not provide for coupon payments. Such bonds are initially placed below par value, and the investor's income is only the difference between the purchase price of the paper and the redemption/sale price. Such securities are quite rare on the Moscow Exchange.

Fixed coupon bonds

A fixed coupon is a certain percentage of the face value, which is paid at predetermined intervals. The interest rate on a bond is known from the moment of issue and, as a rule, is the same throughout the entire circulation period of the paper. For such a security, you can draw up a schedule of coupon payments with exact amounts and unambiguously calculate the yield to maturity.

Example: Corporate bond SberB BO37 with a fixed coupon. This bond provides for payments every six months in March and September at the rate of 9.25% per annum. The maturity date of the bond is September 30, 2021. For such a bond, the yield to maturity can be accurately calculated, including taking into account the reinvestment of coupons.

Variable coupon bonds

Bonds with variable coupons are quite common among corporate securities. For such bonds, the coupon is fixed until the offer date, after which the interest rate changes depending on market conditions. However, the new interest rate is unknown before the offer is made. This mechanism allows the issuer to reduce interest rate risk, especially if the issue is placed during a period of high interest rates with the prospect of their reduction. And the investor, in turn, has the opportunity to repay these bonds early under the offer. In the intervals between offers, such securities are no different from bonds with a fixed coupon, with the only difference that the yield is correctly calculated not to the maturity date, but to the date of the nearest offer. Read more about the offers in the article Offer on bonds. What does an investor need to know about this?

Example: corporate bond ObuvrusB1 with a variable coupon. The bond maturity date is 07/15/2020, the current interest rate of 15% is valid only until the offer date of 07/17/2019. After this, the coupon value will be calculated at the new interest rate.

Important! In the QUIK terminal, there is a “Yield” column in the bonds table. It is worth considering that the correct value can only be obtained for bonds with a fixed coupon, for which the interest rate is known for the entire circulation period. For other securities, you need to calculate the yield yourself or use specialized information resources.

Bonds with a floating (indexed) coupon

The interest rate on such securities is tied to changes in some other indicative financial instrument. This instrument can be the key rate of the Bank of Russia, the consumer price index, the RUONIA rate, the dollar exchange rate, the LIBOR rate (for Eurobonds) and others. As a rule, you can calculate the coupon size for such securities for no more than one coupon period. The calculation formula is published by the issuer and is available to all investors.

Bonds with a floating coupon are inconvenient because future yield can only be predicted, which is not always possible, especially if the formula includes several indicative instruments. However, this form of coupon is good because it allows you to insure yourself, for example, against a sudden change in the interest rate, as was the case at the end of 2014, when the key rate was increased by 6.5%. For securities with a rate tied to it, the coupon was indexed, and investors received higher payments during this period, while fixed-income bonds compensated for the increase in yields by reducing the par value, which was extremely unprofitable for investors owning the securities.

Example 1: corporate bond Rosneft BO-18 with a floating coupon. The interest rate is determined based on the Key Rate of the Central Bank of the Russian Federation plus 0.1%, but not less than 0.01%. The key rate is determined as of the 5th business day preceding the start date of the calculated coupon period. Thus, the next coupon for the period from January 22, 2018 to April 23, 2018 is calculated at a rate of 7.75 + 0.1 = 7.85% per annum.

Example 2: Russian Railways corporate bond 32 OBL with a floating coupon linked to the consumer price index (CPI) in the 2nd month preceding the month of the start of the next coupon period. The interest rate is calculated using the formula (CPI-100%)+2.1%. Thus, the coupon for the period from 01/12/2018 to 07/13/2018 will be paid at a rate of 4.6% per annum. The table below shows all calculated coupon payments during the circulation period

Classification of bonds by type of par value redemption

Full repayment of the face value at the end of the term

By default, the principal amount is paid to the investor in full on the bond's maturity date. This type of repayment is the most common among securities on the Moscow Exchange.

Bonds with indexed par value

Sometimes the float for a bond is not the coupon, but the par value of the paper. A striking example is the OFZ 52001 bond, for which the coupon is fixed at 2.5%, and the nominal value is annually indexed to inflation. This type of OFZ is quite good in times of high inflation or as insurance against a future acceleration in price growth.

The downside is that it will be received only upon redemption or sale; therefore, it will not be possible to reinvest it during the circulation period.

Amortizing Debt Bonds

For most bonds traded on the Moscow Exchange, the par amount is paid to the investor in full on the maturity date. However, the issuer may not be comfortable with such a form of borrowing, in which by the maturity date it will be necessary to accumulate a large amount of money to repay the issue. Then he issues an amortizing bond, the par value of which is repaid in installments in parallel with the coupon payments. This allows the issuer to distribute debt repayments evenly over the entire circulation period. Such securities are often found among municipal bonds.

For an investor, other things being equal, this type of redemption is less profitable, since after receiving part of the par value, the next coupons are accrued on the remaining value of the paper, due to which the total income is less. However, this type of paper can be useful during periods of low interest rates when interest rates are expected to rise. Then the returned part of the nominal value can be reinvested at a higher interest rate.

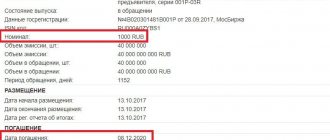

Example 1: Discount bond OFZ-46005 with debt amortization. The bond was issued in 2003 with a discount to the nominal value of 1000 rubles. On January 10, 2021, investors were paid 70% of the nominal value (RUB 700), and on January 9, 2021, the remaining 30% (RUB 300) will be repaid. Currently, the security is trading at 95.6% of the remaining par value (RUB 286.8), which upon maturity will give a yield of about 5.27% due to the difference in price.

Example 2: Corporate bond with a fixed coupon and debt amortization AHML 11ob. The bond's par value is redeemed according to the schedule presented below. The interest rate of 8.2% is fixed for the entire circulation period, accrued on the outstanding balance of the par value. Also for this security there is an offer with a call option on September 15, 2018.

Start investing

BCS Broker

Bonds with debt amortization: cons

- During periods of declining discount rates, this instrument looks less profitable compared to bonds without debt amortization, since they fix a high rate of return that the investor will no longer be able to obtain by reinvesting amortization payments.

- To ensure high returns, such bonds require constant reinvestment of payments - this requires time and labor costs, as well as a constant, competent selection of new securities.

- Without reinvestment, this instrument is not profitable and is inferior in terms of profitability to other bonds with a comparable level of risk.

Now you know what bond depreciation is, how depreciation is repaid, yield is calculated, and what the pros and cons of such a product are for the issuer and the investor. Draw conclusions about how interesting bonds with debt amortization are for you.

The Financial Genius website will teach you how to intelligently earn money in active and passive ways, as well as how to optimally manage your personal finances. Stay with us and stay tuned for updates. See you again!

Estimate:

How to get a tax deduction

IIS gives the right to tax benefits, there are currently two types. If you pay personal income tax at work and a significant part of your portfolio is taken up by bonds, then type A deduction is most likely suitable: the Federal Tax Service will return you 13% of the amount deposited into the account during the year, but not more than 52 thousand rubles. (13% of 400 thousand rubles deposited into the account), and such a relatively generous deduction can still be received every year. But to do this, you cannot withdraw money from the IIS earlier than three years after its opening (but inside the IIS you can do anything - sell and buy different securities). This 13% from the state sharply increases the yield of bonds in the first year of ownership.

Investor reviews

- Private pension fund "Radost". Our investors trust us with their money largely because we invest their money only in highly reliable assets. Bonds in our portfolio make up at least 90%.

Drawing. Comparison of bank deposit and OFZ in terms of profitability.

- Vasily Ivanovich is a private investor. I invest money only in OFZs, since there is no longer any trust in deposits in the banking system, much less in the Russian stock market, not to mention all sorts of forex and binary options.

Drawing. Investment preferences of Russians.

- Vasilisa. I withdrew all the money from my bank account and used it to buy “folk” OFZs through IIS - the interest rate is higher and it will be more secure.

Drawing. Dynamics of investment activity of Russian citizens in the IIS and OFZ market.

Where are traded and who can buy OFZ

"People's" are distributed among private investors through agent banks. As a rule, these are banks with state participation - Sberbank, VTB, Bank Russia and Rosselkhozbank.

All other issues are generally traded on the Moscow Exchange - MOEX.

Is it possible to buy OFZ-N without intermediaries?

No you can not.

The only exceptions are ordinary OFZs. You can buy federal loan bonds directly without intermediaries only if the seller is a private or legal entity. In this case, the transfer of ownership of securities is carried out within the framework of the Civil Code of the Russian Federation, under a purchase/sale agreement, certified by a notary and registered in Rosreestr.

Best brokers

In most cases, it is more profitable and faster to buy OFZs through broker companies. In addition, reputable brokerage companies often take on the obligations of tax agents. This eliminates the need for the client to calculate taxes and submit a tax return.

Opening of Promsvyaz by Rick BKS Keith Tinkoff Finam

One of the mastodons of the market. Excellent web portal, very low commissions and adequate support. I recommend!

Investment department of a famous bank. There are no particular advantages, but there are no disadvantages either. Average.

One of the very first Russian brokers. The commissions are high, but there are interesting auto-following strategies.

Another very large broker. Good support and low commissions are their strong point.

Small but reliable broker. It is great for beginners because it does not impose its services and the commissions are very low. I recommend.

The youngest broker in the Russian Federation. There is a cool app for investors, but the fees are too high.

The largest investment company in Russia. The largest selection of tools, your own terminal. Commissions are average.

Is it worth investing in expert opinion?

The overwhelming number of experts (80%) believe the use of OFZ is justified and beneficial in the following cases:

- accumulation of personal investment capital over a long period, for example, for personal pension provision;

- to form an investment portfolio and insure it against currency risks;

- to protect capital.

Advantages over other securities

The main advantage over other types of securities (stocks, options, futures contracts) is:

- low risk, which provides the investor with an income higher than official inflation and more than in a bank;

- receiving tax benefits and deductions;

- the ability to independently manage personal capital, including transferring assets by inheritance or gift;

- state protection of citizens' investments.

Risk, return and liquidity

The reliability of such securities is slightly lower than that of OFZ, but not everything is clear here.

On the one hand, some regions already have very large debts. For example, Khakassia has debts equal to 95% of the regional budget income for the year, and Mordovia has debts 2.5 times more than annual income.

At the same time, Article 102 of the Budget Code states:

The Russian Federation is not responsible for the debt obligations of the constituent entities of the Russian Federation and municipalities if these obligations were not guaranteed by the Russian Federation.

There were even a few cases where municipal bonds went into default, although the obligations were eventually fulfilled.

Data on municipal bond defaults for the period from February 2, 2009 to February 2, 2021 from the website rusbonds.ru. The Klinsky district twice committed a technical default on coupon payments and once a regular default on them. But no one lost money, they were paid, just later than they should have: see the column “Date of fulfillment of obligations”

On the other hand, it is unlikely that the state will allow regions and municipalities to default on their obligations under bonds. If there is a default on them, investors, including foreign ones, will begin to trust Russian bonds less, and then it will be more difficult to borrow money through debt securities.

Bonds of regions and municipalities have a higher yield than government bonds - OFZ. Let's compare one of the OFZs and a bond of the Nenets Autonomous Okrug with similar maturity dates:

- OFZ 26222 with maturity in October 2024: current yield - almost 7.4% per annum, effective yield to maturity - about 8.2% per annum.

- NAO 2021 with maturity in November 2024: current yield - about 8% per annum, effective yield to maturity - about 9.5% per annum.

There is no tax on coupons, as is the case with OFZs.

Please note: bonds of regions and municipalities are not as popular as OFZs. This means that there is less liquidity and sometimes it is difficult to buy or sell a large block of bonds at an adequate price.