We have already figured out earlier that the Family budget is the income and expenses of the family for a certain period of time (month, year). Family budget allows you to control money in the family and distribute it correctly. To understand what the family budget consists of and how it works, we will break it down into its component parts.

So, there are two components in the family budget - the INCOME part and the EXPENDITURE part.

What are they formed from?

The family receives income and spends it in the form of consumer spending.

Income is money or material assets received from a business, individual, or activity.

All income is divided into

- Cash income consists of:

1) salaries along with various accruals and additional payments; 2) pensions, benefits, scholarships and other social and insurance payments; 3) income from business activities; 4) income from transactions with personal property and cash savings. Wages average 45-50% of a family’s total cash income.

- Income in kind consists mainly of material benefits received from a personal plot (vegetables, fruits, meat, eggs, honey, etc.), gifts, winnings, food allowances, etc.

- Benefits are received by certain categories of the population determined by government agencies. For example, discounted travel tickets for students and pupils, discounts on utility bills, when purchasing medicines, discounted vouchers to sanatoriums, holiday homes, holiday camps for youth, etc.

Who needs a family budget and why?

Every family makes plans or dreams about something. This could be an annual trip to the sea, a trip around the world, buying a new car, cottage or apartment by a certain age. Many Russians at the age of 30-35 think about retirement and that they want to lead a comfortable old age, which the state cannot provide. At the same time, some families achieve their goals, while others cannot find money even for current needs, although peers with the same income level and number of children can be taken for comparison.

It is possible to live without drawing up and maintaining a family budget. As research by HSE senior researcher Olga Kuzina shows, about half of the country’s population does just that. At the same time, 10% of Russians do not know exactly how much money they receive during the month and what it is spent on. This practice has a deplorable effect on the lives of citizens. In 2021, the level of debt among the population reached 32%, which is another 2% higher than a year earlier. If you don't start planning your family budget now, you or your children will make these statistics worse.

Level of debt load of Russians.

Data for November 2020 For anyone who monthly goes into overdraft on a salary card, buys an iPhone in installments, or pays for compulsory motor liability insurance from credit money, it is advisable to understand their attitude towards money. Most likely, such a person will not be able to say how much money he has in his wallet, on his card account, or how much debt he has already accumulated on a credit card. Drawing up a family or personal budget will help change the situation.

A family budget is a financial report that reflects the income and expenses of all family members.

At the same time as your family budget, develop a personal or family financial plan that takes into account short-, medium- and long-term goals. Correct calculation and planning of the family budget helps to achieve financial goals. Remember that setting a goal is not enough. It will be necessary to constantly record the income that comes from all family members and control spending on individual and general needs.

Poll: How much do you spend on utilities per month?

Periodically check current Internet and cable TV rates. Providers often introduce new profitable tariff plans, and you can use the old “expensive” tariff for years.

For those families who live in a rented apartment, savings are especially important. The less you pay for rented housing, the more money remains for other expenses. If the transport infrastructure in your city is developed, then it is not necessary to rent an apartment in the city center. The price of housing in residential areas is much lower. You can easily save money and reduce your monthly expenses by several thousand rubles if you rent an apartment in a residential area with good transport accessibility.

Mortgage repayment costs can also be reduced. To do this, you need to study bank offers on loan refinancing. Surely some bank will have a better offer. By reducing mortgage payments by a couple of thousand per month, you can save 10-30 thousand rubles per year on your budget.

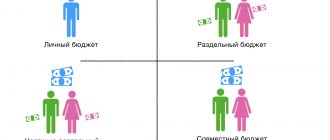

Types of family budgets

There are 4 types of family budget:

- Separated. The initial option for maintaining a family budget upon marriage or cohabitation, which for some couples remains for life. Difficulties may appear after a long period, when it becomes difficult to divide common expenses. This can be avoided by calculating family expenses and dividing them in proportion to income or equally, as the spouses agree.

- Joint. All income is shared and the spouses are jointly and severally liable. A common model for families with children who live together for a long time.

- A mixed budget is suitable if the partners are willing and able to agree on joint financial plans and goals. At the same time, both spouses maintain financial independence.

- Sole proprietorship presupposes the absence of a second spouse or his complete dependence. The second option can lead to conflicts and misunderstandings between spouses.

Each family decides for itself which type of family budget to choose.

Pros and cons of different family budgets

The family budget model is chosen by spouses, but each option has its own advantages and disadvantages that deserve attention:

| Type of family budget | pros | Minuses |

| Separated | Everyone is responsible only for their own financial income and expenses and is in no way dependent on other family members. | Disagreements may arise regarding shared expenses. Poorly suited for couples in which one spouse earns significantly more than the other, increases tension in such marriages. |

| Joint | A shared budget unites the family. Both spouses receive equal rights to manage funds. The goals set are clear and achievable, with a properly planned family budget and financial plan. If one spouse earns significantly more than the other, a joint budget relieves tension if there is agreement on goals and expenses. | Unless you establish rules for spending the overall budget, it is difficult to avoid conflicts. Most purchases will have to be negotiated. Sometimes a minimum threshold is set at 1,000 or 5,000 rubles, above which the second spouse is notified. Difficulties arise with unexpected, spontaneous surprises and large gifts for the other half. |

| Mixed or conditionally joint budget | Spouses remain financially independent and can spend their income as they wish. But the family’s expenses and common goals are established, and everyone contributes their part to realize them. It's easy to give spontaneous gifts and surprises, which is very important for some couples. | Requires the most frequent revision and adjustment. The frequency of verification of adherence to the plan is 3-4 times a year. The couple decides who is responsible for which areas: who pays for housing and communal services, kindergarten, sections, who is responsible for the financial plan and its verification. |

| Sole | Only one of the spouses receives income, and he also provides money for maintenance to the second spouse and children. The second option is if there is only one adult in the family who provides for the rest of the family members. | A difficult situation for the dependent party. It is almost impossible to avoid conflicts or pressure. |

If you know what nuances and reasons for conflicts are possible with each option for managing a family budget, you can minimize them or choose a different format.

What will help you stick to your family budget?

In all family budget models, the most important rule is the ability to negotiate. If the spouses succeed, they can use any of the described options.

The following will help in planning and controlling the family budget:

- mobile banking applications where you can see income and expenses on cards and accounts;

- additional cards for children to control and record their spending;

- setting up SMS alerts about transactions on accounts and cards;

- timely adjustment of set financial goals;

- revision or strict adherence to the chosen strategy in achieving the goal, depending on the current results.

When drawing up a family budget and financial plan, take into account possible risks and create a safety net in case of unexpected changes in life. Additional ways to reduce risks are to take out insurance. For example, compulsory medical insurance for all family members, voluntary medical insurance, at least for those who bring the main income, comprehensive insurance for damages in case of an accident, theft or theft of a car.

How to manage a family budget

There are several ways to keep track of your family budget:

- record all income and expenses on paper Then calculate the balance once a month. The most affordable, but tedious option for most families. Not everyone is able to meticulously record the same type of expenses every day. After a few weeks or months, the process is abandoned due to monotony.

- Google or Excel spreadsheets . Such formats allow you to customize all lists to suit your needs, highlighting the final and intermediate values in color or a different font. Most operations can be automated if you set formulas for calculations. For example, to draw up a family budget, use a ready-made template. Same or projected income and expenses can be copied so as not to waste time on it. As a result, updating data takes up to 2-3 minutes a day. Google Sheets also contains ready-made templates for the annual and monthly family budget.

- Special programs or mobile applications. Some of the most popular are EasyFinance, CoinKeeper, Monefy, 1Money, Zen Money, Feasy. Applications can be paid, free or shareware. To understand which one is more suitable, download several and choose the one that is most convenient for you. Pay attention to the clarity of the interface, adaptation of the application to a computer, mobile phone, and shared access from several devices. Some applications allow you to configure the synchronization of transactions with bank cards and build graphs and diagrams.

You can combine methods: keep daily expenses in the application, and track financial goals in a table. But in most cases, users choose one option and manage their family budget there.

How to correctly calculate and manage a family budget

The process of preparing for drawing up and maintaining a family budget consists of 5 stages:

- Set goals.

- Work out a financial plan.

- Collect data on the current situation.

- Analyze the collected information.

- Identify reserves and find sources.

- Plan your income and expenses for the month.

- Analyze the results of maintaining a family budget and adjust the plan.

The stages of developing a family budget overlap and some are repeated from time to time.

Setting a goal

You can maintain a family budget just for the sake of statistics while collecting data for subsequent analysis. If the family's goal is to achieve financial plan goals, the process becomes meaningful and consistent. At the same time, translate any dream from abstractions to specifics:

| Badly | Fine |

| We want to go on vacation to the sea every year. | Save 250,000 rubles annually for a family vacation at sea. |

| It is necessary to carry out major renovations in the apartment in 2-3 years. | Collect 1.5 million rubles for major renovations in an apartment in 2 years. |

| We want to close all loans and not get into debt anymore. | Repay a loan in the amount of 650,000 rubles in a year. |

Not only correctly formulate the goal and deadline, but also select ways to achieve it. Deposits, savings cards, IIS, mutual funds, brokerage accounts will help with this. The shorter the execution period, the more conservative the instruments. For example, when achieving short-term goals, it is risky to invest free money in stocks; it is safer to choose a deposit, savings card or bonds.

Pay attention to the assets and liabilities in the family budget structure:

- Assets are everything that brings money to the family.

- Liabilities are things that do not generate income or reduce them.

For example, a personal car is an asset if it helps to fulfill work duties and earn more, but a liability if it is used instead of public transport or for prestige. It is cheaper to travel to work by minibus, and it does not require refueling or repairs. The same applies to apartments. Living space can become an asset if it is rented out, the cost of which will cover all costs, but otherwise the apartment is a liability, since the family’s money is spent on its maintenance and repairs.

Development of a financial plan

When drawing up a family budget, the question of developing a financial plan arises. It can affect different periods of life and pursue several financial goals at once:

- accumulate capital that will generate passive income of 50,000 rubles per month and ensure a comfortable old age;

- raise money for children’s education at university - 1.5 million rubles by 2030, another 1.5 million rubles by 2040;

- buy a country house in 5 years, 50 km from the city, measuring 80 sq. m, worth up to 10 million rubles;

- leave his children an inheritance of $1 million after 35 years.

Goals should be specific in amount and time frame and take into account inevitable inflation. The more distant the goal is, the greater the amount you will have to save to maintain the same purchasing power of money.

For example, to buy the same volume of goods in 2010 it took 100,000 rubles, and in 2021 – 186,305 rubles. Over 10 years, accumulated inflation amounted to 86.31%. Nobody knows what the level will be in the next 10, 15 or 40 years. Over the past 4 years, the coefficient has not exceeded 5%, and during 2015 alone it was more than 12.9%.

When setting any financial goal:

- take into account the interests of all family members;

- convey the idea of the goal to all family members - even small children are useful to know what their parents are saving money for and how they are bringing their dream closer;

- budget for unexpected and unplanned expenses; if there are none, transfer the remaining amount to a reserve or use it for other purposes;

- use the services of insurance companies to reduce risks;

- take inflation into account in your calculations, at least use bank deposits or savings accounts to reduce its impact on savings;

- increase assets and reduce liabilities.

To understand what is happening with family income and expenses at the current stage, collect statistical data.

Collection of data on the current situation

Review all amounts and balances:

- on bank cards and accounts;

- in piggy banks;

- under the pillow for a rainy day;

- given as a loan to someone.

Indicate all existing debts:

- mortgage;

- car loan;

- debt on consumer loans, credit cards, installment cards, loans;

- debts to neighbors, parents, friends or relatives.

Record all collected and new information in a notepad or electronically, whichever is more convenient. The main thing is that all income and expenses are recorded. Take into account all the receipts and spending of money by all family members, even if the amounts seem insignificant - it could be a chocolate bar for a snack, coffee to go, a pack of cookies or wet wipes.

Data for 2-3 months is enough to understand where money is flowing from and to. Although the first conclusions can be drawn after the first month of maintaining a family budget.

For ease of accounting, systematize the information, divide it into logical groups:

- communal payments;

- food;

- medications and other medical expenses;

- entertainment;

- hygiene and household products;

- car expenses;

- public transport and taxi services;

- present;

- communication services;

- home shopping;

- eating and drinking out;

- paid sports sections;

- paid subscriptions;

- beauty salon, cosmetologist services;

- other bills and expenses.

In the income category include:

- salary;

- bonuses;

- scholarships and other benefits;

- income from part-time work;

- income from rental housing or other property;

- tax deduction refunds, for example, for treatment, training, from IIS;

- profit on savings accounts and cards - interest and cashback.

A family may have more or fewer categories of income and expenses. For some, detailed detailing is important, for others it is enough to determine the main areas of expenses. At the initial stage, consider items more carefully to find hidden reserves and optimize the family budget.

Analysis of collected data

After collecting data for 2-3 months, conduct a detailed analysis. Even longer recording will reveal more hidden trends that may not appear for 1-2 months. For many families, at the analysis stage, it turns out that the most frequent and unplanned expenses are on entertainment and food.

Expense items can be divided into mandatory and optional. Highlight this category in a different color if you are using Google Sheets or another custom tool. The final numbers at the end of each month are the starting points for developing a further plan.

After analysis, it may turn out that a car is not necessary and it is much cheaper for all family members to travel by public transport. Or, in force majeure circumstances, you can replace meals in canteens or cafes by taking home-made lunches with you.

Identification of reserves and sources of income

After 2-3 months it is clear whether the balance of the family budget is positive or negative:

- If a family spends more than it earns, this is a serious reason to think about it. You can end up in credit bondage if you don’t change anything.

- If the difference is positive but too small, look for reserves or increase sources of income.

Combine the search for reserves and sources, then the family will have more money to achieve its goals:

- rent out an apartment where no one lives;

- sell the car if no one drives it;

- monetize your hobby, start self-employment and provide services in your free time from your main job;

- look for a higher paying job.

It will not be possible to form reserves through mandatory payments - you cannot ignore housing and communal services payments or not buy food. But expenses on fast food, bad habits, paid subscriptions or personal vehicles in most cases can be reduced. Also review your entertainment plan and other optional expenses.

After careful analysis, many families manage to find from 10% to 20% of reserves in the family budget, which can be redirected to more reasonable purposes.

Set aside amounts in reserve automatically. Set up automatic payment in Internet banking on the date of receipt of wages or with a reserve of 1-2 days. Transfer 10-15% of all income to a savings card account, brokerage account or other areas of your financial plan.

Financial literacy experts unanimously advise saving money when you receive it, not at the end of the month, because in 2-3 weeks there may be no money left. If the amount has already been transferred to the reserve, it is perceived as if it does not exist at all. As the experience of rationally managing a family budget shows, most families will be able to live not on 100% of their income, but on 90% or even 80%.

Planning income and expenses for the month

Plan your expenses and income for the next month based on conclusions from previous months. In the off-season, new expenses may be added to change your wardrobe or shoes; insurance premiums must be paid several times a year. Include seasonal, semi-annual or annual expenses in your family budget.

There is no shame in saving, but squandering money can be dangerous. Instill in all family members the habit of making lists and not making thoughtless or spontaneous expenses. Always check prices for the same products in several stores. Pay attention to promotions and sales. Apply for store discount cards and use bank cards with cashback.

For those who do not like to use bank cards, paper envelopes are suitable. You can have one for each type of goal: vacation, pension, car, investment or apartment.

The envelope system is also suitable for maintaining a monthly family budget. Divide them into categories:

- for gasoline;

- products;

- clothing and shoes;

- entertainment;

- housing and communal services payments;

- other types of expenses.

When the amount from the envelope has been spent, there is nothing more to spend on this item. This option is the most practical for some families, especially at the initial stage, when the correct financial habits have not yet been formed.

Print out your financial plan and hang it on your wall or refrigerator. This will help all household members remember what the family is saving money for, especially in moments when you want to give up everything and return to a carefree and thoughtless lifestyle. Photos of a new car, a resort or a future country house will serve the same purpose.

Remember the plan is not a dogma, it can be adjusted, but if you can achieve the indicators without serious restrictions, it’s better to do it. At the same time, the very first savings goal for any family budget should be a financial airbag. Typically this is an amount that is enough to cover all family members for a period of 3 to 12 months. Read about how to accumulate it in a separate article by Brobank.

Analysis of the results of maintaining a family budget and adjustment of the plan

At the end of each month, compare planned income and expenses with real ones. If everything goes according to plan, nothing threatens the fulfillment of your financial goals. If the plan fails, the goals will have to be postponed. Reconsider the opportunities to save money, earn extra money, or set a longer period.

At the initial stage, families often underestimate some categories of expenses and overestimate others. The longer the practice of budgeting continues, the fewer such errors.

When a family has developed a financial plan, all family members become partners in the process of achieving their goals. Both children and parents know what the money is being saved for, and in most cases they show understanding.

It is not necessary to tell your kids that you are saving money for old age, replenishing a brokerage account, or some other unclear goal. At the same time, a trip to the sea or a ski resort will be an excellent motivation to deny yourself another car or doll, unless we are talking about a child of 2-3 years old. Starting from the age of 5-7, children learn from the example of their parents how to set financial goals and achieve them. Preschoolers and primary schoolchildren can and should be taught the basics of financial literacy.

If the family manages to save more money than the plan, it can be used to increase the financial cushion or buy assets. These can be stocks, bonds, and other financial instruments for medium- or long-term accumulation.

Where to store money

The work order finally appeared, you honestly put aside 10% of your salary for it. A decent amount has accumulated. The question arises: “What should I store my money in now?” In fact, it all depends on the purpose of the NT. If the reserve was collected for a rainy day, take it to the bank at compound interest. With the possibility of monthly replenishment and withdrawal at any time, so that there is no need for money, and you can withdraw it 3 years after opening the account.

Are you saving for a car or an apartment? Create a deposit account. Partial withdrawal from it is impossible. Therefore, it will not be possible to spend on something unnecessary. There, interest also accrues on the balance, and you will also remain in the black. If you are going to make several purchases, create several savings accounts to avoid confusion. If the goal is to simply save for a laptop or sofa, get yourself a piggy bank, having previously sealed its bottom or lid so that you are not tempted to take out the amount for goodies.

Many banks now have the “Savings” service - this is an account with interest on the balance, which is replenished automatically every time a salary is received. The replenishment percentage is set independently. Such an account can be opened for free and in 1 minute online. It’s not difficult to withdraw money from there, but it teaches you the discipline to think about the future and create a reserve fund.

What to do with debts

It would be a good idea to get rid of debts before starting to create a safety net. Anyone who has debts and loans clearly does not know how to manage their money. The mortgage on the apartment does not count. It’s difficult to save three million with a salary of 30,000 rubles. So, if you have any debts and the goal is to save, try to pay off your debtors as soon as possible. If this doesn’t work out, try saving at least 5% of your salary. This will give you motivation and confidence. Or, look for a bank that lends on more favorable terms than your existing loans and refinance the loan.

Checklist for developing a family budget

- Discuss with all family members that you will start maintaining a family budget.

- Talk to your household about what a family budget is and why your family needs it.

- Formulate one or more financial goals. Don't forget, they can be adjusted or supplemented at any time, so it is not necessary to make the very first financial plan too detailed. For starters, 1-2 goals are enough, which can then be enlarged or, conversely, detailed. The main thing is that the goals are measurable in amount and deadline.

- Determine who collects information on income, expenses and in what way the accounting is done - a notepad with a pen, a table, a computer or a mobile application.

- Record expenses in as much detail as possible, especially in the early stages. This will help in finding reserves for savings.

- Enter income and expense data immediately or daily at the end of the day. Don't put off recording your expenses until later. Directions of expenses are forgotten, and it becomes more difficult to create an objective picture every day.

- Create a table of planned income and expenses of the family budget for the next month. Repeat step six.

- Compare planned and actual income and expenses. Evaluate whether the plan was successfully completed.

- Determine the categories through which you can save your family budget. Analyze opportunities to increase earnings.

- Plan your family budget for all subsequent months and monitor the implementation of the plan. Make adjustments to goals as needed.

Bad habits

Review your bad habits: smoking, for example, or drinking Coke every day. This will be good not only for your wallet, but also for your health. An average of 25,000 rubles to 40,000 rubles are spent on cigarettes per year. Try not to buy yourself a cup of coffee before work. At least not every day. The ritual is pleasant and sets the mood. But per year this amount is about 55,000 rubles.

Try not to lend money to everyone. After all, there are people who do not repay their debts. Learn to say “no” to those who are not close to you and whom you do not particularly trust. Stop taking online loans! Then you have to pay such interest that it’s just “don’t worry, mom.” Is it necessary?

What is bankruptcy of individuals and what consequences does it have, read more in our article.

Summary

A detailed family budget answers the question of where the money comes from and where it goes. A balanced budget builds confidence in today and tomorrow. Some families fix only long-term plans, and then cannot move towards their goal. It is also important for them to start with accounting and analysis. After collecting data, you can plan one large purchase. For example, a joint vacation or a family car. It is very important that the first goal is of interest to everyone, then it is easier to achieve it and not deviate from the intended path.

An important point: savings and financial goals should not lead to strict restrictions. You cannot completely deprive your family of rest or entertainment. Do not deny yourself new clothes or your child in the sports section if they are needed. Find a balance between “needs” and “wants.” Once you learn this, managing your family budget and achieving your financial plan goals will become much more comfortable.

FAQ

What is the most convenient way to manage a family budget?

Everyone determines for themselves how to manage their family budget. For some, a notebook and pen are suitable, for others - a mobile application, for others - a Google spreadsheet or an Excel file. What is more important is not the way of maintaining a family budget, but the regularity of recording the income and expenses of all family members.

How much time will it take to develop a family budget?

One and a half hours a month or 5 minutes a day, if you approach the issue consistently. To begin with, just record all income and expenses and set financial goals. In a month, you will find out how much money remains freely available, and also determine your reserves. Maintaining a family budget takes up to 3-5 minutes a day to fill out a table or fields in the application, if everything is automated. If you do the calculations manually, it will take more time.

Is it possible to keep a family budget in a notebook?

Yes, you can. But all calculations and calculations will have to be done manually, and this is a more tedious and routine task than when using Google spreadsheets with formulas or mobile applications with built-in functions. Over time, manual recording may become boring and the process will be abandoned. But if this option suits you, choose it.

How to properly distribute the family budget?

The ability to distribute the family budget comes with practice. At the first stages, all expense items seem important. But after detailed analysis and scrupulous accounting, the realization comes that not all costs are equally important. When you figure out the categories on which you can save or which can be eliminated altogether, then the question of distributing the family budget will no longer arise.

How long does it take to maintain a family budget for it to be effective?

It is advisable to maintain a family budget constantly. But if the indicators change slightly from month to month, and all expenses are optimized, you can stop keeping detailed records and only enter the final data. If you notice that the balance is gradually being upset, expenses are increasing or income is falling, return to the practice of detailing your expenses.

about the author

Klavdiya Treskova - higher education with qualification “Economist”, with specializations “Economics and Management” and “Computer Technologies” at PSU. She worked in a bank in positions from operator to acting. Head of the Department for servicing private and corporate clients. Every year she successfully passed certifications, education and training in banking services. Total work experience in the bank is more than 15 years. [email protected]

Is this article useful? Not really

Help us find out how much this article helped you. If something is missing or the information is not accurate, please report it below in the comments or write to us by email

Saving on food

Saving on food does not mean that you need to buy goods on sale and eat only cheap products. This indicates the need to reconsider your diet and stop using low-quality products. People are turning to cheaper and lower quality products and fast food when cutting their budget. And the body suffers from this, which leads to diseases. Ultimately, these savings translate into treatment costs.

People who think about their finances choose proper nutrition. They do not skimp on products, realizing that their health and well-being of life depend on it. They approach their purchases wisely and are not fooled by hyped products, choosing the golden mean.

- To properly save your family budget, make a meal plan for the week. This will eliminate spontaneous purchases and solve the question “What to cook?” It will also save the budget from spoiled products that are thrown away during chaotic purchasing of goods.

- Shop once a week with a list. And take the quantity indicated. After all, the menu has already been compiled with calculation in mind. This means there is no need to take extra. It is clear that bread, milk, cottage cheese, herbs and vegetables are not bought in large quantities - they are perishable. It is better to take them once every 2 days and fresh. And products such as cereals, flour, sugar, spices, and meat should be purchased in wholesale stores. They do not spoil and last longer. And they come with discounts and are cheaper than in regular stores. In the summer, you can generally shop at the grandmothers' bazaar, it will be cheaper and tastier.

- Looking at your shopping list, roughly calculate the amount needed for purchases and when leaving home, take it and no more. This will help you avoid getting caught up in promotions and taking something unnecessary off the shelf.

- Do not visit stores on payday. You have a huge amount in your hands that you want to spend all of, and at this moment it is difficult to control yourself, as there is no real assessment of your financial situation. Postpone your purchases to the next day.

- It is better to go to the store on a full stomach. When there is a feeling of hunger, purchases are made involuntarily. And when a person is full, his needs are reduced.

What expenses does the family budget consist of?- Scientists have proven that men find it easier to go shopping with a list than women. They are less impulsive, so they save the family budget better. Feel free to ask your man to go grocery shopping or take him with you always.

- Try to buy fresh foods rather than processed foods. It's profitable and useful.

- If you visit markets, get into the habit of bargaining. Often, this technique can work. And count the money “without leaving the cash register”; sellers may “make a mistake” with the change. And in the evening there are sales of leftovers at the markets, which is also a kind of savings.

- It is most convenient to freeze seasonal vegetables - fruits that were purchased cheaply or collected from your own garden, than to buy them at exorbitant prices during the off-season. It would also be good to can or make preparations.

- Buy store discount cards. This will help you save up to 30% on your purchases.

- If possible, carry food with you to work. Don't go to cafes for business lunches. It would seem that one lunch costs 300-400 rubles, but per month this amount is 6,600, and per year it is generally 79,200 rubles. It’s better to buy 1000 rubles worth of food for a week for lunches with you, and use the rest of the money to look for a tour abroad. Plus you will have a balanced diet. The body will thank you.

Comments: 2

Your comment (question) If you have questions about this article, you can tell us. Our team consists of only experienced experts and specialists with specialized education. We will try to help you in this topic:

Author of the article: Klavdiya Treskova

Consultant, author Popovich Anna

Financial author Olga Pikhotskaya

- Alexei

03/18/2021 at 02:03 Useful information, thank you.

Reply ↓ Anonymous

05/21/2021 at 03:02Thank you, Alexey)))

Reply ↓