Today it is difficult to find a person who denies the importance of saving money. However, Russian citizens do not even try to save rubles: the experience of past crises and the accompanying rapid inflation of the domestic currency have shown that they can only save their savings by converting them into foreign currency. But if you have a relatively large amount, the question arises - where to store dollars to protect them from theft, damage and depreciation? There are several good ways, each of which has its own advantages and disadvantages.

How to store dollars in your home?

The level of trust in the banking system and the state in general among Russian people remains extremely low. Therefore, many citizens, especially those who have reached retirement age, try to keep their savings at home.

At the same time, the apartment remains vulnerable: you can prevent a thief from entering with the help of a security alarm, but protecting yourself from selfish acquaintances or relatives who want to take over money is almost impossible. The only way left is to figure out how to store dollars at home away from prying eyes. Fortunately, relatively reliable options exist:

- You can remove the cover from a regular socket. Below it is a distribution box that holds a dozen rolled up bills;

- You can remove part of the edging from the table. Several deep holes are drilled at the end of the tabletop, the jumpers between which are removed with a knife;

- You can attach an additional pipe in the bathroom or bathroom that looks similar to water pipes. Its ends should be closed with plugs to protect it from moisture;

- You can hide money behind ceiling or wall plastic panels. You need to remove the last one and then carefully put it in place.

Before choosing a place for a hiding place, you need to find out how to store dollars so that they do not spoil. Banknotes are made from linen and cotton fibers, which are suitable for various mold fungi. In a cold, damp room without ventilation, these crops actively develop, rendering money unusable in two to three months. But if you solve this problem, you can enjoy all the benefits of home storage:

- Funds are always at hand. You need to order a payment of more than $200–500 from the bank in advance, since there may not be cash in the cash register;

- The reliability of the method is quite high, since you can store dollars at home without unnecessary worry about the bankruptcy of the bank or the revocation of its license;

- If you are careful, scammers, bailiffs or tax inspectors will not get to your savings. A bank account can be easily seized.

At the same time, storing money at home is characterized by some disadvantages that can cause a lot of trouble for the investor. In particular:

- Capital is not protected from inflation. The currency depreciates much more slowly than the ruble, but no investor wants to lose their money out of the blue;

- As experience shows, it is impossible to keep cash dollars without additional protection of savings from theft, fires, floods and other force majeure;

- The issuer's financial policy may change. For example, in the EU the 500 euro note is already being withdrawn from circulation, and the Federal Reserve is thinking about banning the 100 dollar note.

How to store dollars on a bank card

As you can see, keeping currency at home in cash is practical, but quite risky.

Therefore, more cautious investors prefer to store money in more secure places, the most accessible of which is a bank card. However, this method must be used with extreme caution. The fact is that modern fraudsters no longer waste time on stealing a card - psychological and phishing technologies for obtaining confidential data are much more common. If you don’t know how to spend money correctly, you can carelessly give them access to your personal account and immediately lose all your savings. Therefore, it is wiser to store relatively small amounts on the card that will be invested or spent in the next couple of months.

There are quite a few advantages of placing capital on a bank card. For example, an investor may find the following features useful:

- To conduct transactions with funds, you do not need to visit the bank. You can buy something or make an investment in real estate in the mobile application;

- Like other bank deposits, savings on the card are insured in the event of bankruptcy or revocation of the organization’s license up to 1.4 million rubles;

- It's easier to hide a card than a thick wad of bills. If you also prohibit payments using it on the Internet, then even if it is lost, the money will remain safe;

- Of course, using a bank card to store money is quite convenient.

But we must not forget about the risks that an investor may face:

- Savings on the card are not protected from the state. By decision of the court or the tax inspectorate, any amount may be written off from her or the account may be blocked altogether;

- Capital does not work and does not bring profit. Although dollar inflation is much lower compared to the ruble, even 2% per year can lead to losses;

- Working with a card requires compliance with the strictest security measures. Fraudsters have come up with many ways to steal data and gain access to your account.

Any bank in Russia is ready to open a currency card today. Therefore, you first need to find out where it is more profitable to store money in dollars. Here are some options:

Currency bank cards

| Bank | Bonus on balance, % | Maintenance, $/year | Cashback, % |

| Solidarity | 1,5 | 0–375 | 1,5 |

| Neiva | 1,5 | 0–348 | 0,0 |

| BBR Bank | 1,2 | 0 | 1,0 |

| SBI Bank | 1,0 | 5–58 | 0,0 |

| LokoBank | 0,75 | 0–120 | 1,0 |

Is it worth buying currency now or can you wait?

Expert opinion

Sergei Litvinchik

Author of the article. Expert, entrepreneur since 2014.

Ask a Question

Why is $ experiencing the worst times in the last decade - what are the reasons and how long will it last? Let's try to figure it out.

In July of this year, the DXY index, which reflects the performance of the US currency against six other major currencies, lost 4.2%. By mid-October, the dollar had not recovered. Since the announcement of the first US economic relief package in late March, the index has fallen 5.4%. In total since the beginning of the year - by 3%, even despite the short-term rally in March-April, when investors fled to the dollar on news of the pandemic.

How to store dollars in a bank account?

When choosing whether to keep dollars at home or in a bank, many citizens are guided primarily by the opportunity to gain free access to money. On the other hand, none of the methods described above generates income, which contradicts the very essence of saving for the sake of improving one’s well-being. But there is a way that allows you to simultaneously earn money and manage capital as you wish: storing money in a foreign currency savings account.

This account combines the advantages of a deposit and a bank card: the user can place funds for a long period of time, transfer part of the money to his card if necessary, replenish savings and protect them from inflation. At the same time, fairly high interest is regularly accrued on the balance, and the capital itself is insured against bank bankruptcy up to 1.4 million rubles.

It is advisable to use a savings account to store a fairly large amount that may be needed at any time. Why is this convenient:

- Savings remain available around the clock. There are no restrictions on the number of transactions with them during the month;

- Interest on the account is accrued monthly. If the client withdraws part of the capital, the bank will pay him a reward in accordance with the actual balance;

- Fraudsters are denied access to money. Even if the user loses his card or phone, nothing will happen - they are not directly linked to the account.

The convenience of storing money in a savings account is obvious. As for the risks and disadvantages, they are as follows:

- By decision of the court or the tax service, a citizen may lose part of his money or all of his capital. It is impossible to protect funds from federal authorities;

- Interest is calculated if there is a fairly large minimum balance. This makes us wonder what is the best way for the common man to store his dollars;

- The Bank has the right to change the conditions for placing funds at its discretion. There is no guarantee that they will be as profitable in six months.

In general, financial institutions are quite reluctant to work with savings accounts, so in Russia there are not many options where you can store dollars:

Currency bank accounts

| Bank | Bid, % | Amount, $ | Duration, days |

| ChelIndBank | 1,1 | 450000 | 366 |

| Garant-Invest | 2,0 | 370000 | 250 |

| Rossita-Bank | 1,4 | 200000 | 180 |

| Rosbusinessbank | 1,0 | 100000 | 500 |

| Tatsotsbank | 1,25 | 100000 | 360 |

How to store dollars in a safe deposit box

Many conservative investors are not ready to entrust their savings to a bank, but they also consider the decision to hide large sums of money at home short-sighted. Is it possible to store money in dollars in the form of cash, while using a reliable system of protection for financial institutions? Of course, if you rent a safe deposit box.

The locker is a personal safe located behind a steel door in a secure vault. You can hide not only stacks of bills in it, but also jewelry, documents, gold coins, and a collection of postcards. Of course, banks prohibit storing weapons, poisons, radioactive and narcotic substances here.

You can rent a cell for any period within the limits established by the institution. If the agreement does not provide for automatic extension, the bank notifies the user a week before the expiration of the term by letter, email or SMS. After 30 days, the contents of the safe are confiscated and placed in a general storage facility, from where it can only be retrieved after the debt has been repaid. Thus, if used correctly, a safe deposit box can become a reliable way to store cash. Besides:

- The contents of the box remain the property of the client. Even if the bank goes bankrupt and closes, all the money to the last penny will be returned to the owner;

- Bank specialists know how to store dollars correctly. The safe is constantly maintained at optimal temperature and humidity, and the air is filtered;

- Information about the presence of the cell and its contents is a secret. If the user does not tell about it himself, no one will be able to obtain such information from the bank.

Thus, a safe deposit box appears to be a very convenient way to store cash. However, there are also disadvantages here:

- Renting a cell requires constant monitoring. You need to renew the storage agreement on time, check its contents, and take care of your copy of the key;

- In cases specified by law, the bank can still open the cell. There are known cases of confiscation of valuables by order of the court or prosecutor's office;

- Placing capital in a cell not only does not generate income, but is also accompanied by losses. The rental cost is low, but for a year it turns out to be a decent amount.

As a rule, in small regional branches there is no storage facility with lockers, so the depositor will have to contact the central office. On the other hand, now every bank offers a personal safe rental service. Where to store dollars in Russia:

Bank cells

| Bank | Price per day, rub. | Cell height, cm | Duration, days |

| VTB 24 | 30–40 | 10–30 | 1–365 |

| Sberbank | 35–75 | 5–40 | 1–1096 |

| Alfa Bank | 25–75 | 5–40 | 1–1096 |

| ICD | 28–50 | 10–25 | 1–365 |

| Rosselkhozbank | 30–60 | 6–24 | 1–365 |

How to store dollars in a foreign currency deposit?

Studying the offers of banks, you will notice that for the right to freely dispose of savings, they significantly reduce interest rates or increase the amount of the minimum balance on the account. If an investor does not intend to spend funds for several months or even years, it is more profitable for him to place them on a foreign currency deposit.

Of course, rates on deposits in foreign currency do not look as impressive as in rubles, but this inconvenience is fully compensated by the lack of inflation characteristic of the domestic monetary unit. The answer to the question of what to store money in, euros or dollars, is also obvious: due to the lack of profitable investment objects, Russian banks offer a maximum of 0.01–0.05% per annum in European currency, while in American currency it is quite possible to earn 1.8–2 .2%. What to do with income:

1. The bank can add interest to the amount of the main deposit. In case of capitalization, payments will increase every month;

2. The bank can withdraw interest to a separate account or plastic card. The money will be available to the user, but payments will remain fixed;

3. A deposit can become a convenient tool for a cautious investor: firstly, the deposit will be insured for 1.4 million rubles, and secondly, attackers will not get their hands on the money under any circumstances. Besides:

- Foreign currency deposits effectively protect capital from ruble inflation. The dollar depreciates by about 1.5% per year, which is compensated by the deposit rate;

- Additional income comes from currency fluctuations. If you choose how to save money from inflation in 2021 during a crisis, you cannot find a more reliable way;

- The investor knows exactly when and how much he will receive. Profit will not change even if the discount rate is reduced, since all conditions are fixed in the contract.

Obviously, it is better to store dollars or euros on a deposit than in cash or on a bank card. However, this method also has disadvantages:

- After the Federal Reserve lowered the discount rate, placing deposits in foreign currency became unprofitable for Russian banks. Many of them began to refuse this service;

- The Duma is discussing a law introducing zero rates on foreign currency deposits. If adopted, the question of how to store dollars in a bank will become irrelevant;

- In the event of bank bankruptcy, the client will receive compensation in rubles at the exchange rate. It is not a fact that the quotes at this moment will be at least equal to the original ones.

Today on the Russian market, 28 commercial banks offer to open a deposit in foreign currency with a rate above 1.5% per annum. Where is the best place to store dollars?

Currency deposit accounts

| Bank | Bid, % | Amount, $ | Duration, days |

| NK Bank | 2,2 | 1000 | 181–735 |

| Transstroybank | 2,1 | 50000 | 91–540 |

| BBR Bank | 2,0 | 50000 | 91–730 |

| Bank Kremlevsky | 2,0 | 1000 | 91–367 |

| Centrocredit | 2,0 | 5000 | 31–370 |

Currency distribution

Most often, questions about storing money are asked by people who want to preserve capital in the long term. And most experts say that in this case, storing money in foreign currency should be carried out in parallel with investing in rubles. That is, choose several investment options at once.

Approximate spread of the savings basket:

- 50% - in dollars. It is recommended to keep most of your savings in American dollars, because today it is the most stable currency. Central Banks of various countries store capital in it because of stability and low inflation;

- 25% - in euros. Also a stable currency. But in light of the exit of some countries from the European Union and various unrest in it, everything may change. So far, the exchange rate is stable, but it is still better to allocate a small part of your savings to the euro;

- 25% - in rubles. If income comes in rubles, and spending is also done in this currency, it makes sense to leave a quarter of the currency basket in rubles. In addition, when storing in Russia, the rates on ruble deposits are the highest.

Most experts, based on the current situation with the near crisis, recommend holding a third in euros, a third in dollars, and a third in cash rubles.

The 50/25/25 ratio is ideal in a normal, stable world situation. But now, when the pandemic is raging, it is better to divide the basket into three equal parts. It is impossible to give a guaranteed forecast of what will happen to the global foreign exchange market next. If one depreciates, two others will remain, which will support capital.

How to store dollars in an electronic wallet?

With the advent of the World Wide Web, banks, due to their conservatism, were not bothered by the development of international payment systems that were convenient for ordinary users, and therefore electronic payment systems quickly occupied the free space on the market.

Electronic currencies are essentially no different from non-cash ones - you can use them to make payments, buy things on the Internet, exchange them for regular money and withdraw them to a card. They are stored in virtual wallets, which are analogues of familiar bank accounts opened on EPS websites. To top up your wallet, you can:

- Buy a prepaid card for a fixed amount;

- Send money by transfer from a mobile phone;

- Deposit the required amount through an ATM or terminal;

- Make a payment from a bank card through a mobile application;

- Make a bank transfer to the appropriate details.

Of course, the activities of payment systems are not regulated by the state as strictly as the real banking sector, however, for placing small amounts in the range of 5-10 thousand dollars, electronic wallets are extremely convenient. In particular:

- You can access your wallet and perform the necessary operation anywhere in the world where there is Internet;

- Replenishing your account and withdrawing money takes literally a few minutes. By linking a bank card to your account, you can perform these actions right from home;

- Payment systems do not require money for account maintenance. The commission is charged only for the transfer, and its amount is comparable to the tariffs of banks.

Storing money in an electronic wallet is a relatively new method, and therefore investors have a certain distrust of it. Why this is justified:

- The client will have to undergo identification, since storing rubles in dollars without proof of identity is inconvenient: all transactions with money are severely limited;

- The wallet is linked to a mobile phone. If the fraudster gains access to it, he will be able to dispose of the funds at his own discretion;

- There is no legislative mechanism for protecting electronic savings in Russia. If the system goes bankrupt, it will be difficult to get money.

There are dozens of payment systems operating in Russia, but it is wise to trust your money only to the largest of them. Where is it more profitable to store euros or dollars:

Electronic wallets

| Name | Max. invoice, rub. | Max. operation, rub. | Commission, % |

| WebMoney | 2000000 | 15000 | 0,8 |

| Qiwi | 600000 | 60000 | 2,0 |

| PayPal | 550000 | 100000 | 2,9 |

| Payeer | 2000000 | 100000 | 0,0 |

| PerfectMoney | 2000000 | 10000 | 0,5 |

Ways to save personal finances

To ensure that money is not wasted, but accumulated, several key conditions must be met:

- identify the main sources of spending;

- calculate how much you can save;

- set specific financial goals.

I have already clarified that successful people are more inclined to save, so the material on investment deposits contains recommendations on how to choose platforms and what to pay attention to. But in order to have funds for investment, you need to learn in detail about ways to save personal finances, taking into account constant spending or large-scale future purchases.

Current needs

Categories of expenses, including all regular expenses: buying groceries, paying for utilities, transport. Due to the fact that this happens regularly, it is not clear how much money is actually spent on such purchases.

In developed countries, a family spends no more than 30% of its total budget on food per month.

I recommend making a clear shopping plan, planning your expenses in advance, buying some products on promotions and for future use.

Airbag

This is an amount that can never be spent, but at the same time it can be replenished and increased. In one of my articles on GQ Blog Monitor, I talked about what capitalization of a deposit is. I recommend using the principle of adding interest to the amount to increase the cushion. The cushion of monetary security and stability should be formed from the national currency and from the international one. For many people, it is extremely important from a psychological point of view to understand that they have savings for urgent treatment or other happier occasions.

Short term goals

Short-term goals also require compliance with rules in storing money. Firstly, I always clarify that you need to plan your expenses in advance and understand what you can afford and in what period. Secondly, you cannot spend all the money that is in your wallet or card. Despite the fact that the goals, although not large-scale, are short-term, they are still costly and require the implementation of certain strategies and rules.

I consider it necessary to talk about where to store money if you decide to spend it today by visiting a market or store. You should only hold a wallet with cash and cards in your hands. And if you plan to make a large cash purchase, put it in your front pants pocket or breast pocket.

Long term goals

Long-term goals can be considered buying a car, real estate, or opening a business. In order to not just store money, but accumulate it towards a specific goal, I recommend making a specific plan and indicating:

- name of the goal;

- approximate date of implementation;

- the total amount to solve the problem;

- how much of the required amount is available now.

To solve this problem, you can invest money in gold by buying bars and storing them in bank deposit boxes.

How to store dollars in Eurobonds?

Trying to find more profitable ways to allocate capital, all investors sooner or later come to the conclusion about the advisability of buying bonds. These securities are issued only by government agencies and have undergone multiple audits by the largest commercial companies, so they can be called one of the most reliable and safe instruments for storing savings. There are bonds denominated in rubles, dollars, euros and in general any currency in the world, which allows you to choose the optimal type of asset for an investor with any capital.

For the placement of funds, the greatest interest is in Eurobonds or Eurobonds intended for trading on the largest international exchanges. Every Russian citizen who has entered into an agreement with any brokerage company can buy them. Of course, the choice will be limited to assets that, according to the legislation of the Russian Federation, are securities and are traded on domestic exchanges, but even in this case, the investor will be able to find hundreds of suitable options.

Why is it profitable to buy bonds? The income it brings will consist of two parts - the coupon payment itself and the increase in the value of the asset itself, associated with the fall in the ruble exchange rate. It should also be noted that:

- Issuers repay debts on bonds regardless of the availability of profits. There is no more reliable way to increase capital without risk;

- The turnover of Eurobonds is regulated by international laws, so the return of money in the event of a company default is guaranteed. However, there have been no such precedents;

- Bond yields are known in advance. Unlike other instruments, it will not change when the refinancing rate decreases or increases.

Many experienced investors prefer placing money in Eurobonds over any other storage methods. However, there are some inconveniences here too:

- Only a qualified investor can buy assets that are not listed on Russian exchanges. A beginner has few options on how to store dollars;

- Income on bonds is subject to personal income tax, and translated into national currency. If the ruble exchange rate falls sharply, the coupon payment may not cover the tax amount;

- Most brokers set the minimum amount for investing in bonds at $10,000 to $30,000. There is nothing to do with a modest capital on the stock exchange.

More than three hundred types of Eurobonds are currently available on the Moscow and St. Petersburg stock exchanges. Where is it profitable to store dollars:

Eurobonds

| Name | Income, % per year | Price, $ | Redemption |

| Gazprom-05-2034-euro | 3,66 | 1549 | 28.04.2034 |

| Gazprom-18-2037-euro | 3,66 | 1465 | 16.08.2037 |

| GTLK-001R-05-bob | 3,25 | 802 | 21.08.2024 |

| VEB.RF-3-2025-eur | 2,97 | 1182 | 22.11.2025 |

| Russia-2028-7t | 2,61 | 1734 | 24.06.2028 |

How to store dollars in dividend stocks?

If you have some experience of trading on the stock exchange along with bonds, it is advisable for an investor to supplement his portfolio with a certain number of dollar-denominated shares along with Eurobonds. The income it brings will also consist of two parts - the increase in the value of the asset itself and the dividends due to its owner.

You should choose assets for purchase carefully: some second- or even third-tier companies sometimes try to improve their dubious financial situation with the promise of large payments. The following questions can serve as a guide:

- Does the company generate stable profits? If it has development prospects, it is worth buying more shares. If the market falls completely, it is reasonable to transfer part of the money into cash and hide it in a safe deposit box;

- Are dividends paid regularly? Some companies make good payments, but arrange arbitrary breaks of two or three years between them. Therefore, the investor has to constantly monitor the dividend calendar;

- Is it wise to hold on to a company's assets if the market situation worsens? A positive answer means that management is pursuing sound policies and has the resources to overcome the crisis.

Since active trading seems like a risky way to store capital, dividend stocks may be of greatest interest to a beginner. As practice shows, such investments have a number of advantages:

- Investing in such assets does not require serious preparation. Even a beginner will figure out how to store savings in dollars by investing them in dividend stocks;

- Typically, the most attractive securities are blue chips. You can sell them and withdraw money to your bank account in literally an hour;

- Shares are usually inexpensive. Even with a small capital, you can create a good portfolio with an optimal combination of risk and return.

Buying dividend shares can be a real way for an ordinary person to get rich in Russia. But do not forget that investing in securities is accompanied by certain risks:

- The decision to accrue dividends is made by the company's management. If last year was unsuccessful and did not bring profit, there may be no payments;

- After negative events, shares may fall in price so much that dividend payments do not compensate for the loss in value. For the investor this means losses;

- Brokers are reluctant to work with newcomers with small capital. If we are talking about an amount of a couple of thousand dollars, you can forget about this method.

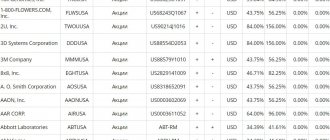

Is it profitable to keep money in dollars when buying dividend stocks? Studying reports and releases for 2021, we can identify several leaders in the global market:

Dividend shares

| Name | Dividend, % per year | Company income, $ | Price, $ |

| AbbVie | 5,5 | 32.75 billion | 92,26 |

| Archer Daniels Midland | 4,4 | 64.34 billion | 38,60 |

| Walgreens Boots Alliance | 4,1 | 136.92 billion | 40,75 |

| Sysco | 3,6 | 55.37 billion | 53,37 |

| General Dynamics | 3,5 | 36..19 billion | 148,55 |

How to store dollars in Eurobond mutual funds?

Investing in Eurobonds is no more difficult than opening a deposit. However, such securities are expensive, so a beginner with a small capital will not be able to form a more or less balanced portfolio. In such a case, it is worth paying attention to Eurobond mutual funds, where the entry threshold most often does not exceed 1,000 rubles.

The purpose of the funds is to profitably invest the consolidated contributions of hundreds and thousands of investors, which allows them to buy any assets. Investments are made by professional managers with extensive experience in economics and stock trading. At the end of the specified period, profits are distributed among investors in proportion to their contributions.

Almost all large funds were created by large financial organizations, including Sberbank, VTB, AFK Sistema and others. As a rule, they were not opened from scratch, but on the basis of previously existing mutual funds of ruble bonds, which confirms their high qualifications and reliability. Why is it worth keeping money in funds:

- Thanks to the low entry threshold, mutual funds can become a profitable investment in 2021 for beginners;

- A mutual fund invests in hundreds of different bonds. To achieve this level of diversification, the average investor would have to spend hundreds of thousands of dollars;

- In addition to payments on bonds, the fund’s profit is also generated by changes in exchange rates. Moreover, the mutual fund can trade both downward and upward.

Investing in mutual funds is extremely convenient for a beginner who does not have the skills and experience of working on the stock exchange. At the same time, there are also some disadvantages here:

- Even the experience of managers does not guarantee the profitability of a mutual fund. No one can say in advance whether it is profitable to store money in dollars here;

- The investment policy of the funds is regulated by the state. Therefore, they often cannot afford to risk capital for a solid profit;

- The commission for capital management does not depend on the presence or absence of profit. The fund receives its fee even in the event of unprofitable activities.

It remains to be seen where it is better to store money in dollars: 2021 showed that the funds of the largest management companies achieved high efficiency. This:

Eurobond mutual funds

| Name | Income, % per year | Share price, rub. | Commission, % |

| Opening | 5,23 | 1000 | 1,5 |

| VTB | 6,03 | 1000 | 1,1 |

| Uralsib | 5,39 | 1000 | 1,5 |

| System Capital | 8,40 | 100 | 0,75 |

| Sberbank | 5,13 | 1000 | 1,5 |

Advantages and disadvantages

Investing in currencies of different countries has its pros and cons. Its advantages include:

- accessibility, since all bank clients can safely invest in dollars, euros, yen and other currencies;

- benefit, because many currencies are constantly rising in price, and an investor can make good money on exchange rate differences;

- liquidity, because any currency can be sold within a few minutes or hours, if necessary.

However, the disadvantages of buying foreign currency are:

- sudden price changes that are difficult to predict even for experienced experts;

- lack of stable income;

- dependence of asset liquidity on government policy.

How to store dollars in a foreign bank?

History demonstrates that in the event of a shock on a national scale, not a single domestic financial organization will avoid dire consequences. If the crisis forces the government to resort to extreme measures, dollar savings owners will likely face the following phenomena:

- Foreign currency deposits can be forcibly converted into a national currency, and at the most unfavorable rate for the investor;

- The government may significantly limit transactions with foreign currency or even prohibit the circulation of dollars for individuals in Russia;

- Fiscal authorities can charge personal income tax on profits in rubles, which are generated due to the depreciation of the national currency. In fact, this means losses.

Therefore, any far-sighted investor sooner or later thinks about how best to store money in dollars in foreign accounts. Every citizen of the Russian Federation can become a user of a foreign bank, but some features must be taken into account.

First of all, you will have to make at least one trip abroad: no serious bank will open an account via the Internet. In addition, European organizations do not really like foreign clients, and therefore set a minimum balance for them in the range of 50–100 thousand euros or dollars. Finally, most banks set deposit rates in the range of 0.01–0.05% per annum, although euro inflation reaches 1.6% annually. However, it is possible to find acceptable service conditions - for example, in the Baltic states. What investors will surely like:

- The European banking system is much more stable than the Russian one. The danger of introducing any extraordinary measures or bankruptcies is much less here;

- An attractive deposit insurance system can show whether it is worth keeping money in dollars abroad. The limit in the eurozone is equivalent to 100,000 euros;

- Foreign financial institutions share data with Russian services only upon request. If you don’t show off your wealth, no one will know about your contribution.

At the same time, this method can hardly be called accessible: in order to conclude an agreement with a foreign bank, you will have to overcome many obstacles. Besides:

- According to the law, it is still necessary to notify the fiscal authorities about a foreign account, although such an extract may be of a formal nature;

- It is often unrealistic for a beginner to keep savings in dollars or euros abroad, since banks require an account balance of at least 50 thousand euros;

- Many European banks do not have a full-fledged web interface, which means that you will have to manage your savings in less than convenient ways.

There are thousands of banks in Europe, so it will take a long time to select the conditions for placing deposits. As an example, we can cite the proposals of Baltic banks:

Deposit accounts abroad

| Bank | Bid, % | Amount, $ | Duration, days |

| Reģionālā investīciju banka | 0,8–1,80 | 500 | 90–1825 |

| Reģionālā investīciju banka | 0,7–1,60 | 500 | 90–1825 |

| Rietumu Banka | 0,8–1,75 | 5000 | 90–1825 |

| LPB Bank | 0,1–1,40 | 5000 | 90–1095 |

| Rietumu Banka | 0,7–1,65 | 5000 | 90–1825 |

Tips for buying currencies during a crisis

According to experts, the average duration of economic crises is 17 months. Those. a person who invests in currency today should be prepared to play the long game.

IMPORTANT!

During a crisis, you need to prepare for yourself some kind of reserve fund, consisting of several currencies.

When forming a currency basket, it is worth choosing currencies of countries located on different continents. In the event of any global troubles, this will help to survive the crisis with minimal losses. After all, it can’t be equally bad in the USA, Australia, China, and Europe!

But such diversification is done more for one’s own peace of mind. During a crisis and economic uncertainty, no expert can say which currency will soar. Also during a crisis, you should use the following tips:

- There is no need to save currency “under the mattress”. Even the dollar or euro can become worthless due to inflation if something extraordinary happens.

- You should not buy a currency at the peak of its value immediately after a sharp jump. As practice shows, after a sharp jump, the currency often becomes cheaper, although it does not return to its “pre-crisis” level.

- You should invest only in well-known and reliable currencies. The dollar and euro will always be in demand, since America and the European Union have a good scientific and technical base and resources, which explains the popularity of these currencies. Honduras cannot boast of this.

Anyone can buy currency and save money with it. Today, this is the most effective way to outwit inflation and make a little money on exchange rate differences for all those who do not have proper experience in investing. You just need to choose the right currency, taking into account the state of the world economy and the political situation on the planet.