Interest on deposits cannot cover losses from inflation. The only reliable way to save money is to invest it, including in securities. But such investing is not passive income and requires knowledge of the features and terminology of the financial market. Otherwise, the invested money can be lost.

Let's consider such a concept as a bond offer and its use to generate additional income associated with investments in this type of securities.

What is a bond offer and how does it work?

So, what kind of beast is this offer? In simple terms, this is a public offer from the issuer of a bond to investors, when they have the right to redeem their bond at par without waiting for its expiration date.

For example, there is a Gazprombank bond GPB-16-bob with a maturity date of 04/18/2024, issued on 04/18/2017, i.e. 7-year bond. However, the bank issued an offer on it on October 20, 2020. This means that on the offer date the investor can sell the bond back to the bank at par. Or he can keep it for himself and continue to receive coupon income under the conditions prescribed by the issuer.

It is important to understand that upon an offer, the bond is repaid at par, i.e. it is acquired back by the issuer. If the face value of the paper is 1000 rubles, then you will receive 1000 rubles, regardless of the market price of the bond.

Therefore, investors often use the offer date to get their money back. Especially if the market price of the bond was below par.

Typically, most long-term bonds have a put option. The presence of an offer allows issuers to get rid of their debt earlier and not incur additional costs for servicing the debt, and investors - to get their money back if the market situation has changed.

Imagine the situation. You bought a 10-year bond with a yield of 8% per year. But then interest rates changed - the Central Bank of the Russian Federation increased the rate to 10%. Now issuers issue bonds with a yield of 12-14% per annum, and no one needs your 8% anymore. The market price of the bond falls to compensate for the difference in rates and provide a higher yield. You bought a bond, for example, for 998 rubles, and now it is trading for 980 rubles. And if you decide to sell it (since the coupon is small, but you want a higher yield), you will lose profit - 18 rubles from each bond.

But the issuer announced an offer that is due in a year. And you calmly hold the bonds until this period and then transfer them to the issuer, who repays them at par (1000 rubles each). And with the proceeds you buy other, more profitable bonds.

Comfortable? Not that word!

The offer date is announced in advance. Therefore, investors always know when they will have the opportunity to get rid of an asset that has become unprofitable.

Coupon yield

As the accumulated coupon yield (ACY) increases, the value of the bond increases.

After the coupon is paid, the cost is reduced by the amount of the NKD. NKD

— accumulated coupon income

C

(coupon) — amount of coupon payments for the year, in rubles

t

(time) — number of days from the beginning of the coupon period

Example:

the investor bought a bond with a par value of 1000 rubles with a semi-annual coupon rate of 8% per year, which means a payment of 80 rubles per year, the transaction took place on the 90th day of the coupon period. His additional payment to the previous owner: NKD = 80 * 90 / 365 = 19.7 ₽

Dangers of the offer

But the offer has one drawback. Thus, the issuer has the right, after issuing an offer, to change the coupon rate to any value other than zero. Even 0.01% per annum.

And here’s another interesting article: The most profitable Russian bonds with a monthly coupon in 2021

Many issuers, by the way, do just that. Here, for example, is the bond Bank FC-Otkritie-10-1-bob. Before 06/06/2018, the yield was 11.75% per annum, but after the offer it dropped to 0.01%.

Thus, if an investor misses the offer date and does not present the bond for redemption, then instead of the planned double-digit return, he will receive a profit of 4 kopecks per year. Agree, this is no longer very pleasant.

Besides, there is one more point here. Take a look at the chart.

This is still the same bond Bank FC Otkritie-10-1-bob. As you can see, immediately after the announcement of the offer and the redemption of a certain volume of bonds from the market, the value of the remaining ones fell. Now this paper is trading at 80% of its value.

Why did it happen? Very simple. Since the coupon on the bond is practically not paid (0.01% - seriously?), the paper becomes unattractive in terms of receiving regular income. Therefore, buyers offer less for it in order to earn money when the bond is redeemed due to the difference between the purchase and redemption.

For example, after the offer there are still 5 years left until maturity. The refinancing rate of the Central Bank of the Russian Federation, which is used as a guideline when determining bond yields, is 7.75%. So the price of the bond will fall by about 5 * 7.75 = 38.75 percent. If there was only one year left until maturity, prices would fall by 7-8%. If 10 years, then generally by 77-80%.

Thus, the longer the period from the offer date to the maturity date, the more the bond falls in price.

Therefore, you have to monitor the offer and take the right actions.

What it is?

An offer is a proposal to conclude a transaction for a limited or unlimited number of persons. At the same time, it stipulates the essential conditions that the recipient must agree to. If these conditions are met, the deal is considered concluded.

For the debt securities market, this concept means the early repurchase of bonds (redemption) at a predetermined price.

Bonds have two types of offers:

- call option;

- put option.

Let's take a closer look at each of them.

Types of offers

There are the following types of bond offer:

- irrevocable, or an offer with a put option - the investor himself decides whether to present his existing bonds for redemption or to keep them for himself;

- revocable, also known as an offer with a call option - the issuer has the right to repay his own bonds without asking investors about it and without obtaining their consent (note - he has the right, but may not repay).

The Russian market mainly presents irrevocable offers, also known as put offers. They are more convenient for the investor, as they help him, in case of a sharp change in the market situation, get rid of an unnecessary asset and buy something more profitable.

If a call offer is announced and the issuer forcibly buys back the bonds, then nothing can be done about it. Investors don't decide anything here.

Let's look at each type of offer in more detail, since you will have to deal with each of them in your practice.

Example

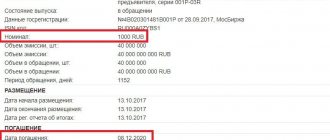

Let's consider an irrevocable offer using a specific example of the PIK BO-4 bond.

Repayment is planned in 2025. The offer is scheduled for August 17, 2021. The purchase will take place at the starting price. The yield on the offer is 9.01%.

The most detailed information on securities is provided by the website www.rusbonds.ru. You can search for bonds both by name and by ISIN code - it is unique for each security.

Here are lists of coupons and payment terms for them. You can find a lot more useful information on this site.

Features of the call offer

So, a call offer gives the issuer the right to fully or partially repay the issue of its bonds unilaterally. This is, of course, very convenient for the issuer. With the help of a call offer, he can regulate the level of his credit load.

So, if interest rates decrease, then it is profitable for him to pay off his issue so as not to overpay. For example, the key rate was 14%, but dropped to 8%. It is more profitable to repay the existing issue and issue new bonds at a rate of 9%.

If rates go up, the issuer will simply not submit an offer and will pay less on the bonds than the market average. Mirror example. The key rate was 8%, and the issuer paid 9%. Then the rate rose sharply to 14%. The issuer does nothing with the old issue, since it is beneficial for him to pay less.

And here’s another interesting article: OFZ-n third issue: cost, commission and purchase features

True, this is no longer profitable for the investor. After all, he could have bought bonds with a higher yield, but instead he is forced to either continue to sit in unprofitable bonds or sell them on the market for less than he bought.

Because of this feature, call bonds are considered riskier and therefore tend to trade slightly below the hospital average, i.e. with a discount (they also say: they have a premium to profitability - for risk).

As for the risk of missing an offer, there is none, since a call offer is simply impossible to miss. The issuer will either buy the bond from you at par or leave everything as is.

How and where can you buy papers?

In Russia, the main platform for trading securities is the Moscow Exchange. Here the broker makes the purchase for the investor. He knows the market situation and can provide useful information that will help you wisely invest money in growth.

Additionally, there are several resources on the Internet that can be installed on smartphones, and then purchase bonds of not only domestic but also foreign borrowers. To carry out such operations, you need to have accounts in different types of currencies.

To work with electronic money, WebMoney, PalPay and other payment systems are used. With their help, you can exchange money between your own accounts, as well as sell and buy currency from participants in the electronic money market.

Applications that can be used to trade securities:

- Sberbank Investor - works with Federal Loan Bonds (OFZ).

- VTB My Investments – can work with OFZs, as well as European securities.

- My broker - books a place on the main financial exchanges. For an additional fee, you can connect an electronic assistant to it, which analyzes the state of the market and gives its recommendations. This application is beneficial when making large transactions.

- FinamTrade is a US development and sometimes brings very significant income. Use with caution, there may be unexplained malfunctions.

- Tinkoff Investments is a new developing project. Here the sale and purchase of stocks and bonds is carried out. Game on exchange rates. Investments in oil and gas contracts of the world's leading companies are possible.

- Yango is quite an interesting platform. Users who have mastered the menu and operating principles say that trading here can be quite profitable.

How does a put offer work?

Let me remind you that a put offer works like this: the issuer sets a date for repurchasing the bond, and investors can, if they wish, submit an application to redeem the bond at par. Redemption under a put offer is voluntary. If you don’t want it under the offer, hold it until maturity or sell it on the stock exchange.

Sometimes issuers assign a penny coupon after the offer - 0.1% or even 0.01% per annum. The goal is not to deceive investors, but to encourage them to pay off the bond as quickly as possible. This is voluntary-compulsory.

On the other hand, as I wrote above, a put offer can be beneficial for an investor if he urgently needs to transfer money to another instrument and the market price of the bond is low. This allows you to hedge against the risks of long-term bond ownership.

The offer date is always known in advance. Immediately before its announcement (more precisely, the announcement of the future coupon), the bond can either rise in price or fall in price - everything will depend on the intentions of the issuer. For example, if before this he consistently reduced the rates on previous issues of his bonds, then a reduction will most likely follow here. The market will react by falling in the value of the bond.

As a rule, the period for presenting bonds for redemption begins 5 days before the payment of the last coupon and ends on the third day after payment (or directly on the same day).

Wiki-Yango

An intelligible dictionary of terms and definitions of the bond market. A reference base for Russian investors, depositors and rentiers. Bond discount is a discount to the face value of the bond.

A bond whose price is below par is said to be selling at a discount. This occurs if the seller and buyer of the bond have agreed on a higher rate of return than the coupon set by the issuer. The coupon yield of bonds is the annual interest rate that the issuer pays for the use of borrowed funds raised from investors through the issue of securities. Coupon income is accrued daily and calculated at a rate based on the face value of the bond. The coupon rate can be constant, fixed or floating.

The coupon period of a bond is the period of time after which investors receive interest accrued on the face value of the security. The coupon period of most Russian bonds is a quarter or six months, less often a month or a year.

Bond premium is an increase to the face value of the bond. A bond whose price is higher than its face value is said to sell at a premium. This occurs if the seller and buyer of the bond have agreed on a lower rate of return than the coupon set by the issuer.

Simple yield to maturity/put - is calculated as the sum of the current yield from the coupon and the yield from the discount or premium to the face value of the bond, as a percentage per annum. Simple yield shows an investor the return on an investment without reinvesting coupons.

Simple yield to sale - calculated as the sum of the current yield from the coupon and the yield from the discount or premium to the sale price of the bond, as a percentage per annum. Since this yield depends on the price of the bond at sale, it can differ greatly from the yield to maturity.

Current coupon yield is calculated by dividing the annual cash flow from coupons by the market price of the bond. If you use the purchase price of the bond, the resulting figure will show the investor the annual return on his cash flow from coupons on the investment.

The total price of the bond is the sum of the market price of the bond as a percentage of the face value and the accumulated coupon income (ACI). This is the price an investor will pay when purchasing the paper. The investor compensates for the costs of paying the NKD at the end of the coupon period, when he receives the coupon in full.

The bond's net price is the market price of the bond as a percentage of the face value, excluding the accumulated coupon income. It is this price that the investor sees in the trading terminal; it is used to calculate the return received by the investor on the invested funds.

Effective yield to redemption/put - the average annual yield on the initial investment in bonds, taking into account all payments to the investor over different periods of time, redemption of the par value and income from reinvestment of coupons at the rate of the initial investment. To calculate profitability, the investment formula for the rate of internal return on cash flow is used.

Effective yield on sale is the average annual return on the initial investment in bonds, taking into account all payments to the investor over different periods of time, proceeds from the sale and income from the reinvestment of coupons at the rate of the initial investment. The effective yield on sale shows the return on investment in bonds for a certain period.

TOP ↑

How to present a bond for redemption under an offer

If you have a call bond, then you don’t need to do anything. The issuer itself will give a signal to the broker about the repurchase. If you are affected by a forced redemption, then instead of bonds, money will appear in your brokerage account. If it doesn’t affect it, the bonds will remain as they were. If the new conditions do not suit you, then you can sell it at the market price.

Please note that if you purchased a bond below par, then upon redemption under the offer, income taxes will be withdrawn. For example, you bought a bond for 990 rubles, and received 1000 for it. If there were one hundred bonds on your balance sheet, then you earned 1000 rubles. The broker will withhold personal income tax from this amount - 130 rubles.

And here’s another interesting article: Exchange-traded mutual funds of Gazprombank GPBS and GPBM: investments in corporate bonds

If you have a put bond, then it’s more complicated. Find out when the offer is and from what date the issuer accepts applications for redemption. Then, through a broker, submit an application to exercise your right. This service is free, but indicate that you are presenting a ransom under the offer. The fact is that some issuers provide the possibility of forced redemption of the bond at any time, but with a hellish commission.

Sample

The notification must be made in the following form:

“Hereby _____________________________________ (full name of the holder) announces his intention to sell interest-bearing non-convertible documentary bearer bonds “Gazpnf1Р6R” series 09 with mandatory centralized storage, state registration number 5-08-51265-Z dated April 15, 2012, in accordance with the terms of the Offeror’s irrevocable offer dated “__”___________201_.

Full name of the Holder:

Number of Bonds offered for sale

Stamp, signature"

The notification must be accompanied by a copy of the demand for fulfillment of obligations, as well as all documents confirming the transaction.

Where to view the offer

Ok, it’s clear what a bond offer is. Now the question is – where can I see the offer? Maybe it’s already on the bond you have, but you can’t sleep? Offers are made mainly for corporate bonds, as well as for a number of OFZs and Eurobonds. Municipal bonds usually do without an offer. but there is depreciation there.

There are several options here:

- go to the bond profile on the Moscow Exchange website;

- use a specialized service like Rusbonds or Cbonds;

- look at the bond prospectus on the issuer’s website;

- in the QUIK terminal.

In addition, you can determine whether there is an offer “by eye”. Just look at the duration. It is calculated based on the offer, not the maturity date, so it will be much shorter. For example, if the maturity date of a bond is several years, and the duration is about a year, then the paper is definitely with an offer. And you have to dig deeper to find it. It is imperative to look at the offer when choosing a bond to include in your portfolio.

Thus, an offer is an opportunity to repay a bond at par before its final maturity date. For an investor, an offer can be convenient if he needs to go to cash or he has found a better way to invest money, but sometimes it can become an unpleasant surprise. For example, if the issuer changes the coupon size after the offer, and the bond sharply loses in price. So you need to keep an eye on her. Now you know about it. Good luck, and may the money be with you!

Rate this article

[Total votes: 2 Average rating: 5]

Types of bonds on the Russian market

Expert - Ivan Ptashnik, leading financial advisor of BCS Premier*, Krasnodar.

The debt market is the oldest of the financial markets, which today is represented by a wide variety of instruments. The Russian bond market is no exception in this sense. It is easy for an inexperienced investor to get confused in the first couple of days in the variety of debt securities.

How does a variable bond coupon differ from a floating coupon? What yield should we focus on: current, at maturity or at the offer date? How are municipal bonds different from government bonds? What is junior debt and how to avoid the risk of subordinated bonds? What is debt amortization? We will answer these and other common questions in this article.

Classification of bonds by presentation currency.

According to the law, all payments on the territory of the Russian Federation are carried out in rubles. Accordingly, the vast majority of bonds traded on the domestic market and available to private investors are denominated in national currency. The nominal value of bonds is most often 1000 rubles, income is paid in the form of coupons and they are traded on the Moscow Exchange.

Bonds denominated in foreign currencies (mainly euros and US dollars) are called Eurobonds. The main trading volumes of Eurobonds take place on the over-the-counter market, but some securities are also available on the Moscow Exchange. When investing in such securities, it is necessary to take into account tax features. The calculation base for personal income tax for them is not only the main income, but also income from exchange rate differences, which can very significantly reduce the benefit from investments. The Ministry of Finance of the Russian Federation is currently developing a bill that will exempt investors in government Eurobonds issued after January 1, 2021 from personal income tax on income from exchange rate differences.

Classification of bonds by type of issuer.

Based on the type of issuer, bonds on the Russian market can be divided into three large categories: state, corporate and municipal.

Government bonds. The most common securities in this category are federal loan bonds (OFZ), which are described in detail in the article OFZ: How they differ and which ones to buy. OFZs have good liquidity, a wide range of investment terms, a low probability of issuer default, and the coupon income on them is exempt from personal income tax. Most often, the coupon is paid on these securities once every six months, but there are exceptions. Among the disadvantages, one can note the low profitability, which is compensation for the low credit risk.

Corporate bonds. This category of securities represents debt securities of large companies. They are distinguished by a higher yield than OFZs, and their coupon is often variable. Income, both coupon and increase in market value, is subject to income tax, but there are exceptions in the form of corporate securities issued after 2021 inclusive, for which coupon income is exempt from personal income tax. A list of such papers can be found in the following article.

It is necessary to separately note subordinated bonds of corporate issuers. A subordinated bond is a loan from a company that ranks below other loans and borrowings in the event of liquidation or bankruptcy of the company, the so-called junior debt. In other words, holders of subordinated bonds will be the last ones, other than shareholders, to receive their share of the company's assets in bankruptcy. Such securities are a riskier investment and, accordingly, are accompanied by higher returns. To calculate the risk of a portfolio, it is necessary to know for sure whether it contains debt securities of subordinated issues, the credit risk of which is higher. A private investor can find these bonds among bank debt securities, since for them this form of raising capital is convenient for a number of reasons. The list of subordinated bonds of Russian banks can be found here.

Subfederal and municipal bonds. These debt securities can be issued by constituent entities of the Russian Federation (subfederal) and municipal entities (municipal). The market for these bonds is small relative to other types of securities, which in turn affects liquidity. About half of the entire market is made up of issues from Moscow, the Krasnoyarsk Territory, the Samara and Nizhny Novgorod regions. Coupons on these bonds, as well as on OFZ, are not subject to personal income tax, while the yield on the securities is slightly higher due to lower reliability. Quite often, such bonds provide for debt amortization.

Important! State and municipal bonds are not identical in terms of credit risk. Of course, the state will do its best to help the region fulfill its obligations if the latter finds itself in a difficult financial situation. But a default by the issuer is still possible, including if the state is solvent, so the risk of such investments is higher than when investing in ordinary OFZs. It is not correct to buy regional bonds because of higher yields and consider them equal in reliability to state bonds.

Classification of bonds by type of income generation.

Discount (zero-coupon) bonds. Bonds of this type do not provide for coupon payments. Such bonds are initially placed below par value, and the investor's income is only the difference between the purchase price of the paper and the redemption/sale price. Such securities are quite rare on the Moscow Exchange.

Bonds with a fixed coupon. A fixed coupon is a certain percentage of the face value, which is paid at certain intervals. The interest rate on a bond is known from the moment of issue and, as a rule, is the same throughout the entire circulation period of the paper. For such a security, you can draw up a schedule of coupon payments with exact amounts and calculate the yield to maturity.

Example: Corporate bond SberB BO37 with a fixed coupon. This bond provides for coupon payments every six months in March and September at the rate of 9.25% per annum. The maturity date of the bond is September 30, 2021. For such a bond, the yield to maturity can be accurately calculated, including taking into account the reinvestment of coupons.

Variable coupon bonds

Variable coupon bonds are often found among corporate securities. For such bonds, the coupon is fixed until the offer date, after which the interest rate changes depending on market conditions. However, the new interest rate is unknown before the offer is made. This mechanism allows the issuer to reduce interest rate risk, especially if the issue is placed during a period of high interest rates with the prospect of a decrease, and the investor has the opportunity to repay the bond early under the offer. In the intervals between offers, such securities are no different from bonds with a fixed coupon, with the difference that the yield is correctly calculated not to the maturity date, but to the date of the nearest offer. Read more about the offers in the article Offer on bonds. What does an investor need to know about this?

Example: corporate bond ObuvrusB1 with a variable coupon. The bond maturity date is 07/15/2020, the current interest rate of 15% is valid only until the offer date of 07/17/2019. After this, the coupon value will be calculated at the new interest rate.

Important! In the QUIK terminal, there is a “Yield” column in the bonds table. It is worth considering that the correct value can only be obtained for bonds with a fixed coupon, for which the interest rate is known for the entire circulation period. For other securities, you need to calculate the yield yourself or use specialized information resources.

Bonds with a floating (indexed) coupon.

The interest rate on such securities is tied to changes in some other indicative financial instrument. This instrument can be the key rate of the Bank of Russia, the consumer price index, the RUONIA rate, the dollar exchange rate, the LIBOR rate (for Eurobonds) and others. As a rule, you can calculate the coupon size for such securities for no more than one coupon period. The calculation formula is published by the issuer and is available to all investors.

Floating coupon bonds are inconvenient because future returns can only be predicted, which is not always possible, especially if the formula includes several poorly predictable indicative instruments. However, this form of coupon is good because it allows you to insure yourself, for example, against a sudden change in the interest rate, as was the case at the end of 2014, when the key rate was increased by 6.5%. For securities with a rate tied to it, the coupon was indexed, and investors received higher payments during this period, while fixed-income bonds compensated for the increase in yields by reducing the par value, which was extremely unprofitable for investors owning the securities.

Example 1: corporate bond Rosneft BO-18 with a floating coupon. The interest rate is determined based on the Key Rate of the Central Bank of the Russian Federation plus 0.1%, but not less than 0.01%. The key rate is determined as of the 5th business day preceding the start date of the calculated coupon period. Thus, the next coupon for the period from January 22, 2018 to April 23, 2018 is calculated at a rate of 7.75 + 0.1 = 7.85% per annum.

Example 2: Russian Railways corporate bond 32 OBL with a floating coupon linked to the consumer price index (CPI) in the 2nd month preceding the month of the start of the next coupon period. The interest rate is calculated using the formula (CPI-100%)+2.1%. Thus, the coupon for the period from 01/12/2018 to 07/13/2018 will be paid at a rate of 4.6% per annum. The table below shows all calculated coupon payments during the circulation period.

Classification of bonds by type of par value redemption

Full repayment of the face value at the end of the term

By default, the principal amount is paid to the investor in full on the bond's maturity date. This type of repayment is the most common among securities on the Moscow Exchange.

Bonds with indexed par value.

Sometimes the float for a bond is not the coupon, but the par value of the paper. A striking example is the OFZ 52001 bond, for which the coupon is fixed at 2.5%, and the nominal value is annually indexed to inflation. This type of OFZ is quite good in times of high inflation, or as insurance against a future acceleration in price growth. The downside is that it will only be received upon redemption or sale; therefore, it will not be possible to reinvest it.

Amortizing bonds.

For most bonds traded on the Moscow Exchange, the par amount is paid to the investor in full on the maturity date. However, the issuer may not be comfortable with such a form of borrowing, in which by the maturity date it will be necessary to accumulate a large amount of money to repay the issue. Then he issues a bond with amortizing debt, the par value of which is repaid in installments parallel to coupon payments. This allows the issuer to distribute debt repayments evenly over the entire circulation period. Such securities are often found among municipal bonds.

For an investor, other things being equal, this type of redemption is less profitable, since after receiving part of the par value, the next coupons are accrued on the remaining value of the paper, due to which the total income is less. However, such securities can be convenient during periods of low interest rates when they are expected to rise. Then the returned part of the nominal value can be reinvested at a higher interest rate.

Example 1: Discount bond OFZ-46005 with debt amortization. The bond was issued in 2003 at a discount to its face value of 1,000 rubles. On January 10, 2021, investors were paid 70% of the nominal value (RUB 700), and on January 9, 2021, the remaining 30% (RUB 300) will be repaid. Currently, the security is trading at 95.6% of the remaining par value (RUB 286.8), which upon maturity will give a yield of about 5.27% due to the difference in price.

Example 2: Corporate bond with a fixed coupon and debt amortization AHML 11ob. The bond's par value is redeemed according to the schedule presented below. The interest rate of 8.2% is fixed for the entire circulation period, accrued on the outstanding balance of the par value. Also for this security there is an offer with a call option on September 15, 2018.

* The name “BCS Premier” is used by the Joint Stock Company “BCS – Investment Bank” (hereinafter referred to as the Bank) (General License of the Central Bank of the Russian Federation No. 101 dated December 15, 2014, issued without limitation of validity) as a commercial designation to identify the services provided by the Bank.

LLC "Company BKS", license No. 154-04434-100000 dated January 10, 2001 to carry out brokerage activities. Issued by the Federal Financial Markets Service. No expiration date.