Financial Guide > Financial Encyclopedia

Standard & Poor's (S&P) is a rating agency and financial market research subsidiary of McGraw-Hill Corporation. Along with Moody's and Fitch Ratings, this company belongs to the three most influential international rating agencies. S&P is also known as the creator and editor of the American stock index S&P 500 and the Australian S&P 200.

|

Company `s logo

Standard & Poor's presentation

Like the others of the Big Three, S&P is headquartered in New York, the financial center not only of the United States, but of the entire world. In the New York area of Manhattan, the world's key stock exchanges are located - NYSE and NASDAQ (for more details, see the Masterforex Academy's author's rating of the TOP stock exchanges in the world), offices of the largest investment funds, banks and other largest companies. There is also the famous Wall Street, which gave a start in life to many financial magnates.

Standard & Poor's was founded in 1860, much earlier than Moody's (1909) and Fitch Ratings (1914).

The founder, Henry Varnum Poor, a lawyer and financial analyst, decided to systematize financial information, for which in 1860 he published the publication “History of Railroads and Canals in the United States.” Thus began the history of the S&P.

As the title suggests, the manual included data only on the financial and operating condition of US railroad companies. A little later, together with his son (Henry William), he founded the HV and HW Poor Co. and began publishing financial statistics on a regular basis.

Fun fact: the last name of the founder of S&P – Poor – means “poor”.

The agency became Standard & Poor's in 1941 after the merger of Poor's Publishing and Standard Statistics. The owner was Paul Talbot Babson.

In 1966, S&P came under the control of The McGraw-Hill Companies.

From April 2021 – S&P Global Inc. It controls S&P Global Ratings, S&P Global Market Intelligence, S&P Global Platts and, partly through its majority ownership, S&P Dow Jones.

History of Standard & Poor's

Standard & Poor's traces its history back to 1860, with the publication of Henry Varnum Poor's History of Railroads and Canals in the United States. This book was an attempt to collect the most complete information on the financial and operating conditions of US railroad companies. Together with his son Henry William, he created and began publishing an updated version of this book annually.

In 1906, Luther Blake Lee founded the Standard Statistics Bureau to provide financial information on non-railroad companies.

In 1941, Poore and Standard Statistics merged to form Standard & Poor's Corp. In 1966, S&P was acquired by McGraw-Hill and currently provides financial support for the division.

Standard & Poor's Long-Term Credit Rating Scale

The S&P rating scale does not differ from similar ratings of other representatives of the Big Three. There is an investment and speculative class, the letter code is from AAA to D.

Investment class of financial assets from Standard & Poor's:

- AAA – maximum rating, no questions about solvency;

- AA – high level, there are practically no credit risks, but the issuer does not yet reach the highest level;

- A – high rating, but there is a dependence of creditworthiness on the economic situation;

- BBB – average, but still investment level.

Speculative class:

- ВВ – solvency is satisfactory, but the financial solvency of the issuer is highly dependent on prices on the world market (this rating is often observed among issuers that have sufficient solvency only under favorable market conditions and do not have sufficient reserves of gold and foreign exchange reserves);

- B – the assessment is similar to BB, but the issuer’s dependence on the economic situation is more pronounced; as soon as the demand for their main export product falls or its price falls, solvency sharply deteriorates;

- SSS – the issuer’s creditworthiness is limited, problems with debt servicing periodically appear;

- SS – low creditworthiness, serious debt servicing problems;

- C – default is possible, but debt obligations are still partially fulfilled;

- SD – partial default – refusal to service certain debt obligations;

- D – the issuer declared a default, refusal on all or most of its debt obligations.

S&P credit ratings

As an international rating agency, Standard & Poor's provides short- and long-term credit ratings for both issuers and individual debt obligations.

S&P ratings on an international scale

The Standard & Poor's international credit rating scale serves to meet the needs of participants in global (international) financial markets. Ratings on this scale allow one to compare the reliability of issuers and the obligations of different states.

Long-term credit ratings

Long-term ratings assess the issuer's ability to timely fulfill its debt obligations. The company's ratings are graded by letter, ranging from AAA, which is assigned to exceptionally reliable issuers, to D, which is assigned to an issuer that has defaulted. Between AA and B grades there may be intermediate grades indicated by plus and minus signs (for example, BBB+, BBB and BBB-).

- AAA - the issuer has exceptionally high capabilities to pay interest on debt obligations and the debts themselves.

- AA - the issuer has a very high ability to pay interest on debt obligations and the debts themselves.

- A - the issuer's ability to pay interest and debts is highly assessed, but depends on the economic situation.

- BBB - the solvency of the issuer is considered satisfactory.

- BB - the issuer is solvent, but unfavorable economic conditions may adversely affect the ability to pay.

- B - the issuer is solvent, but unfavorable economic conditions are likely to negatively affect its ability and willingness to make debt payments.

- CCC - the issuer is experiencing difficulties in making payments on debt obligations and its ability to do so depends on favorable economic conditions.

- CC - the issuer is experiencing serious difficulties with payments on debt obligations.

- C - the issuer is experiencing serious difficulties with payments on debt obligations; bankruptcy proceedings may have been initiated, but payments on debt obligations are still being made.

- SD - the issuer refused to pay on some obligations.

- D - a default has been declared and S&P believes that the issuer will refuse to pay most or all of its obligations.

- NR—no rating assigned.

Short-term credit ratings

Short-term ratings assess the likelihood of timely repayment of short-term debt obligations. Standard & Poor's credit ratings for short-term debt are given an alphanumeric designation, ranging from the highest rating of A-1 to the lowest rating of D. Stronger obligations in the A-1 category may be marked with a plus sign. Grades from category B can also be specified with a number (B-1, B-2, B-3).

- A-1 - the issuer has an exceptionally high ability to repay this debt obligation.

- A-2 - the issuer has a high ability to repay this debt obligation, but this ability is more sensitive to adverse economic conditions.

- A-3 - Adverse economic conditions are likely to impair the issuer's ability to repay the debt obligation.

- B - the debt obligation is speculative in nature. The issuer has the ability to repay it, but these opportunities are very sensitive to unfavorable economic conditions.

- C — the issuer’s ability to repay this debt obligation is limited and depends on the presence of favorable economic conditions.

- D—this short-term debt obligation has defaulted.

National ratings

Along with the international credit rating scale, Standard & Poor's also supports a number of national scales, including the Russian one. National scales are designed to meet the needs of participants in national financial markets. The issuer rating and debt rating on the national scale reflect an assessment of the relative reliability of issuers and debt obligations present in the national market. The national scale provides more opportunities for distinguishing the creditworthiness of issuers, as it excludes some sovereign risks, in particular the risk of transferring funds outside the state and other systematic risks that are equally characteristic of all issuers in a given market.

Since ratings on a national scale reflect national specifics, it makes no sense to compare ratings on different national scales. Similarly, ratings on the national scale and on the international scale are not comparable.

The Standard & Poor's credit rating scale for the Russian Federation uses the traditional Standard & Poor's symbols with the prefix "ru".

Forecasts

Along with assigning a rating, S&P also indicates a forecast for changes in the rating in the next two to three years:

- Positive outlook - possible rating increase.

- Negative outlook—possible rating downgrade.

- Stable forecast - the rating will most likely remain unchanged.

- The developing forecast is that both an increase and a downgrade in the rating are possible.

BICRA

The BICRA (banking industry country risk assessment) indicator reflects the strengths and weaknesses of the banking system of a particular country in comparison with the banking systems of other countries. Using the BICRA grading, banking systems are divided into 10 groups in terms of their exposure to country risks, with the strongest countries in group 1 and the weakest in group 10.

For example: the following countries are included in group 9: Kazakhstan, Belarus, Azerbaijan, Georgia.

Standard & Poor's short-term credit rating scale

Short-term ratings show the issuer's creditworthiness over a 12-month period.

- A-1 – the highest level;

- A-2 – high level, there is sensitivity to economic changes;

- A-3 – economic instability can undermine the creditworthiness of the issuer;

- B – speculative level, the issuer is solvent, but is especially sensitive to the economic situation;

- C – solvency is limited, strong dependence on market conditions;

- D – the issuer is in default.

TOP countries with high Standard & Poor's ratings

11 countries have the highest long-term credit rating S&P (AAA) in foreign currency (as of 2021). Many of them have huge foreign debts, but are considered highly reliable because, even though they borrow a lot, they repay them on time (debt in $ in parentheses).

North America:

- Canada (1.6 trillion).

Australia and Oceania:

- Australia (1.5 trillion).

Asia:

- Singapore (633 billion).

Europe:

- Germany (2.56 trillion);

- Switzerland (1.84 trillion);

- Sweden (910 billion);

- Norway (615 billion);

- Netherlands (513 billion);

- Denmark (109 billion);

- Luxembourg (16.14 billion);

- Liechtenstein (0).

Interesting fact: S&P is the only representative of the Big Three on whose scale the United States does not have the maximum credit rating.

In the author’s article “Creditors or to whom the world’s population owes $244 trillion,” you will become familiar with the reasons for the emergence of huge external debt.

Table of countries by size of external debt.

| № | State | National currency (Ticker) | External debt ($ billion) | External debt ($) per capita | External debt to GDP in % | |

| 1 | Austria | Euro (EUR) | ECB | $345.9 billion | $98.7 thousand | 194% |

| 2 | Belgium | $566.4 billion | $136.2 thousand | 338% | ||

| 3 | Germany | $2.557 trillion. | $31.4 thousand | 71% | ||

| 4 | Greece | $589.6 billion | $52.7 thousand | 234% | ||

| 5 | Ireland | $2.747 trillion. | $542.1 thousand | 737% | ||

| 6 | Spain | $1.849 trillion. | $8 thousand | 137% | ||

| 7 | Italy | $3.16 trillion. | $52.66 thousand | 144% | ||

| 8 | Cyprus | $95.2 billion | $81.2 thousand | 107% | ||

| 9 | Latvia | $39.8 billion | $18.4 thousand | 131% | ||

| 10 | Lithuania | $29.5 billion | $8.4 thousand | 63% | ||

| 11 | Luxembourg | $16.14 billion | $4.55 million | 3600% | ||

| 12 | Malta | $46.2 billion | $112 thousand | 496% | ||

| 13 | Netherlands | $515.3 billion | $29.99 thousand | 64% | ||

| 14 | Portugal | $452.4 billion | $43.7 thousand | 190% | ||

| 15 | Slovakia | $68.4 billion | $12.5 thousand | 70% | ||

| 16 | Slovenia | $53.9 billion | $27.1 thousand | 115% | ||

| 17 | Finland | $158.6 billion | $111.3 thousand | 266% | ||

| 18 | France | $6.266 trillion. | $32 thousand | 98% | ||

| 19 | Montenegro | $650 million | $939 | 24% | ||

| 20 | Estonia | $26.7 billion | $21.2 thousand | 110% | ||

| 21 | Albania | Albanian Lek (ALL) | Bank of Albania | $1.55 billion | $ 497 | 21% |

| 21 | Belarus | Belarusian ruble (BYN) | NBB | $38.6 billion | $4 thousand | 79% |

| 22 | Bulgaria | Bulgarian Lev (BGN) | BNB | $37.8 billion | $5.4 thousand | 70% |

| 23 | Great Britain | pound sterling (GBP) | Bank of England | $2.681 trillion. | $119 thousand | 108% |

| 24 | Hungary | Hungarian Forint (HUF) | National Library of Hungary | $170.3 billion | $17.1 thousand | 130% |

| 25 | Denmark | Danish krone (DKK) | National Library of Denmark | $109.1 billion | $105.3 thousand | 244% |

| 26 | Iceland | Icelandic krona (ISK) | Central Bank of Iceland | $102 billion | $321.4 thousand | 699% |

| 27 | Moldova | Moldovan Leu (MDL) | National Library of Moldova | $3.9 billion | $1.1 thousand | 73% |

| 28 | Norway | Norwegian krone (NOK) | Norwegian bank | $614.8 billion | $139.8 thousand | 201% |

| 29 | Poland | Polish zloty (PLN) | National Library of Poland | $352.3 billion | $9.5 thousand | 71% |

| 30 | Romania | Romanian leu (RON) | National Library of Romania | $130.4 billion | $6 thousand | 71% |

| 31 | Russia | Russian ruble RUB | Bank of Russia | $453.75 billion | $3 thousand | 36% |

| 32 | Ukraine | Hryvnia (UAH) | NBU | $78.3 billion | $1.8 thousand | 63% |

| 33 | Czech | Czech crown (CZK) | National Library of the Czech Republic | $103.2 billion | $9.7 thousand | 52% |

| 34 | Croatia | Croatian Kuna (HRK) | Croatian NB | $63.3 billion | $14.1 thousand | 108% |

| 35 | Sweden | Swedish krona (SEK) | Bank of Sweden | $910 billion | $16 thousand | 18% |

| 36 | Switzerland | Swiss franc (CHF) | National Library of Switzerland | $1.844 trillion. | $191.5 thousand | 27% |

| Oceania | ||||||

| 37 | Australia | Australian dollar (AUD) | RB Australia | $1.486 trillion. | $66.9 thousand | 151% |

| 38 | New Zealand | New Zealand dollar (NZD) | RB NZ | $81.3 billion | $18.4 thousand | 45% |

| Asia | ||||||

| 39 | Azerbaijan | Azerbaijani manat (AZN) | Central Bank of Azerbaijan | $6.0 billion | $647 | 8% |

| 40 | Armenia | Armenian dram (AMD) | Central Bank of Armenia | $8.6 billion | $2.9 thousand | 75% |

| 41 | Vietnam | Vietnamese dong (VND) | GB of Vietnam | $68.3 billion | $732 | 40% |

| 42 | Hong Kong | Hong Kong dollar (HKD) | Hong Kong parole | $1.63 trillion. | $155.9 thousand | 290% |

| 43 | Georgia | Lari (GEL) | National Library of Georgia | $14.1 billion | $3.7 thousand | 90% |

| 44 | Israel | Shekel (ILS) | Bank of Israel | $96.3 billion | $12.3 thousand | 35% |

| 45 | India | Indian Rupee (INR) | RB India | $550 billion | $423 | 27% |

| 46 | Indonesia | Indonesian Rupiah (IDR) | Bank Indonesia | $223.8 billion | $882 | 26% |

| 47 | Iraq | Iraqi Dinar (IQD) | Central Bank of Iraq | $59.5 billion | $1.8 thousand | 27% |

| 48 | Iran | Iranian rial (IRR) | Central Bank of Iran | $15.6 billion | $193 | 4% |

| 49 | Kazakhstan | Tenge (KZT) | NB RK | $161.4 billion | $9.1 thousand | 94% |

| 50 | Kyrgyzstan | Som (KGS) | NB KR | $3.7 billion | $600 | 54% |

| 51 | China | Chinese Yuan (CNY) | National Bank of China | $1.607 trillion. | $1.15 thousand | 14% |

| 52 | Kuwait | Kuwaiti Dinar (KWD) | Central Bank of Kuwait | $34.4 billion | $12.5 thousand | 19% |

| 53 | Malaysia | Malaysian ringgit (MYR) | BNM | $100.1 billion | $3.3 thousand | 32% |

| 54 | UAE | UAE Dirham (AED) | Central Bank of the UAE | $163.8 billion | $24.2 thousand | 41% |

| 55 | Pakistan | Pakistani Rupee (PKR) | GB of Pakistan | $66.4 billion | $346 | 22% |

| 56 | The Republic of Korea | South Korean won (KRW) | Bank of South Korea | $430.9 billion | $8.7 thousand | 36% |

| 57 | Saudi Arabia | Saudi Riyal (SAR) | ADO SA | $149.4 billion | $5.4 thousand | 20% |

| 58 | Singapore | Singapore dollar (SGD) | DKUS | $632.6 billion | $210.8 thousand | 346% |

| 59 | Tajikistan | Somoni (TJS) | National Library of Tajikistan | $2.1 billion | $270 | 28% |

| 60 | Thailand | Thai baht (THB) | Bank of Thailand | $86.1 billion | $1.2 thousand | 21% |

| 61 | Turkmenistan | New Turkmen manat (TMT) | Central Bank of Turkmenistan | $5.0 billion | $934 | 31% |

| 62 | Türkiye | Turkish lira (TRY) | Central Bank of TR | $685.2 billion | $4.4 thousand | 44% |

| 63 | Uzbekistan | Uzbek sum (UZS) | Central Bank of the Republic of Uzbekistan | $17.3 billion | $520 | 33% |

| 64 | Philippines | Philippine Peso (PHP) | Central Bank of the Philippines | $72.8 thousand | $676 | 27% |

| 65 | Sri Lanka | Sri Lankan Rupee (LKR) | CB SHL | $1.2 thousand | $42 | 66% |

| 66 | Japan | Japanese Yen (JPY) | Bank of Japan | $13.5 trillion. | $76.8 thousand | 295% |

| North America | ||||||

| 67 | Dominican Republic | Dominican Peso (DOP) | Central Bank of the DR | $18 billion | $1.7 thousand | 30% |

| 68 | Canada | Canadian dollar (CAD) | Bank of Canada | $1.613 trillion. | $38.2 thousand | 88% |

| 69 | Cuba | Cuban Peso (CUP) | Central Bank of Cuba | $23.4 billion | $2.1 thousand | 32% |

| 70 | Mexico | Mexican Peso (MXN) | Bank of Mexico | $1.444 trillion. | $10.7 thousand | 27% |

| 71 | Panama | Balboa (PAB) | NB of Panama | $15.2 billion | $4.2 thousand | 37% |

| 72 | USA | US dollar (USD) | Fed | $23.14 trillion. | $69.6 thousand | 135% |

| South America | ||||||

| 73 | Argentina | Argentine Peso (ARS) | Central Bank of Azerbaijan | $111.5 billion | $2.5 thousand | 23% |

| 74 | Brazil | Brazilian real (BRL) | Central Bank of Brazil | $3.195 trillion. | $2.3 thousand | 122% |

| 75 | Chile | Chilean Peso (CLP) | Central Bank of Chile | $119 billion | $6.8 thousand | 42% |

| Africa | ||||||

| 76 | Algeria | Algerian Dinar (DZD) | Bank of Algiers | $3.4 billion | $97 | 2% |

| 77 | Egypt | Egyptian pound (EGP) | Central Bank of Egypt | $48.7 billion | $561 | 19% |

| 78 | Morocco | Moroccan Dirham (MAD) | Bank of Morocco | $36.5 billion | $1.1 thousand | 35% |

| 79 | Nigeria | Naira (NGN) | Central Bank of Nigeria | $15.7 billion | $89 | 5% |

| 80 | Tunisia | Tunisian Dinar (TND) | Central Bank of Tunisia | $26.9 billion | $2.4 thousand | 56% |

| 81 | South Africa | South African rand (ZAR) | SARB | $139 billion | $2.8 thousand | 39% |

Credit rating of Russia from Standard & Poor's

- BBB- – long-term credit rating of Russia in foreign currency;

- BBB – long-term credit rating of Russia in local currency;

- A3 – short-term credit rating of Russia in foreign currency;

- A2 – short-term credit rating of Russia in local currency

S&P evaluates the credit rating of the Russian Federation as follows:

- long-term in foreign currency - the lower level of investment grade, under threat of being downgraded by one level if the economic situation changes;

- long-term in local currency - lower level of investment grade

- short-term in foreign currency - the lower level of investment grade;

- short-term in local currency – high level, but there are risks if the economic situation worsens;

History of the credit rating of the Russian Federation

| date | International rating | National ranking scale | |||||

| In foreign currency | In national currency | ||||||

| Long term | Forecast | Short-term | Long term | Forecast | Short-term | ||

| 21.12.09 | BBB | Stable | A-3 | BBB+ | Stable | A-2 | ruAAA |

| 08.12.08 | BBB | Negative | A-3 | BBB+ | Negative | A-2 | ruAAA |

| 04.09.06 | BBB+ | Stable | A-2 | A- | Stable | A-2 | ruAAA |

| 15.12.05 | BBB | Stable | A-2 | BBB+ | Stable | A-2 | ruAAA |

| 19.07.05 | BBB- | Stable | A-3 | BBB | Stable | A-3 | ruAAA |

| 31.01.05 | BBB- | Stable | A-3 | BBB | Stable | A-3 | ruAAA |

| 12.07.04 | BB+ | Stable | B | BBB- | Stable | A-3 | ruAA+ |

| 27.01.04 | BB+ | Stable | B | BBB- | Stable | A-3 | ruAA+ |

| 03.11.03 | BB | Stable | B | BB+ | Stable | B | ruAA+ |

| 05.12.02 | BB | Stable | B | BB+ | Stable | B | ruAA+ |

| 26.07.02 | BB- | Stable | B | BB- | Stable | B | ruAA+ |

| 22.02.02 | B+ | Positive | B | B+ | Positive | B | ruAA+ |

| 19.12.01 | B+ | Stable | B | B+ | Stable | B | — |

| 04.10.01 | B | Positive | B | B | Positive | B | — |

| 28.06.01 | B | Stable | B | B | Stable | B | — |

| 08.12.00 | B- | Stable | C | B- | Stable | C | — |

| 27.07.00 | SD | — | — | B- | Stable | C | — |

Credit rating of Kazakhstan from Standard & Poor's

- BBB- – long-term credit rating of Kazakhstan in foreign and local currency;

- A-3 – short-term credit rating of Kazakhstan in foreign and local currency.

S&P's assessment of Kazakhstan's long-term foreign and local currency credit rating is similar to Russia's foreign currency rating, and its short-term multi-currency rating is similar to Russia's foreign currency rating.

That is, S&P considers the solvency of Russia and Kazakhstan in foreign currencies to be the same, but in local currencies, Russia is one level higher.

Country rating according to S&P

Long-term credit ratings

Long-term ratings assess the issuer's ability to timely fulfill its debt obligations.

The company's ratings are graded by letter, ranging from AAA, which is assigned to exceptionally reliable issuers, to D, which is assigned to an issuer that has defaulted. AAA - the issuer has exceptionally high capabilities to pay interest on debt obligations and the debts themselves. AA - the issuer has a very high ability to pay interest on debt obligations and the debts themselves. A - the issuer's ability to pay interest and debts is highly assessed, but depends on the economic situation. BBB - the solvency of the issuer is considered satisfactory. BB - the issuer is solvent, but unfavorable economic conditions may adversely affect the ability to pay. B - the issuer is solvent, but unfavorable economic conditions are likely to negatively affect its ability and willingness to make debt payments. CCC - the issuer is experiencing difficulties in making payments on debt obligations and its ability to do so depends on favorable economic conditions. CC - the issuer is experiencing serious difficulties with payments on debt obligations. C - the issuer is experiencing serious difficulties with payments on debt obligations; bankruptcy proceedings may have been initiated, but payments on debt obligations are still being made. SD - the issuer refused to pay on some obligations. D - a default has been declared and S&P believes that the issuer will refuse to pay most or all of its obligations. NR—no rating assigned. CCC ratings from AA may be supplemented by plus and minus signs (for example, BBB+, BBB and BBB-) for intermediate evaluation.

Short-term credit ratings

Short-term ratings assess the likelihood of timely repayment of short-term debt obligations. Standard & Poor's credit ratings for short-term debt are given an alphanumeric designation, ranging from the highest rating of A-1 to the lowest rating of D. Stronger obligations in the A-1 category may be marked with a plus sign. Grades from category B can also be specified with a number (B-1, B-2, B-3).

A-1 - the issuer has an exceptionally high ability to repay this debt obligation. A-2 - the issuer has a high ability to repay this debt obligation, but this ability is more sensitive to adverse economic conditions. A-3 - Adverse economic conditions are likely to impair the issuer's ability to repay the debt obligation. B - the debt obligation is speculative in nature. The issuer has the ability to repay it, but these opportunities are very sensitive to unfavorable economic conditions. C — the issuer’s ability to repay this debt obligation is limited and depends on the presence of favorable economic conditions. D—this short-term debt obligation has defaulted.

Forecasts

Along with assigning a rating, S&P also indicates a forecast for changes in the rating in the next two to three years:

Positive outlook - possible rating increase. Negative outlook—possible rating downgrade. Stable forecast - the rating will most likely remain unchanged. The developing forecast is that both an increase and a downgrade in the rating are possible.

Standard & Poor's stock indices

S&P is a well-known and authoritative compiler of stock indexes of the S&P Dow Jones Indices family. It is a joint venture between S&P Global, CME Group and News Corp.

The most famous indices of the S&P Dow Jones Indices family:

- S&P 500 (one of the key NYSE indexes);

- Dow Jones Industrial Average (DJIA), also known as Dow Jones 30 (also one of the key NYSE indexes).

In total, the agency compiles over 130,000 indexes!

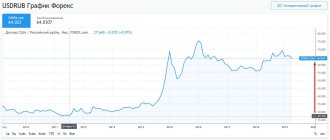

Owner of Standard & Poor's and its shares on the stock exchange

The S&P rating agency is a subsidiary of S&P Global, whose shares are listed on the New York Stock Exchange under the ticker symbol SPGI.

The dynamics of the S&P Global stock price for 5 years (2015-2020) are shown in the graph:

Standard & Poor's - rating service

Standard & Poor's (S&P) is a financial market research subsidiary of McGraw-Hill Corporation. The company is located in New York and belongs to the three most influential international rating agencies. S&P is also known as the creator and editor of the American stock index S&P 500 and the Australian S&P 200. As an international rating agency, Standard & Poor's assigns short- and long-term credit ratings to both issuers and individual debt obligations.

The Standard & Poor's international credit rating scale serves to meet the needs of participants in global (international) financial markets. Ratings on this scale allow one to compare the reliability of issuers and the obligations of different states.

Long-term ratings assess the issuer's ability to timely fulfill its debt obligations. The company's ratings are graded by letter, ranging from AAA for exceptionally reliable issuers to D for a defaulting issuer. Between AA and B grades there may be intermediate grades indicated by plus and minus signs (for example, BBB+, BBB and BBB-).

AAA - the issuer has exceptionally high capabilities to pay interest on debt obligations and the debts themselves. AA - the issuer has a very high ability to pay interest on debt obligations and the debts themselves. A - the issuer's ability to pay interest and debts is highly assessed, but depends on the economic situation. BBB - the solvency of the issuer is considered satisfactory. BB - the issuer is solvent, but unfavorable economic conditions may adversely affect the ability to pay. B - the issuer is solvent, but unfavorable economic conditions are likely to negatively affect its ability and willingness to make debt payments. CCC - the issuer is experiencing difficulties in making payments on debt obligations and its ability to do so depends on favorable economic conditions. CC - the issuer is experiencing serious difficulties with payments on debt obligations. C - the issuer is experiencing serious difficulties with payments on debt obligations; bankruptcy proceedings may have been initiated, but payments on debt obligations are still being made. SD - the issuer refused to pay on some obligations. D - a default has been declared and S&P believes that the issuer will refuse to pay most or all of its obligations. NR —no rating assigned.

Short-term ratings assess the likelihood of timely repayment of short-term debt obligations. Standard & Poor's credit ratings for short-term debt are given an alphanumeric designation, ranging from the highest rating of A-1 to the lowest rating of D. Stronger obligations in the A-1 category may be marked with a plus sign. Grades from category B can also be specified with a number (B-1, B-2, B-3).

A-1 - the issuer has an exceptionally high ability to repay this debt obligation. A-2 - the issuer has a high ability to repay this debt obligation, but this ability is more sensitive to adverse economic conditions. A-3 - Adverse economic conditions are likely to impair the issuer's ability to repay the debt obligation. B - the debt obligation is speculative in nature. The issuer has the ability to repay it, but these opportunities are very sensitive to unfavorable economic conditions. C — the issuer’s ability to repay this debt obligation is limited and depends on the presence of favorable economic conditions. D —this short-term debt obligation has defaulted.

Why are rating agencies needed?

Rating agencies S&P, Fitch Ratings and Moody's make life much easier for traders and investors, saving them time, i.e. money to collect analytical information about the solvency of a potential investment object.

The rating scale immediately shows how financially sound the issuer is and how exposed it is to economic risks.

A high credit rating results in a low profit, but this is a guaranteed income without nerves. Often, investors receive little profit from highly reliable securities, so they use them not as the main source of profit, but as a means of diversifying risks from investments in high-yield but risky stocks, bonds, futures, stock indices, options and other assets.

According to ratings from S&P:

- Central banks approve the key rate, and it already forms the amount of loans and deposits in private banks (see the table of key rates of the world's central banks).

- The foreign exchange market (forex and exchanges) changes the bullish trend to a bearish one or vice versa, based on expectations of the issue of fiat money, rising inflation, the level of devaluation of national currencies to USD, CHF, JPY, EUR, GBR and other currencies.

- The stock market is revising quotes for securities and derivatives;

- Investors and shareholders decide to withdraw or bring capital into the country if the profitability of investments in EUR and USD changes.

- Investment funds change the contents of investment portfolios, making changes to the list of financial assets and quasi-money.

Broker rating

Trading is gaining widespread popularity. In the West, people have long realized that investing in securities is much more profitable than keeping money in a bank savings account. In the USA, the population's involvement in the stock market exceeds 50%!

Now imagine the potential of Russia, if the involvement here barely reaches a few percent. The reason is the insufficient development and accessibility of the local stock market and a considerable number of negative reviews from cooperation with brokerage companies.

The Masterforex-V Academy has compiled a rating of the reliability of Russian brokers, after reading which current and future traders will be able to avoid mistakes when choosing a partner to conquer financial heights.

| Broker name | Year of foundation | Financial instruments | Licenses from financial regulators | |

| 1. | NordFX | 2008 | currency pairs, commodity futures, stock indices, cryptocurrencies, stocks | CySEC, MiFID |

| 2. | Swissquote | 1996 | commodity futures, currency pairs, stock index futures, cryptocurrencies, metals, ETFs, warrants, shares | FINMA, FCA, SFC, Dubai FSA |

| 3. | Dukascopy | 1998 | stock indices, commodity futures, currency pairs, stocks, bonds, ETFs | FINMA, FCMC |

| 4. | Alpari | 1998 | metals, energy, indices, currency pairs, cryptocurrencies | ARFIN |

| 5. | FxPro | 2006 | indices, commodity futures, stocks, currency pairs | FCA, CySEC, FSB, Dubai FSA, BaFin, ACPR, CNMV |

| 6. | Interactive Brokers | 1977 | stocks, bonds, derivatives, currency pairs, forward contracts, bills, warrants, options, stock indices, currency and commodity futures | NFA, CFTC, FCA, IIROC |

| 7. | Oanda | 1996 | bonds, stock indices, currency pairs, commodity futures | NFA, CFTC, FCA, IIROC, MAS, ASIC |

| 8. | FXCM | 1999 | currency pairs, stock indices, commodity futures, cryptocurrencies | FCA, BaFin, ACPR, AMF, Dubai FSA,SFC, ISA, ASIC, FSB |

| 9. | Saxo Bank | 1992 | currency and commodity futures, stock indices, currency pairs, ETFs, stocks, bonds, derivatives | Danish FSA, Consob, Czech National Bank, Bank of the Netherlands, ASIC, Monetary Authority of Singapore, FINMA, Bank of France, Central Bank of the UAE, Japanese Financial Services Agency, Securities and Futures Commission in Hong Kong. |

| 10. | FOREX.com | 1999 | currency pairs, stocks, stock indices, commodity futures, cryptocurrencies | NFA, CFTC, FCA, ASIC, JSDA, MAS, SFC |

| 11. | FIBO Group | 1998 | metals, energy, currency pairs, commodities, cryptocurrencies, indices | CySEC |

| 12. | FINAM FOREX | 1994 | currency pairs | Bank of Russia |

How the incident in Minsk affected Nord Stream 2

The authorities should not allow themselves to make decisions that are questionable from the point of view of the law, although the motivation for such a decision can be understood, political scientist Gleb Kuznetsov told the newspaper VZGLYAD. This is how he assessed the message that the government of Yakutia is introducing mandatory vaccination against COVID-19 and intends to fine companies that have not ensured that their employees are vaccinated.

“Honestly, the decision of local authorities to compulsorily vaccinate the entire adult population of the region does not seem legal to me. As far as I know, we don't have such rules. The authorities cannot afford to stoop to making illegal decisions even in emergency circumstances,” said Gleb Kuznetsov, head of the expert council of the Expert Institute for Social Research (EISRI).

On Tuesday, RIA Novosti reported that the head of Yakutia, Aisen Nikolaev, at a meeting of the republican operational headquarters with the participation of municipal leaders, announced the introduction of mandatory mass vaccination in the republic. Nikolaev referred to the resolution of the chief sanitary doctor of the republic, adopted on May 19. Yakut companies that do not organize mandatory vaccination against coronavirus will be fined in the amount of 200 thousand rubles, the press service of the regional government said in a statement.

The same message explains: “First of all, all educational workers involved in organizing children’s summer holidays, as well as the entire contingent, from organizers and participants to hired personnel, involved in holding mass events on a republican scale are required to be vaccinated.” Later, a message appeared that the head of the Khanty-Mansiysk Autonomous Okrug, Natalya Komarova, instructed to study the experience of Yakutia.

A few hours later, changes were made to the publication on the website of the government of Yakutia, which announced the start of mandatory vaccination of the population in the republic. Now, instead of the word “mandatory” there is the word “massive”.

“If this decision is declared illegal, then the federal authorities will correct this situation. But if they find at least some legal grounds for compulsory vaccination, then perhaps this will become a kind of precedent for other subjects. Change the law and then do what you want,” noted political scientist Kuznetsov. At the same time, he noted that it is possible to understand the motivation for making such a decision. “Due to the very large territory, scattered population and small number of health care institutions, natural difficulties arise when administering a pandemic. And it is quite logical that the local authorities of the region want the pandemic to end on their territory once and for all,” the interlocutor explained.

At the same time, Kuznetsov expressed doubt about the existence of effective methods that can be used to encourage the population to voluntarily get vaccinated. “All over the world, everyone understood perfectly well that only direct state coercion creates a large number of people who want to get vaccinated. And even distributing gifts will not help here, because there will definitely be those who will not be interested in them. Moreover, even the European Union openly declares that no one will be able to travel anywhere until they are vaccinated,” the expert concluded.

Let us recall that Deputy Chairman of the Russian Security Council Dmitry Medvedev, speaking at a plenary meeting of the St. Petersburg International Legal Online Forum, noted that vaccination, although voluntary, in some cases it can become mandatory if the interests of the state require it. Medvedev later clarified his words.

Presidential press secretary Dmitry Peskov, commenting on Medvedev’s words, clarified: the issue of changing legislation to make vaccination against coronavirus mandatory in Russia is not being considered.