It is recommended to continue reading the article after familiarizing yourself with the topics:

- Bonds - what are they?

- Bond yield

To answer the question “how to choose bonds for an IIS,” we can recall the process of choosing a bank for a deposit in those days when the deposit insurance system and DIA did not yet exist.

Investors are usually interested in two main points:

- Reliability of investments

- Return on investment

Accordingly, in the “pre-insurance” era, the reliability of the bank and the rates on its deposits were studied. After the introduction of the deposit insurance system, bank depositors stopped paying attention to the first factor (the reliability of the bank), although there are still categories of people who trust only Sberbank.

By the way, this behavior is not entirely illogical, because there are already many precedents when bank depositors were denied compensation. In fact, you really shouldn’t rely on the deposit insurance system, especially for those who have already received compensation from the DIA. Why? Read about this in the article “The End of Bank Deposits.” Now let’s focus on the fact that reliability should ALWAYS be studied.

This is also true for bond investments. With bond yields, everything is simple - it’s easy to find out:

- Calculate for yourself

- Find out on the Internet

The issue is discussed in more detail in the article “Bond Yield”, and in brief, the bond yield is as follows:

- 8-8.5% (OFZ)

- 9-10% (Municipal bonds)

- 7-15% (Corporate bonds)

Why was IIS invented?

Our state borrows money through bonds to create a surplus (positive) budget , to carry out infrastructure projects, from which there will then be a return.

Accordingly, it would be good to take this money from the citizens of your country.

Why specifically the residents of our country?

Let's figure out the key rate

In this example, it is important for us to understand that the key rate affects the maximum interest on deposits and bonds.

The higher the bet, the more money you will receive.

You can see the rate on the Central Bank website https://cbr.ru/hd_base/keyrate/.

World betting

As we see, there are even negative rates in the world now! That is, people pay banks, despite inflation, just to save their money! Don't even exaggerate! In developed countries it is about 2%.

Investors (including large investment funds) try to choose a country where this rate is maximum, and the risk of default of this country would be low..

In our country, as in other developing countries, the rate is an order of magnitude higher than in developed ones.

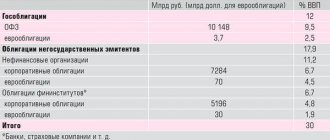

Therefore, the share of non-residents in government bonds is quite high . (34% as of January 2021)

Exchange differences

But when the currency exchange rate of the country in which you decide to invest changes, your profitability changes greatly!

Example: You are a US citizen . You have $1000 and want to buy Russian bonds. The dollar exchange rate is 50 rubles . 1 bond costs 100 rubles. Yield per annum is 10% in rubles. You buy - $1000*50/100= 500 bonds . Your projected profitability for the year: 500*(100*10%)= 5000 rubles In the currency of your country (dollars) = 5000/50= $100

There is a devaluation in the country where you bought the bonds . The dollar exchange rate rose to 100 rubles . Your projected profitability for the year: 500 * (100 * 10%) = 5000 rubles In your country’s currency (dollars) = 5000/100 = $50 Moreover, your $1000 has become = 500 bonds * 100 rubles / 100 (dollar exchange rate) = 500$

Conclusion: You not only received a return 2 times less than you planned, but also lost half of your funds!

Basic rule on the stock exchange

If something is sold, its price drops. If they buy something, it grows.

Our bonds are denominated in rubles (traded). Accordingly, if someone buys them , our ruble strengthens . If they are sold en masse , this means a budget deficit and a weakening of the ruble .

This is the main reason why it is beneficial for our state that you and I buy the national debt!

Possible negative consequences for the state with a large share of non-residents in bonds

- Lack of stability in raising funds.

- Risks of ruble weakening.

- Freezing of infrastructure projects.

It is for this purpose that the state is developing mechanisms such as IIS, trying to attract “long-term” money.

3 years, of course, cannot be called long-term money. But the initiatives have already gone further - IPA (individual pension account) https://www.banki.ru/news/lenta/?id=10892051. This has already been planned for several decades.

UPDATE : low rates + new tax on interest on deposits also forces people to buy OFZs.

Hierarchy of bond yields

Since bond yields are constantly changing, there is no need to remember what kind of yield they bring, but you can simply clarify it every time you make decisions related to investing money.

We do the same thing when we are going to deposit money in a bank: before going there, we study the conditions and rates for deposits and only after that we make a decision.

It's always a good idea to evaluate all your investment options. State, municipal and corporate bonds primarily differ in yield, and the relationship between the yields between them is approximately as follows:

- Government bonds (OFZ) = standard of risk-free return

- Municipal = OFZ * 1.15-1.2

- Corporate = OFZ * 1.2-1.4

This is an empirical observation, not a hard and fast rule. Over time, these proportions and relationships may change, but the reference point will remain unchanged - OFZ, the standard of risk-free profitability,

which, as a result, has the minimum yield among all bonds:

So, if everything is more or less clear with bond yields, then what about reliability?

Hierarchy of bond reliability

The above picture shows not only the hierarchy of returns, but also the hierarchy of risks inherent in these bonds: in any economy, government debts are considered the safest, and business debts are considered the riskiest of all types of debt.

Thus, all other things being equal, OFZs (in different countries they are called differently, but the essence is the same - these are “government bonds”, government debt) have a lower yield, because involve less risk.

Business is exposed to commercial risks, while government debt is secured by all of the government's assets (and, most importantly, the printing press).

Of course, this is not a hard and fast rule. It is quite possible to find corporate bonds with a yield lower than OFZ, but it is logical to assume that such bonds will be in less demand among investors (analogy: few people will take money to an unknown regional bank for a deposit, the interest rate on which is lower than a similar deposit in Sberbank).

Types of IIS

There are two types of IIS:

- Type A (deduction for contributions).

- Type B (income deduction).

Type A

You can return UP TO 52,000 rubles per year! (with an ANNUAL replenishment of 400,000 rubles)

Let's look at it in more detail to make it clearer.

If you work, then the employer withholds 13% of your income and pays them to the tax authority (personal income tax - personal income tax).

- When opening an IIS, the state gives you the right to return this retained 13%, but not more than 52,000 rubles per year .

- To “choose” ALL 52,000 rubles, your annual salary must be NOT LESS than 400,000 rubles. Or 400,000 rubles/12 months = 33,333 rubles/month. In general, it is important that you earn 400,000 “in white” a year.

- Then the personal income tax withheld from you will be 400,000*13%=52,000 rubles. You return this amount.

If you earned less than UP to 52,000. Accordingly, if you earned less, you’ll simply receive less . From the amount earned 13%.

Example: Earned 200,000 rubles. We topped up the IIS account with this amount for the year. Your deduction is 200,000*13%=26,000 rubles.

Lifehack

Some brokers allow you to withdraw stock dividends and bond coupons not to your brokerage account, but to your debit card.

Then, when transferring them to IIS, this will be considered a replenishment! If they immediately come to the IIS, then they WILL NOT BE CONSIDERED AS A DEPOSIT.

It makes sense to do this in the case when you have enough salary of 400,000 per annum to deduct, but there is less money to contribute.

Type B

Suitable for those who do not have official income. That is, no one pays 13% for it, so there is nothing to return!

The government offers to refund your income tax on profits made in the stock market.

Type B deduction can be obtained upon closing the account.

IMPORTANT POINT: no less than 3 years.

You must obtain a certificate from the broker that you have never received a deduction under type A (income on contributions).

Coupon harvester

Obviously, for more efficient operation of the Coupon Harvester, it is most advisable to use the following criteria for selecting OFZ:

- OFZ with the maximum possible coupon size (at the same time, the OFZ yield itself may be low - this does not play any role)

- OFZ with the closest coupon payment date

- If you plan to use margin lending, then you need OFZs included in the broker’s margin list

Here is the schedule for OFZ coupon payments in 2021:

| Name | maturity date | Coupon size, rub | Months until maturity | Next coupon date |

| OFZ 46023 | 2026.07.23 | 36.62 | 103.4 | 2018.02.01 |

| OFZ 29006 | 2025.01.29 | 52.9 | 85.7 | 2018.02.07 |

| OFZ 46021 | 2018.08.08 | 12.47 | 8.1 | 2018.02.07 |

| OFZ 46020 | 2036.02.06 | 34.41 | 217.6 | 2018.02.14 |

| OFZ 26207 | 2027.02.03 | 40.64 | 109.8 | 2018.02.14 |

| OFZ 52001 | 2023.08.16 | 14.03 | 68.2 | 2018.02.21 |

| OFZ 26215 | 2023.08.16 | 34.9 | 68.2 | 2018.02.21 |

| OFZ 26217 | 2021.08.18 | 37.4 | 44.4 | 2018.02.21 |

| OFZ 46014 | 2018.08.29 | 17.45 | 8.8 | 2018.02.28 |

| OFZ 46018 | 2021.11.24 | 16.21 | 47.6 | 2018.02.28 |

| OFZ 26208 | 2019.02.27 | 37.4 | 14.8 | 2018.02.28 |

| OFZ 29007 | 2027.03.03 | 51.96 | 110.7 | 2018.03.14 |

| OFZ 26204 | 2018.03.15 | 37.4 | 3.3 | 2018.03.15 |

| OFZ 46019 | 2019.03.20 | 8 | 15.4 | 2018.03.21 |

| OFZ 26219 | 2026.09.16 | 38.64 | 105.2 | 2018.03.28 |

| OFZ 26218 | 2031.09.17 | 42.38 | 165.1 | 2018.04.04 |

| OFZ 26221 | 2033.03.23 | 38.39 | 183.2 | 2018.04.11 |

| OFZ 24019 | 2019.10.16 | 45.52 | 22.3 | 2018.04.18 |

| OFZ 29008 | 2029.10.03 | 51.01 | 141.7 | 2018.04.18 |

| OFZ 26205 | 2021.04.14 | 37.9 | 40.2 | 2018.04.18 |

| OFZ 26222 | 2024.10.16 | 35.4 | 82.2 | 2018.04.25 |

| OFZ 26216 | 2019.05.15 | 33.41 | 17.3 | 2018.05.16 |

| OFZ 29009 | 2032.05.05 | 50.11 | 172.7 | 2018.05.23 |

| OFZ 29012 | 2022.11.16 | 44.63 | 59.3 | 2018.05.23 |

| OFZ 26214 | 2020.05.27 | 31.91 | 29.7 | 2018.05.30 |

| OFZ 25083 | 2021.12.15 | 48.33 | 48.3 | 2018.06.20 |

| OFZ 46011 | 2025.08.20 | 99.73 | 92.3 | 2018.08.29 |

| OFZ 46012 | 2029.09.05 | 83.63 | 140.8 | 2018.09.19 |

| OFZ 48001 | 2018.10.31 | 7.58 | 10.9 | 2018.10.31 |

Thus, the question “Which OFZ to buy on IIS” in the light of the strategy under consideration implies completely different answers than were true for the “Buy and Hold” strategy.

Stock market profits and taxation

- Dividends (dividend tax 13%).

- Coupon income from bonds (13% - including for municipal and OFZ bonds from 2021 - you can read here.)

- Change in the bond body rate. (13%). Example: We bought a bond for 950 rubles - sold it for 1000 rubles. Tax = (1000-950) * 13% = 6.5 rubles.

- Change in stock price. (13%). Example: We bought a Gazprom share for 150 rubles and sold it for 200 rubles. Tax (200-150)*13%= 6.5 rubles.

Important: tax refunds on dividends and coupons CANNOT be returned! You can return 13% only from points 3 and 4 - the profit received from the sale of shares or bonds!

How to find out your current yield

It is not enough to know the size of the coupon - the percentage of the face value paid by the issuer of the paper. It is necessary to take into account that the price differs from the face value and that when buying a bond, the accumulated coupon income will be withheld from you in favor of the seller - as compensation for the fact that he sold the paper without receiving the coupon, and it will go to you in full. The price of the bond without the cash flow is called the net price, and depending on it, the current yield at the maturity date is calculated (this is indicated in investment applications). For example, with a coupon rate of 7%, the current yield could be 4.3% if the bond is worth more than par. If a bond is trading below par, the yield will be higher than the coupon rate.

OFZs with a maturity of two to three years can be a good choice for novice investors to gain first experience

Coupon rates depend on the level of the key rate on the date of bond issue. When the key rate rises, coupons for new bond issues also rise, and vice versa, explains Alexandra Wald, an expert at the Association for the Development of Financial Literacy, a member of the Central Bank Expert Council for protecting the rights of retail investors.

Which type is more profitable

It turns out that the main question is as follows: can we get a Type B return of more than 52,000 rubles per year?

We remember that replenishments are no more than 1 million per year.

Then we get the following equation:

Profit from purchase and sale *13%>=52,000

Profit from purchase and sale >= 52,000/13%

Profit from purchase and sale >= 400,000 rubles

And our account is 1 million > = Profit on the account should be >= 400,000 / 1,000,000 >= 40%

And the average return on the Moscow Exchange index is about 12-17% per annum.

This index already takes into account the reinvestment of dividends. That is, the index must be beaten, and this is very difficult! This is why the benefits of Type A accounts attract so many more people.

But developments are already underway in the government to improve the investment attractiveness of Type B IIS.

More details here: https://iz.ru/972175/tatiana-bochkareva/nagruzili-portfel-porog-dlia-iis-budet-povyshen.

They plan to do for IIS type B (for income):

- Replenishment up to 2,500,000 rubles . (There are offers up to 5,000,000 rubles ). Then it will really be easier to show a profit of 400,000 ( only 8% per annum with 5 million deposits ).

- Possibility to withdraw partial funds early.

What is OFZ

OFZs are bonds issued by the state, namely the Ministry of Finance. The Russian Federation acts as a guarantor for these securities, so they are one of the most reliable. The chance of losing the invested money is extremely small - for this to happen, at a minimum, a default must occur.

When you buy government bonds, you are lending your money to the government. It, in turn, pays interest for this and buys back the securities at a certain price at the end of the term. The average yield on government debt securities is 4–6%.

Before getting acquainted with the types of OFZ, we suggest you understand the terms:

- The issuer is the government or private corporation that issued the bonds. The issuer of OFZ is the Russian Federation.

- A broker is an intermediary who is licensed to operate on the stock exchange. In simple words, it is an intermediary between the investor and the exchange. To invest in OFZs, you need to open a brokerage account.

- The face value is the cost of one bond, set by the issuer when it was issued. The par value of bonds issued by Russian issuers is usually 1,000 rubles. During circulation on the market, the price of OFZ may change.

- A coupon is a certain amount of interest that the bondholder receives for allowing his money to be used.

- The repayment period is the period for which you lend the funds. In simple terms, this is the time during which the government will use your money.

Common points for type A and type B

- You can top up only 1,000,000 rubles per year. It is not necessary to do this right away. The account term is calculated from the moment of opening.

- It cannot be closed earlier than after 3 years.

- If you close early, all benefits are canceled and you must return them, and be prepared to pay penalties.

- You can extend your IIS for a year in advance as much as you like.

- You can select only one type of deduction; when you change, the period is reset to zero.

- Only Russian rubles can be deposited into an IIS.

- There can only be ONE IIS per person. Therefore, they often open it on all relatives.

- You can transfer an account from one broker to another, maintaining the deadline. It's not free. Margin positions cannot be transferred!

- The broker withholds income tax upon account closure. (This is a big plus; you can reinvest this money).

To receive an IIS deduction, you need not only to top up your account, but also to buy financial instruments (stocks or bonds).

The account actually begins to mature from opening, not from replenishment. Therefore, people began to cheat, opening an IIS in the last month of the year (December), buying bonds for a very short period of time, only to formally fulfill the requirements for receiving a deduction.

But since such cases have become more frequent, the tax office has already begun to conduct explanatory conversations on this matter. (See Article 54.1 of the Tax Code of the Russian Federation, almost literally it sounds like this: “a taxpayer has the right to reduce the tax base if the purpose is not to offset the tax amount.”)

That is, if you are caught in the fact that you simply want to get a deduction without buying bonds or shares, or pretending that you are buying them, 52,000 rubles may bypass you.

Lifehack#5. Just top up your IIS or buy bonds?

In the fall, brokers and management companies, as a rule, begin to persistently remind their clients that it is important to have time to replenish an individual investment account before the end of the year . And this is reasonable, as it will give you the opportunity to submit documents for a tax deduction for 2018 already in the first quarter of 2019.

But if you opened an IIS not only to receive a bonus from the state while the money simply lies in the account for three years, but you want the funds deposited into the IIS to also work, that is, to bring stable passive income, then now is the best time It’s time not only to replenish the IIS, but also to buy highly reliable bonds at competitive prices with the deposited funds.

Due to high volatility, bond prices of most securities traded on the Russian market have seriously declined, and yields have increased . This is a good time to enter the market by purchasing securities from interesting issuers for your portfolio. Yango experts have selected for you several interesting ideas for buying bonds on IIS .

Source: Yango

Differences from a brokerage account

- There are no restrictions on the amount of deposits on a brokerage account. On IIS there is - 1,000,000 rubles / year .

- Personal income tax on transactions is immediately withheld in the brokerage account. On IIS - no.

- Some brokers do not have all tariffs available for IIS. (As a rule, these are premium tariffs, there are lower commissions - but also a subscription fee per month - up to 6,000 rubles).

- YOU CANNOT WITHDRAW MONEY EARLY TO IIS!

- There are no tax deductions for a brokerage account. On IIS - yes!

- There can be as many brokerage accounts as you like. IIS - only one!

- You cannot buy over-the-counter securities (on the OTC market) on an IIS!

The main difference is that you cannot withdraw money! Therefore, the investment period is at least 3 years.

Numbers

2,200,000 investors - individuals are registered today in Russia, according to the Moscow Exchange. In total, since the beginning of 2015, about 750 thousand new private investors have entered the market. 341 thousand people made at least one transaction on stock markets over the past six months.

400 000

individual investment accounts registered on the Moscow Exchange as of August 20, 2021. At the end of 2021, 302 thousand IIS , in 2021 - 195.2 thousand, in 2015 - 88.9 thousand IIS.

850,000,000,000 rub.

amounted to the trading volume on IIS for the period 2015 - 9M 2021.

Source: Moscow Exchange

Obviously, an individual investment account is a very interesting opportunity for private investors, which allows them not only to invest, but also to receive a bonus from the state . However, the devil is in the details. Here are some practical tips for using IIS that will help make investing through an individual investment account even more profitable .

How profitable is this compared to a bank deposit, and how does it work?

For example, let's take OFZ (Federal Loan Bonds), as the most reliable instrument with fixed payments, for comparison with a deposit.

| Basic introductions | |||||

| We decided to buy OFZ 25084 with a yield of 5.28% per annum for 3 years | |||||

| Bond yield per year = (Annual coupons / Face value) × 100% | |||||

| Bond yield per year = (26.43*2/1000)*100% = 5.28% per annum | |||||

| Coupon income on them is not subject to personal income tax |

PS: if you don’t know which bonds to buy, just buy OFZ (now it’s important to buy “short” bonds - for a year). Or put the money in trust.

| Of the year | Contribution | Profitability for the year | Deduction 1 year | Total: | Yield in % |

| 1 year | 400000 | 421120 | 52000 | 473120 | 18,28 |

| 2 year | 400000+473120 | 919221 | 52000 | 971221 | 11,23 |

| 3 year | 400000+971221 | 1443621 | 52000 | 1495621 | 9,07 |

| Total return for 3 years from an investment of 1,200,000 rubles | 24,63 | ||||

| Average annual yield | 8,21 | ||||

| *PS: Profitability decreases as the total investment body grows. | |||||

Let's compare with a deposit; in private banks you can now find a rate of 5%.

| Of the year | Contribution | Profitability for the year | Yield in % |

| 1 year | 400000 | 420000 | 5 |

| 2 year | 400000+420000 | 861000 | 5 |

| 3 year | 400000+861000 | 1324050 | 5 |

| Total return for 3 years from an investment of 1,200,000 rubles | 10,33 | ||

| Average annual yield | 3,44 | ||

Types with transcripts

There are several types of bonds with the OFZ ticker, starting in 1995.

The main typology of OFZ is as follows:

- Federal loan bonds with a variable coupon or OFZ-PK. These securities began to be issued in 1995, and after the default of 1998, the issue was suspended. The coupon was paid once every six months. The value of the coupon rate changed and was determined by the weighted average yield on government short-term bonds over the last 4 sessions (trading). At the end of 2014, the issue of these bonds was resumed.

- Federal loan bonds with constant income or OFZ-PD. They began issuing them in 1998. The coupon was paid once a year and was fixed for the entire circulation period.

- Federal fixed income bonds OFZ-FD. They began issuing them in 1999. They were issued to owners of state bonds and OFZ-PK, frozen in 1998. The circulation period is 4-5 years. The coupon was paid quarterly. The rate decreased annually from 30% in the first year to 10% at the end of the term.

- Federal loan bonds with OFZ-AD debt amortization. Periodic repayment of the principal amount of the debt.

- Federal loan bonds with indexed par value OFZ-IN. Issued since 2015. The nominal value of the bonds is indexed monthly for the coming month in accordance with the consumer price index for goods and services in the Russian Federation.

By coupon payment type

Based on the type of coupon payments, all OFZs can be divided into 4 groups:

- with constant coupon payments that do not change throughout the entire validity period of the security;

- with a variable when the issuer, i.e. the state can “link” the percentage of payments to inflation for a certain period;

- a zero-coupon bond, when no interest payments are made, but the price of placing the bonds among investors is significantly lower than the par value (usually by 20 or even 30%);

- with an indexed coupon, which is indexed, for example, by the amount of inflation, or when the coupon is “tied” to the price of oil.

At par

All OFZs, with rare exceptions, have a denomination of 1000 rubles. However, for example, for OFZ-N (folk) there is a minimum purchase volume (minimum lot) - it is 100 pieces or 30 thousand rubles.

The maximum purchase size of OFZ-N by one investor is also limited to 15 million rubles or 15,000 bonds “in one hand.”

Popular questions

Is it possible to use the deduction for income and contributions at the same time?

No.

Is it possible to use trust management so as not to choose assets yourself?

Yes. The benefits are the same. Statistics on trust management can be viewed here.

I am not a tax resident of the Russian Federation, can I claim a deduction?

No , you don’t pay 13% on income in the Russian Federation.

How to return tax if I am an individual entrepreneur?

This means that there must be personal income tax paid for other transactions - the sale of real estate, rental income. As well as personal income tax paid on profits from securities from a regular brokerage account (not IIS).

How to buy shares of American and Chinese companies using IIS?

To do this, the broker must have access to the St. Petersburg Stock Exchange . Check!

Is it possible to transfer securities from a brokerage account to an IIS?

It is forbidden.

Is it possible to transfer IIS from one broker to another? And how to do this if you end up with 2 accounts open at the same time!

Can . The simultaneous existence of old and new accounts with this procedure is allowed for 1 month during the transfer .

Can an account be inherited?

This option is not provided.

Is it possible to buy OFZ-N on an IIS?

It is forbidden.

At what age can you open an account?

From the age of 18. From 14 for a child you can open it with some brokers, but you can withdraw money only with the permission of the guardianship authorities. Check with your broker!

What is better - mutual fund or individual investment account?

Everywhere has its advantages. The advantages of a mutual fund are that they manage the account for you, but there is a management fee. Even if you end the year with negative profitability, you will have to pay a commission. On the other hand, few mutual funds manage to beat the index. It may be easier to buy an ETF for the Russian or American market.

Yes, but only Trust Management . But a conflict of interest is possible, you need to look at the purchased issuers of securities, and so that you have nothing to do with them.

What penalties will I have to pay for early account closure?

1/300 of the current refinancing rate for each day of delay.

Is the year counted from the moment of opening or the calendar year for receiving the deduction?

Calendar. You can open an account in December. Top it up with 400,000 rubles, buy securities with them, and receive a deduction in April of next year. (3 months tax check + 1 month crediting funds).

3 years have passed, what's next?

There are no time limits . You can keep your IIS open for 4-5-6-7 etc. years and receive deductions. But remember that in order to receive a deduction of 52,000 EVERY YEAR, you must REPLACE your account with 400,000 rubles . Therefore, many people close the account and open it again in order to deposit the money that was in the account.

How do I find out if I have an open IIS account?

The easiest way is to call the MOEX exchange, since it aggregates all the data from brokers.

How is the bill divided in a divorce?

Like all things acquired together, if the account was opened when you were already married. If before marriage, whoever contributed gets the money!

Where is the best place to open an account? (Broker Rating)

I recommend Tinkoff Investments. A little later I will write a whole article why. But like all brokers, DON’T JUST STORE YOUR FUNDS IN MONEY, STORE IN SECURITIES . Then they are stored in the depository, and you are not afraid of any bankruptcy of the servicing bank!

If you find it useful: statistics on the number of active accounts with leading operators on MOEX.

comparison table

I have summarized the main points in one table - to decipher it, you still need to look in more detail, since different brokers have different commission ranges, even within the same tariff, due to the daily turnover of securities, the amount of money in the account and trading operations .

I didn’t bother doing columns for the depository and opening an account, since these services are either free everywhere or 30-150 rubles/month. (VTB)

| Margin lending | ||||||

| Broker | Rate | Transaction commission % | Applications by phone | Currency transactions | Transferring cash positions | Transfer of a security |

| Sberbank | Independent | 0,018-0,060 | 150 rubles for 1 order | 0,02-0,2% | 17 | 15 |

| Investment | 0,3 | 150 rubles for 1 order | 0,20% | 17 | 15 | |

| VTB | Base | 0,0295-0,05 | 99-150 rubles for 1 order | 0,05% | 16,8 | 13 |

| Privilege | 0,02714-0,03776 | 99-150 rubles for 1 order | 0,05% | 16,8 | 13 | |

| Prime | 0,012-0,03455 | 99-150 rubles for 1 order | 0,05% | 16,8 | 13 | |

| Tinkoff | Investor | 0,3 | absent | 0,3 | 12-18 | 12-18 |

| Trader | 0,025-0,05 | absent | 0,025 | 12-19 | 12-19 | |

| Premium | 0,025 | absent | 0,025 | 12-20 | 12-20 | |

Advantages and disadvantages

"People's bonds", like other bonds, have their advantages compared to other types of investment instruments. These advantages include, first of all:

- Reliability, since the guarantor that the debt and interest on it will be paid on time and in full is the state, its state budget, and gold and foreign exchange reserves.

- Liquidity. OFZ is the most liquid security, since it can always be bought or sold. Moreover, this can be done not only where there is a free market - on the stock exchange, but to private or legal entities (in the form of a civil purchase/sale agreement).

- The interest income of OFZ with constant income is 7-8% per annum, despite its small value, it is still 10-20% higher than interest on bank deposits.

- Ease of ownership, use and disposal. It can be stored both in paper form, for example, in a safe deposit box, and electronically - in the form of digital records in the National Depository Center. You can manage your bond portfolio remotely using special programs and applications that every bank or broker operating in financial markets has.

In addition, OFZ as a financial asset can be inherited or given as a gift.

My personal choice of broker

At the moment I have 4 accounts open - in Sberbank, Tinkoff, Alfa-Bank, and now I have opened one in ATON for access to IB (they are a tax agent).

I can say that Tinkoff is simply several heads taller than everyone else. This all deserves a separate article, and I will write it separately.

But I can list the main advantages for me:

- Very convenient and functional applications - like a terminal, like an application!

- Very prompt technical support on all issues.

- There is no need to transfer currency by instructions to special foreign currency accounts and wait several days to complete the transaction.

- Your risk profile is determined, and dangerous securities (with a large debt load, probability of bankruptcy) are marked with a marker. And you are offered a choice of buying analogues!

- Analysts' forecasts for the security, order book, dividend history, main multiples. Convenient and usable price chart.

- Access to the St. Petersburg Exchange (Sberbank does not have it; in Alfa, even with a signed Form W-8BEN, dividends are withdrawn in double amount from foreign securities).

- All issues are resolved remotely - even signing the Qualified Investor Form and W-8BEN).

- Opportunity to participate in IPO at the Premium tariff.

- Now the platform is the social platform Pulse - where, apparently, they will soon enable auto-following, and you can still earn money from the fact that others copy your portfolio.

- The lowest rates on margin lending.

- Lowest transaction rates.

- Even on March 9 (Black Tuesday) - the terminal was working - it was slow, but it worked. Sberbank-investor did not work until lunch! You can read about it here.

What are the disadvantages?

Of course, Tinkoff is a less reliable bank than Sberbank. With a large loan portfolio, and even in such a difficult time. On the other hand, many remember Sberbank and deposits in 1991!

But this can be solved very simply - keep your money in papers! Then they are stored in a depository. It's much safer than money in the bank!

It is best to distribute funds between several brokers. But for convenience and for a beginner, I don’t know a better broker!

I don’t have VTB, but according to reviews from friends, Tinkoff is very much inferior. I can only attach a good video about this.

How to open an account with Tinkoff

I recommend the broker Tinkoff Investments. I wrote more about the choice in this article. Up to 25,000 rubles for completing lessons as a GIFT

Tinkoff-Investments

until April 31, 2021 for new accounts

Open an Account

You can open an account with a broker using this link.

Tinkoff Investments in the period from January 1, 2021 to March 31, 2021 (inclusive) gives up to 25,000 rubles as a gift when taking lessons! You can open an account using the link.

Tariffs with Sberbank

Can be found here.

Sberbank has only 2 tariffs available: Independent and Investment.

Detailed instructions for the Self-service tariff.

Detailed instructions on the Investment tariff.

Tariffs at VTB

There are 3 tariffs available at VTB - Basic, Privilege, Prime.

You can find it here.

Tariffs in Tinkov

Can be found here: https://www.tinkoff.ru/invest/tariffs/.

OFZ-PK

OFZ-PK are debt securities with a variable coupon (PC). The coupon of such bonds depends on the average value of RUONIA (“reference” rate). In simple words, this is the rate at which various Russian banks issue loans to each other in rubles. Usually it is close to the current key rate of the Central Bank.

RUONIA is an indicator that gives an idea of the state of the financial market. If the key rate, as well as rates on deposits and loans, increase, the value of RUONIA will also increase. The higher this indicator, the greater the profit on coupons that OFZ holders can expect.