Dividend policy

The current version was approved by the board of directors on December 12, 2016. Basic principles:

- transparency of payments;

- increasing the investment attractiveness of Transneft;

- taking into account the amount of future dividends when determining tariffs for services.

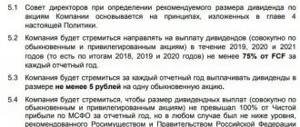

The basic level of payments to Transneft shareholders is 25% of net profit according to IFRS standards.

When establishing dividends, they evaluate:

- availability of sources of financing for investment projects in the medium term (K1);

- availability of sources for repayment of the principal debt in the medium term (K2);

- level of debt burden (K3).

25% of Transneft’s normalized consolidated profit is allocated for payments if K1 ≥ 2, K2 ≥ 0.33, K3 ≤ 1.5. 20% if K1 ≥ 1, K2 ≥ 0.17, K3 ≤ 2.5. 15% if K1 ≤ 1, K2 ≤ 0.17, K3 ≥ 2.5.

The total amount of payments to Transneft for shares of all types cannot exceed net profit, be less than 15% of normalized consolidated profit and 25% of net profit.

The distribution of Transneft dividends by type of shares is in accordance with the Charter. In 2021, adjustments have been made regarding the determination of payments for preferences (at least 10% of net profit).

Their size per preferred share may be lower than per ordinary share. In this regard, the largest holder of preferred shares, United Capital Partners, filed a lawsuit with the Moscow Arbitration Court demanding additional payment of dividends, which was rejected.

The Board of Directors of the Company approved the Dividend Policy of the Company (hereinafter also referred to as the Policy), according to which, when determining the amount of dividends on shares of all categories (types), the following principles are observed:

- transparency of the procedure for determining the amount of dividends;

- unconditional fulfillment of the main objectives of the Company’s activities, enshrined in the Charter, including the implementation of investment activities for the development of the production base, expansion, reconstruction and technical re-equipment of the main pipeline system;

- focus on increasing the investment attractiveness of the Company;

- ensuring financial stability and minimizing possible negative effects on the Company’s credit ratings;

- taking into account the amount of dividends on shares of all categories (types) when setting tariffs for oil transportation services through main pipelines established by the Federal Antimonopoly Service;

- the sufficiency of the funds available to the Company, received for the provision of services for the transportation of oil through main pipelines, taking into account the established tariff indexation indicators, to finance operating, investment and financial activities.

In accordance with the approved Policy, the basic level of dividend payments is 25% of the consolidated net profit of the reporting year, calculated in accordance with IFRS and normalized taking into account the share in the profit of affiliates and jointly controlled companies; income received from the revaluation of financial investments; positive balance of exchange rate differences and other irregular (one-time) non-cash components of net profit.

The distribution of the total amount of dividends between categories (types) of the Company's shares is made in accordance with the Company's Charter and the requirements of the legislation of the Russian Federation.

In April 2021, changes were registered to the Charter of Transneft PJSC regarding the determination of the amount of dividends on preferred shares. The new version establishes that 10% of the Company’s net profit at the end of the year is allocated for the payment of dividends on all preferred shares. In this case, the amount of dividend paid per preferred share cannot be less than the amount of dividend paid per one ordinary share.

Dividend history of Transneft PJSC over the past 7 years

| For the period, years | Amount of declared dividends on ordinary shares | Amount of declared dividends on preferred shares | Total amount of declared dividends, rub. | Payout ratio from the net profit of the reporting year according to RAS | Payout ratio from the net profit of the reporting year according to IFRS* | Date on which persons entitled to receive dividends were determined | Payment decision/decision date | ||

| total amount of dividends, rub. | per share, rub. | total amount of dividends, rub. | per share, rub. | ||||||

| For 2013 | 6 774 807 988,86 | 1 221,38 | 1 126 056 023,75 | 724,21 | 7 900 864 012,61 | 70,2 % | 5,0% | 20.07.2014 | AGM dated June 30, 2014 |

| For 2014 | 1 767 613 733,49 | 318,67 | 1 178 393 116,25 | 757,87 | 2 946 006 849,74 | 25,0 % | 5,0% | 20.07.2015 | AGM dated June 30, 2015 |

| For 2015 | 11 521 265 863,73 | 2 077,08 | 1 280 144 136,25 | 823,31 | 12 801 409 999,98 | 100,0 % | 8,9% | 20.07.2016 | AGM dated June 30, 2016 |

| For 2016 | 23 926 014 407,04 | 4 296,48 | 6 680 489 340,00 | 4 296,48 | 30 606 503 747,04 | 100,0 % | 18,3% | 20.07.2017 | AGM dated June 30, 2017 |

| For the first half of 2017 | 21 581 627 186,52 | 3 875,49 | 6 025 902 513,75 | 3 875,49 | 27 607 529 700,27 | 46,9 % | 50,0% | 19.09.2017 | EGM dated 08/30/2017 |

| For 2017 | 43 154 216 010,36 | 7 578,27 | 11 783 262 566,25 | 7 578,27 | 54 937 478 576,61 | 93,4% | 10.07.2018 | AGM dated June 30, 2018 | |

| For 2018 | 60 964 689 684,60 | 10 705,95 | 16 646 414 006,25 | 10 705,95 | 77 611 103 690,85 | 767,6% | 51,2% | 20.07.2019 | AGM dated June 30, 2019 |

| For 2019 | 66 125 301 309,60 | 11 612,20 | 18 055 519 475,00 | 11 612,20 | 84 180 820 784,60 | 110,2% | 53,1% | 20.10.2020 | AGM dated September 30, 2020 |

* Normalized net profit according to IFRS from 2021. Net profit is normalized for key non-cash components.

Dividend policy of Transneft PJSC

Hotline for dividend payments:

Tel. e-mail

Contact telephone number of the share capital and information disclosure service of the corporate governance department:

+7, ext. 1168, 2006, 1076

Investor Relations contact number (for institutional investors):

+7

All company dividends for the last 10 years

| For what year | Period | Last day of purchase | Registry closing date | Size per share | Dividend yield | Closing share price | Payment date |

| 2019 | 16 Oct 2020 | 20 Oct 2020 | 12M 2019 | 11 612,2 ₽ | 8,03% | 3 Nov 2020 | |

| 2018 | July 18, 2016 | July 20, 2016 | 12M 2015 | 823,31 ₽ | 0,51% | Aug 3, 2016 | |

| 2017 | 16 Jul 2015 | July 20, 2015 | 12M 2014 | 757,87 ₽ | 0,55% | Aug 3, 2015 | |

| 2016 | 16 Jul 2014 | July 20, 2014 | 12M 2013 | 724,21 ₽ | 0,96% | 1 Aug 2014 | |

| 2016 | May 30, 2013 | May 30, 2013 | 12M 2012 | 685,10 ₽ | 0,99% | June 13, 2013 | |

| 2015 | May 24, 2012 | May 24, 2012 | 12M 2011 | 716,58 ₽ | 1,6% | June 7, 2012 | |

| 2014 | May 24, 2011 | May 24, 2011 | 12M 2010 | 314,73 ₽ | 0,82% | June 7, 2011 | |

| 2013 | May 28, 2010 | May 28, 2010 | 12M 2009 | 250,39 ₽ | 0,96% | June 11, 2010 | |

| 2012 | May 28, 2009 | May 28, 2009 | 12M 2008 | 236,78 ₽ | 1,45% | June 11, 2009 | |

| 2011 | May 26, 2008 | May 26, 2008 | 12M 2007 | 258,45 ₽ | 0,76% | June 9, 2008 |

Dividends on shares of FESCO JSC in 2021 - size and date of closure of the register

Home → Dividends→ FESCO shares - forecast, payment history

A table with the complete history of dividends of the company DVMP JSC indicating the amount of payment, the date of closure of the register and the forecast:

| Payment, rub. | Registry closing date | Last day of purchase |

*Note 1: The Moscow Exchange operates on the T+2 trading system. This means that settlements for buying and selling shares occur within 2 business days. Therefore, to be included in the register of shareholders and receive dividends, you must be a shareholder 2 days before the cutoff.

*Note 2: Exact payout date varies by broker and issuer. The predicted closest date for the receipt of dividends to the brokerage account for the company DVMP JSC: January 14, 1970.

Total dividends of FESCO shares by year and changes in their size compared to the previous year:

| Year | Amount for the year, rub. | Change, % |

| Total = 0 |

The amount of dividends paid by FESCO for the entire period is 0 rubles.

Average amount for 3 years: 0 rubles, for 5 years: 0 rubles.

You can buy FESCO shares with minimal commissions from stock brokers: Finam and BCS. Free deposits and withdrawals. Online registration.

Brief information about the issuer Far Eastern Shipping Company

| Sector | Logistics |

| Issuer's full name | DV Shipping Company PJSC |

| Issuer's name is short | DVMP JSC |

| Ticker on the stock exchange | FESH |

| Number of shares in lot | 100 |

| Number of shares | 2 951 250 000 |

Other companies from the Logistics sector

| # | Company | Div. profitability for the year, % | The nearest registry closing date | Buy before |

| 1. | TransK JSC | 5,98% | 03.10.2021 | 29.09.2021 |

| 2. | NCSP JSC | 5,72% | 28.07.2021 | 26.07.2021 |

Calendar with upcoming and past dividend payments

| Immediate | Past | ||||

| Company Sector | Size, rub. | Registry closing date | Company Sector | Size, rub. | Registry closing date |

| RusAqua JSC Foodstuff | 5 | 27.05.2021 | MDMG-gdr Miscellaneous | 19 ✓ | 25.05.2021 |

| FGC UES JSC Energy | 0.016 | 29.05.2021 | TransK JSC Logistics | 403.88 ✓ | 24.05.2021 |

| SevSt-ao Metals and mining | 46.77 | 01.06.2021 | M.video Retail trade | 38 ✓ | 18.05.2021 |

| Tattel. JSC Telecoms | 0.0393 | 01.06.2021 | PIK JSC Construction | 22.51 ✓ | 17.05.2021 |

| SevSt-ao Metals and mining | 36.27 | 01.06.2021 | PIK JSC Construction | 22.92 ✓ | 17.05.2021 |

| GMKNorNik Metals and mining | 1021.2 | 01.06.2021 | Moscow Exchange Finance and Banking | 9.45 ✓ | 14.05.2021 |

| MOESK Energy | 0.0493 | 01.06.2021 | Sberbank Finance and Banking | 18.7 ✓ | 12.05.2021 |

View full calendar for 2021 »

7 Best Dividend Stocks for 2021

| # | Company | Sector | Dividend yield for the year, % | The nearest registry closing date | Buy before |

| 1. | Surgnfgz-p | Oil Gas | 16,84% | 20.07.2021 | 16.07.2021 |

| 2. | iMMTSB JSC | Miscellaneous | 15,24% | 09.06.2021 | 07.06.2021 |

| 3. | Unipro JSC | Energy | 15,08% | 22.06.2021 | 18.06.2021 |

| 4. | ALROSA JSC | Metals and mining | 14,99% | 04.07.2021 | 30.06.2021 |

| 5. | NLMK JSC | Metals and mining | 14,91% | 09.06.2021 | 07.06.2021 |

| 6. | Rusagro | Food | 11,85% | 18.09.2021 | 15.09.2021 |

| 7. | MMK | Metals and mining | 11,80% | 17.06.2021 | 15.06.2021 |

View the full company rating for 2021 »

Interesting read:

- How to buy shares for an ordinary person - a complete guide;

- How to trade on the stock exchange - step-by-step instructions;

- How to buy securities;

- How to create an investment portfolio - instructions and tips;

- How to live on dividends;

- How to buy gold for an individual;

- What is the average profit of stocks;

- Investing in shares - what you need to know;

← Return to main catalog

What dividends will be paid in 2021?

Transneft allocated 16.646 billion rubles for payments for 2021. (RUB 10,705.95 per share, yield 6.48%). In November 2019, they plan to pay 3,520.27 rubles. (2.29%), 07/20/2020 – 8185.38 rub. (5.32%).

Transneft's dividends in 2018 reached record values in absolute and percentage terms. Total dividends for 2019 will increase by 1.5 billion rubles. (according to the decision of the Government, they included half of the dividends received from subsidiaries in 2018).

The Transneft paradox

As experts note, the consulting company has high operational efficiency in comparison with foreign analogue companies. At the same time, it is also the cheapest company in the international oil transportation sector. Lenta.ru looked into what the paradox is and how to turn Transneft’s share into a blue chip.

The international consulting company KPMG, commissioned by Transneft PJSC, released last week a review of the main indicators of its activities and comparable foreign companies for 2018-2019. In addition to the Russian monopoly, the study included 44 companies from the USA and Canada, 11 European companies and seven companies from South America, Africa and the Asia-Pacific region. The analysis, which was carried out using more than 30 indicators, confirmed that among foreign pipeline companies there are no analogues comparable in the scale of Transneft’s pipeline activities in terms of key production indicators, KPMG notes. Thus, in 2018-2019, the Russian company’s cargo turnover was more than 1.2 trillion ton-kilometers, which is more than seven times higher than the company with the largest cargo turnover in the United States (Enbridge).

Photo: Sergey Guneev / RIA Novosti

Transneft shows consistently high results in terms of oil transportation volumes - 480 and 485 million in 2018 and 2021, respectively (with a median value of 81 million tons). In 2021, oil cargo turnover amounted to 1,217,397 million ton-kilometers. Transneft's oil transportation volume exceeds that of all compared companies. KPMG analysts explain this difference not only by the scale of the main pipeline network, but also by the significantly larger transportation distance (as of 2021 - 2,572 kilometers, which exceeded the median value by 3.3 times). At the same time, the revenue from the provision of oil transportation services by Transneft significantly exceeded the revenue of other companies in the sample. In 2021, it was $10.87 billion ($1.07 billion is the median). KPMG experts also noted that the revenue of the largest foreign company by this indicator last year was Enbridge Inc. almost 29 percent lower than the value of Transneft PJSC.

In the category “transport of petroleum products,” Transneft showed results close to the average for the final sample - 38 million tons in 2021, with a median of 48 million tons. At the same time, the company is also one of the largest companies in the world in terms of cargo turnover of petroleum products, exceeding that of most foreign analogues. Last year - 49,800 million ton-kilometers (which is almost 5.5 times more than the median). In terms of the length of oil product pipelines, Transneft also ranks first. For their transportation, the company's revenue also exceeded that of most other companies in the sample and amounted to $1.05 million, which is almost 2 times higher than the median value ($633 million).

From the KPMG review it follows that the weighted average tariff of Transneft in 2018-2019, calculated per 100 ton-kilometers of oil cargo turnover, is more than half the median value for comparable companies: $0.87 versus a median of $2.13. The situation is similar with the tariff for the transportation of petroleum products - its value for Transneft is more than 32.9 percent lower than the median among foreign companies: $2.12 versus $3.16.

Photo: Maxim Bogodvid / RIA Novosti

“The value of Transneft PJSC’s specific operating costs for oil transportation in 2021 is 3.2 times lower than the median value among foreign companies ($0.31 per 100 ton-kilometers versus the median of $1.01),” KPMG experts note. “In Transneft PJSC in 2018-2019, the “weight” of specific costs per 100 ton-kilometers of oil freight turnover, when compared with the level of the weighted average tariff, remained at 35-36 percent.”

Transneft's EBITDA margin in 2018-2019 was at a stable level and amounted to 44-46 percent, but was slightly below the median value (50 percent) for the compared companies. Analysts noted that Chevron Pipeline and ExxonMobil Pipeline recorded negative EBITDA in 2018-2019, which led to negative profitability for this indicator.

The depreciation rate of fixed assets of the Russian monopoly in 2019 (41 percent) was below the median value (46 percent), and the level of specific electricity consumption during oil transportation, one of the key items of operating expenses for all pipeline companies, was 25 percent below the median value. 4 percent. At the same time, labor productivity in physical terms turned out to be more than 2 times higher than the median value. Compared to 2021, this figure increased by 1.7 percent. The specific accident rate during transportation via main pipelines was also 17 times lower than the median value among comparable companies.

It is paradoxical that with such excellent operating indicators, Transneft shares perform worse than the market from year to year. For example, since the beginning of this year, the company’s capitalization has fallen by 18 percent against the backdrop of the Moscow Exchange index, which has grown by 3.8 percent.

Transneft remains the cheapest among all international companies in its profile. The estimated Business Value (EV) to EBITDA ratio for the global sector is on average 10.5, for Transneft this figure is only about 4, Transneft is on average 2.5 times cheaper than the average company in the sector.

The main reason is low dividends. The company pays below 50 percent of net profit under IFRS. At the end of 2021, 11,612.2 rubles per share were allocated for dividends (47 percent of profit). The current dividend yield is 7.9 percent, which is higher than rates on bank deposits and government bonds, and the high dividend yield is due to the low share price.

However, 50 percent of the profit today is not enough. The gold standard in the industry is to pay out 100 percent of net profits. Currently, Transneft has completed its main investment projects and its cash flow is growing. It is likely that in the future the state, as the main shareholder, will insist on raising dividends to market levels. According to Raiffeisenbank analyst Sergei Garamita, in the future, as an option to increase dividends, the possibility of paying out all free cash flow is not excluded. In this case, the dividend yield could reach double digits in 2022.

Photo: Ilya Pitalev / RIA Novosti

Another disadvantage of Transneft is that, unlike many other public companies, it does not conduct buybacks of its shares. Thus, the market lacks a stabilization mechanism in the event of sharp drawdowns on the stock exchange. Two years ago, in November 2018, a member of the board of directors of the oil transportation monopoly, CEO of the Russian Direct Investment Fund (RDIF), Kirill Dmitriev, announced a program for the redemption of Transneft preferred shares from the market. “Transneft management is taking a number of important steps to increase the company’s capitalization. We will have several more discussions about this program both on the strategy committee and on the board of directors. Therefore, I think all this can begin to be implemented next year,” he said. But in reality, the program has not yet been adopted. The same program should have provided for the development of a new management motivation system tied to the growth of dividends and the value of the company's preferred shares, which are considered undervalued in the market.

There was also talk about splitting shares, but it never came to fruition. The problem here is of a technical nature - one share of the company costs more than 140 thousand rubles, which means that this paper is not available to a wide range of individual investors, which reduces overall demand. A simple technical action of splitting shares with a ratio of 1:1000 could solve this problem and make shares available to the mass investor, especially since the market for private investment in shares is currently growing rapidly.

Investment analysts point to a significant undervaluation of the company's shares - for example, Sberbank has a fair price for a Transneft share of 250 thousand rubles (75 percent growth potential to the current market price). But in order for this potential to be realized, the company requires more active work with the stock market. Perhaps, after the KPMG study, the largest shareholders of Transneft (the state represented by the Federal Property Management Agency, NPF Gazfond Pension Savings, Closed Mutual Fund Gazprombank-Finansovy, Russian Direct Investment Fund, Russian-Chinese Investment Fund, Russian-Japanese Investment Fund, Sovereign Fund Saudi Arabia) will accelerate work on a program to increase dividends and capitalization of the company.

Fast news delivery - in the “Feed of the day” in Telegram

subscribe

Stock return

The yield of securities increases annually. A significant reduction in foreign currency debt could have a positive impact on Transneft's dividends. The loan from the China Development Bank ($4.6 billion) was repaid ahead of schedule. Experts consider the company's shares to be undervalued and predict an increase to 182.5 thousand rubles.

Payments can be negatively affected by:

- weak dynamics of pumping tariffs, which will not provide good financial results (indexation by 3.42%);

- formation of a reserve to cover damage on the Druzhba oil pipeline;

- possible splitting of shares (consent of foreign regulators required due to non-resident shareholders);

- consideration of the issue of share repurchase;

- large capital investments in 2019–2023 (RUB 1.3 trillion).

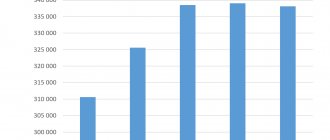

| Year | Profitability, % |

| 2010 | 0,96 % |

| 2011 | 0,82 % |

| 2012 | 1,60 % |

| 2013 | 0,99 % |

| 2014 | 0,96 % |

| 2015 | 0,55 % |

| 2016 | 0,50 % |

| 2017 | 4,59 % |

| 2018 | 4,49 % |

| 2019 | 6,48 % |

Monopoly proposes an increase in its tariffs

Transneft continues to argue with the FAS about the increase in oil transportation tariffs for 2021. The service believes that the increase in tariffs for monopolies should not exceed inflation, while Transneft proposes tariffs that are “significantly higher” taking into account the Ministry of Finance’s requirements for high dividends. In October, JSC Russian Railways also spoke out against the FAS methodology, for which a ten-year tariff was established according to the “inflation minus 0.1%” scheme.

Transneft and the FAS continue their dispute over the monopoly’s tariffs for 2019. As Anatoly Golomolzin, deputy head of the service, said on October 22, the company is asking to increase tariffs “significantly” above inflation. “Transneft has its own interests, expenses, investment plans, dividend obligations and many other factors. On the other hand, there are service users who have deviations in the opposite direction,” Interfax quotes the official.

The position of the FAS when calculating tariffs is to calculate their maximum level according to the “inflation minus” scheme. As Igor Demin, adviser to the head of Transneft, told Kommersant, when determining the tariff, the company proposes to take into account the Ministry of Finance’s requirement to allocate 50% of profits under IFRS to dividends, otherwise this may interfere with the company’s investment plans. Currently, Transneft’s dividend policy involves payments of 25% of profits according to IFRS, and, as the head of the monopoly Nikolai Tokarev noted in August, the company proposed focusing on this level.

Transneft can use up to 20 billion rubles to buyback its preferred shares. within three years

In 2021, the company paid out 58.2 billion rubles. (dividends for 2016 and the first half of last year). This year, 54.9 billion rubles were spent on dividends—28.6% of net profit under IFRS for 2021. But Transneft has not yet managed to achieve the desired increase in tariffs. She proposed indexing the tariff by 21% for 2021, but the FAS agreed only to 3.95%. The monopoly then drew attention to the fact that the Ministry of Finance’s requirement to allocate half of profits to dividends would lead to a deficit of 90 billion rubles. As a result, the company did not comply with the requirement. According to Kommersant’s interlocutor, Transneft again proposes to raise the tariff by about 20%; the company itself does not disclose the figures. A Kommersant source in the industry believes that the government is more likely to disagree with Transneft, avoiding conflicts with oil workers, for whom the tax burden will already increase from 2021.

Disputes over tariffs between monopolies and the Federal Antimonopoly Service intensified this fall. Since December 2021, a ten-year tariff of “inflation minus 0.1%” has been established for JSC Russian Railways; a similar mechanism is now being discussed for Transneft and Rosseti. As Kommersant reported on October 9, Russian Railways proposed dramatically changing the formula and taking into account not consumer inflation, but rising prices in industry. “We, like Russian Railways, cannot buy these goods in the store, because inflation for them in recent years has not fallen below 9%,” Transneft told Kommersant at the time.

Igor Artemyev, head of the FAS, in an interview with Kommersant on September 25

No super-inflationary tariffs can be approved, including for Transneft

According to the general director of Infoline-Analytics, Mikhail Burmistrov, in order to maintain investment plans and dividends of 50% of profits under IFRS, the increase in Transneft tariffs should be at the level of 17–18% in 2021. As the analyst notes, the monopoly has already reduced capital investments, which in the first half of the year amounted to 34.7 billion rubles, while in 2021 - 143 billion rubles, including due to an increase in dividends. In a presentation for investors, Transneft indicated that it was ready to reduce costs by 120 billion rubles. in 2018–2023, as the main projects are completed - the expansion of the ESPO and Kuyumba-Taishet oil pipelines, the construction of the South oil product pipeline system.

Sergei Garamita from Raiffeisenbank notes that dividends at the annual level for 2021 can be covered by free cash flow for 2021 due to a drop in CAPEX. “To increase payments to 50% of profits under IFRS, an additional indexation of 6.5–7% may be required,” he notes. “The company can use funds in accounts and short-term deposits (more than 420 billion rubles at the end of the first half of the year).”

Dmitry Kozlov

How to buy shares and receive dividends

Individuals cannot independently buy preferred shares of Transneft on the Moscow Exchange; access is provided through a broker (exchange commission and brokerage percentage should be taken into account).

Purchasing securities from legal entities or private owners is labor-intensive and time-consuming. The price may differ significantly from actual market quotes. Transneft does not practice direct sales plans.

Best brokers

List of licensed brokers that are trustworthy:

Reliable Russian brokers

| Name | Rating | pros | Minuses |

| Finam | 8/10 | The most reliable | Commissions |

| Opening | 7/10 | Low commissions | Imposing services |

| BKS | 7/10 | The most technologically advanced | Imposing services |

| Kit-Finance | 6.5/10 | Low commissions | Outdated software and user interface |

Warning about Forex and BO

Expert opinion

Vladimir Silchenko

Private investor, stock market expert and author of the Capitalist blog

Ask a Question

Forex and binary options are not related to real exchange trading and do not involve transactions with real assets. It is advisable to abandon dubious methods of earning money, similar to gambling, in order to avoid losing the invested money.

Transneft taxes do not depend on the place of registration of divisions

Gennady Stepanov, January 29, 2021, 13:16 - REGNUM Tomsk media are competing to see who will scare the population more with the reorganization of Transneft Central Siberia JSC. This subsidiary is disbanding the Tomsk division, the functions of which will be distributed among neighboring divisions of the company.

Ivan Shilov © IA REGNUM

Kommersant-Sibir, citing the head of the finance department Alexander Fedenev, reports that as a result of the departure of Transneft, the region’s budget will receive a shortfall of 400-500 million rubles annually. RIA-Tomsk increased its losses to 800 million rubles. As usual, “Moskovsky Komsomolets - Tomsk” outdid everyone, giving news under the headline “The Tomsk region will lose more than 3 billion rubles in taxes from the departure of Transneft”! True, somewhere in the depths of the text, journalists admit that these are “estimated” (!) losses for “five years” (!), but who now reads anything beyond the headline?

It’s just like the old Armenian joke: “Is it true that Professor Ayvazyan won a million rubles in the lottery? True, but not a professor, but a student, and not a million, but a hundred rubles, and not a lottery, but a preference, and didn’t win, but lost.”

Tomsk journalists have forgotten how to write the truth; apparently, there has been no need for a long time. We help.

"Transneft - Central Siberia", like the rest of its subsidiaries, constitute the "Consolidated Group of Taxpayers" (KGN, see Tax Code Article 25.1). One of the features of this form of tax payment is the independence of the distribution of income tax by region from the place where the CTG participants are registered. The income tax of all participants of the Group of Companies is summed up, and its distribution among the constituent entities of the Russian Federation is made based on the average number of employees and the residual value of fixed assets of the structural unit of the Group of Companies in the region. Since oil pumping and other production facilities, formally transferred to the balance sheet of other divisions of Transneft Western Siberia JSC, will actually continue to operate in the Tomsk region and the number of employees at these facilities will not change, the distribution of income tax will not change. By the way, when in 2012 the largest companies in the country switched to KGN, Moscow and St. Petersburg significantly lost in taxes.

JSC "Transneft - Central Siberia"

Transneft.ru

The main regional taxes are property tax and personal income tax. In 2021, Transneft will pay them in the same amount as the year before, they will even grow a little. The income tax will indeed become lower, but its reduction has nothing to do with the reorganization of Transneft-Central Siberia.

The reduction in income tax to the budget of the Tomsk region in 2021 is associated with a general decrease in profit for the Transneft group. This is due to several reasons. One of the most significant is the limitation of tariffs for pumping oil and petroleum products (the only source of income, which is adhered to by the regulator: the Federal Antimonopoly Service (FAS) of Russia. FAS, as a matter of principle, does not accept any arguments from Transneft about the real level of inflation for the pipes and equipment purchased by the company, stubbornly equating the rise in prices for iron pipes with the rise in the cost of potatoes and cheap varieties of bread, inflation for which is two times lower.As a result, Transneft's expenses are growing much faster than its income.

The second reason: in accordance with the dividend policy of the Russian government in relation to companies with state participation, Transneft PJSC must now annually allocate up to 50% of its consolidated net profit according to IFRS to pay dividends. This also affects the profits of subsidiaries that pay taxes to the budgets of the constituent entities of the Russian Federation. The actual figures of tax payments to the budget of the Tomsk region from organizations of the Transneft system are shown in the table.

Tax payments by Transneft system organizations to the budget of the Tomsk region for the period 2019-2021. in thousand rubles

| Tax name | 2019(fact) | 2020(plan) | 2021(forecast) |

| Income tax | 819 706 | 396 056 | 758 410 |

| Property tax | 462 051 | 480 106 | 550 839 |

| Personal income tax | 550 697 | 617 447 | 630 707 |

| Other taxes | 8 197 | 8 435 | 8 518 |

| Total | 1 840 652 | 1 502 044 | 1 948 474 |

It can be seen that the only serious failure in taxes is the reduction in income tax payments in 2021 relative to last year. But in 2021, the company plans to return to the previous amount of this tax, and the total amount of taxes will increase significantly.

The question arises: why do regional government officials underestimate budget revenues if the money will arrive anyway? And in order to independently distribute the “unexpectedly arising” surplus, without the approval of the regional Duma and informing the governor. However, this is also the case at the federal level, in the Ministry of Finance, when they prepare the country’s annual budget, setting the most pessimistic expectations for both the cost of oil and the ruble exchange rate. This, of course, is not corruption, but such facts involuntarily set one up for certain thoughts.

Transneft may leave its shareholders without money

“Attracting investment, increasing purchasing power, increasing the efficiency of the economy and management” - this is how President Vladimir Putin described the essence of the anti-crisis plan during the April “direct line” with Russians. Under sanctions, the national economy is desperately short of money, so the government is considering the privatization of a number of the largest state-owned companies.

Subject: Offshores, Corruption

In response, the management of the Transneft corporation seems to be doing everything to make investors forget the way to Russia and not interfere with the implementation of established schemes.

A big scandal is breaking out around Transneft's payment of dividends for 2015 to its shareholders. However, it would be more accurate to say otherwise - it seems that the management of Transneft is actively dragging the state into the scandal, covering up its not very nice actions with its name, as a result of which the budget and minority shareholders risk being left with nothing.

photo: Yuri Mashkov/TASS

To whom we owe - we forgive

“We have one shareholder – the state. We don’t have minority shareholders... We have privileged [shareholders]. But privileged, you know, this is such a conventional name. These are not actually shareholders ...,” Transneft President Nikolai Tokarev said bluntly in December 2014. If the head of some foreign corporation had publicly blurted out something like that, the very next day he would have been standing in line at the labor exchange. After all, in the civilized world, a shareholder is a sacred figure; he invests his money in the company. But Nikolai Tokarev did not study at financial universities.

After all, it is only formally that Transneft belongs to the state - 21.9% of the shares are in the hands of private holders. However, they own only preferred shares: they do not give the owners the right to participate in voting, but they guarantee the receipt of dividends, the amount of which, according to the law, cannot be lower than payments on ordinary shares. And even if, for some reason, a disproportion arises and preferred shares account for a smaller amount, then in this case an additional payment should follow, equalizing the amount of dividends. For many years, Transneft has regularly observed this rule. However, last week the Vedomosti newspaper reported that Transneft will use 100% of the company’s net profit under RAS to pay dividends for 2015, but in this case the owners of preferred shares will only get 10%. This means that payments per preferred share may be 2.5 times less than per ordinary share. That is, Transneft actually decided to screw over its minority investors.

Surely everyone here will have a question: how can this be? Back in 1998, the charter of Transneft JSC was approved by a decree of the Russian government. It contained clause number 12.3, which literally read: “Owners of preferred shares have the right to receive an annual fixed dividend in the amount of 10%... Moreover, if the dividend paid per ordinary share exceeds the dividend payable on a preferred share, then the amount the dividend on a preferred share must be increased to the amount of the dividend paid on an ordinary share" (“surcharge clause”).

On this topic

1685

The flight attendant, who found herself without money due to the pandemic, showed off her new job in the store

A flight attendant who resigned from Air New Zealand showed her new place of work in a video. Due to a lack of livelihood, the girl had to get a job in a warehouse in a supermarket.

However, a year later, this provision disappeared from the charter and another one appeared in its place: “The amount of the annual dividend payable on each preferred share is 50 kopecks” (in accordance with the court decision, 50% of the value of the preferred share with a par value of 1 ruble). That is, there was a clear infringement of the interests of investors.

This was done, as the court later confirmed, illegally - without taking into account the 2/3 votes of the owners of preferred shares necessary to make such a decision. By the way, at the same time, with the same changes, Transneft completely deprived the latter of their voting rights. As a result, one of the minority shareholders was outraged and went to court. In 2001, the Moscow Arbitration Court ruled that the changes made were considered invalid. However, the whole point is that the minority shareholder only challenged the reduction in the amount of payment per preferred share by more than 200 times - from 10% of net profit to 50 kopecks, and the additional payment of dividends did not bother him, since at that time the rights of minority shareholders in terms of additional payments on dividends were not violated (dividends to owners of ordinary shares for 1998 were not paid at all). Therefore, the trial concerned exclusively the amount of dividends, while it is obvious from the court decision that all changes to the charter were illegal. Nevertheless, Transneft seemed to “forget” to return the “additional payment clause” to the charter.

To be fair, it is worth noting that for quite a long time Transneft still tried not to become impudent to the limit and paid minority shareholders, albeit small dividends, but in legal proportions (i.e., dividends on ordinary shares did not exceed dividends on preferred shares). However, this was the case until 2014, when the company unexpectedly announced: the owner of ordinary securities, that is, the state, will receive 1,221 rubles per share in the form of dividends for 2013, and holders of preferred shares - 724.21 rubles each. A big scandal broke out, minority shareholders even sent a letter to the chairman of the government, Dmitry Medvedev. As a result, at the end of 2014, fairness was restored, including the status quo in the ratio of payments on preferred and ordinary shares. After this, apparently trying to save the company’s image, Transneft’s first vice-president Maxim Grishanin vowed to develop a new dividend policy and not to infringe upon the owners of preferred shares (a message about this can be found on the company’s website). But, as they say, the legend is fresh. And now, apparently, they decided to rob the shareholders again. However, investors' patience seems to have run out. One of the main minority shareholders of Transneft, the company UCP, went to court. She demands that Transneft pay an additional 97.2 million rubles in dividends for 2013 that were not received. Only in this way, according to the investor, will it be possible to put an end to the described lawlessness.

Who can live well at Transneft?

In this regard, someone may have a question: maybe Transneft is doing everything right? Indeed, in a situation where the state does not have enough money, transferring the bulk of the dividends to the state would be the right decision. Alas, there are great doubts that the management of Transneft is thinking about the interests of the state in this situation.

Independent economists have long been intrigued by the policy of Transneft’s bosses, according to which the bulk of the company’s profits for some reason end up in its subsidiaries. As the reporting figures show, only 4–20% of the profit of the entire group is left to its parent company. In 2013, Transneft’s profit under IFRS was 14 times (!) higher than net profit under RAS. And at the end of 2014 – 5 times. As a result, the state, as the main shareholder, receives only 3% of the total profit of the Transneft group. Although back in 2014, Vladimir Putin noted: they say, we have agreed on a general rule for paying dividends for state-owned companies - at least 25% of net profit. And what do we see in the end? It turns out that Transneft is deceiving the president and the state? There is nothing to say about minority shareholders...

It’s interesting what Transneft spends its money on. So, before the collapse of the ruble exchange rate, Nikolai Tokarev, apparently, decided to insure the risks against the fall of the exchange rate - not just the ruble, but... the dollar. As a result, after the US currency skyrocketed, Transneft lost 76 billion rubles, which is almost half of the company’s annual net profit. What can I say... Almost 28 billion rubles were stuck in the accounts of Vneshprombank, which had lost its license, and the collapse of Interkommerts Bank cost the company another 6.6 billion rubles. Their problems did not arise overnight - why did Transneft turn a blind eye to this?

Or another interesting nuance. During 2007–2014, Transneft allocated 33 billion rubles to charity, which is approximately 1.5 times more than the dividends paid by the company during the same period. The question arises: is Transneft a charitable foundation? Or is charity being used only as a front to disguise the write-off of money?

Against this background, the news that in 2012-2013 for the needs of Transneft

50 American Robinson helicopters were purchased for $25 million - justifying this by the need to fly over pipelines will seem like a trifle. However, it later became clear that the use of such helicopters is prohibited. Well, okay, the monopolist has a lot of money... But why then did the Accounts Chamber find out that the company’s pipeline construction rates are 23% lower than planned?

But the management of Transneft, apparently, feels good. So, last week the media reported that “the luxurious Villa Carolina (in Croatia) is at the disposal of the daughter and son-in-law of Transneft President Maya and Andrei Bolotov.”

“It’s amazing, with such happiness - and in freedom,” Ostap Bender used to say. Maybe the competent authorities should still take a closer look at what is happening at Transneft?

BY THE WAY

A liberal attitude towards its minority shareholders seems to be Transneft's policy. In October last year, she also applied to arbitration with a demand to recognize preferred shares as voting due to incomplete payment of dividends. According to the plaintiffs, the monopolist deliberately understated its profits, passing them on to its subsidiaries. As a result, the court decided to involve the Russian Federation as a co-defendant. I wonder how the highest echelons of power feel about the fact that the company’s management is actually exposing the entire state by its actions?

But will maintain the level of tariffs

After a three-month discussion, the government made a fundamental decision on the size of Transneft’s dividends: the company must pay the 50% of net profit according to IFRS recommended by the Ministry of Finance. The monopoly itself offered the option of installment payments for three years, taking into account the drop in its cargo turnover by 20% due to the OPEC+ deal to reduce production. The government must resolve the issue by the end of the year, but Kommersant’s sources claim that it has been removed from the agenda taking into account the position on dividends and increased oil prices.

The Ministry of Energy and Transneft, on behalf of the government, must once again study the issue of the possibility of reducing tariffs for oil pumping by the end of the year, Deputy Prime Minister Yuri Borisov said at the Tyumen Oil and Gas Forum. In May, Igor Sechin, the head of the largest consumer of the pipeline monopoly, Rosneft, asked to reduce the cost by 2.5 times. Then he referred to the record drop in oil prices, against the backdrop of which the producer’s transportation costs increased by a third relative to the final cost of oil. In mid-June, President Vladimir Putin instructed to consider the option of introducing a special tariff for Transneft and Russian Railways for the duration of the OPEC+ deal, but the issue has not yet been resolved.

Due to uncertainty with Transneft's tariffs, on which the bulk of the company's income depends, the government has not yet sent its board of directors a directive to vote on the level of dividends, which, at the request of the Ministry of Finance, should be 50% of net profit under IFRS.

On June 19, the monopoly itself proposed allowing it to pay the 81 billion rubles due to the state. in installments: about half the amount immediately, and the rest over three years. The board of directors was unable to make a final decision due to the lack of a directive, which the company is still awaiting, to conduct an absentee vote.

The deadline for this is September 30, before which the government allowed state-owned companies to approve dividends amid the pandemic. After this, the powers of the board of directors will expire, and there will be no one to recommend the level of payments to shareholders, says a Kommersant source familiar with the situation.

According to another Kommersant source in the government, the fundamental decision regarding Transneft dividends has already been made: there is no talk of any installment payments, so the company will have to pay the entire 50% of its profits, although the directive itself has not yet been formalized. He notes that after rumors about this decision appeared, quotes for preferred shares of the pipeline monopoly grew over the last week “against the market” (peak on September 17 at the level of 145.1 thousand rubles).

Kommersant's sources claim that the issue of reduction can also be considered closed, despite the formal instruction to continue its consideration.

Yuri Borisov himself (current Urals quotes are $41.5 per barrel). The Ministry of Energy, Kommersant’s interlocutors explain, has always been against any change in the system for calculating pumping prices, pointing out that this would unbalance adjacent markets, for example, tariffs in the electricity sector.

In the government, as Kommersant’s interlocutors reported, only the Ministry of Economy took the side of Rosneft, which considered that the pipeline monopoly’s profitability was too high, and proposed reducing this figure by about five times by 2025 - to 5% (see Kommersant ” dated July 17). The option of a floating tariff tied to the price of oil was also discussed.

Transneft itself emphasized that the decline in oil prices, which peaked in April (the price of Urals was at $16 per barrel at an exchange rate of 75 rubles/$), was short-term, and the drop indicated by Rosneft was calculated only for one of the export directions - via Primorsk. At the same time, according to Transneft’s calculations, if its tariffs are reduced to the 2008 level, it will lose 40% of revenue and will have a funds deficit of 130 billion rubles for 2021, and 227 billion rubles for 2021. and for 2022 - 304 billion rubles, so it will not be able to service loans and the investment program. The company declined to comment on Thursday.

Experts are confident that if the principle of calculating Transneft’s tariffs “inflation minus” is maintained, the company will be able to pay all 50% of its net profit to the state.

Sergei Garamita from Raiffeisenbank believes that if interest income (in addition to interest expenses) is taken into account in last year’s free cash flow, then only due to this, dividends could be higher than the level recommended by the Ministry of Finance, exceeding 100 billion rubles. According to him, the company has enough liquid funds if necessary, and a decrease in pumping this year will affect dividends for 2021 through profits, so there is no point in lowering the coefficient, and dividends for 2021 will in any case be paid from money already earned .

Olga Mordyushenko