What are Eurobonds

To begin with, I will explain what Eurobonds are in simple words, literally for dummies. This is the same bond issued by a Russian issuer, but only denominated in foreign currency. For example, Eurobonds in euros, dollars, yuan, Swiss francs and pounds sterling are popular on the Russian market.

There is no need to look at the prefix “Euro” - this does not mean that the security is necessarily issued in euros. It’s just that the first Eurobonds were issued for circulation on the stock exchanges of old Europe, hence their name. Now they are issued on various exchanges, including American, Asian, even African - but they are traditionally called “Eurobonds”.

The issuer of Eurobonds can be:

- the state (more precisely, the Ministry of Finance);

- banks - for example, Sberbank, VEB, VTB, Alfa-Bank;

- private enterprises - Gazprom, TMK, Polyus, BKS, etc.

The issue of Eurobonds is organized, as a rule, on foreign exchanges - in fact, that is why they are issued in foreign currency. But the Moscow Exchange provides a whole range of corporate Eurobonds from Russian companies and banks, as well as from the Ministry of Finance. So, if you wish, you can buy these securities in Russia.

So, let's summarize. Eurobonds are debt securities issued by governments or companies in foreign currencies, usually on foreign exchanges. Typically, this tool is aimed at investors from abroad.

FAQ

Is it possible to buy Eurobonds on an IIS account?

Even necessary. For more or less significant amounts, it is better to use type B , which provides exemption from personal income tax on profits received through trading operations. You top up your account in rubles, then RUB is converted into foreign currency, and Eurobonds are purchased with it. They are then sold or redeemed and USD or EUR are converted into RUB and withdrawn back to the bank account.

How does taxation work for individuals?

For state Eurobonds, personal income tax is paid only if income is generated due to exchange rate differences. For corporate – and from coupon income. You can get a tax deduction if you hold securities for more than 3 years.

I have a sufficient amount in EUR, I want to buy Eurobonds denominated in EUR, how can I avoid conversions?

Open a foreign currency account at a bank, then transfer funds to a brokerage account (opened in the same currency). With this scheme there will be no unnecessary conversions.

Will there be conversion if the money is in euros, but I buy bonds in dollars?

If the currencies are different, then you cannot do without conversion.

How do Eurobonds work?

Why do they issue Eurobonds? For the same thing as regular bonds: a company (or state) borrows on the foreign market to replenish its capital.

Eurobonds are placed on the stock exchange, and they can be purchased by any trading participants - individuals, legal entities, funds, other states, etc.

Investors who purchased Eurobonds are entitled to receive a coupon payment. Its size is specified in advance in a special document - a prospectus. There are coupons:

- fixed – the price is determined in advance;

- variables – the company can change the price at its discretion;

- floating - the coupon size is tied to some indicator, for example, the consumer price index (inflation), the key rate of the Central Bank of the Russian Federation, the RUONIA indicator, etc.

After the Eurobond's circulation period expires, the issuer repays it - pays the last holder the face value of the bond. In this case, the purchase price does not matter - repayment is still made at par.

Calculation of purchases using an example

When calculating profitability, you need to take into account that profit must be calculated in rubles. The exchange rate of the national currency changes, it may become cheaper relative to the dollar or euro, then the profit of the bond holder increases.

For example, if the exchange rate was 65 rubles, and the security was purchased for $1,000, then the investor paid 65,000 rubles for it. When the settlement date arrived, he received $1,000 back, but the exchange rate became 68 rubles, so he earned 68,000 rubles.

There is another situation when, if the value of the dollar decreases, the holder faces a loss in terms of receiving the face value. But when calculating profitability, coupon payments must also be taken into account, then the figure may be different.

Types of Eurobonds

Eurobonds can be classified according to various criteria. For example, by coupon income - I outlined this classification above. Other options would be:

1) by deadline:

- short-term – up to 1 year;

- medium-term – up to 3 years;

- long-term – from 3 years;

- “Sleeping Beauties” – 100 years;

- perpetual – they are also perpetual Eurobonds (there is no maturity date, and the coupon is paid until the winner, i.e. while the company exists);

2) by type of issuer:

- government (for example, Russian Eurobonds);

- municipal (but we have almost none);

- Eurobonds of Russian banks;

- corporate;

3) by type of payment:

- coupons are those for which the issuer pays;

- discount – the issuer does not pay for them, but they are issued at a price below par (with a discount);

4) by method of repayment:

- with a put option - the issuer can buy back such a bond under the offer within a specified period;

- with a put option – the Eurobond holder can present it for redemption;

- with both types of options;

- without the right of early withdrawal (i.e. the Eurobond is repaid only on the offer date);

And here’s another interesting article: Where to invest small money so that it makes money: full review

5) by type of buyer:

- for qualified investors;

- for everyone, including private individuals;

6) according to geographical principle:

- Russian;

- European (European companies);

- USA;

- other countries.

There are other types of Eurobonds, but we won’t bother too much. We will leave more exotic options to funds and professional investors.

Investor reviews

Many private investors are interested in the Eurobond market. They see it as protection against fluctuations in the ruble exchange rate, inflation and financial crises. Dollar bonds and euro securities allow you to receive passive income.

Oleg, 37 years old, Moscow

I became interested in Eurobonds after 2021, when turmoil in the world of finance began again. I decided that I wanted to protect my savings, so I bought IOUs from leading companies.

Marina, 42 years old, Novosibirsk

I can't afford to buy Eurobonds, so I chose to invest in ETFs. I like the funds because you can buy shares with every salary.

Mikhail, 52 years old, St. Petersburg

I have a business, and I use part of my income to purchase Eurobonds. I think this is a good alternative to retirement. I like investing in them because now I don’t have to fear the collapse of the ruble.

How to make money on Eurobonds

An individual can earn Eurobonds in three ways:

- just buy and hold by receiving a coupon;

- buy a bond below par and hold it until maturity;

- speculate - buy low and sell high / make short sales.

Usually they combine the first two ways of earning money - they try to buy an income-bearing Eurobond at a price lower than its face value in order to receive more upon repayment and at the same time earn money on coupons.

However, for a number of reasons, the price of the bond may be higher than the face value, so the strategy may not work - I will explain why this happens below.

And in general, the market price of Eurobonds rarely differs greatly from the nominal price, so the main way to earn money is still receiving payments, i.e. Eurobond coupons. If the difference in prices is strong, it means that something is wrong with the issuer, and such a bond should not be purchased without a thorough analysis of the situation.

Recommendations for private investors – individuals. persons

Purchasing Eurobonds by individuals in Russia does not cause any difficulties, but before choosing bonds, you need to conduct a market analysis or trust specialists.

Recommendation! Pay attention to securities of Russian companies.

Advantages of domestic companies:

- Profitability is higher than that of foreign issuers.

- There is no need to transfer funds for trading and register accounts.

- Availability of information about issuers.

Companies that deserve attention from an investment point of view are Rosneft, Gazprom, Novatek.

In the financial sector, these are Sberbank, Promsvyazbank, Alfa Bank.

Eurobond yield

Exactly how much coupon income the issuer pays on a Eurobond depends only on him. The larger and “state-owned” the company, the smaller the coupon it offers. The highest profitability is for companies with a low credit rating - you can earn more from them, but the potential losses are also high.

For example, the VimpelCom company offers the VimpelCom Holdings-2021 Eurobond with a yield of 3.95% per annum. Alrosa - 2024-euro issue with maturity in 2024 with a coupon of 4.65% (however, this particular issue is intended for qualified investors).

On average, the income on Eurobonds is about 3-5% per year - I mean, on high-quality securities and with a good rating.

Anything more expensive carries potential risks. Even more generous non-state Alfa Bank. He pays as much as 8% per annum on the Alfa-Bank-24-00-euro issue, and these are perpetual bonds.

And the Moscow Credit Bank offers as much as 16.5% on the MoskovKredBank-05-2025-ev paper - as you understand, this is an absolutely crazy yield, especially for a foreign currency Eurobond.

In general, Eurobonds turn out to be about 2-2.5 times more profitable than a foreign currency deposit. And sometimes even at 3-4.

But we are only talking about coupon yield. The yield to maturity may be different. The fact is that if the demand for a bond increases, then its selling price also increases. As a result, the yield to maturity decreases.

For example, a Eurobond costs $1,000 and its coupon yield is 10% per annum. At the same time, the key rate of the Central Bank of the Russian Federation is 6%. The bond becomes more profitable than deposits, and it is actively bought. As a result, its market price becomes equal to $1,040 - and the yield to maturity is equal to the key rate.

The example is, of course, conditional, but we just need you to understand the main idea. If the demand for a bond falls, then prices also decrease, and the yield of the bond increases. I wrote about this in detail in an article about how to determine the yield of a bond.

Summary

Eurobonds cannot be considered a solution to all investor problems. Risks of issuer default remain, and changes in exchange rates can also greatly affect profitability. But Eurobonds are the only way to get the maximum return in foreign currency . According to this criterion, bank deposits are inferior by more than 2 times. Considering the behavior of the ruble in recent years, I consider it justified to convert at least part of the funds into foreign currency and invest in Eurobonds. There is a high probability that in the future you will make a profit both due to coupons and due to the next weakening of the ruble. Moreover, for this you do not need to be a qualified investor or have a multimillion-dollar capital.

For beginners, I recommend reading the post on how to buy shares for an individual in Russia. You will work with Eurobonds according to the same scheme. In the comments, be sure to share your experience of working with Eurobonds. If something remains unclear, ask questions - I will try to answer everyone. And don’t forget to subscribe to blog updates, so you don’t miss the release of new materials. With this I say goodbye to you. All the best and good luck in investing!

If you find an error in the text, please select a piece of text and press Ctrl+Enter. Thanks for helping my blog get better!

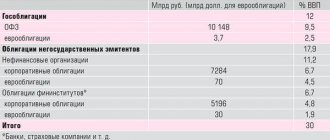

How much do Eurobonds cost?

Now a little bit of ointment in the ointment. The fact is that the cost of Eurobonds is quite high, and they are not available to many investors. The price range is wide - but the minimum is 1000 units of currency. For example, the Novatek-22 bond costs $1,000, VEB-23 EUR – 1,000 euros.

But that is not all. Eurobonds of Russian issuers are sold not one at a time, but in lots. One lot usually contains 200 Eurobonds. So it turns out that the minimum amount for purchase is 200 thousand units of currency.

Such a high entry barrier sharply limits the number of possible buyers. Fortunately, some brokers allow you to enter the market with a fractional number of lots - for example, 0.01. And if there are 200 Eurobonds worth $1,000 in one lot, then in this case you will have to fork out at least $2,000. Quite a lot too.

And here’s another interesting article: Where to invest money for a novice investor

You can view current Eurobond quotes in your Kwik using the ticker symbol of the selected security. And the bond itself is easier (and better) to study on a free service - I use, for example, www.rusbonds.ru. There you can select Russian Eurobonds, sort them according to various criteria (coupon type, yield, market sector, issue status, etc.), and also look at the cost, yield to maturity, offer date (if declared), etc.

Which is better - Eurobonds or dividend shares?

It is impossible to say unequivocally what is better - to buy dividend stocks or prefer Eurobonds. Each security has its own characteristics, so the individual needs of the investor must be taken into account.

Over a long period of time, shares generate greater income, but during a crisis their value can drop sharply. Therefore, experienced investors recommend holding both stocks and bonds in your portfolio. IOUs will generate income during a crisis, and with this money you can buy shares that have fallen in price.

When the economic situation stabilizes, stocks will rise, the investor will make money on an increase in their value, and the bonds will continue to provide a fixed income.

Taxation

What tax must be paid on Eurobonds? You must pay standard income taxes on the income received from the coupon or the difference between the purchase and sale prices. Personal income tax on Eurobonds is 13%.

For example, you bought Eurobonds for 50 thousand rubles and earned 5 thousand rubles in the form of coupons, and then sold them for 58 thousand rubles, you must pay:

- 13% of 5000 (dividends) – i.e. 650 rubles;

- 13% of 8000 (exchange difference) – i.e. 1040 rubles.

Total: 1690 rubles. You don’t need to calculate anything yourself; the broker automatically calculates and withholds taxes, both from coupons and from exchange rate differences.

Taxation of Eurobonds for individuals has its own peculiarity, which should not be forgotten – currency revaluation. The fact is that all Eurobonds are issued in foreign currencies, and taxes are paid in rubles. Therefore, it is also necessary to calculate profit in rubles.

For calculations, the exchange rates on the day of purchase/sale/coupon payment are taken. Sometimes a paradoxical situation may arise when you receive a loss in dollars, but a profit in rubles, and still have to pay tax. Or, on the contrary, there will be a profit in dollars, but a loss in rubles, and it (the loss) can be carried forward to the next tax period.

For example, you bought a Eurobond for 1010 dollars and sold it for 1020. At the same time, at the time of purchase, the dollar cost 65 rubles, and the sale cost 62 rubles. We count: 1020 * 62 – 1010 * 65 = 63,240 – 65,650 = – 2410. Despite the fact that you earned money in dollars, you incurred a loss in rubles. It can be transferred to the next year and reduce the tax base.

An example of choosing a specific security for a portfolio

Let’s imagine that a hypothetical investor with a ruble portfolio worth 1,500,000 rubles (that is, it contains shares, OFZ bonds in rubles, and deposits). The stock portfolio is diversified by industry:

The portfolio consists of more than 60% shares of Russian companies, so the investor plans to reduce the total risk by investing $20,000 in Eurobonds. The table below provides a comparative analysis of possible options from different industries for 2020:

| Industry | Denomination, $ | Coupon, % | Profitability, % per annum | |

| Lukoil | Oil | 1000 | 6,66 | 2,93 |

| Alfa Bank | Bank | 1000 | 7,75 | 2,26 |

| Norilsk Nickel | Metal | 1000 | 6,62 | 3,17 |

| OFZ2030 | — | 0,38 | 7,5 | 4,1 |

| STLC | Leasing | 1000 | 5,95 | 2,41 |

Wherein:

- Lukoil has the lowest debt burden in the industry, has government support and depends on energy prices;

- Alfa Bank is a systemically important bank and shows stable performance indicators;

- Norilsk Nickel bonds have potential for growth in value due to limited reserves of copper and palladium;

- Government Eurobonds are not subject to personal income tax;

- STLC is engaged in leasing of vehicles and equipment. Due to high tensions in the international transportation market, the value of bonds may fall. High market risk.

If there is a need for long-term investments with minimal risks, the Eurobond portfolio will be as follows:

| Issuer | Denomination, $ | Investments, $ | Portfolio share |

| Lukoil | 1000 | 4000 | 20,00% |

| Alfa Bank | 1000 | 1000 | 5,00% |

| Norilsk Nickel | 1000 | 6000 | 30,00% |

| STLC | 1000 | 1000 | 5,00% |

| Ministry of Finance | 0,38 | 8000 | 40,00% |

Let's imagine it more clearly in the diagram:

With this portfolio structure, the investor:

- Receives a weighted average portfolio return of 7.003 over a 12-month horizon (until Alfa Bank maturity);

- Reduces the risks of investing in Lukoil and State Transport Leasing Company by investing in the growing Norilsk Nickel and the stable Ministry of Finance;

- Introduces long-term investments into the portfolio structure through Eurobonds of the Ministry of Finance;

- Diversifies the total portfolio by increasing the share of investments in the raw materials industry, while reducing the total risk in the industry (Norilsk Nickel).

Using a similar principle, you can create portfolios with different levels of risk and investment terms, subordinating the investment structure to the current investment strategy.

In addition to the bonds indicated in the table, VTB perpetual securities have a high yield (8.63%), but they are associated with a high level of risk: the debt is subordinated, that is, the claims of creditors will be satisfied after investors and holders of term bonds.

In addition to Russian companies, investments in bonds of foreign issuers are possible.

The buying and selling procedure remains the same. But there are taxation nuances. Typically, income tax is paid to the country in which the borrower is located.

If we talk about risks, the main one is the risk of issuer default. To reduce risk, you should contact rating agencies for information: Moody's, JCR (Japan), Dagong Global Credit Rating (China).

Comparisons of foreign currency deposits and Eurobonds

| Parameter | Eurobonds | Currency deposits |

| Investment terms | Up to 10-15 years | Up to 5 years |

| Average yield | About 7% | About 1% |

| Early repayment | Possibly without loss | Possibly with interest losses. For deposits with the possibility of early withdrawal, the rate is lower. |

| Reinvestment | Possible (self-reinvestment) | Possibly (deposit capitalization) |

| Minimum amount | From 1000$ | Not limited |

| Tax deduction | When purchasing through IIS | No |

| Insurance | Not insured | Insured by DIA |

Below are the main parameters of the most profitable foreign currency deposits in Russian banks:

What are high yield bonds

Risks of Eurobonds

The most important risk is the issuers' failure to fulfill their obligations to repay Eurobonds or pay the next coupon. When the issuer fails to make payments, the following options are possible:

- technical default, when payment is made but with a delay;

- complete default, when the issuer goes bankrupt;

- restructuring, when the issuer defers payment while simultaneously increasing (or decreasing) the coupon.

Other risks associated with Eurobonds:

- trading – you can buy a bond at a higher price and sell it at a lower price;

- lack of liquidity – you can buy a Eurobond, but it is impossible to sell due to lack of demand;

- change in the security rating - then the bond may fall in price (but if you still hold until maturity, then this does not matter much);

- change in rates - then the yield of the Eurobond will change accordingly.

Let’s also add another risk – currency revaluation, which I wrote about above. Sometimes you can make a loss in rubles, although you will make money in foreign currency.

Risks when investing in Eurobonds

I can highlight several dangers that await an investor in Eurobonds:

- Technical default – payments are maintained, but the schedule is violated.

- Complete default is the most unpleasant thing; payments stop.

- Changes in exchange rates . Under unfavorable circumstances, income in USD may turn into a loss in rubles.

It will not be possible to completely eliminate the risks, but we can at least reduce them. I recommend excluding subordinated bonds from the portfolio - securities issued by banks.

Remember 2021, then Binbank, Promsvyazbank and Otkritie fell under reorganization. According to the current rules, if capital adequacy falls below the threshold or the DIA begins to work with a financial institution to prevent bankruptcy, then the subordination is simply written off. In theory, they could be converted into shares, but most of the subordinated bonds of the Russian Federation are non-convertible . As a result, those who invested in them simply lost their money completely. You can filter such securities on rusbonds.com and through the MICEX. Read the description of the bond and do not mess with the subords .

Where and how to buy

There are several options for how to buy Eurobonds for an individual. The first is to go directly to the exchange. You need:

- enter into an agreement with a broker;

- open a brokerage account (possibly IIS);

- place the required amount on it;

- give an order to purchase the selected Eurobond (in the QUIK terminal, through your personal account or by phone).

Each broker has its own tariffs for the purchase of Eurobonds, as well as the minimum lot size, which allows you to reduce the required amount to start. I won’t go into this now, as brokers are constantly changing conditions. Go through the websites of 4-5 of the largest brokers and choose what suits you.

Which Eurobonds to buy will depend on your investment strategy. If you don’t want to take risks, choose government ones (from the Ministry of Finance). If you want to earn more, take bank or corporate ones. You need a constant income - you need to make a choice in favor of perpetual Eurobonds.

And here is another interesting article: How to calculate the yield of a bond and what types of yield there are

You can find a complete list of Eurobonds for individuals on the Moscow Exchange website at https://www.moex.com/s729.

Here is a list of corporate Eurobonds:

And a hundred more titles. And here are government Eurobonds:

The second option is to buy a mutual fund of Eurobonds. There are quite a lot of companies offering such a tool. Eurobond funds are available from Sberbank Asset Management (OPIF RFI “Sberbank – Eurobonds”), VTB Capital Asset Management (two at once – “Eurobonds” and “Eurobonds of Emerging Markets”), Ingosstrakh, RSHB Asset Management, Otkritie, Gazprombank, Alfa Capital.

The third option is to purchase a Eurobond ETF. There is only one such fund on the Moscow Exchange - Russia-focused USD Eurobond Index (ITIEURBD Index) with the ticker RUSB from ITI Funds.

The fourth option is to buy Eurobond mutual funds. Here, too, there is only one option for now - the Moscow Exchange Index of Russian Liquid Eurobonds (RUEU10) from Sberbank Asset Management with the ticker SBCB. You can buy it directly on the MICEX.

Thus, it is easier for an individual not to buy individual Eurobonds, but to invest in mutual funds or ETFs that follow a certain Eurobond index. The threshold for entry into such funds is much lower - around 2000-5000 rubles (depending on the value of the share). And no problems with finding a foreign broker and selecting individual securities.

Investing in mutual funds

Mutual investment funds are convenient because their composition is selected by the manager. The investor can only buy shares and wait.

BCS has 2 main mutual funds, the shares of which include Eurobonds. The first is BKS Osnova , a fairly old fund, operating since 2003. The price of a unit of this mutual fund has increased by more than 400%. The management strategy is not high risk. The cost of a share starts from 50,000 rubles.

BCS Eurobonds specializes in Eurobonds and is positioned as a replacement for a foreign currency deposit. The mutual fund is young, launched in June 2021. During the pandemic, the price of the unit dropped significantly, but then a confident recovery began. There is a high entry threshold - from $15,000 per share.

BCS has other interesting mutual funds; I will give the conditions for them in tabular form.

| Name of mutual fund | The basis | Russian shares | Perspective | Russian Eurobonds | International bonds |

| Beginning of work | 26.12.2003 | 21.02.2005 | 10.05.2000 | 04.06.2019 | 04.06.2019 |

| NAV as of April 23, 2020, million rubles. | 872,07 | 506,459 | 527,129 | 138,73 | 593,314 |

| Growth of the share from its inception to 04/23/2020 | 400,34% | 454,38% | 1032,04% | 4.43% (in USD), about 20% in RUR | -4.69% (USD), increase 8.62% in RUR |

| Manager's commission | 1,5% | 3,9% | 3,9% | 1,0% | 1,5% |

| Depository fee | 0,3% | 0,3% | 0,3% | 0,5% | 0,5% |

| Minimum investment amount | 50,000 rub. first time, 10,000 rub. – second and subsequent | 1 million rub. or $15,000 | |||

| Open an account in BCS | |||||

Advantages and disadvantages

Let's summarize. What are the advantages of Eurobonds:

- a fairly wide selection of issuers - from reliable government types to riskier ones - banking and corporate;

- high yield - on average 4-5% in foreign currency;

- the opportunity to earn extra money due to the fall of the ruble;

- upon sale you will receive a tax accreditation, i.e. you will not lose the already accrued coupon income;

- you will receive a stable income - issuers pay the coupon once a year or once every six months;

- you can fix profitability for a long time - for example, for 5-10 years;

- Eurobonds are available on IIS.

Disadvantages of the tool:

- limited liquidity for a number of instruments - many are intended only for qualified investors, others are simply low-liquidity due to the nature of the offer;

- when purchasing a Eurobond on the Moscow Exchange, you will have to pay the NKD to the previous owner;

- there is a possibility of default;

- some Eurobonds are subordinated, so they can be written off if the issuer has financial problems;

- profitability may change due to political factors;

- quite high entry threshold.

To select more reliable issuers, it is recommended to look at the Eurobond ratings assigned by various rating agencies. The higher the rating, the lower the likelihood of default.

In general, Eurobonds are a very profitable and interesting instrument, but you need to know how to handle them. It is important to maintain a balance between profitability and reliability of the issuer, and also to choose a broker that allows you to enter the market with a fractional lot - otherwise the minimum purchase amount is clearly beyond the capabilities of a novice investor. In addition, if you want to make money on Eurobonds, but don’t understand it all, then you can invest in Eurobonds using funds - mutual funds, BPIF or ETF. Good luck, and may the money be with you!

Rate this article

[Total votes: 2 Average rating: 5]

Basic parameters of bonds

When evaluating Eurobonds, pay attention to the following parameters:

- Nominal cost . This is the payment that you will receive when the issuer redeems the Eurobonds. For example, for government Eurobonds rus-28 the par value is $1000. If you have 10 securities of this type, then in addition to regularly paid coupons you will also receive $1000 x 10 = $10,000 when you redeem the Eurobonds.

- maturity date – indicates when the issuer will repurchase the Eurobonds and repay the loan.

- Annual return. It is set as a percentage of the face value, for our example (rus-28) it is equal to 12.75%, that is, the holder of these Eurobonds receives $127.5 per year. Since coupons are paid out once every six months, the size of one is equal to $63.75.

- Accumulated coupon income. Shows what amount is due to the Eurobond holder as of the current date, constantly recalculated using the formula NKD = N x C x T / B. In it, N is the par value , C is the annual yield in fractions of a unit , T is the time in days since the last coupon was accrued , B is the number of days in a year . For our example, 165 days have passed since December 24, 2019 (the date of the previous coupon accrual), and the annual income is 0.1275, which means the cash flow = $1000 x 0.1275 x 165 / 365 = $57.63 . We see the same number in the description of the Eurobond; the slight difference is explained by rounding in the calculations. If the holder of the securities sold them right now, the NKD would not be lost and the money would be credited to his brokerage account.

- Coupon payment date. On this day, money is credited to the Eurobond holder's account.