Lazy Investor Blog > Stock Exchange

Today we’ll talk about a macroeconomic indicator that reflects the degree of risk in the interbank market. Beginners usually ignore it, although it is important, just like the key rate of the Central Bank. This is the Ruonia indicator - a benchmark for a conservative investor. For example, its value is a factor that determines the profitability of a number of OFZ issues. The securities linked to it are used to protect the portfolio during a crisis.

Definition of the term

The term RUONIA (also spelled Ruonia or RUONIA) is a Russified abbreviation RUONIA. The abbreviation itself comes from the abbreviation Ruble OverNight Index Average - an indicative weighted rate of one-day ruble loans issued on overnight terms on the interbank market.

In simple terms, RUONIA is the average rate at which banks issue loans to each other or take deposits overnight, i.e. overnight (from English overnight - “overnight”).

The credit risk of such borrowings is minimal, since the funds are placed in reliable banks and for an ultra-short term. The overnight debt is repaid on the next business day. An overnight deposit allows the bank to place excess liquidity, and a loan allows it to attract funds if, according to the forecasts of the analytical department, tomorrow there may not be enough money to pay clients.

Ruonia's rate is sometimes called the cost of money, since it actually shows how money increases in value over time. Therefore, together with the key rate and the rate of inflation, the RUONIA rate is decisive in the economy. And investors need to know it.

By the way, you can make money on overnight trading. How exactly - in the article about overnight VTB bonds.

OFZ-PK with reference to RUONIA. How to protect funds from inflation

There are several types of Federal Loan Bonds (OFZ) on the Russian exchange market - debt securities, the reliability of investments in which is directly ensured by the state. The most famous are the OFZ-PD issues with a fixed coupon size. However, there are OFZs with other characteristics that can also be convenient for conservative investments. Such bonds are OFZ-PK .

The abbreviation "PC" stands for "variable coupon". The OFZ coupon depends on the RUONIA rate. The higher this rate, the higher the yield on the bond, and vice versa. The current values of RUONIA can be found on the corresponding page of the official website of the Central Bank.

RUONIA (Rouble Overnight Index Average) is an indicative weighted rate of one-day ruble loans on “overnight” terms. Simply put, this is the average rate at which the largest Russian banks issue loans to each other for one day.

The OFZ-PD coupon represents a fixed percentage of the face value. For example, for OFZ 25083 bonds the coupon is 7% and does not change until maturity. For OFZ-PK the situation is different - here the coupon represents the average value of RUONIA for a certain period plus a fixed premium. When the RUONIA rate changes, the bond coupon also changes.

For example, for the issue of OFZ 29012, the coupon is determined as the average RUONIA rate for 6 months plus a premium of 0.4%. Thus, if the average RUONIA for the period is 6.8%, then the coupon on the bond will be 7.2%. If the average RUONIA rises to 7.6%, then the coupon will be equal to 8%.

The RUONIA rate is usually close to the key rate with a slight deviation of 0.5%. Currently, the key rate of the Russian Federation is 6%. At the same time, inflation as of January 2021 is below 3%. Thus, investors in OFZ-PK can receive solid returns above the inflation rate. Even if inflation rises, the key rate and the RUONIA rate will follow it, thanks to which OFZ-PK will provide reliable protection for invested funds and maintain a positive real return.

As of February 14, 2021, 8 issues of OFZ-PK were issued on the Russian market; brief characteristics are given in the table below.

Please note that for all issues except 24020 and 24021, the coupon size reacts to the RUONIA rate with a delay of six months. This means that if the bond provides for coupon payments on December 25, 2019 and June 24, 2020, then the coupon that the investor will receive on June 24, 2020 is determined based on the average RUONIA rate for 6 months before December 25, 2019. For issue 29012, this period is shifted another 2 business days ago.

Releases 24020 and 24021 are more responsive to RUONIA changes. Firstly, due to a delay of only 7 days, and secondly, due to quarterly payments.

For investors who want to effectively protect their funds from inflation with the maximum level of reliability, we can recommend considering the issues listed above to add to your portfolio.

How to make a forecast using RUONIA

In addition to OFZ-PK, the Moscow Exchange has such an instrument as futures on RUONIA. These instruments were designed to enable banks placing funds in OFZ-PK to hedge floating interest rate risk if necessary. In other words, RUONIA futures allow you to fix the yield on OFZ-PK by buying or selling these contracts.

The face value of one contract is equivalent to 1 million rubles, which makes these futures not very convenient for a private investor with a relatively small amount of capital. This tool is mostly suitable for large banks. However, based on the quotes of these futures, it is possible to build a forecast for RUONIA for the year ahead and guess what coupon for OFZ-PK can be obtained on this horizon.

There is a special page on the Moscow Exchange website that provides a forecast for RUONIA based on futures quotes. This information is posted in the section: “Quotes and expectations for the RUONIA rate.” And in the section “Coupons for OFZ floaters” you can see the expected values of coupons for some OFZ-PCs.

Conclusion

— For a conservative investor, OFZ-PK provide a good opportunity to protect their funds from inflation, regardless of its level, and to receive a small return on top of it.

— Issues 24020 and 24021 respond more quickly to changes in the RUONIA rate. Other issues react to rate changes with a six-month delay, but offer a good premium over the rate.

— RUONIA futures allow you to forecast the rate for the year ahead.

History of the indicator[edit | edit code]

Indicator development[edit | edit code]

RUONIA was developed by the Bank of Russia jointly with the National Currency Association in 2010. The development was a response to the need for prompt information about the state of the interbank market during the financial crisis of 2007-2008. RUONIA is a rate that measures the pricing conditions of the interbank market in a group of major banks. The purpose of its introduction was to create an indicator both for the Bank of Russia and for market participants who could use the rate in financial analysis and operational activities, including pricing of financial products. The creation of RUONIA became possible after the Bank of Russia introduced new daily reporting on conversion transactions and bank operations in the money markets. Daily reporting continues to be the main source of timely information on transactions in the interbank market[3].

Until 2021, the administrator of RUONIA was the SRO "National Financial Association" (until 2015 - the National Currency Association, which in 2015 was merged with the SRO "NFA"). The functions of the settlement agent and the agent for publishing the rate were performed by the Bank of Russia. Since 2021, in connection with the global reform of benchmark financial indicators, the administration of RUONIA has been transferred to the Bank of Russia[1].

Global reform of benchmark interest rates[edit | edit code]

Following investigations into the manipulation of the LIBOR benchmark interest rate, international organizations and G20 member countries decided to change financial market pricing. In 2014, a global reform was launched, which includes a revision of the methodology for creating benchmark interest rates in reserve currencies and the introduction of regulation of the activities of indicator administrators. During the reform, the widespread use of indicative rates was abandoned in favor of rates on actual transactions. Interest rates of the LIBOR family were replaced by new risk-free interest rates, the administrators of which were central banks, index companies, information and analytical agencies, and exchanges[3].

Rebirth of RUONIA

RUONIA (Ruble OverNight Index Average) is a weighted overnight rate on interbank loans in rubles. It plays a special role in Russian financial markets. The indicator is critically important, since the difference between RUONIA and the key rate reflects the effectiveness of the interest rate policy of the Bank of Russia. In addition, RUONIA has a large amount of debt tied to it. In particular, the Ministry of Finance issued government bonds (OFZ-PK) linked to RUONIA, which at the beginning of 2020 accounted for 1.7 trillion rubles, or expressed in securities. Finally, RUONIA is a mirror of the liquidity situation in the interbank market.

The RUONIA rate was developed in 2010 by the Bank of Russia and the National Monetary Association (NMA), which became its administrator. In 2015, NFA joined the National Financial Association (SRO “NFA”), to which, in connection with this, the administration of RUONIA was transferred. From May 21, 2021, RUONIA became the Bank of Russia.

RUONIA in monetary policy and financial markets

All inflation-targeting central banks engage in so-called operational money market interest rate targeting on a daily basis. Its purpose is to ensure that bet values remain within a narrow range.

The limits of the range within which fluctuations in the market rate must fit are determined by the rates of the central bank's operations to provide liquidity, that is, repos or loans, and to withdraw liquidity, that is, deposits. If the rate fluctuates within the corridor without going beyond its boundaries, this stability helps banks plan liquidity management, as well as effectively redistribute it among themselves.

The Bank of Russia is no exception: RUONIA floats within the interest rate corridor of its monetary policy. Where possible, the Central Bank seeks to reduce the deviation of RUONIA from the key rate.

RUONIA underlies the pricing of many financial products. In particular, the Ministry of Finance is the largest issuer of floating rate bonds linked to RUONIA. They protect investors from inflation and from rate volatility during periods of financial instability. RUONIA is less common in the credit market because it is not a term rate and in this regard is inferior in popularity to MosPrime. Through RUONIA interest rate risk. Ruble interest rate swaps on RUONIA in nominal volume reach about 170 billion rubles. This is less than swaps with MosPrime (471 billion rubles), but more than the key rate of the Bank of Russia (155 billion rubles).

Thus, RUONIA is a classic benchmark interest rate indicator. This is an aggregated index, references to which appear in financial contracts. Disturbances in settlement and interruption of publication of RUONIA have the potential to create systemic risk in the financial sector.

Rate RUONIA

RUONIA is calculated and published by the Bank of Russia daily based on the results of the previous working day. Interest rates on interbank transactions of each bank are weighted by volume and summed up using the arithmetic average formula. The source of initial information is the official reporting of banks on operations in the money market. The sample of banks for which RUONIA is calculated includes 35 credit institutions, both Russian and foreign subsidiaries. SRO "NFA" conducts a publication dedicated to the RUONIA indicator.

RUONIA has several interbank alternatives, and each has its own characteristics. They are either general banking sector rates (MIACR), individual market rates (RIBOR), or indicative rates (MosPrime). RUONIA is distinguished by the fact that it describes the situation among the largest banks, representing the most active part of the interbank market.

Global rate reform

Indicators similar to RUONIA, that is, OverNight Index Average - weighted average overnight interest indices - are widespread in the world. The first such indicator is considered to be the sterling SONIA, which in 1997, according to data from its members, began to be calculated by the British Wholesale Markets Brokers' Association. The family of such rates became famous after the introduction of the euro, when the European Money Market Institute (EMMI) began publishing the EONIA rate, which characterizes the cost of unsecured overnight interbank loans in euros in the countries of the European Union and the European Free Trade Association. The European Union was followed by other jurisdictions where local money markets had developed (see table).

The global reform of financial benchmarks was a turning point in the life of interest rates.

Following the LIBOR reference rate, international regulators decided to change the pricing framework in the global financial market. included a methodological revision of benchmark indicators and the introduction of specialized regulation of the activities of their administrators. During the reform, some of the administrators and the method of calculating indicators changed.

The SONIA rate has undergone a complete transformation: from an interbank rate it has become a money market rate at which banks attract overnight loans. The powers to regulate and supervise the administration of SONIA were transferred to the UK Financial Conduct Authority, and the Bank of England replaced the rate administrator from the Money Market Brokers Association.

Similar changes occurred with the NOWA benchmark rate. From 2021, administration of NOWA has moved from financial sector mega-association Finance Norway to Norges Bank, which was previously the settlement and publishing agent.

EONIA will cease to be published from 2021 and will be replaced by €STR, which is calculated by the European Central Bank based on the reports of the 50 largest banks in the eurozone. Unlike EONIA, which was an interbank rate, €STR reflects banks' borrowing costs in the unsecured money market as a whole.

In 2021, administration of Canada's CORRA rate, which measures the average overnight repo rate in Canadian dollars, moved from UK financial markets data provider Refinitiv Benchmark Services to the Bank of Canada.

Global benchmark reform has prompted the introduction of new money market rates. Thus, in 2014, the Federal Reserve Bank of New York began publishing SOFR - repo rates secured by US government securities. The Bank of Indonesia, the Central Bank of Egypt, and the Central Bank of Morocco developed and began publishing local analogues of indicators; the Bulgarian People's Bank was forced to solve the problem of low representativeness of the rate by expanding the list of contributors to all banks and branches of foreign banks in the country.

The new regulation of benchmark indicators in the European Union and the UK, which comes into full force from 2022, prohibits residents from dealing with indicators that do not comply with the new regulations. These regulations require, inter alia, that the indicator administrator be accredited by the European Union or the United Kingdom. European legislation has extraterritorial influence, and since Russian interest rates figure in cross-border derivatives, loans and bonds, global reform of financial benchmarks directly affects Russian interests.

However, European legislation makes an exception for central banks. Many took advantage of this: the vast majority of overnight risk-free benchmarks were taken over by central banks. The US Federal Reserve, the European Central Bank, the Bank of Japan, the Reserve Bank of Australia, etc. are responsible for their administration. Mostly urgent indicators remain in the hands of private administrators, represented by index companies, information and analytical agencies and exchanges.

New life RUONIA

The transfer of administration of RUONIA to the Bank of Russia is intended to solve three problems. First, ensure that RUONIA is aligned with the International Organization of Securities Commissions (IOSCO) benchmark financial indicators. Secondly, adapt RUONIA to new foreign legislation in force in leading financial centers - London, Frankfurt, Paris, etc. Compliance with international standards and norms is necessary for Russian indicators to be recognized in global markets and used in cross-border transactions. Thirdly, to ensure the operational continuity of the interest rate indicator, since decisions in situations of failure or lack of data are made by one person - now the Bank of Russia. The absence of the need for approvals speeds up decision making and allows you to quickly respond in a critical situation.

Previously, the NFA SRO determined the indicator methodology and the list of banks, and the Bank of Russia acted as a settlement agent and was responsible for publishing the rate. The new agreement between the Bank of Russia and the NFA changes the order of interaction between the parties: now the Bank of Russia is fully responsible for the administration of RUONIA - collects data, approves the methodology, calculates and publishes the indicator.

To monitor compliance with international standards, the Bank of Russia will soon form a Committee for Monitoring RUONIA, which will include representatives of the regulator and the NFA. The Expert Council of the SRO "NFA" on indicators and rates will be responsible for the work on methodological examination, analysis of critical situations and the representativeness of RUONIA and its source data, work with complaints from users of the indicator, as well as consideration of reports of the Monitoring Committee for RUONIA and the external auditor. By the end of 2021, the Bank of Russia plans to conduct an audit of RUONIA and its administration with the involvement of an international auditor. All together, this is intended to guarantee both Russian and foreign investors the high quality of the interest rate indicator on which monetary policy and the Russian government debt are oriented.

How is RUONIA calculated?

The RUONIA rate began to be calculated on July 15, 2010. The National Monetary Association (now the SRO National Fund Organization) adopted the methodology for calculating this indicator, and also proposed a list of the first banks on the basis of whose transactions the calculation was made. Since then, the list of banks has changed several times.

In accordance with the methodology, the list can contain from 25 to 35 banks, no more, no less. Now it has the maximum number of banks - 35. These are mainly large banks such as Sberbank, VTB, Alfa-Bank, Rosselkhozbank, Gazprombank, Otkritie, etc.

In general, the RUONIA value is somewhere approximately close to the key rate, sometimes exceeding it, sometimes lagging behind. According to BCS Express, over the past three years the spread (this very spread) ranged from -78 to +87 basis points, i.e. from -0.78% to +0.87%. But on average, RUONIA is ahead of the key rate by 12 points (0.12%).

Data sources[edit | edit code]

RUONIA is calculated based on the reporting data of the largest credit institutions in Form 0409701 “Report on transactions in the foreign exchange and money markets”, submitted by credit institutions to the Bank of Russia in accordance with Bank of Russia Directive No. 4927-U dated October 8, 2018 “On the list, forms and procedure for compilation and submission of reporting forms of credit institutions to the Central Bank of the Russian Federation.” The RUONIA value is published on the next business day after credit institutions carry out transactions no later than 15:00 Moscow time. The number of contributors, according to the reporting data of which RUONIA is calculated, has included three dozen credit institutions since April 27, 2020[4].

List of banks participating in the RUONIA interest rate (opening table):

Concept and mechanism of action

Overnight, in simple words, is a short-term loan or deposit, the placement period of which is usually one night. In some cases, the period may be more than one day. For example, when the day following the posting date is a non-working day (holidays, weekends). Overnight in this case is issued before the next business day.

The English word is written as overnight. Translated it means “nightly”, “from evening to all night”, “all night”, etc.

Raising and placing money is not free. In this regard, overnight is no different from regular loans and deposits. The interest rate is calculated for each day the funds are used by dividing the annual value by 365 or 366 days. Active participants in the short-term money market are the Central Bank, commercial banks, legal entities, and individual entrepreneurs.

The minimum amount limit (for example, at VTB Bank it is 1 million rubles) does not allow the practice of borrowing or placing money for one night among individuals to spread.

Complete information about current strategies that have already brought millions of passive income to investors

Mechanism of action for the enterprise:

- A company that has available funds in its accounts can place them in a one-day deposit and receive them the next day with accrued interest. The income is small, but it is better than if the money did not work at all. For example, on Friday evening a company puts a certain amount into a short-term deposit until Monday, because it still won’t make any transactions over the weekend.

- You can enter into a long-term agreement with the bank for the placement of funds. Used for frequent overnight deposits. In this case, there is no need to conclude an agreement every time; everything is done automatically, online.

- An enterprise may need a one-day loan, for example, if it needs to buy raw materials from a supplier, and the receipt of money in the account is expected only in a day. In this case, it is convenient to borrow at a small interest rate.

Overnight is often used for interbank transfers. One bank provides a loan to another. In this case, the first one earns money from the operation, and the second one solves temporary financial difficulties. Interbank transactions are under the control of the Central Bank, which itself is an overnight participant. As of February 2021, the overnight loan rate is set by the Central Bank of the Russian Federation at 7%.

How to find out the size of Ruonia

Unlike the key rate, the Ruonia indicator is not on the front pages of the media, although it is present in the news feed. You can find out its value on information sites for investors. First of all, this is the Central Bank resource cbr.ru/hd_base/ruonia/. Here you will find values that were valid in any period of interest. The information is presented in tabular form. The downside is that there is no option to download information.

Another resource is ruonia.ru. It allows you to study the chart and get a file in xls format. Both presented sites display two parameters:

- the value of Ruonia on a particular date;

- volume of overnight transactions concluded per day by participating banks.

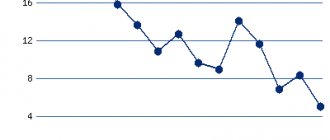

Those who are only interested in the first value can use the usual resources with stock quotes. For example, https://www.finmarket.ru/. Below is a scan of Ruonia's performance over the past year, presented on this site.

Information on the current coupon yield of OFZ linked to this indicator can be found on rusbonds.ru or on the Ministry of Finance website minfin.ru/ru/document/?id_4=1862-parametry_vypuskov_obligatsii_federalnykh_zaimov_s_peremennym_kuponnym_dokhodom_ofz-pk.

Types of overnight deals

In addition to loans and deposits, overnight transactions are practiced in the securities market. They are called repos. The bottom line is that the broker does not borrow money for one night, but securities that are stored in the client’s account. For example, to lend them to another investor.

Sberbank offers such a service. The mechanism is as follows:

- The Client agrees to the placement of free securities by submitting a special Order.

- The bank sells the securities it received from the client at the price of the last trade of the trading day on the stock exchange.

- The next day, Sberbank buys exactly the same amount of securities at the sale price the day before.

- The bank returns the client's securities with an accrual of 2% annual yield. In this case, a transaction fee of 0.001% of the amount is charged.

The period may be more than one day if overnight falls during non-trading sessions of the exchange.

There are the following types of overnight:

- Standard. A loan or deposit is issued to a separate legal entity or individual.

- Corporate. Issued for a group of companies. The algorithm is presented on the VTB website.

Administration[edit | edit code]

In 2021, the Bank of Russia moved from performing the functions of a settlement agent and publishing agent to full-function administration of RUONIA. Administration of RUONIA by the Bank of Russia ensures the solution of three tasks[5]:

- RUONIA's compliance with the International Organization of Securities Commissions' Principles of Financial Benchmarks;

- adaptation of the Russian financial market with minimal costs to the requirements of the legislation of the European Union and Great Britain on financial indicators ( EU Benchmark Regulation

); - complete operational continuity of RUONIA.

The operational tasks of the Bank of Russia as the administrator of RUONIA include[5]:

- methodological support for the administration of RUONIA;

- collection and preparation of data related to RUONIA;

- RUONIA calculation;

- publication RUONIA;

- storage of data related to RUONIA;

- internal audit of RUONIA administration;

- handling requests;

- interaction of the Bank of Russia with the SRO “National Financial Association”;

- interaction with international organizations.

Monitoring the implementation of international requirements in the Bank of Russia is the responsibility of the RUONIA Supervision Committee[6].

Composition of the RUONIA Interest Rate Monitoring Committee (disclosed table):

| Full name | Position (representation) |

| Yudaeva K.V. | first deputy Chairman of the Bank of Russia (Chairman of the Committee) |

| Ivanova N. S. | Advisor to the First Deputy Chairman of the Bank of Russia |

| Moiseev S. R. | Advisor to the First Deputy Chairman of the Bank of Russia |

| Melnikova I. A. | deputy Director of the Department for Strategic Development of the Financial Market |

| Mukhlynov R.V. | deputy Director of the Department for Combating Unfair Practices |

| Shevchuk I. V. | Head of the Financial Markets Risk and Stress Testing Department of the Financial Stability Department |

| Zablotsky V.V. | President of SRO "National Financial Association" |

| Gorlinsky O. Yu. | representative of SRO "National Financial Association" |

Advantages and disadvantages

Benefits of overnight deals:

- The ability to make money work around the clock and generate income even on weekends and holidays.

- With a one-day loan, a company can receive funds to conclude a profitable contract, and a bank can solve financial problems.

- Minimum number of documents. Possibility to conclude a long-term contract and automate the process.

- You can place funds in any currency, but interbank transfers are carried out only in rubles.

- There is no limit on the maximum placement amount.

Flaws:

- Rates on overnight deposits are significantly lower than on long-term deposits and are revised daily depending on the market situation.

- There is a minimum amount limit.

- There is no insurance for funds in overnight deposits, and overnight securities transactions are not insured against broker bankruptcy.

Where to see the current bet value

To see the current RUONIA rate or, for example, the RUONIA rate for 6 months, you can use the official website of the SRO NFA, where this very value is published: ruonia.ru. However, this site often lies down.

Therefore, the second option for viewing the required indicator is the website of the Central Bank of the Russian Federation, namely the page https://www.cbr.ru/hd_base/ruonia. All the necessary information, including the rate archive, can be viewed there.

For example, this is what the statistics look like for the last two weeks of April 2021.

Users[edit | edit code]

RUONIA is a price standard, that is, a percentage indicator, the comparison of the values of which allows you to analyze the cost of other financial instruments, assess the state of the credit or debt markets, as well as their individual segments. A distinctive feature of a reference interest rate is that it is referenced by other financial instruments. The main users of RUONIA are the Bank of Russia and the Government of the Russian Federation. RUONIA participates in targeting interest rates of the Bank of Russia in the interbank market. The operational goal of the Bank of Russia's monetary policy is to maintain interbank market interest rates close to the Bank of Russia key rate. Along with other interest rate indicators, the difference between RUONIA and the key rate of the Bank of Russia reflects the effectiveness of the Bank of Russia in achieving its operational goal. The Ministry of Finance issues federal loan bonds with the coupon value pegged to RUONIA, and the Federal Treasury pegs the cost of placing temporarily free budget funds to RUONIA. RUONIA can be used in the pricing of other financial instruments, including corporate loans and bonds, as well as mortgages. RUONIA is primarily used in pricing derivatives markets to hedge interest rate risk[2].

What is RUONIA used for?

OK then. We understood what RUONIA is. This is the rate at which banks lend to each other in order to speculate on Western stock markets at night to remove excess liquidity.

But why should an investor know the meaning of RUONIA of the Central Bank of the Russian Federation and how to use this knowledge in our everyday investor life? For example, to determine the normal dividend yield on shares. If the dividend yield is higher than the RUONIA rate, then this stock is not only profitable, but also has increased risks. If it is lower, it means that the stock is not so profitable, you need to look for more profitable options.

But, naturally, you need to compare the yield with RUONIA wisely. If a company traditionally pays low dividends but is stable, then it can be included in your portfolio. If the dividends are each time significantly higher than the market, but the stock itself does not tend to “catch up” to the “price minus dividends” quote, then something is wrong here. For some reason, investors don't want to buy it. We need to analyze the stock more closely.

In addition, RUONIA is directly related to the key rate of the Central Bank of the Russian Federation. Let me remind you that the key rate is used by the Central Bank to regulate the level of inflation (in fact, there are many purposes - but this is the most basic). And this is also the rate at which the Central Bank lends to commercial banks, providing them with liquidity.

If RUONIA is below the key rate, then the largest banks have additional money in reserve. If RUONIA is higher, then there is not enough money. How to use it - think for yourself.

How to analyze the meaning of Ruonia

Ruonia plays a significant role for Russian investors not because it determines the coupons of several bonds. Its main task is to reflect the current liquidity situation.

When assessing this indicator, first of all you need to compare it with the key rate of the Central Bank. If Ruonia is below this value, we can conclude that banks have free money that they are willing to place at a lower interest rate. If the key rate is lower than Ruonia, this means that the financial sector is faced with a lack of funds for lending. A sharp increase in this macroeconomic indicator is considered a sign of crisis.

Beginners may decide that mutual lending by banks does not concern them. Many people think that if they do not use Ruonia-linked investment instruments, then they do not need to track this indicator. In fact, the level of liquidity directly affects the situation in the stock market. A striking example is the crisis of March 2021 and the actions of the Federal Reserve aimed at overcoming it.

The American regulator has taken a number of unprecedented measures to stabilize the stock market. Among them are a sharp reduction in rates, a program for purchasing securities, as well as an injection of cheap money into the economy. The latter was achieved by providing banks with short-term loans (analogous to Ruonia) for $1.5 trillion. The Russian Central Bank also did not stand aside. To maintain the current level of liquidity, 500 billion rubles were allocated. Thanks to this move, Ruonia did not exceed the key rate in March 2021.

Why is GO so low?

This can be easily understood by simply calculating how much you will lose if the bet goes against your direction. Let's say you bought a July contract with a built-in rate of 4.25%. Suddenly the economic situation worsened and rates rose to 5.25%. That is, the contract value changed from 95.75 to 94.75 (100-5.25).

Your loss was: 100 steps x -8.21 ruble cost per step = -821 ruble or -50% of the GO. Considering the cost of the entire contract (1 million rubles), one can understand that this is not a lot compared to other instruments.

Now let's think about what is the probability of such an event occurring? If you analyze changes in RUONIA over the entire period, you will notice that for most of its history it changed smoothly by 0.25-1% per month. Therefore, in the event of an unfavorable change in the rate, one could always have time to close the position before more serious losses.

Of course, there was a case in history when one could lose everything and even more with such an instrument, but at that time it did not exist. Moreover, such a sharp increase in the indicator in December 2014 was preceded by a long structural change in the economy. From July to December 2014, the price of oil fell almost twice from 106 to 57 dollars per barrel. Knowing how much the Russian economy depends on oil prices, only an avid gambler would buy RUONIA futures in December.

RUONIA and OFZ

RUONIA is even more important for those investors who actively invest in bonds. The fact is that there are government bonds on the market with a floating interest rate - they are designated as OFZ-PK. The coupon income for them is tied to the current RUONIA rate. That is, RUONIA + some meaning.

For example, according to OFZ-24019-PK, coupon rates are determined as the arithmetic average of the RUONIA rate for the last 6 months + 0.3 percentage points.

By the way, such bonds are called floaters - from the English float - “to float” (because the coupon is “floating”).

In total, there are 8 such issues on the Russian market. All of them with their characteristics are provided on the screen.

Enlarged version:

The size of the next coupon payment on floaters is determined using the same method: the arithmetic average of the RUONIA rate for the last 6 months is taken, then a certain value (fixed premium) is added to it.

Purchasing such a bond allows you to fix income for up to six months, and what will happen next is unclear. Thus, the yield of such bonds reacts to changes in interest rates with a delay of six months.

This seems like a disadvantage, but that's why investors buy floaters - it protects them from sudden changes in rates. Unlike bonds with a constant coupon, the market value of OFZ-PK does not sag so much when the rate rises (why the price of a bond changes when the key rate changes is explained in this article). Consequently, even if the rate rises sharply, the OFZ-PK portfolio will not lose as much weight as the OFZ-PD portfolio.

Massive demand for OFZs with a variable coupon linked to the RUONIA rate began after the 2014 crisis. In 2015-2016, the volume of investment in floaters increased by 46%.

Today, when there are no prerequisites for easing the credit and financial policy of the Central Bank of the Russian Federation, investors are again becoming interested in instruments with a mechanism for insuring against changes in rates.

Even more information about OFZs tied to Ruonia is in this incredibly useful manual from Otkritie: OFZs - RUONIA.

So, RUONIA is the rate at which banks issue loans to each other overnight, i.e. for the night. Overnight lending allows liquidity to be distributed more intelligently in the banking system. An investor needs to know the value of RUONIA in order to compare dividend yield, inflation rate and key rate with it. Ruonia is also used as a basis for calculating the coupon yield on OFZs with a variable coupon. Now you know a little more about economics. Good luck, and may the money be with you!

Rate this article

[Total votes: 3 Average rating: 5]

What is Ruonia

Ruonia is an indicator showing how much an unsecured ruble loan costs for a Russian bank with a high credit rating. It was first introduced in July 2010. In November 2015, the calculation methodology was revised. Since then it has remained unchanged. This value is established on the basis of overnight transactions, but is expressed as a percentage per annum.

The term "overnight" means that the loan is provided for a period of one night. It will be fully refunded the next business day.

The Ruonia indicator is sometimes called the cost of money. Its value is quite close to the key rate. Experts note that on average it deviates by 0.12%. The maximum difference does not exceed 1%.

The value of Ruonia is calculated by the Bank of Russia every working day. As initial data, it uses information about transactions that were concluded between the participating banks in the settlement. This list may include from 25 to 35 largest players in the financial market. Their composition is regularly reviewed by the National Financial Association together with the Central Bank. News about its changes are published on the website https://ruonia.ru.

Along with the key rate, Ruonia is one of the leading economic indicators. Based on this indicator, the value of the OFZ-PK floating coupon is determined. In general, the calculation is carried out using the following formula:

where Coupon is the value in percent per annum that will be valid during the next period.

I also recommend reading:

How does the additional issue of shares affect quotes?

Additional issue of shares: what to expect?

n – the number of calendar days over the last 6 months, excluding the date on which the calculation is made.

Ruoniai – the value of the Ruonia bet on each day. For weekends and holidays, the value recorded the day before is used.

spread is an arbitrary value established by the terms of the bond issue. For existing issues it ranges from 0.4% to 1.6%. The value for each specific type of OFZ-PK can be found in the bond card on the website rusbonds.ru.

In total, 8 issues of federal loan bonds with a variable coupon are traded on the Moscow Exchange. All of them are linked to the Ruonia indicator. Such a tool is considered a means of protection against changes in rates. Its popularity grew sharply after the events of 2014-2015. This is due to the fact that during periods of crisis such bonds not only provide a higher coupon income, but also practically do not lose value, unlike OFZ-PD with constant income.

Experienced investors can use not only bonds, but also derivatives to diversify interest rate risk. There are 12 Ruonia futures available on the Moscow Exchange derivatives section.

There is no such direct connection between dividends and Ruonia. However, if a company shows a dividend yield below this indicator, it is unlikely to be of interest to a wide range of private investors. Only traders who expect to win due to price increases can add securities of this issuer to their portfolio.

Literature[edit | edit code]

- Alyokhina O.

Methodological issues in the analysis of the interbank credit market // Banking. — 2012. — No. 10. — p. 14-19. - Moiseev S.

The second birth of RUONIA (Russian) // Econs.online. — 2020a. — May 25. - Moiseev S.

Consequences of the reform of benchmark interest rates // Economic Issues, 2021. - No. 1. - p. 93-110. - Moiseev S.

Reincarnation of RUONIA, or the Second Life of the Interest Indicator (Russian) // Banking. — 2020b. — July (No. 7). - P. 18-25. - Fedorenko I.

Is the RUONIA rate protected from manipulation: calculation method // Money and Credit, 2012. - No. 9. - p. 62-70.