Securities are documents that secure rights to certain property and allow various transactions with it. They are drawn up in a strictly established form and have mandatory details. The most common types of securities are stocks, bills, bonds and checks. Thanks to such certified documents, the management of material or other benefits is simplified. Such transactions are called securities transactions.

In Russia, these issues are regulated by various regulatory documents:

- Chapter 7 of the Civil Code of the Russian Federation, dedicated to securities and their description.

- Federal Law No. 39, which describes specific rules for regulating the securities market.

- Federal Law No. 208, regulating the activities of joint stock companies.

During purchase and sale transactions or gratuitous transfer of securities, a transfer of property rights to real estate and debt obligations occurs from one person to another. The issuer (holder) of securities acts as a seller, and the investor acts as a buyer in the market.

Types of transactions

Classification according to the characteristics of a transaction with securities:

- urgent;

- unlimited;

- cash;

- combined;

- over-the-counter;

- repo contracts.

Urgent

Urgent transactions with securities require the determination of specific deadlines for the execution and termination of the transaction.

They are necessary primarily for obtaining short-term profits or for hedging long-term assets during periods of unstable situation in the financial markets, with the accompanying increased risks.

Indefinite

Perpetual transactions for the purchase/sale of assets on the stock market do not imply specific timing in the matter of execution and termination of the transaction, but regulate only the prices and volume of assets that participate in it. For example, buying 100 shares of a company at 100 rubles per share.

Cash

Cash (Spot) transactions in the market are transactions with the Central Bank on the stock market in real time with current execution.

Depending on their focus, they can be:

- Purchase (Long).

- Sale (Short) - a participant can not only sell the instruments that he has, but also use borrowed stock instruments in order to buy them back cheaper in the future, and make money on this action.

Can also be divided into two types using:

- own funds;

- borrowed funds (leverage).

Combined

Combined or rollover transactions with securities are those that, in their structure, combine elements of both cash and forward transactions in relation to one exchange asset. Those. Initially, a fixed-term instrument is purchased in order to obtain speculative profit, but after the contract expires, for some reason, a decision is made to extend the agreement.

OTC

Over-the-counter transactions involve the exclusion of intermediaries and stock exchange regulators from the chain.

However, other financial intermediaries, for example, a broker or bank, may be involved in organizing trade. Or, a transaction to buy/sell securities can be made directly with the counterparty of the transaction.

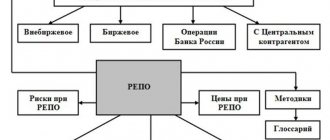

Repo contracts

Repos involve the provision of borrowed funds to a market participant for a limited period, secured by its stock assets.

Such contracts provide the opportunity to open Long/Short positions on securities, but establish an obligation to perform a reverse transaction after a certain period.

Registrants

The functions of the registrar are somewhat similar to the functions of the depository. It also records and stores information about the current owners of securities. Only for the depositary the starting point is a specific investor (owner of securities) and he opens a deposit account for each of them, and for the registrar - the issuing company with the register of which (which) he works.

The securities register is a collection of information that includes information about the owners of securities, their nominal holders and the encumbrances imposed on them. It includes data on the number and category of securities owned by each shareholder of the company. Can be stored both electronically and in paper form.

Among other things, the responsibilities of the registrar include:

- Accounting for incoming/outgoing documentation (usually in the form of a journal);

- Maintaining personal accounts of all persons registered in the register;

- Accounting of all operations performed (also in the form of a journal);

- Accounting for securities certificates;

- Accounting and storage of all documentation that served as the basis for making changes to the register.

According to the laws of our country, issuers of securities do not have the right to independently maintain their register (in accordance with the provisions of Federal Law No. 142-FZ of July 2, 2013). Therefore, professional registrars (as registrars are sometimes called) who have the appropriate license from the Central Bank of the Russian Federation are quite popular participants in the domestic securities market.

Deal implementation stages

Concluding transactions for the purchase/sale of stock assets includes many nuances, therefore the construction of the transaction process and recording its result is divided into several successive stages:

- submitting a client request;

- conclusion of an agreement;

- verification of parameters;

- clearing settlements;

- delivery of a security in exchange for cash payment.

Further details about each of these stages.

Client application order for a transaction

Any operations for the purchase/sale of securities begin with the submission of an order by market participants.

A client application is the provision of information about the investor’s desire to complete a transaction under certain conditions.

Applications are:

- Market, providing for the purchase/sale of a security at the nearest possible price.

- Limited, indicating a specific price at which a market participant is ready to complete a transaction.

However, regardless of whether the order is a market order or a limit order, it must contain the following information:

- identification code, information about the client and broker;

- type of order - buy or sell;

- stock instrument ticker;

- volume;

- period of execution.

Make a deal

This stage represents the conclusion of a security purchase/sale agreement between the two parties to the agreement.

At this moment, the date of conclusion of the agreement is recorded on the exchange, but the owner of the stock instrument receives a complete list of all rights only on the date of the actual transaction after recording information about this register.

It is determined by the formula “T + n”, where

T is the trading day on which the contract was concluded;

n is the number of business days after which the transaction is completely completed and all rights are transferred to the new holder of the securities.

Reconciliation of the parameters of the concluded transaction

This stage is necessary to eliminate or minimize the possibility of committing a technical error, as a result of which an agreement will be concluded that does not meet the agreed conditions of market participants.

Clearing

Clearing settlements are a reconciliation of parameters that establishes the fact of the mutual ability of the parties to purchase/sell securities on the specified conditions.

The complete clearing process includes the following steps:

- checking the relevance and correctness of transaction parameters;

- calculating and monitoring the availability of financial capacity to complete a transaction;

- formation of document flow, sending information to the settlement center.

Delivery of a security in exchange for cash payment

This is the final stage at which the netting and final execution of the transaction occurs, involving the transfer of securities and funds between the accounts of the counterparties to the transaction.

For example, the Moscow Exchange operates in the “T+2” mode (trading day + 2 business days). This means that the date of the final exchange and transfer of property rights will be set two trading sessions after the conclusion of the agreement for the purchase/sale of securities.

What can you buy on the stock market?

Each participant can independently determine which financial market instruments can be used for trading. They are presented in several types. In order to decide, you can read the news of the stock market and get acquainted with which instruments are most in demand, and with the help of which of them you can currently make successful transactions.

On the stock market you can make transactions on the following types of instruments:

- options

- stock

- bonds

- futures

Stock

Shares are a type of securities, when purchased, a person makes a contribution to the capital of the company. It is equal to the cost of one share. After completing the transaction, he has the right to receive part of the company's income. By owning 50 percent of the shares of one of the companies, a person has the opportunity to have the right to half of its profits.

Bonds

Bonds represent obligations. Thanks to such a valuable document, a financial market participant has the opportunity to receive a cash payment from the company (issuer) upon presentation. Such securities can be issued either by the state or by private or public companies.

Options

When trading various instruments, market participants make their own assumptions about how the price of a particular financial instrument may change. Then the option is purchased at a certain price. Forex trading robots allow you to automate similar work on the stock exchange, creating almost passive income for their owners. “Almost” means that it is still necessary to monitor the robots, modify them and change algorithms depending on the market situation. In order to successfully trade options represented by foreign exchange instruments, for example, you can study financial markets and exchange rates.

Futures

Futures are obligations between parties in which one of them is obliged to transfer another commodity at a certain value.

Types of forward transactions

Urgent ones can be divided into the following categories:

- Simple (forward) - counterparties enter into a regular forward agreement for the purchase/sale of an asset indicating a specific date and price. Such transactions are carried out outside organized exchanges.

- A futures contract is a derivative financial instrument, the terms of which regulate the delivery or settlement of an underlying asset in the future, but at a pre-agreed price. Such contracts are traded on the exchange.

- An option is a derivative financial instrument that implies the right (but not the obligation) to buy/sell an underlying asset under pre-agreed conditions during a specified period in the future.

Cash and forward transactions schemes

Cash transactions involve a fairly simple settlement structure. It is based on the following actions:

- payment for securities;

- transfer of assets.

In the case of an urgent transaction, the scheme becomes a little more complicated and takes the following form:

- A request is generated to the seller of the asset.

- A contract is concluded, which specifies all the necessary parameters and urgency characteristics for the execution of the contract.

- After a certain date, final delivery and settlement of assets occurs.

Treaties and taxes

The agreement is concluded for both the purchase and sale of an asset. Tax obligations relate only to the seller and only to the amount of profit received by him in the calculation of the difference between the price at which he previously acquired this asset and the value established in the current contract.

In Russia, individuals who receive profit from such transactions must pay 13% personal income tax to the tax service. But other tax jurisdictions may have different tax conditions and rates.

If transactions for the purchase/sale of securities take place through the services of a financial intermediary in the form of a brokerage company, then the market participant, as a rule, does not need to personally fill out and submit a tax return, since the financial agent will do this for him.

In trading through an organized exchange, the tax on profits from stock transactions is not levied on an instant basis, but tends to be amortized, i.e. decrease in case of losses from subsequent transactions.

Taxation of transactions with securities in banks

Regardless of whether the services of a bank, broker are used, or a transaction is carried out to sell securities directly to the final counterparty of the transaction, individuals must pay a standard 13% personal income tax rate on profits from these transactions.

Taxes and repurchase agreements

The main thing to consider when calculating taxable income on repo transactions is the fact that there is a double sale, but there is only one actual transaction, so only the income received by the original borrower will be taxed.

Depositories

After you make a purchase of securities on the stock exchange, you will not receive a knock at the door from a courier wearing a jacket with the inscription “Moscow Exchange” and a bunch of purchased shares in his hands. Because, firstly, most securities are currently issued in book-entry form (not on paper, but in electronic form), and secondly, the securities you purchased will be stored in the databases of special organizations called depositories.

Although, even if you bought securities presented on paper (documentary form), you would not have to put them in neat piles in your home or bank safe. After all, for this purpose, again, there is a depository, which also deals with the storage of documentary securities (such as, for example, deposit and savings certificates or bills).

In addition to recording and storing information about the current owners of securities, the functions of depositories also include:

- Mediation in the payment of dividends;

- Mediation in terms of exercising the rights of the owner of securities (for example, his participation in general meetings of shareholders).

Thanks to depositories, there is no need to enter information about each new shareholder into the register of shareholders. All this information is recorded in the depository and transferred to the issuer only when necessary, for example, before the next cutoff in connection with the payment of dividends.