olegas Dec 18, 2021 / 269 Views

One well-known futures trader said that if several traders have the same level of income at the end of the year, the Sharpe ratio shows which of them achieved it due to their skill (advantages in the market), and which by taking too high risks. Obviously, the bet should be on the first ones, on those who achieve results while maintaining an acceptable level of risk, solely due to their trading skills. Since it is clear that high risks, sooner or later, lead to significant losses (often to the complete loss of the deposit).

In a nutshell, the Sharpe ratio shows how much profit a trader receives per unit of risk.

First, just a little history. This coefficient was first published in 1966 thanks to the efforts of the future Nobel laureate William Sharp (he would receive his Nobel Prize 44 years later for developing a model for valuing capital assets, CAPM).

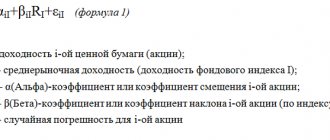

Sharpe ratio calculation formula

Where:

rp – average return of a mutual fund (investment portfolio);

rf – average return of a risk-free asset;

σp – standard deviation of returns on assets of a mutual investment fund (investment portfolio risk).

Let's take a closer look at how to calculate each of the formula indicators.

| ★ Excel spreadsheet for creating an investment portfolio of securities (calculate the portfolio in 1 minute) + assessment of risk and return |

| ★ InvestRatio program - calculation of all investment ratios in Excel in 5 minutes (calculation of Sharpe, Sortino, Treynor, Kalmar, Modiglanca beta, VaR ratios) + forecasting rate movements |

Standard deviation

The Sharpe ratio measures the performance of an investment in terms of the dispersion of returns. Since we have already calculated the excess return (return minus the risk-free rate), all that remains is to divide this value by the standard deviation of the asset's return. That is, calculate the ratio of return to risk.

Although this is no longer required today, it is still easy to calculate the standard deviation manually. Let's say you have collected small statistics on the profitability of transactions: 3%, 4%, 5%, 2%, 1%. At the first stage, we subtract the average from this sequence and get the following series: 0%, 1%, 2%, -1%, -2%.

Next, we square the values, get the arithmetic mean and derive the root of the result - sqrt((0.00% + 0.01% + 0.04% + 0.01% + 0.04%) / 5) = 1.41%.

For comparison, let's take a slightly different sample: 2%, 8%, 5%, 4%, 6%. Obviously, the profitability of such a system within the period under review is greater, but we also observe much greater volatility of profitability, 2% versus 1.41% for the previous example. Accordingly, the first strategy is less risky.

Calculation of the return on a risk-free asset

To assess the excess return that an investor received, it is necessary to calculate the minimum possible return that he could receive by investing in absolutely reliable assets. It is the excess return that reflects the quality of management and the effectiveness of decisions made by the manager of a mutual investment fund.

There are several ways to estimate the return on a risk-free asset:

- Profitability of bank deposits of the largest and most reliable banks in the Russian Federation. Such banks include Sberbank, Alfa Bank, VTB 24.

- The yield of risk-free government securities (GKOs, OFZs in Russia, 10-year bonds for the USA), which have the highest possible reliability according to the ratings of the international rating agencies Moody's, Standard&poor's and Fitch.

As a result, it is necessary to compare the profitability obtained by managing risky securities and the minimum level of profitability of an absolutely reliable asset.

Take our proprietary course on choosing stocks on the stock market → training course

Mutual Fund Valuation by Sharpe Ratio

The Sharpe ratio estimate is presented in the table below. For example, if the indicator is greater than one, it means the level of excess return is higher than the existing risk of the fund or investment portfolio. Evaluating the indicator allows you to select the most investment-attractive funds, portfolios or investment strategies.

| Indicator value | Management effectiveness assessment |

| Sharp ratio >1 | High performance in mutual fund or portfolio management. This fund is attractive for investment |

| 1>Sharp ratio >0 | The level of risk is higher than the excess return of a mutual fund. It is necessary to consider other indicators of the fund’s investment attractiveness |

| Sharp ratio <0 | The level of excess return is negative, it is more advisable to invest in a risk-free asset with a minimal level of risk |

| Sharp ratio1 > Sharp ratio2 | The first mutual fund is more attractive for investment than the second |

Conclusion

In most cases, the Sharpe ratio will show the true profitability of the strategy. But sometimes the Sharpe ratio can be misleading. For example, some bonds may show stable returns above the bank interest rate for many years, to which the ratio will respond with unrealistically high rates. In this case, the resulting value will say nothing about the real risks behind investing in a given bond, even if the risk is actually minimal. In general, this coefficient is suitable for comparing two strategies with relatively frequent entries and not the most huge goals.

Best regards, Alexey Vergunov TradeLikeaPro.ru

An example of choosing a mutual fund based on the Sharpe ratio

Information about existing funds can be obtained on the website nlu.ru (national league of managers). We go to the website and select the “ANALYTICS” section. → “Ratio” → “Sharpe Ratio”. The system has the ability to filter funds by various parameters: by type, by management company, by category and date.

Valuation of Mutual Funds Based on Sharpe Ratio

The figure below will reflect the ranking of all mutual funds by Sharpe ratio. Thus, the REGION Equity Fund fund has the maximum value of the Sharpe ratio, which indicates a high quality of management.

Evaluation of mutual funds based on their management efficiency

An example of estimating the Sharpe ratio for an investment portfolio

If you are creating an investment portfolio yourself and you need to compare different portfolios of securities, then to do this you need to get quotes for changes in all shares included in the portfolio, calculate their profitability and the overall risk of the portfolio. Let's take a closer look at an example of calculating the Sharpe ratio in Excel.

You can get quotes from the website finam.ru in the section “About the market” → “Data export”. Let's take a portfolio of three shares: OJSC Gazprom, OJSC MMC Norilsk Nickel and OJSC Sberbank. For each stock, we will estimate the share in the total portfolio, so for Gazprom - 0.3, GMK Nor. Nickel – 0.5 and Sberbank – 02. For the analysis, quotes were taken during the year from 01/31/2014 – 01/31/2015.

Calculating the Sharpe ratio for an investment portfolio in Excel

The next step is to calculate the yield for each security in the portfolio. To do this, we will use the formula in Excel:

Gazprom stock return =LN(B7/B6)

MMC share return Norm. Nickel =LN(C7/C6)

Sberbank share return =LN(D7/D6)

Assessing the return on investment portfolio shares

Next, you need to calculate the parameters of the coefficient: profitability and risk of the portfolio as a whole, as well as estimate the risk-free return. The portfolio return is the weighted sum of the arithmetic average daily returns, the portfolio risk is equal to the weighted sum of the standard deviations of stock returns.

Take our proprietary course on choosing stocks on the stock market → training course

The risk-free yield was taken as the annual interest rate on a bank deposit and is 12%. We will use the following evaluation formulas:

Portfolio return = AVERAGE(E7:E256)*B4+AVERAGE(F7:F256)*C4+AVERAGE(G7:G256)*D4

Portfolio risk =STDEV(E7:E256)*B4+STDEV(F7:F256)*C4+STDEV(G7:G256)*D4

Sharpe ratio =(H7-J7)/I7

Assessing the effectiveness of an investment portfolio using the Sharpe ratio

As we see the value of the Sharpe indicator is negative, this indicates that this investment portfolio is not formed correctly and should be reconsidered. The return on the risk-free asset turned out to be higher than the return on the shares itself. It was more appropriate for an investor to invest in a risk-free asset rather than actively manage and bear additional risks. You can learn more about the coefficients for assessing the effectiveness of investments in the article: “Assessing the effectiveness of investments, investment portfolio, shares using an example in Excel.”

Risk-free income

Risk-free income is a theoretical income with zero risk. That is, this is the return that an investor can receive absolutely without risk for a certain period of time. In theory, this is the minimum income that an investor expects to receive from any investment. By comparing this figure with actual income, you can determine how well compensated you are getting for the additional risk.

In practice, the concept of a zero-risk investment does not exist, since even the safest investments carry with them some degree of risk. However, risk-free returns include a deposit in a savings bank or money invested in US Treasury bonds. The Forex market is always a high-risk investment, so the risk-free return in our case will be zero. But, if your deposit is kept in a bank, you can substitute the value of the current base rate into the formula.

In the MT4 terminal, the Sharpe index is calculated as the ratio of the arithmetic average return of a transaction to the standard deviation, with a zero risk-free rate.

The full formula looks like this:

Modified Sharpe ratio

The classic Sharpe ratio has a number of disadvantages, which are solved in its modification. Modification of the indicator mainly affects the change in the risk assessment of the investment portfolio. To assess risk, not only standard deviation is used as a measure of portfolio return variability, but a modified VaR (Value at Risk) risk measure. This measure allows you to estimate future losses more realistically by assessing the nature of the distribution of historical stock returns. Its calculation formula is as follows:

where: rp – average return on the investment portfolio; rf – average return of a risk-free asset; σp – standard deviation of investment portfolio returns; S – kurtosis of the distribution of returns; zc – kurtosis of the distribution of portfolio returns; K – quantile of the distribution of returns.

Risk assessment in this model is based solely on statistical calculations, which allows for a more adequate assessment of the risks of an investment portfolio or mutual fund.

| ★ InvestRatio program - calculation of all investment ratios in Excel in 5 minutes (calculation of Sharpe, Sortino, Treynor, Kalmar, Modiglanca beta, VaR ratios) + forecasting rate movements |

Comparison of Sharpe's Ex-Ante and Ex-Post

One of the benefits of the Sharpe ratio is flexibility in choosing the type of performance data to enter into your calculations.

On the one hand, the Sharpe ratio can be used to evaluate the past performance of an investment or portfolio. In this case, actual earnings are used in the formula.

This Sharpe ratio is called "Ex-Post". The term "Ex-Post" means "after the fact." Such a Sharpe ratio can be further used to predict future returns from investment choices with sufficient past data.

In the case of an investment or portfolio without adequate historical performance data, an investor may use expected performance to calculate what is known as the Sharpe Ex-Ante Ratio.

The term "Ex-Ante" means "before the fact" and this Sharpe ratio is based on estimates and/or forecast performance.

Where is the Sharpe ratio applied?

One of the areas of application of the Sharpe ratio is to compare and evaluate the effectiveness of investment portfolios, Funds (ETFs, REITs, etc.), and trading strategies. It is not wise to compare investment portfolios only by the profitability received or only by the risk (losses). Therefore, to determine performance, an integral indicator is used, including profitability and risk. The higher the Sharpe ratio, the more effective the investment portfolio.

You can simulate a portfolio using the portfoliovisualizer.com service. To do this, let's take the shares of the Big Four: Apple (APPL), Google (GOOG), Amazon (AMZN), Facebook (FB). We will create the first portfolio without optimizing stock weights. Each stock will have an equal weight of 25%. We optimize the second portfolio to maximize the Sharpe ratio.

Maximizing the Sharpe ratio allows you to find the optimal shares of shares in the portfolio

The weights of shares in the optimized portfolio will change ↓

| Ticker | Name | New briefcase weight |

| AMZN | Amazon. | 44.29% |

| GOOG | Alphabet | 5.43% |

| FB | 27.11% | |

| AAPL | Apple | 23.18% |

The table below shows the returns and risks for the 10th period. As we can see, despite a slight increase in portfolio volatility, profitability is higher.

| Briefcase | Profitability over 10 years | Risk (average volatility) | Sharpe ratio |

| Portfolio with equal weights | 840% | 20,8% | 3,06 |

| Optimized portfolio | 1030% | 22,6% | 3,20 |

Our portfolios have a Sharpe ratio greater than 3, which means that the selected stocks can generate returns 3 times higher than the risks (expressed in volatility).

The figure below shows the dynamics of the profitability of the first and second portfolios.

Portfolio optimization based on the Sharpe ratio allows you to rebalance the portfolio and increase profit with a slight increase in risk

Relativity of calculations and results

Of course, the Sharpe ratio quite clearly illustrates the potential and risks. But at the same time, there are cases when these figures will not adequately show the real state of affairs and will not provide entirely correct information, which will ultimately lead to the loss of great earning opportunities.

Let's consider two simple cases that can be called ordinary and which are often found in Forex and other financial markets:

- There is a trader who works intraday, uses huge leverage and the deposit swings quite strongly in both directions. If you look at the final result for the month, it can be tens and sometimes hundreds of percent. This is especially common among cryptocurrency lovers, when they manage to catch a powerful movement, as well as on volatile cross-pairs of the foreign exchange market, they can run 500 points a day. That is, the result looks amazing, but in reality we understand that such trading will not be infinitely successful, sooner or later the deposit of such a scalper is lost. This happens for one simple reason - if we use the deposit in full, then we can earn as many points as we want, but the drain will always be through a fixed value. For the eurodollar it will be about 110-120 points with a leverage of 1:100. This approach of working “for everything” is practiced by many. The Sharpe ratio will be very high and will show the real picture.

- There is a trader who really knows a lot, knows how to trade and works on a huge number of instruments at once, but with small lots. It is often practiced to build trend pyramids, that is, as you move in the right direction, you will get a constantly growing profit, but open orders are transferred to breakeven. And so on for many instruments at once. Stops are short, breakeven if possible, but profit is retained to maximum values.

What do we get in this case? The Sharpe ratio will still be high due to high profitability, but the risks are actually completely different . Such a trader is not in danger of losing money; his working approach is completely different, which involves quickly fixing a small loss. And due to skills, huge distances are taken according to the trend. If you look at the statement, there will be 70-80% of unprofitable and zero (break-even) transactions, but profitable ones will be tens of times larger in size.

So it turns out that two identical situations in terms of income and Sharpe ratio, but how different everything is in real life. That is why you should not look at numbers alone, you also need to pay attention to details and study history, look at many more indicators. This is well illustrated by PAMM services, where you can study account indicators in detail before investing - what the maximum drawdown was, what the yield curve looks like, and so on. All this will allow you to make the right decision and not invest in an account that could be lost tomorrow.