- VEON reported weak results, somewhat in line with market expectations. Revenue and EBITDA were below the consensus forecast by 2.8% and 2.6%, respectively.

- The main unpleasant surprise was the potential cancellation of dividends for 2021, which, in our opinion, could disappoint investors.

- However, we believe the weak 2021 performance is reflected in the company's valuation, which trades at an EV/EBITDA multiple of 3.5x versus MTS's 5.2x.

- In the long term, the Group remains optimistic about its growth opportunities, given the ongoing 4G rollout programme. As for the Russian business, Veon expects to see the first signs of a turnaround in 1H21.

Important points

Revenue in 2Q20 decreased by 16.3% YoY to $1.89 billion – 2.8% below consensus estimates

. The group's revenue was impacted by a high base effect due to special compensation of $38 million received in 2Q19, as well as exchange rate dynamics of $178 million during the quarter and quarantine measures in the markets where VEON operates. Organic revenue fell 6.9%, partially offset by a 14.4% increase in organic mobile data revenue, while organic mobile and fixed-line revenue declined 5.7%. In all markets except Ukraine and Kazakhstan, the dynamics of revenue in local currency turned out to be negative.

EBITDA fell 18.7% YoY to $809 million, missing consensus by 2.6%

. Pressure was exerted by unfavorable changes in foreign exchange rates ($178 million), special compensation in 2Q19 and negative revenue dynamics. Despite revenue pressures, effective cost management (the Group's structural operating expenses fell by 15% YoY in 2Q20) enabled it to demonstrate a strong EBITDA margin in 2Q20, which amounted to 42.7% versus 43.9% in 1Q20. Organic EBITDA decreased by 11.2%.

Operating capex, excluding licenses, reached $492 million, an increase of 9.3%

YoY from $450 million in 2Q19, mainly due to investments in 4G networks.

Forecast

. The group has revised its forecast for 2021 - the company expects a stable recovery in results in 2H20 and a decline in organic revenue within a few percent of both revenue and EBITDA. The intensity of capex should be 22-24%. The revised forecast assumes a recovery in the Group's performance in 2H20, taking into account the gradual easing of quarantine measures in all VEON markets. The outlook for the Russian segment in 3Q20 remains unclear (according to VEON), but the Group expects to see early signs of improved business activity in 1H21 given continued network investments and other support measures.

Dividends

. Under its current dividend policy, VEON aims to pay out at least 50% of equity free cash flow (EFCF) after licensing expenses, while maintaining a 12M net debt to EBITDA ratio of 2.0x. In 1H20, EFCF after license expenses reached $68 million (vs. $600 million in 1H19), while net debt to 12M EBITDA was 2.2x. With this situation, there is some uncertainty in the 2H20 plan. Veon reported that the cancellation of dividends for 2021 is very likely.

Important indicators of the Russian division

Revenue for 2Q20 decreased by 9.7% YoY to RUB 65.5 billion

. Revenue was negatively impacted by the dynamics of revenue from mobile services (-9.8%), reflecting a sharp drop in revenue from roaming (by almost 90% in the quarter) and a significant contraction in the subscriber base (-8.4% y-o-y), partially offset by growth in revenue from fixed-line services (+8.9% y/y). As a result, ARPU decreased by 4.6% to RUB 332. Revenue from sales of equipment and accessories fell by 29.2% YoY. The reduction in the subscriber base was the result of temporary store closures and a significant reduction in the migrating subscriber base (-56% in 2Q20).

EBITDA in 2Q20 decreased by 20% YoY, amounting to RUB 25.7 billion

. The dynamics of EBITDA are primarily due to a decrease in revenue as a result of the introduction of restrictive measures, as well as higher structural costs due to increased costs for maintaining and operating the network and increased costs for interconnection due to the increased share of inter-network traffic. The decline in EBITDA was partially offset by a number of cost optimization initiatives. EBITDA margin amounted to 39.3% (versus 44.3% in 2Q19).

VEON: cancellation of dividends will not affect debt burden

VEON (ВВ+/-/ВВВ-) published results for the 2nd quarter. 2021 and reinstated its 2021 guidance previously withdrawn due to uncertainty due to the global coronavirus pandemic. The holding's management announced a waiver of dividends, however, according to our estimates, this will not significantly change the debt burden. VEON's revenue declined in Q2. 2021 by 16% y/y in dollar terms and by 7% y/y. excluding exchange rate fluctuations and one-time effects, and the EBITDA decline was 19% year-on-year. and 8% y/y, respectively. General trends amid the introduction of quarantine around the world include a drop in roaming income to almost zero, the closure of communication stores and, as a result, a decrease in revenue from sales of phones and equipment and the outflow of the subscriber base, as well as a decrease in the migrant user base. These effects were most noticeable in Russia, where the decline in revenue and EBITDA in rubles was 10% and 3%, respectively. At the same time, a positive effect under quarantine conditions was the acceleration of revenue growth from fixed-line communication services, which, however, constitute a small share of the holding’s total revenue.

Ukraine and Kazakhstan were the only markets where there was an increase in revenue and EBITDA in local currencies due to less saturation of the market with high-speed mobile Internet services. In addition, VEON provides fixed access services in both of these markets, which also supported financial performance.

Debt load in Q2 2021 increased to 2.0x Net debt/EBITDA excluding leasing obligations, or 2.2x including them, compared to 1.8x/2.0x as of the end of Q1. 2021 The growth was driven by both deteriorating operating performance and the devaluation of the currencies of VEON's operating countries, since even despite hedging, dollar debt accounts for 47% of the group's total debt. According to management, aligning the currency structure of debt and revenue is one of the priorities in the current environment, along with reducing overall costs and extending borrowing terms.

Based on the results of Q2. 2021 VEON renewed guidance for 2021, withdrawn after 1Q. 2021 due to uncertainty at the peak of the coronavirus pandemic. In the current environment, VEON management expects revenue and EBITDA to decline by 1-6% y/y. in local currencies and forecasts the ratio of operating capex (excluding licenses and leasing) to revenue at 22-24%. Taking into account this forecast and the continued uncertainty regarding the further development of the pandemic, as well as possible M&A transactions, VEON management announced its intention not to pay dividends for 2021. According to our estimates, even taking this into account, free cash flow for 2021 will be range of 0-150 million dollars, which will not significantly change the debt burden relative to the level of 2Q. 2021

In the Eurobond market, credit spreads remain widened: for VEON issues by 50-60 bp. wider than at the beginning of the year, however, in absolute terms, yields have already returned to the levels at the beginning of the year (due to a significant decrease in UST yields). VEON securities, in our opinion, are not of interest for purchase; the best alternative to them are sovereign bonds of the Russian Federation. Also, in the segment of riskier securities (issuers with increased debt loads), we continue to recommend POGLN 22 bonds in conditions of favorable conditions on the gold market.

VEON spoke about a new dividend policy and strategy with a focus on know-how

Telecommunications holding VEON presented shareholders on Tuesday a new development strategy and specified its dividend policy, promising to pay shareholders at least 50% of free cash flow from 2021. VEON also raised its forecast for EBITDA dynamics. If earlier the company expected growth in the indicator “from low to mid-single digits” (that is, from 1-3% to 4-6%), now it is “at least mid-single digits” (that is, there is at least 4-6%). “VEON is performing well relative to its targets for the current year,” said holding CEO Ursula Burns.

Strategy The updated VEON strategy includes three vectors: “communications”, “new services” and “future assets”. As Alex Kazbegi, the company's vice president for strategy, said during Capital markets day, the strategy is similar to a pyramid, at the base of which lies the company's fundamental business - providing and developing communications, and in the middle - digital transformation of business. The top of the pyramid will be the acquisition of assets and the development of know-how, while this area will become the driver of growth in the company’s profitability in the long term.

The first step in implementing the “future assets” strategy will be to increase investment in digital financial services in Pakistan (the first asset of the newly created VEON Ventures division). Top management did not disclose details of further plans for the development of this area, noting only that investments in it could amount to tens or hundreds of millions of dollars.

Ursula Burns also said that the company has successful experience in creating its own assets (digital financial assets of Pakistan and Russian Beeline-TV), so the issue of investments outside the holding needs to be carefully considered.

VEON operates in 10 countries (Russia, Ukraine, Pakistan, Algeria, Bangladesh, Uzbekistan, Kazakhstan, Kyrgyzstan, Armenia and Georgia) and divides its assets into 3 clusters. The Russian VimpelCom is the “cornerstone” of the entire VEON; the second direction includes Ukraine, Pakistan, Uzbekistan and Kazakhstan. The third cluster contains the remaining countries that VEON classifies as emerging markets.

Dividends The company also presented a dividend policy, which will come into effect from next year. If previously VEON adhered only to the wording “stable and progressive dividends based on the dynamics of free cash flow,” now the company has clarified: at least 50% of FCF (Free Cash Flow, free cash flow) will be allocated for dividends after deducting the cost of paying for licenses .

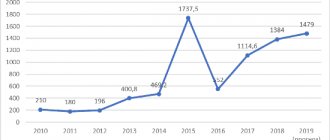

At the end of 2021, the company forecasts FCF at $1 billion. FCF at the end of the first half of 2021 amounted to $795 million (or $630 million excluding IFRS-16), but even taking into account the good results of the first half of the year, VEON did not increase the forecast for the indicator, expecting more difficult second half of the year.

In 2021, VEON paid out $0.29 per share. The company's interim dividend for 2021 was $0.13 per share. As Kazbegi noted, the final dividends for the current year will be announced in February, when the company sums up the results of 2021, they will be calculated from the current policy.

At the same time, Xtellus analysts believe that the new dividend policy, along with the company's plans to invest in an updated strategy, may negatively affect investor income. During the conference, analysts expressed concerns that dividends for 2021 may be lower than previous periods.

Pakistan VEON also announced that it may exercise a put option to buy out a minority stake in Pakistani operator Warid. “We have to make a decision (on the option) next year,” the vice president of strategy said.

According to VEON's 2021 annual report, the holding has the right to exercise the option beginning July 1, 2021 from Pakistan Mobile Communications Limited (Mobilink) "at fair market price."

As reported, at the end of 2015, the Pakistani operator Mobilink (now Jazz), controlled by VEON, agreed to purchase 100% of the shares of competitor Warid. The owners of Warid - shareholders of the Dhabi Group - received 15% of Mobilink. It was then reported that 4 years after the closing of the transaction, the put option of Dhabi Group shareholders to sell their shares in Vimpelcom (formerly VEON) and the call option of the latter would come into force.

Pakistan, together with Ukraine, Kazakhstan and Uzbekistan, are defined by the holding as a cluster of “growth engines”. The Pakistani asset is currently part of GTH, a subsidiary of VEON, but will be integrated into VEON itself to simplify the corporate structure.

The Pakistani business provides a significant increase in revenue for VEON: organically, business income grew in the first half of 2019 by 22% year-on-year, EBITDA organically increased by 24.2%. Further growth of the operator is facilitated by the fairly low penetration of smartphones in the country (about 37% according to VEON), as well as continued investment in the network - both expansion and upgrade of the current one.

News / May 2020Wireless • ReportsVeon upset analysts

In Russia, VimpelCom (Beeline brand) attributes the drop in revenue to roaming, the closure of some communication stores (34% of its own offices and 25% of franchise stores) and the outflow of subscribers represented by migrant workers amid the coronavirus. Service revenue of the Russian division in the mobile segment decreased by 4.4% to RUB 52.5 billion. According to the operator, due to a decrease in revenue from international roaming and the negative impact of the prevalence of unlimited tariffs. “This decline was partially offset by a 7.2% increase in fixed revenue for the same period. As a result of challenges related to the competitive situation in the market, the level of efficiency of our retail network, as well as a decrease in the number of migrants in the base in the first quarter of 2021, the company’s subscriber base decreased by 1.4% compared to the same period last year,” - VimpelCom said in a statement.

The company estimates that significant growth in mobile data and revenue from mobile financial services was not enough to offset the decline in revenue from voice and SMS services. Revenue from sales of equipment and accessories in the last quarter decreased by 1.7% year on year. VimpelCom tried to partially compensate for these losses with a higher volume of shipments to the dealer network.

“In dollar terms, all the main financial metrics of Veon showed a decline, including under the influence of unfavorable changes in exchange rates in the countries of presence,” observes Veles Capital analyst Artem Mikhailin. In local currencies, revenue growth was close to zero. The negative effect of the spread of coronavirus and the strengthening of quarantine measures in the world has partially manifested itself. The holding's assets in Ukraine, Kazakhstan and Bangladesh showed positive growth dynamics in local currencies, while divisions in Russia, Pakistan, Algeria and Uzbekistan showed negative growth dynamics. “The holding’s EBITDA was under pressure due to the high base effect, since in the first quarter of last year Veon received an additional $350 million from the revision of the contract with Ericsson, and the adjusted figure decreased by 3% year-on-year in foreign currency,” notes a representative of Veles Capital. .

Amid the uncertainty of the coronavirus and the economic crisis, the operator withdrew financial forecasts for 2021 and reported that in April it recorded a decline in revenue of 7-9% year-on-year and EBITDA of 14-16% year-on-year in local currencies.

Freedom Finance analyst Valery Emelyanov believes that VimpelCom’s data for Russia “looks moderately negative.” According to him, the decline in revenue by 2.6% occurred under pressure from the mobile segment - and this was unexpected. The main burden fell on operators to provide communications to that part of the economy that now exists outside of offices. “Despite the growth in traffic, the company was unable to convert this into sales growth, which is partly due to the predominance of unlimited tariffs in the Beeline product line, as well as unsuccessful positioning and weak marketing,” Valery Emelyanov is sure.

The analyst notes that the reduction in the subscriber base has become a stable trend for Beeline. In this quarter, the net outflow amounted to 700 thousand customers, of which 500 thousand were in the mobile Internet segment, which shows the lag behind competitors in the development of high-speed communication channels. “The positive part is that ARPU continues to grow faster than inflation. Although this may partly cause the outflow of the client base, adds Valery Emelyanov. — The broadband segment also shows positive dynamics, both in terms of the number of clients and in terms of revenue. However, this is a niche story, and it accounts for a small part of the turnover. Formally, the indicators are depressing,” said Finam analyst Leonid Delitsyn. This includes a decrease in revenue, EBITDA, and the number of mobile Internet clients (by 2.2%). In addition, ARPU and MOU decreased simultaneously. “Although market players are now thinking that the telecom industry is going through the pandemic easily compared to others and is expecting a quick recovery and new business opportunities, this is keeping shares from falling sharply,” says the Finam expert. In his opinion, growth in revenue in the fixed segment (by 8.6%), including revenue from broadband access (by 6.2%) and an increase in the number of clients (by 8.5%) may mean the beginning of a trend of accelerated development of the segment due to for the mass transition to remote work.

According to the forecasts of surveyed analysts, the second quarter will be difficult for Beeline: a sharp decline in sales of SIM cards and gadgets due to the closure of retail in April and May may accelerate the contraction of the subscriber base and the decline in revenue. Experts expect that the revenue of all operators will decline in the B2B sector, and telecoms will more actively look for growth drivers in IT services, including in partnership projects with the largest IT companies.